Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 2.21 Billion |

| Market Size (2026) | USD 2.31 Billion |

| Market Size (2031) | USD 2.86 Billion |

| Growth Rate (2026 - 2031) | 4.42% CAGR |

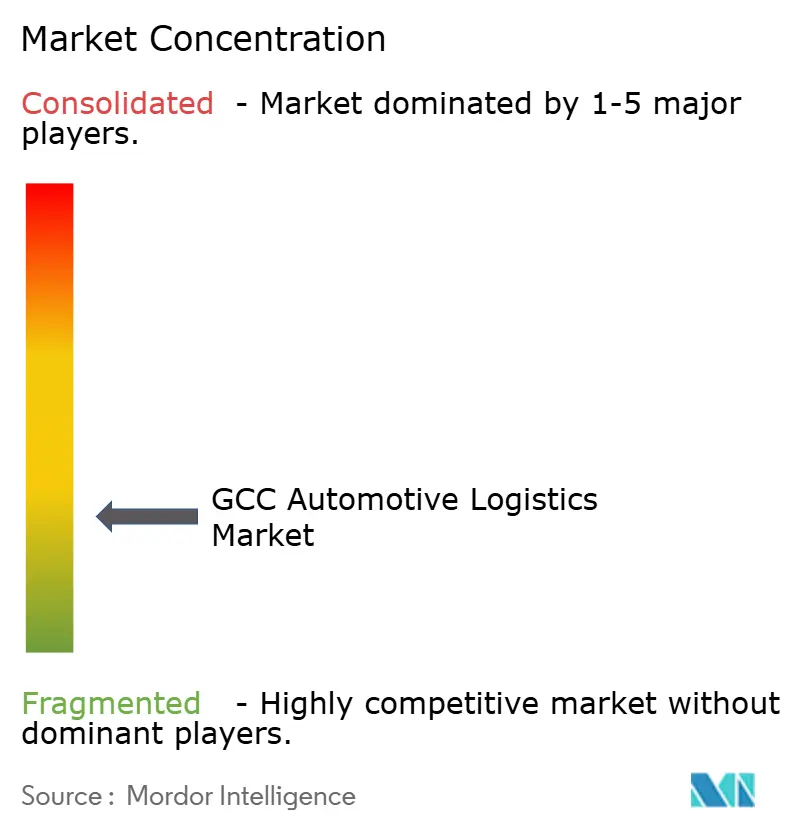

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

GCC Automotive Logistics Market Analysis by Mordor Intelligence

The GCC Automotive Logistics Market size is expected to grow from USD 2.21 billion in 2025 to USD 2.31 billion in 2026 and is forecast to reach USD 2.86 billion by 2031 at 4.42% CAGR over 2026-2031.

The growth reflects the bloc’s position as a tri-continental trade bridge, rising sovereign investment in multimodal corridors, and a decisive rebound in vehicle imports after the pandemic. Chinese vehicle makers are funneling larger volumes through Gulf ports, realigning historical flows that once centered on Japanese and European brands. Early adoption of digital customs platforms under the new Integrated Customs Tariff is trimming border dwell times, while a wave of cold-chain warehouse projects is preparing the network for electric-vehicle battery traffic. Intensifying cross-border commerce, combined with new truck and fuel regulations in Saudi Arabia, continues to test freight margins even as it unlocks demand for higher-margin value-added services.

