Market Trends of Europe Aerospace and Defense Industry

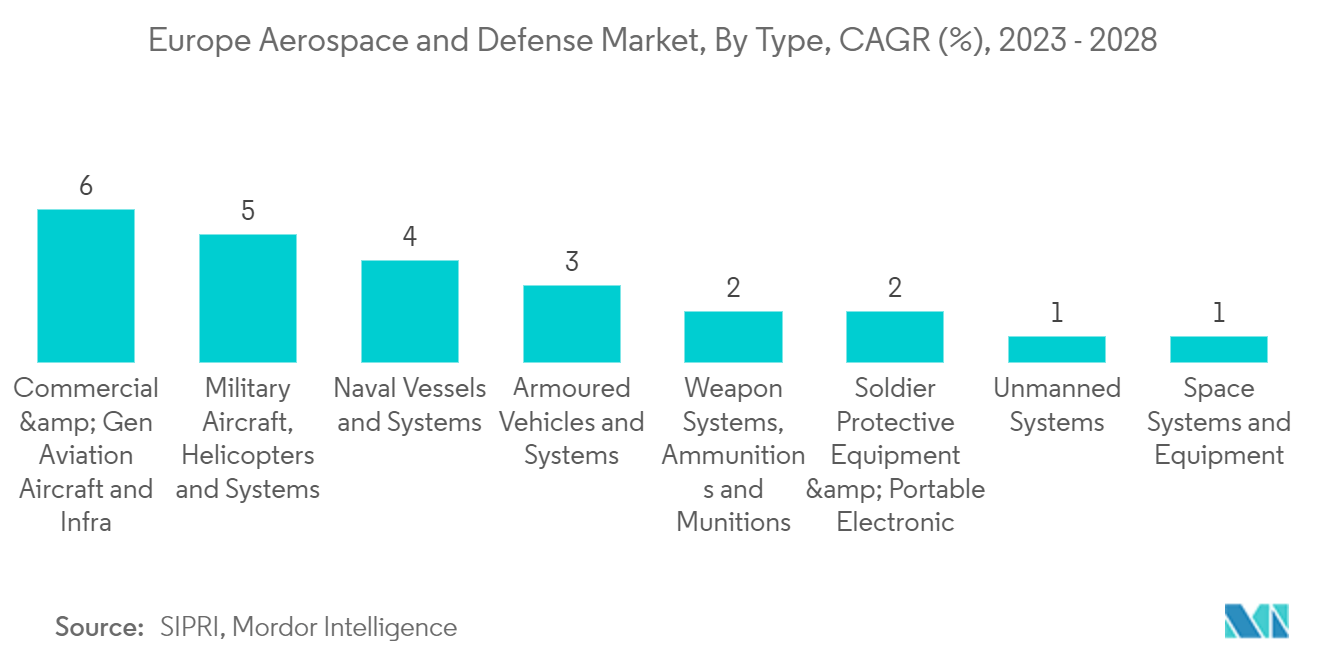

Commercial And General Aviation Aircraft And Infrastructure Segment is Expected to Witness Growth During the Forecast Period

- The commercial and general aviation aircraft and infrastructure segment is expected to experience growth during the forecast period. The prospect of a sustained recovery in the commercial aviation sector is becoming stronger due to passenger traffic data presented by the International Air Transport Association (IATA) in April 2022. According to the reports, passenger traffic in the European region witnessed a growth of approximately 50% in April 2022 compared to April 2021. The gradual relaxation of travel restrictions in various European countries in recent months has made air travel to European nations more accessible to passengers worldwide, resulting in a significant surge in international demand. The data presented by IATA also shows that international traffic from the European region grew by approximately 434.3% in March 2022 compared to March 2021.

- To facilitate the growth in passenger traffic, various airlines in the European region, such as Delta Airlines and International Airlines Group (IAG), have correspondingly increased their capacity within the European region. For example, Delta Airlines announced its plans to purchase 12 A220 aircraft from Airbus in July 2022.

- The COVID-19 pandemic led to accelerated corporate, consumer, and regulatory scrutiny of air travel emissions, limiting the expansion plans of various airports in the European region in the long term. Terminal bottlenecks remain a problem at various European airports. Before the pandemic, many airports were preparing for capacity expansion by issuing debt and accumulating cash to fund these investments.

- Heathrow Airport, for instance, had USD 3.79 billion in cash and committed undrawn lines earmarked for third runway construction at the beginning of 2020. However, most of these projects were delayed or canceled at the start of the pandemic, while the accumulated funds strongly supported liquidity during 2020-21. In the third quarter of 2021, the European region invested in five larger airport construction projects, with a total value of USD 1.3 billion, to cater to the ever-increasing passenger traffic at European airports.

