Market Overview

| Study Period | 2020 - 2030 |

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

| Market Size (2025) | USD 340.86 Billion |

| Market Size (2030) | USD 550.13 Billion |

| Growth Rate (2025 - 2030) | 10.05% CAGR |

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Europe Prepaid Cards Market Analysis by Mordor Intelligence

The Europe prepaid card market size is valued at USD 340.86 billion in 2025 and is forecast to reach USD 550.13 billion by 2030, reflecting a steady 10.05% CAGR. Accelerated adoption of embedded-finance rails by neo-banks, mandatory instant-payment capabilities under the EU regulation effective 2024, and the rebound in Southern European tourism collectively sustain double-digit growth momentum.[1]European Commission, “Legislative proposal on instant payments,” finance.ec.europa.eu Physical cards continue to dominate everyday spending, yet virtual issuance is expanding quickly as corporate platforms and gig-work marketplaces demand instant provisioning and granular controls. Regulatory certainty under PSD2 and the forthcoming Payment Services Regulation encourages cross-border scalability, while tokenisation and mobile-wallet integrations lift security standards and user convenience. Incumbent payment networks defend pricing power even as interchange caps tighten, compelling issuers to monetise value-added services rather than pure transaction fees.

Key Report Takeaways

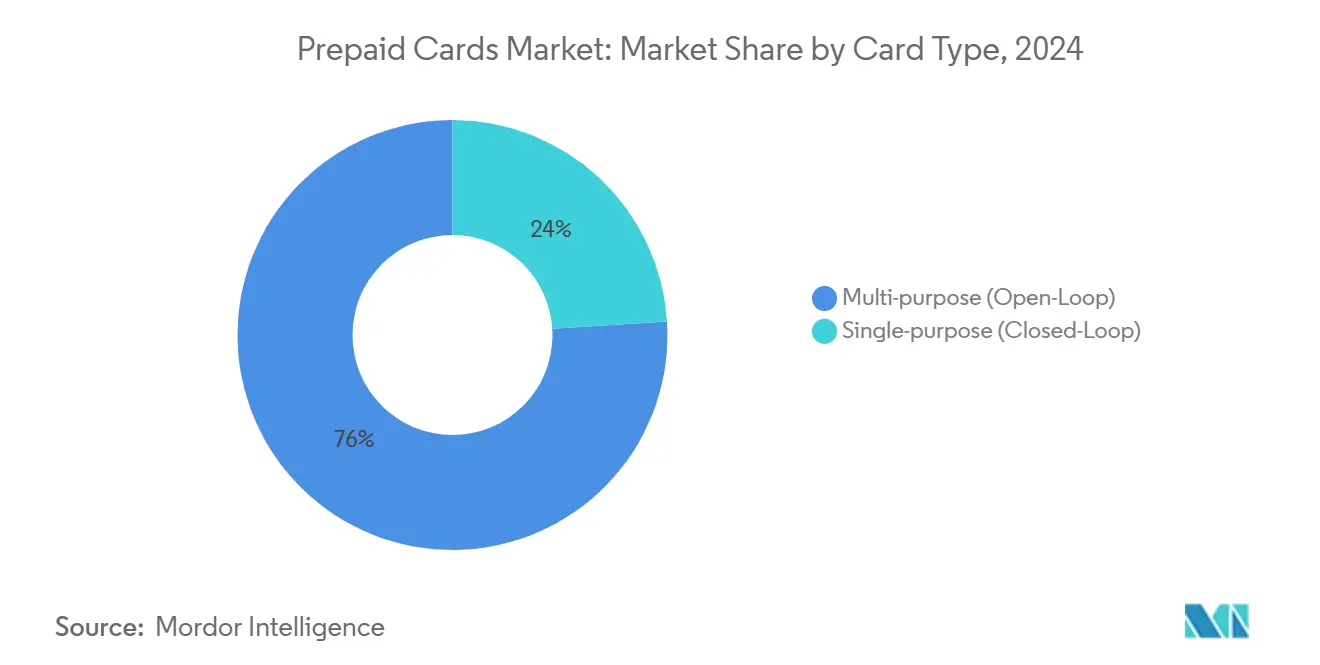

- By card type, multi-purpose open-loop cards led with 76% of the Europe prepaid card market share in 2024, whereas single-purpose closed-loop cards are projected to grow at an 11.7% CAGR through 2030.