Key Report Takeaways

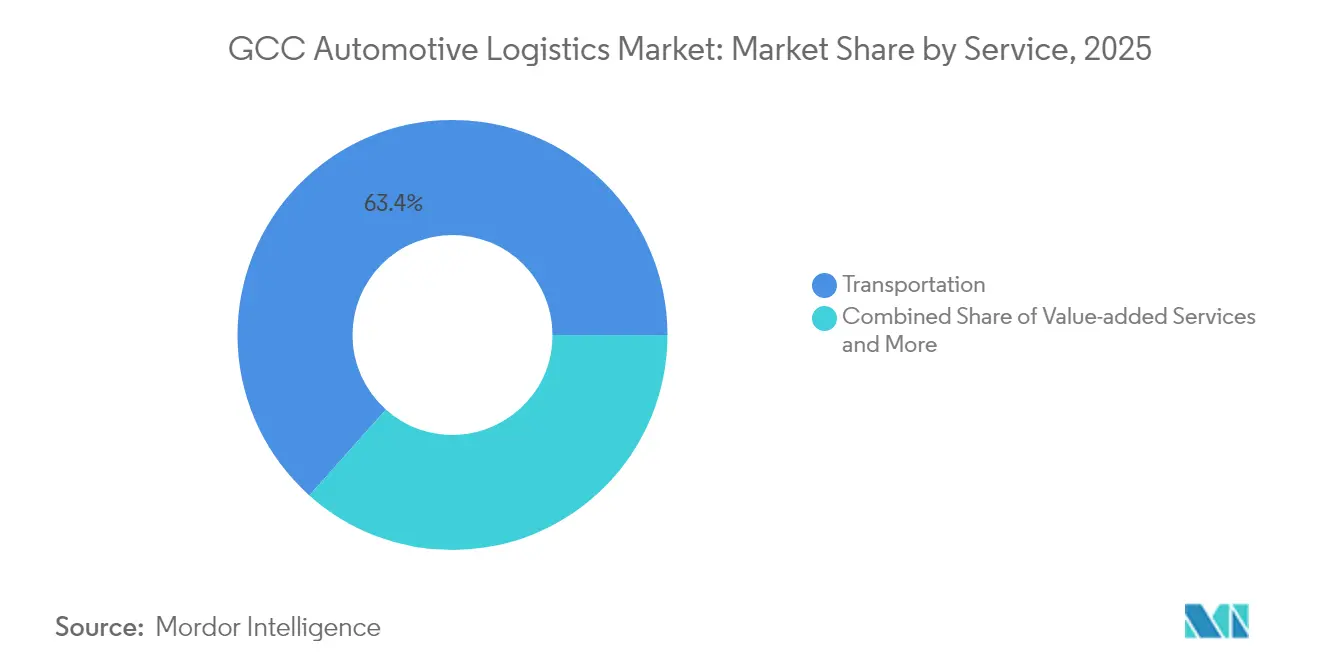

- By service, transportation held 63.40% of GCC automotive logistics market share in 2025; value-added services are poised for the quickest advance at a 3.62% CAGR through 2031.

- By type, OEM flows accounted for 67.30% of GCC automotive logistics market share in 2025, whereas aftermarket logistics is expected to record the fastest rise at a 4.08% CAGR to 2031.

- By cargo, finished vehicles represented 62.30% of the GCC automotive logistics market size in 2025, yet EV batteries and power electronics are forecast to grow at a 4.64% CAGR.

- By country, Saudi Arabia led with 40.55% revenue share in 2025; the United Arab Emirates is projected to log the highest 4.28% CAGR during 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

GCC Automotive Logistics Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Robust vehicle-sales rebound post-COVID | +1.2% | Saudi Arabia, UAE, wider GCC | Short term (≤ 2 years) |

| Mega-projects under Saudi Vision 2030 & UAE NLS 2030 | +1.8% | Saudi Arabia, UAE, spillover to neighbors | Long term (≥ 4 years) |

| E-commerce surge boosting last-mile LCV demand | +0.9% | UAE, Qatar, expanding to Saudi Arabia | Medium term (2-4 years) |

| EV and battery import boom | +0.7% | Saudi Arabia, UAE | Medium term (2-4 years) |

| Sovereign capex for logistics automation | +0.6% | Saudi Arabia, UAE | Long term (≥ 4 years) |

| Rising Chinese OEM penetration | +0.8% | GCC-wide, especially Saudi Arabia and UAE | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Robust Vehicle-Sales Rebound Post-COVID Drives Infrastructure Utilization

Sales volumes surpassed pre-pandemic levels in 2024, crowding RoRo berths and inland yards across the bloc. Saudi dealerships reordered aggressively as consumer sentiment strengthened, while Chinese marques such as MG and Geely seized shelf space once dominated by Japanese sedans. Gulf ports responded by re-striping yards to accommodate different vehicle dimensions and revising parts-picking logic inside distribution centers. Bahrain’s Ministry of Transportation reported that Khalifa bin Salman Port handled 4,357 vehicles in September 2024, up from 2,618 units a month earlier[1]Ministry of Transportation Bahrain, “September 2024 Vessel Statistics,” mot.gov.bh.

