Market Trends of Japan Data Center Construction Industry

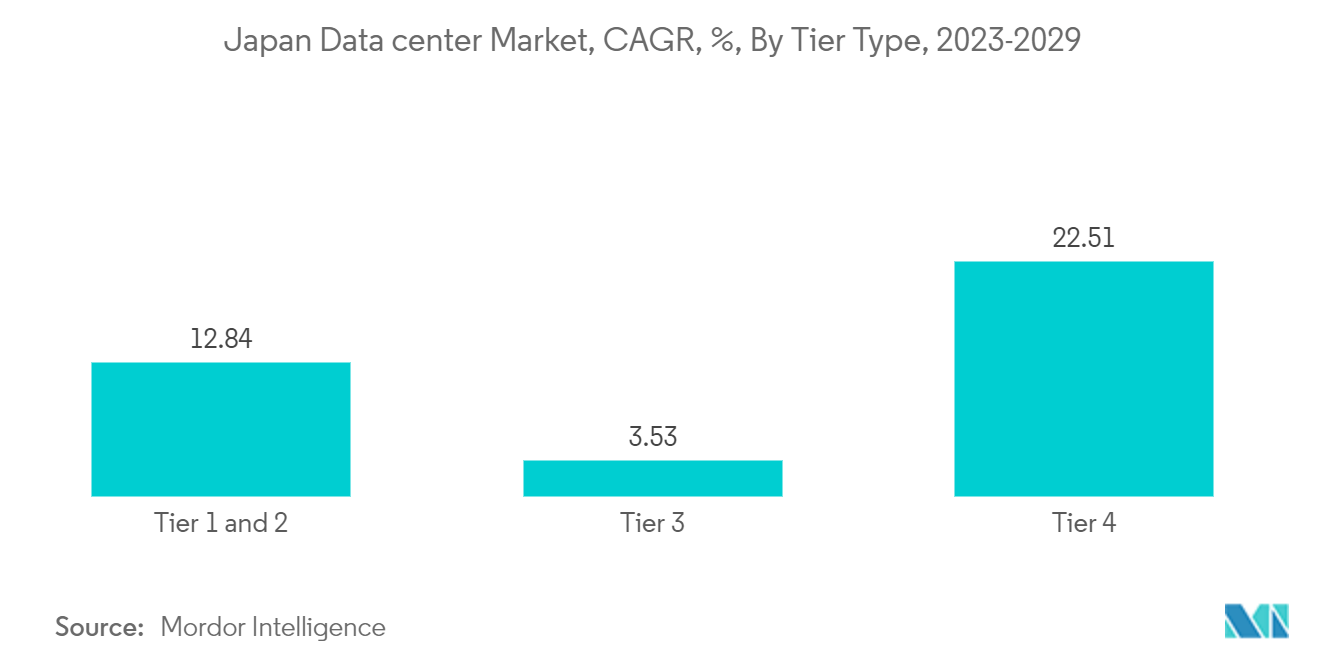

Tier 3 is the largest Tier Type

- Tier-3 data centers are mostly preferred by SMBs (small and medium businesses) for their far superior redundancy protection offerings. There is a significant jump in uptime from tier-2, with tier-3 offering annual uptime of 99.982%. The segment is expected to grow from 1,300 MW in 2022 to over 1,900 MW by 2029, registering a CAGR of 5.51%. These data centers are mainly opted for by large companies.

- Tier-4 facilities are large businesses' next most preferred data centers due to their performance, lower downtime, and 99.99% uptime. However, most facilities still prefer tier-3 data centers due to their long-term financial and operational sustainability. Tier 3 is the most widely adopted standard across the industry. However, the growth rate for tier-4 facilities is expected to be the largest.

- Tier-1 & tier-2 data centers are the least preferred due to their higher downtime durations and low redundancies, but start-up companies usually prefer these data centers. However, in Japan, start-up companies also prefer tier-3 data center facilities. Currently, in Japan, there are no facilities certified with Tier 1 and Tier 2, and this trend is expected to continue during the forecast period.

Understand The Key Trends Shaping This Market

Download Sample

Hyperscale data centers growing popularity among large enterprises

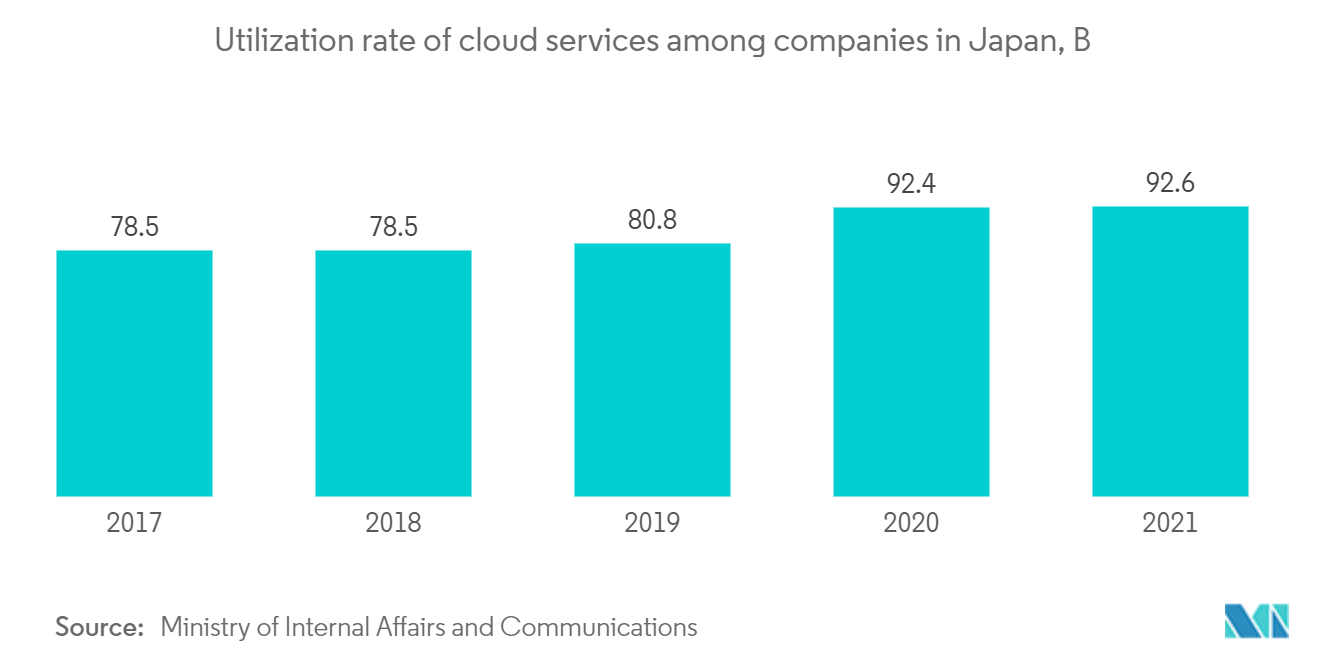

- Hyperscale data center facilities in the Japanese market reached an IT load capacity of 432.9 MW in 2022. The growing cloud penetration in the country is driving constructions to the hyperscale data center market. According to the Ministry of Internal Affairs and Communications, the telecommunication industry utilized the highest cloud services in 2021, resulting in greater dependency on hyperscale data centers.

- Hyperscale data centers are expected to overtake retail colocation to accommodate higher-density needs from hyperscale platforms. Hyperscale data centers (HSDCs) are concentrated mainly in Inzai City in Chiba and the western region of Tokyo in the Kanto area. The Kansai region is located in Osaka city center and the northeastern parts of Osaka prefecture, including the Saito area.

- A global data center vendor invested an initial amount into tens of billions of Japanese yen in the Tokyo metropolitan region for one block of a hyperscale data center it constructed. The entire project is rumored to be in excess of JPY 100 billion (USD 687.6 million). The source funding for this project came from Asian sovereign wealth funds, and a joint venture between the global DC vendor and a Japanese company is expected to be in charge of its operations.

- Such development points to the globalization of the DC business, and such projects are becoming investment targets as REITs. The demand for connectivity in data centers is expected to continue, including from cloud vendors. Leveraging favorable locations to construct hyperscale data centers will continue with major real estate companies entering the business.