- By the card model, physical cards held 68% revenue share in 2024; virtual cards exhibit the fastest expansion at an 11.2% CAGR to 2030.

- By reloadability, reloadable products accounted for 63% of the Europe prepaid card market size in 2024, while non-reloadable formats advance at a 10.3% CAGR.

- By usage, general-purpose reloadable cards captured 41% share in 2024, whereas payroll and incentive solutions are increasing at a 10.5% CAGR.

- By geography, the United Kingdom retained 24% share of the Europe prepaid card market size in 2024; the Nordic region is the fastest-growing cluster, expanding at an 11.2% CAGR.

Europe Prepaid Cards Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Adoption of Embedded Finance by European Neo-banks | +1.8% | UK, Germany, Netherlands, France | Medium term (2-4 years) |

| EU Instant Payments Regulation Boosting Reloadable Prepaid Demand | +1.5% | Eurozone countries, expanding to non-euro EU | Short term (≤ 2 years) |

| Payroll Digitisation by Gig-Work Platforms Across UK & DACH | +1.2% | UK, Germany, Austria, Switzerland | Medium term (2-4 years) |

| SEPA Instant Payments Mandate Accelerating Open-Loop Prepaid Adoption | +1.0% | All SEPA participating countries | Short term (≤ 2 years) |

| Tourism Rebound Driving Multi-Currency Travel Cards (Spain, Italy) | +0.9% | Spain, Italy, France, Greece | Short term (≤ 2 years) |

| Municipal Digital-Voucher Schemes Fueling Retail Closed-Loop Cards | +0.7% | Germany, Greece, France, Netherlands | Medium term (2-4 years) |

| Tokenised Contactless & Mobile Wallet Integration of Prepaid Cards | +0.6% | Global, with early adoption in Nordics and UK | Long term (≥ 4 years) |

Source: Mordor Intelligence

Embedded Finance Adoption by European Neo-banks

European neo-banks scale prepaid issuance by embedding card functionality in third-party platforms, evidenced by Revolut’s 50 million customers and USD 545 million profit in 2024. Embedded rails reduce acquisition friction, allowing instant digital issuance across e-commerce, gig-work, and corporate-expense ecosystems. PSD2 passporting plus the forthcoming Payment Services Regulation harmonise compliance, enabling borderless distribution. Real-time analytics let issuers configure spend controls, loyalty rewards, and risk-scoring in-app, creating higher engagement than legacy prepaid propositions. Consequently, the Europe prepaid card market benefits from network-effects as fintech platforms bundle payments, budgeting, and lending around a single stored-value core.

EU Instant Payments Regulation Boosting Reloadable Demand

The 2024 regulation mandates equal pricing for instant versus traditional transfers and compels 24/7 availability, making reloadable prepaid instruments ideal for gig-economy payouts, cross-border remittances, and SME cash-flow management cashmanagement. Compliance obligations such as verification-of-payee create a scale advantage for established issuers, reinforcing moderate market concentration. Early movers leverage instant settlement to market “fund-in-seconds” propositions that improve card stickiness and interchange stability, thereby extending the Europe prepaid card market growth runway.

Payroll Digitisation by Gig-Work Platforms

Variable-income workers in the UK and DACH increasingly prefer prepaid payroll cards that circumvent 1–3-day bank clearing delays. Platforms issue virtual cards at the point of onboarding, satisfying IR35 and cross-border compliance rules while offering real-time earnings access. Card-linked apps bundle tax calculators and expense trackers, boosting worker retention. Industrial logistics and last-mile delivery sectors demonstrate outsized usage due to high shift variability, reinforcing demand throughout the Europe prepaid card market.