Mega-Projects Under Saudi Vision 2030 & UAE NLS 2030 Transform Regional Connectivity

Saudi Arabia’s SAR 4 billion (USD 1.06 billion) SAL Logistics Zone clusters processing, storage, and cold-chain facilities near Jeddah Islamic Port, while the USD 10 billion NEOM–DSV partnership is embedding automated yards, drone inventories, and green-hydrogen truck docks within the futuristic city[2]Saudi Logistics Academy, “SAL Logistics Zone Initiative,” sla.gov.sa. Parallel UAE investments include Dubai’s AED 90 million (USD 24.5 million) JAFZA Logistics Park extension and Abu Dhabi’s AED 10 billion (USD 2.72 billion) industrial strategy that fast-tracks temperature-controlled units for battery warehousing. Coordinated rail spurs will eventually knit these mega-nodes into a seamless corridor stretching from the Red Sea to the Gulf of Oman.

E-Commerce Surge Accelerates Last-Mile LCV Demand and Urban Distribution Networks

Online retail volumes doubled in key Gulf capitals in the past two years, pivoting logistics priorities toward light commercial vehicles. Fulfillment providers are rolling out micro-hubs within 20 kilometers of dense neighborhoods to shorten delivery cycles. Technology start-ups, backed by USD 9 million in venture capital, are integrating auto-parts stocking with same-day consumer parcel flows, allowing warehouses to toggle between B2B and B2C pick paths.

EV & Battery Import Boom Requires Specialized Temperature-Controlled Logistics Infrastructure

Electric-vehicle shipments surged in 2024, introducing UN 3480 and UN 3481 battery classes into Gulf freight portfolios. Each lithium-ion pack now travels in fire-retardant packaging equipped with temperature sensors and data loggers. RSA Global, in collaboration with Americold, commissioned a 15,000-pallet cold box in Dubai dedicated to 15-25 °C battery staging. Compliance with Gulf fire codes and International Maritime Organization rules is filtering out smaller haulers and concentrating flows among certified 3PLs[3]CHEP, “Sustainable Battery Transport Solutions,” chep.com.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Fragmented customs across GCC borders | −0.8% | All member states | Short term (≤ 2 years) |

| Skilled warehouse & truck-driver shortage | −1.1% | Saudi Arabia, UAE, wider GCC | Medium term (2-4 years) |

| Limited rail haulage capacity | −0.5% | Saudi Arabia, UAE | Long term (≥ 4 years) |

| High capex for automation & cold-chain | −0.7% | GCC-wide | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Fragmented, Non-Harmonized Customs Across GCC Borders Creates Operational Inefficiencies

While the unified tariff aligns duty rates, physical inspection rules still diverge. Trucks entering Oman via the Al Buraimi post clear in under four hours, yet similar loads can wait 12–18 hours at the Al Batha gate into Saudi Arabia. Documentation redundancies inflate demurrage bills and complicate just-in-time parts programs for regional assembly lines. A common digital window remains under pilot testing, with full certification reciprocity still at least two years away as per Gulf Cooperation Council secretariat updates[4]GCC Secretariat, “Customs Union Progress Report,” gcc.int.

Shortage of Skilled Warehouse & Truck-Driver Labor Constrains Operational Capacity

The International Road Transport Union projects that global truck driver shortages will double by 2028, with the GCC region experiencing particularly severe constraints. Gulf wage inflation has made driver recruitment competitive with construction and oil-field jobs, pushing some fleets to park idle tractors. Warehouses confront a parallel gap in technicians capable of maintaining automated sortation or operating hazardous-goods zones for batteries. Bahri Logistics signed a two-year program with the Saudi Logistics Academy to upskill local talent in 2024, yet the cadence of graduates lags demand.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service: Transportation Dominance Faces Value-Added Disruption

Transportation services controlled 63.40% of GCC automotive logistics market share in 2025, anchored by road freight corridors that knit together port cities and desert hinterlands. RoRo berths at Jebel Ali, Dammam, and Sohar funnel full shiploads into convoys bound for dealer yards, while sea-to-rail transload remains nascent outside the Etihad Rail Phase 2 stub. The GCC automotive logistics market size tied to transportation is forecast to grow in lockstep with finished-vehicle imports yet cede relative weight as higher-margin services proliferate.

