Market Size of Global Steel Sections Industry

| Study Period | 2020 - 2029 |

| Base Year For Estimation | 2023 |

| CAGR | > 6.00 % |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Asia-Pacific |

| Market Concentration | Low |

Major Players

*Disclaimer: Major Players sorted in no particular order |

Need a report that reflects how COVID-19 has impacted this market and its growth?

Steel Sections Market Analysis

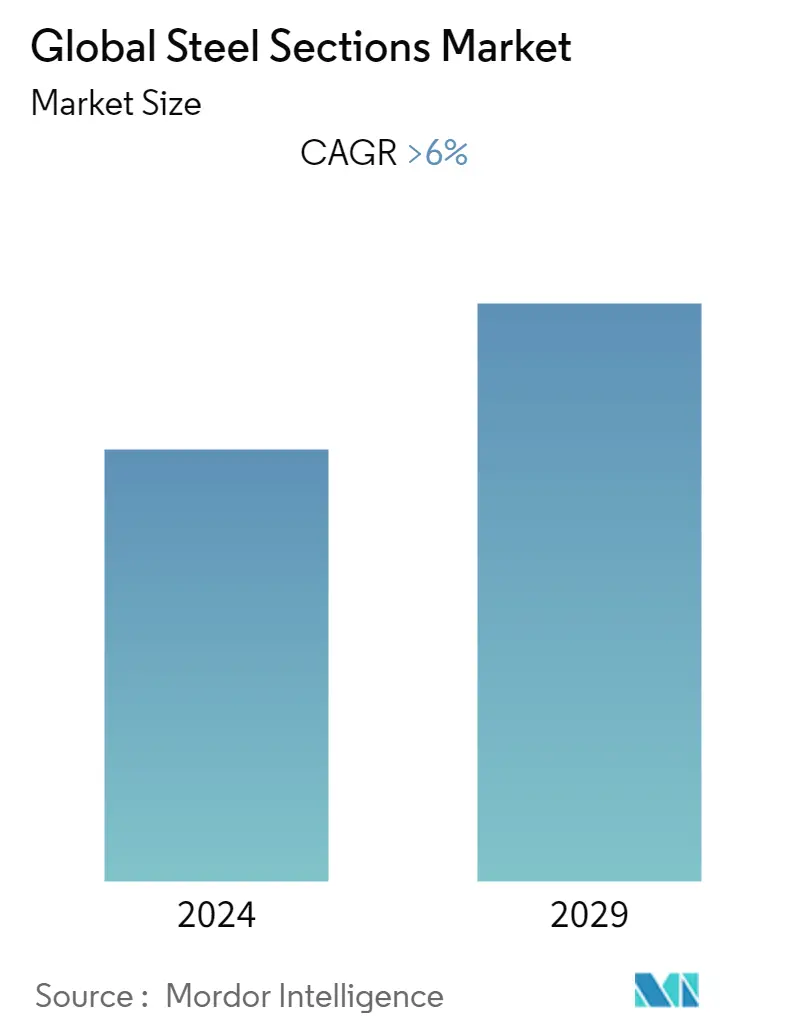

The size of Steel Sections market is USD 110.23 billion in the current year and is anticipated to register a CAGR of over 6% during the forecast period. The market is driven by the huge demand for steel sections at the infrastructure and construction project sites. Furthermore, the residential segment is also creating a huge demand due to its durability and anti-corrosive properties.

- Many metals and steel businesses in advanced markets have benefited from strong pent-up demand and high sales prices in 2021 and early 2022. As a result, profit margins increased, and financial resilience increased. Trade liberalization in the US's partial elimination of Section 232 tariffs on EU aluminum and steel imports should boost European production and exports. Fiscal stimulus has increased demand for metals and steel in key markets such as the United States and China.

- Following a very high growth rate in 2021, US metals and steel output increased by about 5% in 2022, driven primarily by continued robust demand from residential construction, aerospace, transportation, and engineering. However, given high fuel costs and consumer price inflation, the decline in automotive sales in H1 2022 indicates dwindling demand for high-priced, metal-intensive consumer goods. Order backlogs persist in the face of supply chain constraints. While oil and gas prices have skyrocketed, strong demand allows metals and steel companies to pass on higher input costs. These industry benefits have made some US manufacturers return to their home countries to avoid further supply chain disruptions and improve price stability.

- In August 2022, the price range for steel hollow sections in Europe narrowed, despite producers in the region pushing for higher prices due to alarming increases in energy costs. Further, current section prices are based on imported HRC from eastern and southeast Asia, or Turkey, which can take up to three months to arrive in Europe after an order is placed. The price of imported HRC, CFR main port Northern Europe, in May 2022 was EURO 850-920 (USD 891.20-964.59) per tonne. Some mills were also thinking about cutting production to help manage the effects of rising input costs.

- Weathering steel is a term used to describe products made from billets and blooms that are primarily used in the construction industry. They are typically produced in electric arc furnaces. Weathering steel items include rebar, wire rod, merchant bars, rails, and sections. Factors such as rapid urbanization and infrastructure projects such as railways and bridges that require high-strength weathering steel are propelling the market growth.

- However, fluctuations in raw material prices are expected to stymie market growth. Furthermore, the emergence of value-added rebar products, as well as an increase in infrastructure investments, are expected to provide growth opportunities for the weathering steel market in the coming years.

- Although several nations declared the steel sector to be essential, the pandemic has significantly reduced demand for steel production. In an attempt to slow the spread of COVID-19, steel consumption in the automotive industry, one of the biggest consumers, has been reduced. At the same time, falling energy prices have resulted in significantly reduced demand from industries like oil and gas. The COVID-19 outbreak has caused many non-essential building projects to be put on hold, which has hurt steel demand.