SEPA Instant Mandate Accelerating Open-Loop Adoption

The 2025 SEPA rulebook removes residual pockets of non-compliance, ensuring universal rail availability across 36 member states.[2]European Payments Council, “2025 SEPA Instant Credit Transfer Rulebook,” europeanpaymentscouncil.eu Open-loop prepaid cards integrate instant-credit transfers to provide continuous balance updates without correspondent banking overhead. Policy support from the European Central Bank favours domestic-scheme innovation, enabling issuers to differentiate via real-time refunds, peer-splitting, and dynamic FX conversion. Consequently, open-loop solutions consolidate their leadership position inside the Europe prepaid card market.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Interchange Fee Regulation Compressing Issuer Margins | -1.4% | EU-wide, particularly affecting tourist card segments | Short term (≤ 2 years) |

| Declining Refugee Benefit Loads Post-2022 Peak | -0.8% | Germany, Poland, Central European countries | Medium term (2-4 years) |

| A2A Wallet Proliferation in Nordics Cannibalising Prepaid Usage | -0.6% | Denmark, Sweden, Norway, Finland | Medium term (2-4 years) |

| Fragmented AML/KYC Rules Elevating Cross-Border Issuance Costs | -0.5% | Cross-border operations, particularly affecting smaller issuers | Long term (≥ 4 years) |

Source: Mordor Intelligence

Interchange-Fee Regulation Compressing Margins

Visa and Mastercard agreed to extend EU tourist-card interchange caps through 2029, constraining issuer revenue pools. The UK Payment Systems Regulator calculates that domestic merchants pay USD 250 million additional scheme fees annually, intensifying scrutiny.[3]Payment Systems Regulator, "MR22/1.9 Market Review of Card Scheme and Processing Fees Interim Review., psr.org.uk Issuers respond by pivoting to subscription pricing, data monetisation, and B2B expense-management bundles to defend returns, reshaping profit pools within the Europe prepaid card industry.

Declining Refugee Benefit Loads Post-2022 Peak

Germany, Poland, and other CEE markets are tapering emergency disbursements as Ukrainian refugee inflows stabilise, reducing transaction volumes for specialised benefit cards. Providers that scaled rapidly on humanitarian programmes must diversify into municipal voucher and social-assistance schemes with tighter KYC rules and domestic-spend restrictions, moderating segment expansion inside the Europe prepaid card market.

Segment Analysis

By Card Type: Open-Loop Strength, Closed-Loop Momentum

Multi-purpose open-loop solutions held 76% share in 2024, benefiting from universal merchant acceptance and regulatory harmonisation that streamlines cross-border top-ups. Instant-payment connectivity further enhances appeal to frequent travellers and SMEs operating pan-Europe. Government agencies, however, are adopting closed-loop architectures for asylum-seeker and tourism-voucher programmes, accelerating single-purpose card issuance at an 11.7% CAGR through 2030.

Closed-loop designs deliver granular spend controls, real-time analytics, and reduced fraud exposure, attributes suited to targeted subsidy and corporate-expense schemes. Municipal deployments in Germany and Greece showcase scalable templates that anchor future demand. As a result, closed-loop offerings widen their addressable base, even while open-loop formats remain the backbone of the Europe prepaid card market.

By Card Model: Physical Resilience, Virtual Upswing

Physical variants accounted for 68% usage in 2024, reflecting consumer familiarity, backup utility when mobile batteries fail, and the prevalence of contactless acceptance across transit and retail networks. Senior segments and tourist populations still prefer tangible cards, stabilising absolute volumes.

Virtual cards, expanding at an 11.2% CAGR, dominate new-to-market issuance on embedded-finance platforms. Instant provisioning, tokenisation-driven security, and merchant-specific dynamic controls make them the default choice for corporate-expense and gig-payout programmes. Neo-banks harness these attributes to deepen wallet share, reinforcing structural gains for digital issuance inside the Europe prepaid card market.

By Reloadability: Flexible Products Prevail

Reloadable formats represented 63% revenue in 2024, aligning with the EU Instant Payments Regulation that supports perpetual top-ups and real-time fund availability. Budget-management features and recurring payroll loads anchor consumer loyalty, especially among migrant and gig-economy segments.

Non-reloadable cards nevertheless grow at a 10.3% CAGR, propelled by gift-card programmes below EUR 150 (USD 165) thresholds that enjoy simplified KYC verestro.com. Tourism-oriented single-load products gain traction as travellers seek fixed-budget tools, reinforcing balanced growth across reload profiles in the Europe prepaid card market.