Value-added modules - pre-delivery inspection, battery conditioning, and software flashing - are on course for a 3.62% CAGR. Logistics providers are converting ambient sheds into temperature-managed zones with 24-hour flame-suppression and ISO17025 testing booths. The resulting bundled propositions fetch premiums of 15-25% over standard cross-dock moves and form a key entry barrier for asset-light start-ups.

By Type: OEM Networks Drive Volume While Aftermarket Accelerates

Original-equipment manufacturer flows represented 67.30% of GCC automotive logistics market share in 2025, mirroring the region’s reliance on imported finished cars and CKD kits. Routinely scheduled block-trains and chartered car carriers allow tier-one 3PLs to leverage density economics.

Aftermarket lanes, growing at a 4.08% CAGR (2026-2031), favor agile operators that can execute high-frequency, low-volume deliveries to 2,000-plus service outlets. E-commerce portals specializing in brake pads and lubricants now demand next-day fulfilment, tightening cut-off windows for parts hubs in Dubai South and Riyadh’s Sudair City. The shift compels OEM-centric forwarders to invest in piece-picking automation and reverse-logistics workflows for remanufactured components.

By Cargo Type: Finished Vehicles Lead Despite EV Battery Surge

Finished vehicles retained 62.30% of cargo share in 2025 thanks to large-lot imports from China and Korea. A single vessel call can discharge 5,000 sedans, necessitating purpose-built marshalling yards with vehicle-tracking RFID gates. This concentration allows the GCC automotive logistics market size associated with vehicle moves to remain the revenue spine of many 3PL contracts.

EV batteries and power electronics are scaling from a lower base yet advancing at a 4.64% CAGR (2026-2031). Each GCC country now enforces Class 9 labeling, shock sensors, and thermal stripping before inbound clearance. The capital intensity - special racks, foam insulation, and fire blankets - spurs alliances between shipping lines and cold-chain specialists. As battery volumes mount, total landed cost per unit is expected to dip by 2030, making electric cars more price-competitive across dealer showrooms.

Geography Analysis

Saudi Arabia dominated the GCC automotive logistics market in 2025 with a 40.55% slice, propelled by Vision 2030 capital programs and its role as the Gulf’s biggest car buyer. The SAR 4 billion (USD 1.06 billion) SAL Logistics Zone near Jeddah Islamic Port integrates battery chambers, bonded yards, and an air-freight feeder, enabling two-hour truck transfers to inland distributors. Planned NEOM freight villages will plug into a 6,000-kilometer rail network, promising modal shifts from diesel trucks to electric locomotives once operational.

The United Arab Emirates is on track for the fastest 4.28% CAGR (2026-2031) thanks to Dubai’s trade-first infrastructure and Abu Dhabi’s diversification into advanced manufacturing. Jebel Ali’s newly unveiled 13,000-CEU yard gives the port a total 75,000-CEU footprint, letting shipping lines stage peak-season overflow without costly diversions. Meanwhile, the Einride-DP World autonomous-truck pilot aims to slash 14,600 t of annual emissions across 100 battery-electric tractors, underscoring the UAE’s sustainability branding.

Competitive Landscape

The field is moderately fragmented, with regional stalwarts mixing with multinational heavyweights. Almajdouie Logistics pairs local ground assets with deep-sea alliances, whereas DHL and DSV inject end-to-end visibility platforms spanning origin factories in China to Gulf showrooms. The CEVA–Almajdouie joint venture finalized in 2024 illustrates the trend toward hybrid models that blend regional access with global control towers.