- Although the European defense industry is not among the top defense industries worldwide, it employs approximately 500,000 personnel, which gives the industry additional importance beyond its inherent security aspect. The structure of the European defense industry is highly dispersed, with a few large players and about 1,350 small and medium-sized enterprises (SMEs). While companies are scattered over almost the whole EU, a few countries (Austria, Czech Republic, France, Germany, Italy, Poland, Spain, Sweden, and the United Kingdom) host the bulk of SMEs as well as top companies. The European defense industry has undergone various changes after the COVID-19 pandemic to be on par with various global defense industries.

- Thus, ongoing investments in both the aerospace and defense sector in Europe are likely to lead to market growth during the forecast period.

Understand The Key Trends Shaping This Market

Download Sample

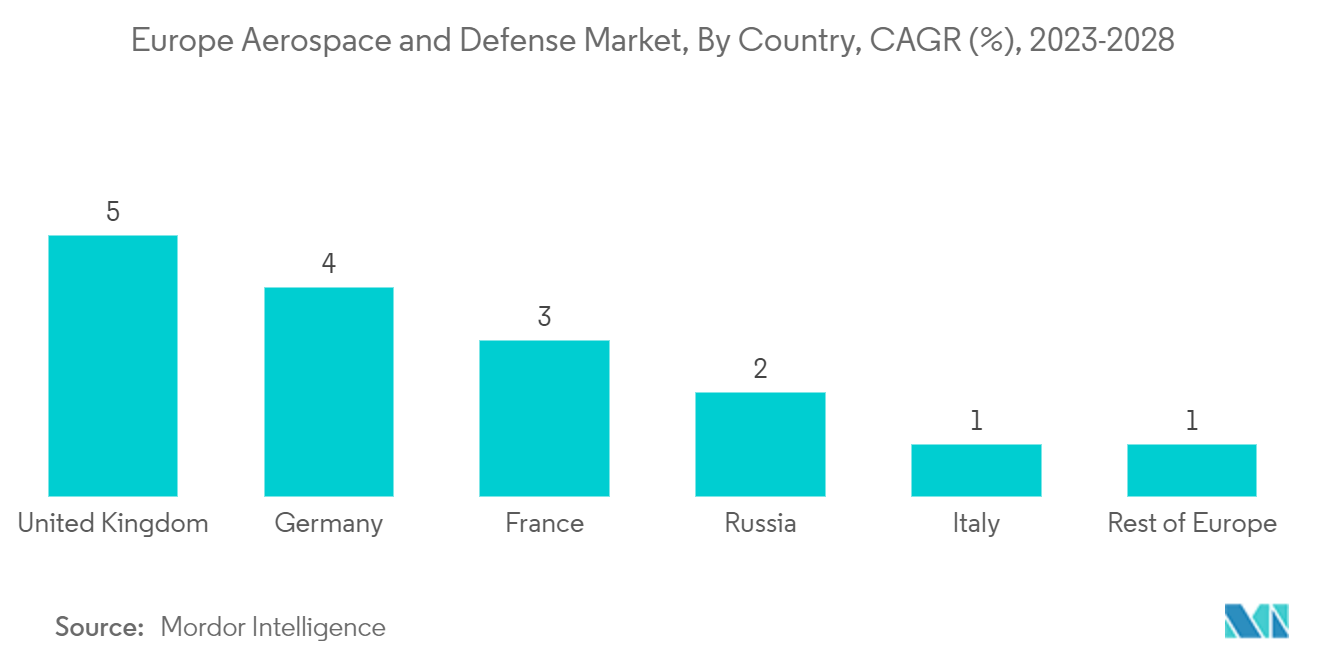

Germany is Expected to Witness Growth During the Forecast Period

- Germany's aerospace and defense sectors were adversely affected by COVID-19. With travel restrictions in place in many countries, aircraft manufacturing companies have experienced a decline in orders, resulting in a slowdown in the market's growth. However, in recent months, there have been indications of a recovery in demand for commercial aircraft.

- Despite these challenges, Germany remains one of Europe's leading economies and a major global spender on military and aerospace. The country is home to prominent defense manufacturers, including Rheinmetall AG, Diehl Stiftung & Co. KG, and Krauss-Maffei Wegmann GmbH & Co. KG, which are increasing the development of defense technologies and production rates through national and international investments, partnerships, and collaborations.

- The International Air Transport Association (IATA) predicts steady growth in Germany's aviation industry due to the increasing number of passengers in the country. To support this growth, the government is increasing its investments in airport infrastructure development.

- Germany is the third-largest spender on military and defense in Central and Western Europe, trailing behind France and the United Kingdom. Last year, the country allocated USD 56.0 billion, which represented 1.3% of its GDP.

- Although this amount was 1.4% lower than the previous year, the new German government, formed in December 2021, declared its intention to invest 3% of the country's GDP in diplomacy, development, and defense. In light of the Russian invasion of Ukraine in February 2022, the government aims to increase military spending further in the future, which will result in the growth of Germany's defense market in the years to come.

Get Analysis on Important Geographic Markets

Download Sample