By Usage: General-Purpose Dominance, Payroll Acceleration

General-purpose reloadable solutions retained 41% share in 2024 as households use them for day-to-day spend, cross-border remittances, and disciplined budgeting. Neo-bank onboarding funnels amplify adoption by positioning prepaid as a stepping stone toward full banking relationships.

Payroll and incentive cards, expanding 10.5% CAGR, capitalise on immediate wage-access demands in the gig and logistics sectors. Integrated tax and expense modules embed the product deep into platform ecosystems, driving repeat loads. Gift, benefit, and travel cards continue to fill niche use cases, diversifying revenue streams within the Europe prepaid card market.

By Vertical: Retail Leads, Corporate Expense Surges

Retail and e-commerce applications command 38% share as omnichannel merchants deploy prepaid for loyalty, acquisition, and closed-loop gift solutions. Spending analytics generated by retail cards create upsell opportunities and drive incremental footfall.

Corporate-expense programmes post a 10.7% CAGR as firms digitise spend controls in hybrid work environments. Edenred’s EUR 1.395 billion (USD 1.53 billion) H1 2024 revenue underscores scale potential. Integration with ERP and HR systems ensures policy compliance and auditability, magnifying the strategic appeal of prepaid within B2B contexts of the Europe prepaid card market.

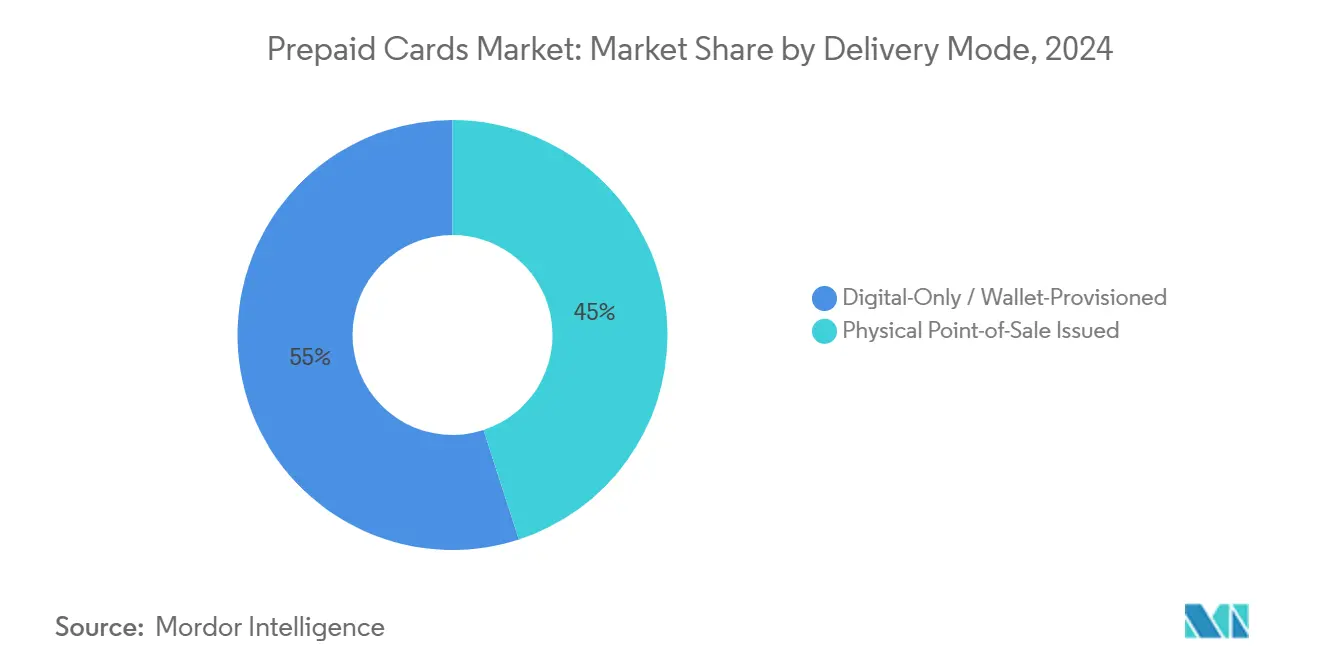

By Delivery Mode: Digital-First Leadership

Digital-only provisioning captured 55% share in 2024, and it is growing fastest with 11.5% CAGR during the period. reflecting frictionless remote onboarding and zero physical-inventory costs. Fintech providers layer biometric ID verification and AI fraud screens to meet supervisory requirements while sustaining instant issuance.