Technology is the prime battleground. Kuehne + Nagel’s AI-driven ETA engine trims yard dwell by 9%, while DP World’s port community system automates tendering for last-mile drayage slots. Certified battery cells move only through facilities sporting FM-approved sprinklers and 24/7 thermal cameras, narrowing the field of compliant operators. The rising bar for ESG reporting further advantages scale players able to finance solar rooftops and hydrogen truck pilots.

M&A momentum is set to continue as asset-heavy regional firms seek partners for digital upgrades and network reach. DSV’s acquisition of Schenker in 2025, raising combined revenues above EUR 39 billion (USD 40.6 billion), signals a capital-powered push into high-service niches such as finished-vehicle remarketing. Smaller fleets face succession issues and may opt to fold into larger groups to access telematics platforms, driver academies, and bonded-warehouse licenses.

GCC Automotive Logistics Industry Leaders

Almajdouie Logistics

Gulf Agency Company Ltd.

Al-Futtaim Logistics

Bahri Logistics

RSA Global

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- August 2025: DP World opened a 2.6 million sq ft vehicle yard at Jebel Ali Terminal 4, lifting storage capacity to 75,000 CEUs.

- June 2025: DHL committed EUR 500 million (USD 520 million) to expand Gulf facilities, spotlighting Saudi Arabia and the UAE.

- April 2025: DSV announced the EUR 14.3 billion (USD 14.9 billion) takeover of Schenker, boosting automotive vertical scale.

- October 2024: CEVA Logistics and Almajdouie Group closed a joint-venture agreement to build an integrated Saudi platform.

GCC Automotive Logistics Market Report Scope

Automotive logistics refers to the efficient coordination and transportation of resources, including equipment, inventory, and materials, linked to both finished vehicles and automotive parts. This process ensures their smooth movement from their origin to the intended destination.

The GCC automotive logistics market is segmented by service (transportation, warehousing, distribution, & inventory management, and other services), type (finished vehicles, auto components, and other types), and country (United Arab Emirates, Saudi Arabia, Qatar, Kuwait, Bahrain, and Oman).

The report offers the market size and forecast values in USD for the above segments.

By Service

| Transportation | Road |

| Rail | |

| Air | |

| Sea / Ro-Ro / Short-Sea | |

| Warehousing, Distribution & Inventory Management | |

| Value-added Services |

By Type

| OEM |

| Aftermarket |

By Cargo Type

| Finished Vehicles |

| Auto Components |

| EV Batteries and Power-Electronics |

| Other Cargo |

By Country

| Saudi Arabia |

| United Arab Emirates |

| Qatar |

| Kuwait |

| Oman |

| Bahrain |

| By Service | Transportation | Road |

| Rail | ||

| Air | ||

| Sea / Ro-Ro / Short-Sea | ||

| Warehousing, Distribution & Inventory Management | ||

| Value-added Services | ||

| By Type | OEM | |

| Aftermarket | ||

| By Cargo Type | Finished Vehicles | |

| Auto Components | ||

| EV Batteries and Power-Electronics | ||

| Other Cargo | ||

| By Country | Saudi Arabia | |

| United Arab Emirates | ||

| Qatar | ||

| Kuwait | ||

| Oman | ||

| Bahrain |

Key Questions Answered in the Report

What is the current value of the GCC automotive logistics market?

The market is valued at USD 2.31 billion in 2026 and is forecast to reach USD 2.86 billion by 2031.

Which service segment leads revenue in Gulf automotive logistics?

Transportation accounts for 63.40% of 2025 revenue, reflecting heavy reliance on road and RoRo links.

Which Gulf country is the fastest-growing logistics hub for vehicles?

The United Arab Emirates shows the highest 4.28% CAGR between 2026 and 2031, buoyed by port and free-zone expansions.

How quickly are EV batteries becoming a logistics opportunity in the region?

Battery and power-electronics flows are rising at a 4.64% CAGR, faster than any other cargo category.

What is the biggest operational constraint faced by logistics firms today?

A shortage of qualified truck drivers and warehouse technicians is suppressing capacity and raising labor costs.

How fragmented is competition among Gulf automotive logistics providers?

The market scores 5/10 on concentration, with the top five firms holding just over half of total revenue.

Page last updated on: