Market Overview

| Study Period | 2020 - 2030 |

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

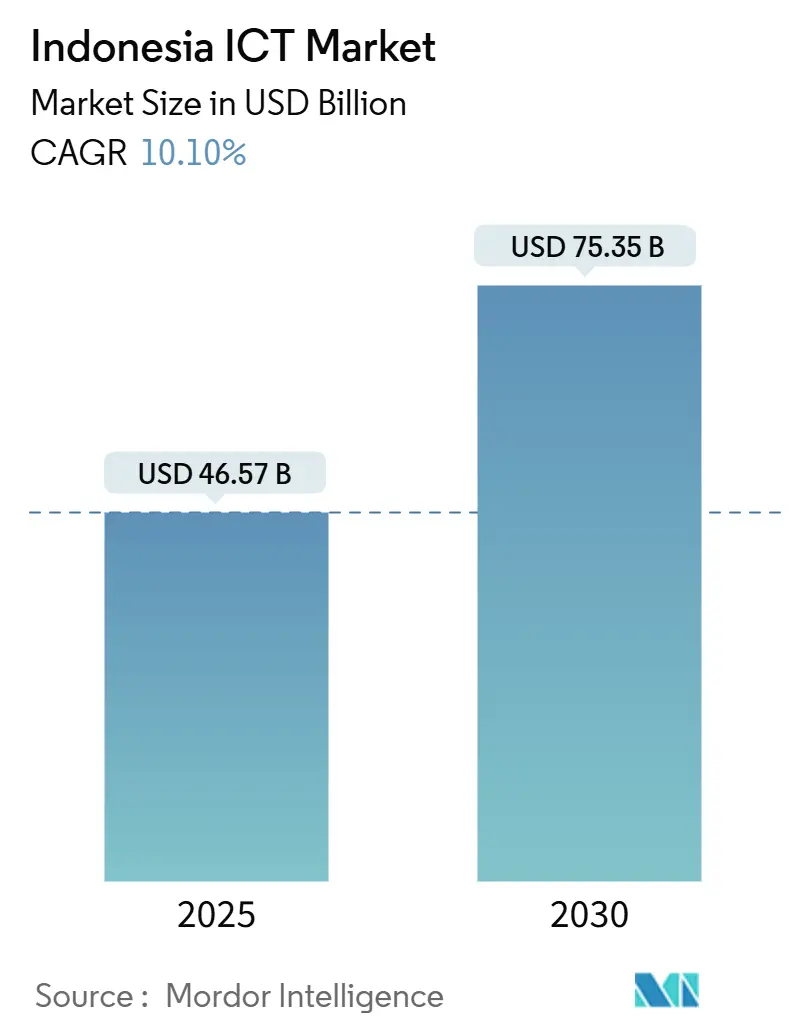

| Market Size (2025) | USD 46.57 Billion |

| Market Size (2030) | USD 75.35 Billion |

| Growth Rate (2025 - 2030) | 10.10% CAGR |

| Market Concentration | Low |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Indonesia ICT Market Analysis by Mordor Intelligence

The Indonesia ICT Market size is estimated at USD 46.57 billion in 2025, and is expected to reach USD 75.35 billion by 2030, at a CAGR of 10.10% during the forecast period (2025-2030). Sustained economic expansion, an ambitious Golden Indonesia 2045 agenda and the completion of critical connectivity assets such as the Palapa Ring and SATRIA-1 satellite underpin this outlook, widening high-speed coverage across more than 17,000 islands. Hardware remains the revenue anchor, but rapid enterprise digitalisation, accelerating e-commerce adoption and sovereign AI programmes are pivoting budgets toward cloud, analytics and cybersecurity solutions. International hyperscalers and local telecom operators continue to inject multi-billion-dollar capital into data-centre clusters, while small-business demand for scalable SaaS services intensifies following nationwide QR-based payment uptake. At the same time, the rupiah’s volatility, new 12% VAT and tighter local-content rules heighten cost pressures for import-dependent vendors, reinforcing the need for flexible pricing and local manufacturing strategies.

Key Report Takeaways

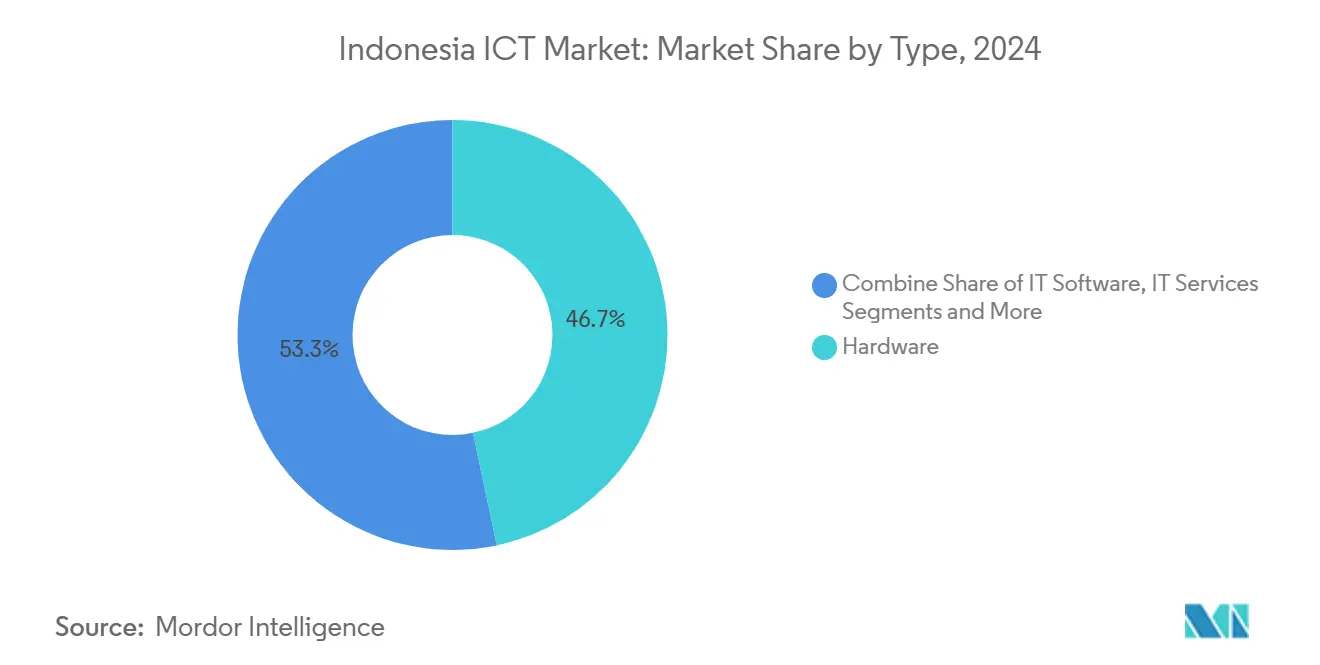

- By type, hardware led with 46.7% revenue in 2024, whereas IT security posted the fastest 13.2% CAGR through 2030.

- By enterprise size, large enterprises held 71.8% of the Indonesian ICT market share in 2024; SMEs are projected to expand at a 12.1% CAGR to 2030.

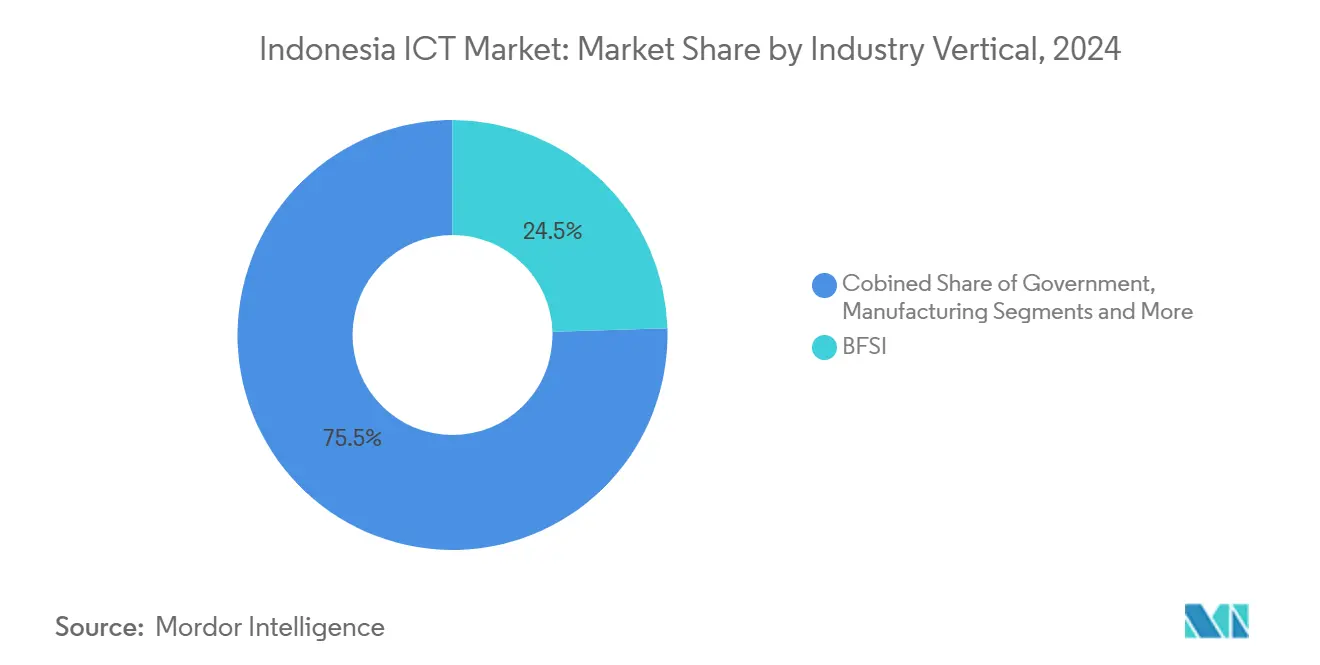

- By industry vertical, BFSI captured 24.5% revenue in 2024, while retail & e-commerce is advancing at a 14.3% CAGR to 2030.

- By technology, cloud computing commanded 39.0% of the Indonesian ICT market size in 2024; AI & analytics is growing the fastest at 14.2% CAGR.

- By region, Java controlled 63.0% of 2024 revenue; Papua presents the quickest 16.0% CAGR outlook to 2030.

Indonesia ICT Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Digital transformation of Indonesian enterprises | +2.8% | National, with concentration in Java and Sumatra | Medium term (2-4 years) |

| Government digital-skills & infrastructure push | +2.1% | National, prioritizing eastern regions including Papua and Sulawesi | Long term (≥4 years) |

| E-commerce boom spurring online payments | +1.9% | National, with urban concentration in Java and Bali | Short term (≤2 years) |

| Palapa Ring & SATRIA-1 satellite roll-out | +1.5% | National, with emphasis on remote areas | Medium term (2-4 years) |

| Shift to “green” data-centres amid high power tariffs | +1.2% | Java and Sumatra industrial corridors | Long term (≥4 years) |

Source: Mordor Intelligence

Digital Transformation of Indonesian Enterprises

A growing share of manufacturers and banks now pilot artificial-intelligence workloads: 62% of firms in these verticals tested AI use-cases during 2024.[1]IBM, “Indonesia Leans Into AI,” asean.newsroom.ibm.com Flagship projects such as Bank Rakyat Indonesia’s BRIVOLUTION and PT Pegadaian’s infrastructure overhaul trimmed product launch cycles by up to twentyfold while holding strict compliance thresholds. Energy-intensive manufacturers that deployed compressor-optimisation tools reported an 8.5% drop in electricity consumption, proving immediate ROI and encouraging broader uptake azbil.com. This transformation wave fuels sustained demand for cloud platforms, secure networks and real-time analytics across the Indonesian ICT market.

Government Digital-Skills & Infrastructure Push

The state plans IDR 47,587.3 trillion in infrastructure outlays for 2025-2029, with large allocations for connectivity corridors and human-capital programmes.[2]PT Sarana Multi Infrastruktur, “Driving Sustainable Growth Through Infrastructure Financing,” ptsmi.co.id Microsoft’s USD 1.7 billion pledge adds training for 840,000 citizens, directly backing the Golden Indonesia 2045 roadmap. Completed roads such as the 1,042 km Trans-Sumatra toll accelerate logistics and push cloud and IoT deployments into secondary cities trabas.co. The policy mix scales broadband and talent simultaneously, raising the Indonesian ICT market’s long-term growth ceiling.

E-commerce Boom Spurring Online Payments

Indonesia’s online-retail receipts are set to hit USD 82 billion in 2025, doubling sectoral share of total retail to 21.8% by 2027.[3]Investor.id, “E-commerce to Reach USD 82 Billion,” investor.id The central bank’s QRIS system processed a record jump in micro-merchant transactions, pushing SMEs toward formalised digital channels. Social-commerce uptake reached 69% of shoppers before policy shifts curtailed some live-stream platforms, underscoring both demand momentum and regulatory volatility. Rising payment volume translates into heightened calls for fraud-management, API orchestration and scalable cloud gateways across the Indonesian ICT market.

Palapa Ring & SATRIA-1 Satellite Roll-out

Nationwide fibre backbones now interlink 514 districts, while SATRIA-1 adds 150 Gbps of Ka-band capacity for 93,000 public-service sites. Eastern provinces, led by Gorontalo, posted the sharpest digital-competitiveness gains after infrastructure went live. Operators quickly leverage the new backhaul to pilot AI-enhanced RAN features, with Indosat Ooredoo Hutchison setting a regional first in collaboration with Nokia and NVIDIA. Better coverage elevates cloud adoption and IoT sensor roll-outs, especially in education, healthcare and public-safety projects across the Indonesian ICT market.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Data-privacy & cyber-security concerns | -1.8% | National, with heightened focus in financial and government sectors | Short term (≤2 years) |

| Shortage of advanced ICT talent | -1.4% | National, most acute in Java and emerging tech hubs | Medium term (2-4 years) |

| Local-content (TKDN) rules inflate hardware costs | -1.1% | National, with manufacturing concentration in Java | Long term (≥4 years) |

Source: Mordor Intelligence

Data-Privacy & Cyber-Security Concerns

A sharp rise in digital payments and personal-data processing exposes systemic vulnerabilities. Forty percent of enterprises still report immature governance frameworks that slow AI deployment. Telco-grade firewall upgrades delivered by Lintasarta drove false-positive rates down to 5%, demonstrating effective mitigations but at growing cost.[4]Palo Alto Networks, “Lintasarta Deployment Case,” paloaltonetworks.com The evolving privacy law and forthcoming ethical-AI guidelines compel larger budgets for identity management, encryption and regulatory audit solutions, tempering short-term margins across the Indonesian ICT market.

Shortage of Advanced ICT Talent

Indonesia needs an estimated 9 million additional digital specialists to meet 2030 objectives. Electronics and software firms struggle to hire cloud architects, data scientists and OT cyber-engineers, inflating wage bills and elongating delivery cycles. Public-private training schemes, including Huawei’s USD 50 million pledge for 100,000 talents, help but the gap persists. Persistent scarcity pushes service providers to automate low-complexity tasks and reinforce offshore development hubs, moderating near-term velocity in the Indonesian ICT market.

Segment Analysis

By Type: Hardware Leads Despite Security Acceleration

The segment captured 46.7% of 2024 revenue as telecom operators upgraded transport networks and enterprises refreshed servers and storage to support cloud migration. Local-content rules inflated component costs, yet domestic assemblers that met TKDN thresholds gained share amid import hurdles. Cyber-security spending, though smaller in absolute terms, is scaling fastest at 13.2% CAGR as boards elevate risk oversight and regulators impose stricter compliance. Managed-security-service demand therefore rises, creating bundled propositions that blend hardware, software and 24/7 threat monitoring across the Indonesian ICT market.

Service lines such as IT outsourcing and data-centre colocation also expand, aided by more than USD 1 billion of fresh capacity from Tencent, Microsoft and Korean joint ventures. Communications services show modest revenue erosion as voice continues its secular decline but are partially offset by 5G-enabled enterprise solutions. The resulting portfolio mix keeps hardware dominant, yet value migrates quickly toward software and service wrappers that monetise installed equipment throughout the Indonesian ICT market.

Note: Segment shares of all individual segments available upon report purchase

By Enterprise Size: SME Growth Outpaces Corporate Dominance

Large organisations retained 71.8% revenue share in 2024 owing to deep pockets and complex multi-cloud roll-outs that demand premium support. Nonetheless, SMEs are projected to post a 12.1% CAGR through 2030, out-running corporate growth as SaaS models lower entry barriers. Payment-system interoperability through QRIS lets micro-merchants accept low-cost digital transactions, nudging them toward inventory-management apps, online storefronts and basic cyber-hygiene tools.

Government programmes that target a 40% GDP contribution from SMEs further catalyse adoption, offering subsidised licences and cloud credits. Vendors increasingly create stripped-down bundles that match SME workflows, from payroll automation to omnichannel marketing suites. Such tailored propositions enlarge the Indonesian ICT market size for smaller buyers without eroding enterprise-grade revenue streams.

By Industry Vertical: Fintech Drives BFSI Leadership

Financial services held 24.5% of 2024 spend as incumbent banks digitised core systems, expanded mobile onboarding and fortified fraud analytics. Fintech challengers sharpened the urgency, pushing incumbents to modernise governance and accelerate API openness. Retail & e-commerce, growing at 14.3% CAGR, ramps up demand for scalable cloud, last-mile logistics software and omni-channel analytics, reshaping customer-experience benchmarks across the Indonesian ICT market.

Manufacturing adoption centres on Industry 4.0 pilot sites that prioritise asset-tracking and predictive-maintenance tools, while public-sector investment in smart-city platforms standardises IoT sensor deployment in 100 municipalities. Energy utilities deploy grid-monitoring and renewable-dispatch optimisation as the country pursues its updated 19-21% renewable-mix target. These vertical dynamics diversify revenue channels, reinforcing resilience of the Indonesian ICT market.

Note: Segment shares of all individual segments available upon report purchase

By Technology: AI Challenges Cloud Computing Dominance

Cloud platforms remained top at 39.0% share in 2024, benefiting from hyperscaler expansion and a ‘cloud-first’ posture in most IT refresh cycles. AI & analytics, however, records the quickest 14.2% CAGR as enterprises pursue predictive insights and multilingual customer-service chatbots, buoyed by sovereign-AI initiatives such as Sahabat-AI. IoT adoption escalates in logistics, agri-tech and environmental monitoring, while edge-computing nodes appear in mining pits and remote healthcare clinics to curb latency. Blockchain use remains exploratory in trade finance but gains policy interest as regulators test supply-chain provenance pilots.

The convergence of AI, edge and cloud reshapes solution packaging: vendors now position unified stacks that secure data pipelines from device to algorithm. Google Cloud’s BerdAIa consortium, projected to add IDR 620 trillion output by 2030, illustrates cross-industry collaboration that accelerates AI maturity. These trends reaffirm that while cloud revenue is large, AI’s growth momentum will recalibrate spending priorities within the Indonesian ICT market.

Geography Analysis

Java’s leadership stems from extensive fibre grids, the highest density of universities and a critical mass of hyperscale facilities, including a USD 300 million Jakarta campus led by Korea Investment and Sinar Mas. Jakarta’s Future City Hub initiative further lifts digital-competitiveness scores, translating into acute demand for low-latency edge nodes in retail and public safety. Sumatra now benefits from 1,042 km of tollway, trimming freight times and stimulating ERP and warehouse-management roll-outs by automotive and consumer-goods makers. Medium-sized cities such as Padang and Batam serve as natural logistics gateways, supporting wider adoption of 5G fixed-wireless and cloud point-of-presence nodes within the Indonesian ICT market.

Kalimantan’s momentum links to the greenfield administrative capital, Nusantara, which targets smart-city blueprint roll-outs with autonomous public transport and high-efficiency street-lighting grids. Papua enjoys the fastest expansion speed as Palapa Ring hand-off sites and SATRIA-1 ground stations bridge connectivity gaps for schools and clinics, enabling aggressive e-government and telemedicine pilots. Sulawesi’s industrial parks embed private LTE and process-control networks to lift mineral output efficiency, while Bali reinforces tourism resiliency through cashless-payment penetration and facial-recognition passenger processing flows at Ngurah Rai airport.

Collectively these regional patterns reflect a national drive to dilute Java’s dominance, supported by multi-modal transport links and aggressive last-mile broadband grants. Providers that customise offerings for local languages, intermittent-power environments and decentralised implementation teams will capture outsized gains as the Indonesian ICT market broadens beyond traditional urban strongholds.

Competitive Landscape

The market remains moderately fragmented. State-owned Telkom Indonesia sustains scale advantages by folding fixed-broadband arm IndiHome into Telkomsel and adding 13 MW of data-centre head-room to reach 55 MW in 2024. Rivalry intensified after the USD 6.5 billion XL Axiata–Smartfren merger formed TXSmart with 94.5 million subscribers, securing 26.3% wireless share and strengthening their 5G spectrum pool. Indosat Ooredoo Hutchison pursues a partner-driven playbook, co-building a USD 200 million AI centre with NVIDIA in Surakarta to anchor regional AI workloads.

International entrants prioritise capital efficiency and compliance alignment. Microsoft allocates USD 1.7 billion for cloud and skilling, while Tencent earmarks USD 500 million for its second Indonesian data-centre cluster. Hardware vendors such as Samsung benefit from strict TKDN enforcement that blocked iPhone 16 imports, enabling rapid share expansion in the premium-handset tier. Cyber-security players like Palo Alto Networks and Fortinet build managed-security hubs with local MSSPs to circumvent talent shortages. Overall, scale, localisation agility and energy-efficient facility design emerge as deciding success factors in the Indonesian ICT market.

Future rivalry will likely pivot around AI infrastructure depth, renewable-power procurement and regional outreach beyond Java. Firms able to integrate cloud, security and connectivity stacks, while meeting localisation thresholds and carbon targets, are positioned for durable advantage. Conversely, those slow to localise supply chains risk margin erosion under the 12% VAT regime and currency swings.

Indonesia ICT Industry Leaders

-

Huawei Technologies Co., Ltd.

-

Samsung Electronics Co., Ltd.

-

IBM Corporation

-

SAP SE

-

Oracle Corporation

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- June 2025: Google Cloud unveiled the Indonesia BerdAIa programme to seed cross-sector AI solutions worth a projected IDR 620 trillion by 2030.

- May 2025: Axiata agreed to acquire a 95% stake in Axis for USD 865 million, pending approvals.

- April 2025: Microsoft confirmed a USD 1.7 billion AI-cloud investment and pledged to train 840,000 Indonesians.

- March 2025: Indosat Ooredoo Hutchison activated the region’s first AI-RAN with Nokia & NVIDIA.

Indonesia ICT Market Report Scope

Information and communications technology, or ICT, is a broader term for information technology (IT). It refers to all communication technologies, such as wireless networks, the internet, computers, cell phones, software, videoconferencing, middleware, social networking, and other media applications and services, which enable users to store, access, transmit, retrieve, and manipulate information in digital form.

The Indonesia ICT market is segmented by type (hardware [computer hardware, networking equipment, peripherals], IT software, IT services [managed services, business process services, business consulting services, cloud services], IT infrastructure/data centers [colocation data centers, data center storage, data center servers, data center compute], IT security/ cybersecurity [application security, cloud security, data security, identity and access management, infrastructure protection, integrated risk management, network security equipment, endpoint security], communication services), by enterprise size (small and medium enterprises, large enterprises), by industry vertical (BFSI, IT and telecom, government, retail and E-commerce, manufacturing, energy and utilities, others). the market sizes and forecasts are provided in terms of value (USD) for all the above segments.

| By Type | Hardware | Computer Hardware | |

| Networking Equipment | |||

| Peripherals | |||

| IT Software | |||

| IT Services | Managed Services | ||

| Business Process Services | |||

| Business Consulting Services | |||

| Cloud Services | |||

| IT Infrastructure / Data Centres | Colocation Data Centres | ||

| Data-centre Storage | |||

| Data-centre Servers | |||

| Data-centre Compute | |||

| IT Security / Cyber-security | Application Security | ||

| Cloud Security | |||

| Data Security | |||

| Identity & Access Management | |||

| Infrastructure Protection | |||

| Integrated Risk Management | |||

| Network-security Equipment | |||

| Endpoint Security | |||

| Communication Services | |||

| By Enterprise Size | Small & Medium Enterprises | ||

| Large Enterprises | |||

| By Industry Vertical | BFSI | ||

| IT & Telecom | |||

| Government | |||

| Retail & E-commerce | |||

| Manufacturing | |||

| Energy & Utilities | |||

| Others | |||

| By Technology | Cloud Computing | ||

| Artificial Intelligence & Analytics | |||

| Internet of Things (IoT) | |||

| Blockchain | |||

| Edge Computing | |||

| By Region | Java | ||

| Sumatra | |||

| Kalimantan | |||

| Sulawesi | |||

| Papua | |||

| Bali & Nusa Tenggara | |||

By Type

| Hardware | Computer Hardware |

| Networking Equipment | |

| Peripherals | |

| IT Software | |

| IT Services | Managed Services |

| Business Process Services | |

| Business Consulting Services | |

| Cloud Services | |

| IT Infrastructure / Data Centres | Colocation Data Centres |

| Data-centre Storage | |

| Data-centre Servers | |

| Data-centre Compute | |

| IT Security / Cyber-security | Application Security |

| Cloud Security | |

| Data Security | |

| Identity & Access Management | |

| Infrastructure Protection | |

| Integrated Risk Management | |

| Network-security Equipment | |

| Endpoint Security | |

| Communication Services |

By Enterprise Size

| Small & Medium Enterprises |

| Large Enterprises |

By Industry Vertical

| BFSI |

| IT & Telecom |

| Government |

| Retail & E-commerce |

| Manufacturing |

| Energy & Utilities |

| Others |

By Technology

| Cloud Computing |

| Artificial Intelligence & Analytics |

| Internet of Things (IoT) |

| Blockchain |

| Edge Computing |

By Region

| Java |

| Sumatra |

| Kalimantan |

| Sulawesi |

| Papua |

| Bali & Nusa Tenggara |

Need A Different Region or Segment?

Customize Now

Key Questions Answered in the Report

What is the current size of the Indonesian ICT market?

The Indonesian ICT market is valued at USD 46.57 billion in 2025 and is projected to reach USD 75.35 billion by 2030.

Which segment is expanding the fastest?

Cyber-security solutions post the highest 13.2% CAGR through 2030, driven by rising threat awareness and stricter compliance.

How dominant is Java in national ICT spending?

Java accounts for 63.0% of spending, but eastern provinces such as Papua are closing the gap with a 16.0% CAGR.

Why are SMEs important to future growth?

Cloud-based SaaS and QR-enabled payments lower entry barriers, allowing SMEs to grow at a projected 12.1% CAGR through 2030.

What role does government policy play?

Large-scale infrastructure budgets, digital-skills programmes and local-content mandates collectively lift demand but also raise compliance costs.

Who are the leading competitors?

Telkom Indonesia, Indosat Ooredoo Hutchison and the newly formed TXSmart lead infrastructure and subscriber share, while Microsoft, Google Cloud and Tencent head hyperscale investment.

Page last updated on: June 25, 2025