Point-of-sale issued cards retain relevance for tourism and in-store gift applications, offering immediate tangibility and upsell potential at checkout. Nonetheless, falling unit costs for digital delivery and rising mobile-wallet penetration favour continued migration toward fully virtual distribution across the Europe prepaid card market.

By Distribution Channel: Online Platforms in Ascendance

Online and app-based channels generated 59% of 2024 sales as consumers gravitate to self-service interfaces and contextual card provisioning within e-commerce checkouts. Social-commerce integrations further propel digital activation volume.

Retail reload kiosks and partner supermarkets grow 11.4% CAGR, bridging cash-to-digital conversion for unbanked populations. Bank branches and post offices maintain niche roles for high-value loads and identity-verified issuance, sustaining multi-channel equilibria throughout the Europe prepaid card market.

Geography Analysis

The United Kingdom leads the Europe prepaid card market with 24% share, leveraging a mature fintech talent base, progressive Financial Conduct Authority guidance, and rapid uptake of embedded-finance services. London-based issuers export models across the continent through passporting equivalence post-Brexit, preserving scale economies while adapting to distinct EEA compliance regimes.

Nordic countries collectively advance at an 11.2%CAGR, pairing account-to-account wallets such as Wero with prepaid overlays that deliver merchant ubiquity absent among domestic schemes. Consumers embrace hybrid payment stacks that toggle seamlessly between bank and stored-value rails, fostering innovation clusters in Stockholm and Helsinki.

Core Eurozone markets—Germany, France, Italy, and Spain—sustain depth via diversified use cases: corporate-expense controls in DACH, tourism travel cards along the Mediterranean corridor, and municipal voucher programmes targeting SME digitisation. The Netherlands and Belgium act as cross-border testing grounds for real-time FX and multicurrency propositions, while Poland extends the Europe prepaid card industry’s reach into rapidly growing Central European retail segments.

Competitive Landscape

Visa and Mastercard process 61% of euro-area card transactions, granting scale economies that partially offset interchange-fee compression. [4]European Central Bank, “Most EU countries rely on international card schemes for card payments,” ecb.europa.eu Their strategic extension of cap agreements to 2029 stabilises regulatory risk while prompting issuers to shift towards subscription and data-driven revenue constructs.

Neo-banks and embedded-finance specialists escalate rivalry by packaging prepaid cards as gateways to multicurrency accounts, crypto trading, and micro-savings products. Revolut’s USD 1 trillion annual transaction throughput and sustained profitability validate the platform thesis, while Solaris’ majority acquisition by SBI underscores capital-intensity and compliance overhead inherent in banking-as-a-service models.

Consolidation accelerates: Railsr’s USD 283 million purchase of Equals Group builds scale across FX and expense-management verticals, Edenred commits to 10% EBITDA growth via acquisitive expansion, and Visa bolsters risk analytics through its Featurespace buy-out. Competitive positioning now hinges on real-time fraud prevention, tokenisation breadth, and instant-credit transfer connectivity that deepen user engagement inside the Europe prepaid card market.

Europe Prepaid Cards Industry Leaders

-

Visa

-

Mastercard

-

PayPal Holdings Inc.

-

American Express Company

-

Green Dot Corporation

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- February 2025: Payrails partners with Mastercard to embed next-gen payment orchestration in enterprise ERP stacks, illustrating a platform scaling strategy that targets high-volume corporates.

- January 2025: SBI Holdings acquires a majority stake in Solaris, injecting EUR 100–150 million (USD 109–164 million) to stabilise the BaaS provider and secure Asian-European corridor synergies.

- December 2024: Railsr closes a USD 283 million all-cash acquisition of Equals Group to create a multi-currency powerhouse spanning prepaid, FX, and cross-border settlements.

- December 2024: Edenred announces a EUR 600 million (USD 655 million) share-buyback and re-affirms ≥10% EBITDA growth targets, signalling confidence in corporate-expense demand.

Europe Prepaid Cards Market Report Scope

Where consumers or companies prefer to utilize an electronic means of payment without attaching the payment to a credit or debit account, prepaid cards have replaced cash, checks, and other payment cards. However, various taxes and security concerns are projected to limit market expansion. Europe Prepaid Card Market segmented By Card Type (Multi-Purpose, Single-purpose), Vertical (Retail, Corporate Institutions, Government, Financial Institutions & Others), Usage (General Purpose Reloadable Cards, Gift Card, Government Benefits Disbursement Card, Incentive Payroll Card), Geography (Germany, France, the United Kingdom, Russia, Netherlands, and Spain).

| By Card Type | Multi-purpose (Open-Loop) |

| Single-purpose (Closed-Loop) | |

| By Card Model | Physical Cards |

| Virtual Cards | |

| By Reloadability | Reloadable |

| Non-Reloadable | |

| By Usage | General Purpose Reloadable |

| Gift Card | |

| Government Benefit Disbursement | |

| Payroll and Incentive | |

| Travel and Foreign Currency | |

| Other Usage | |

| By Vertical | Retail and E-commerce |

| Corporate Expense Management | |

| Government and Public Sector | |

| Financial Institutions and Fintech | |

| Travel and Hospitality | |

| Others | |

| By Delivery Mode | Physical Point-of-Sale Issued |

| Digital-Only / Wallet-Provisioned | |

| By Distribution Channel | Bank Branches |

| Online and Mobile Apps | |

| Retail Stores and Kiosks | |

| Others (Post Offices, Transit Hubs) | |

| By Geography | United Kingdom |

| Germany | |

| France | |

| Italy | |

| Spain | |

| Netherlands | |

| Nordics (Denmark, Sweden, Norway, Finland) | |

| Poland | |

| Rest of Europe (Switzerland, Austria, Belgium, etc.) |

By Card Type

| Multi-purpose (Open-Loop) |

| Single-purpose (Closed-Loop) |

By Card Model

| Physical Cards |

| Virtual Cards |

By Reloadability

| Reloadable |

| Non-Reloadable |

By Usage

| General Purpose Reloadable |

| Gift Card |

| Government Benefit Disbursement |

| Payroll and Incentive |

| Travel and Foreign Currency |

| Other Usage |

By Vertical

| Retail and E-commerce |

| Corporate Expense Management |

| Government and Public Sector |

| Financial Institutions and Fintech |

| Travel and Hospitality |

| Others |

By Delivery Mode

| Physical Point-of-Sale Issued |

| Digital-Only / Wallet-Provisioned |

By Distribution Channel

| Bank Branches |

| Online and Mobile Apps |

| Retail Stores and Kiosks |

| Others (Post Offices, Transit Hubs) |

By Geography

| United Kingdom |

| Germany |

| France |

| Italy |

| Spain |

| Netherlands |

| Nordics (Denmark, Sweden, Norway, Finland) |

| Poland |

| Rest of Europe (Switzerland, Austria, Belgium, etc.) |

Need A Different Region or Segment?

Customize Now

Key Questions Answered in the Report

What is the current value of the Europe prepaid card market?

The Europe prepaid card market size stands at USD 340.86 billion in 2025.

How fast is the market expected to grow?

It is projected to expand at a 10.05%CAGR, reaching USD 550.13 billion by 2030.

Which card type holds the largest market share?

Multi-purpose open-loop cards led with 76% share in 2024.

Which geographic region is growing the fastest?

The Nordic region posts the highest growth trajectory at an 11.2%CAGR through 2030.

How are interchange-fee caps affecting issuers?

Caps extended to 2029 compress transaction-based margins, prompting issuers to pivot toward subscription and data-driven revenue models.

What role do neo-banks play in market expansion?

Neo-banks accelerate growth by embedding prepaid functionality in third-party apps, enabling instant digital issuance and cross-border scalability.

Page last updated on: July 7, 2025