Market Size of Distributed Control Systems Industry

| Study Period | 2019 - 2029 |

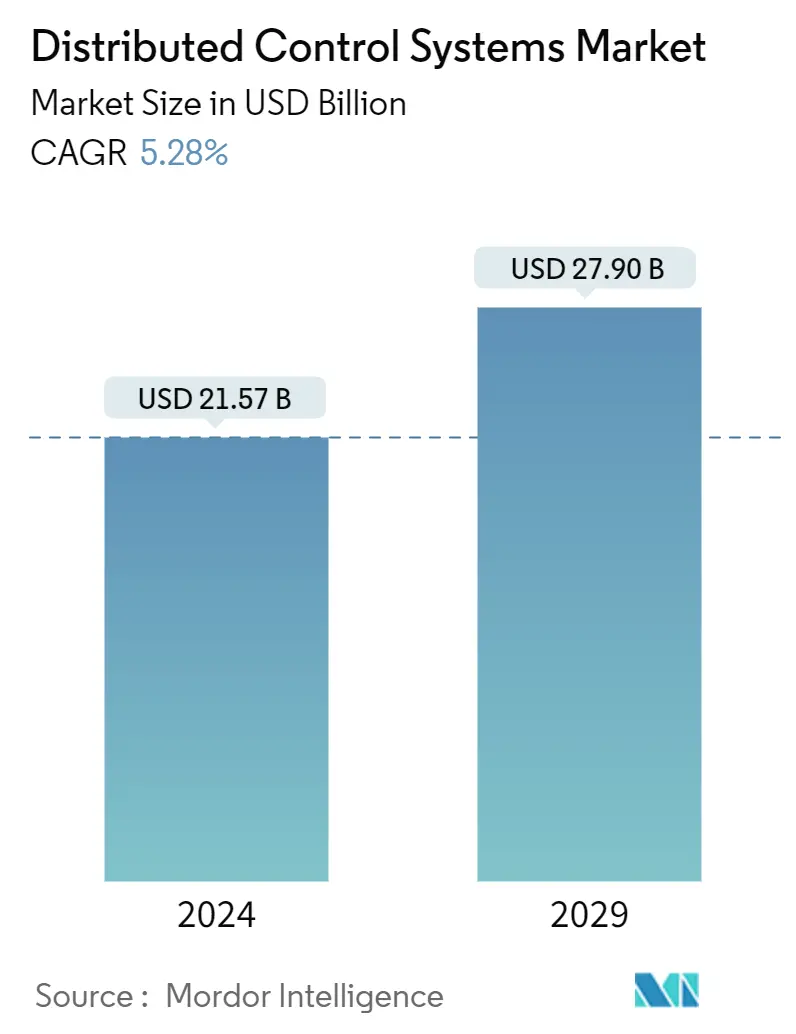

| Market Size (2024) | USD 21.57 Billion |

| Market Size (2029) | USD 27.90 Billion |

| CAGR (2024 - 2029) | 5.28 % |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

Major Players

*Disclaimer: Major Players sorted in no particular order |

Need a report that reflects how COVID-19 has impacted this market and its growth?

Distributed Control Systems Market Analysis

The Distributed Control Systems Market size is estimated at USD 21.57 billion in 2024, and is expected to reach USD 27.90 billion by 2029, growing at a CAGR of 5.28% during the forecast period (2024-2029).

The distributed control system market will be driven in the future by the tendency for manufacturers in the process industry to implement the best automation technologies to obtain a competitive edge in the current competitive environment.

The growing adoption of smart applications and IoT technologies are the key drivers for the market. With the increased adoption of smart devices, there is an increase in the demand for multifunctional microelectronics with reduced time delays and improved performance.

The process industry currently operates in a very complex environment, and the requirements for its control technology are correspondingly demanding. Control technology is a key lever for gaining a competitive edge in the process industry, all the more so if it can meet the tremendous challenges of both today and tomorrow. The latest iterations of DCS systems provide marked improvements over their predecessors regarding security, compatibility with the latest technology, and operator effectiveness, which drives the distributed control systems market.

COVID-19 had a significant impact on all industries worldwide. Because of the rapid growth, governments worldwide took stronger measures for functioning industrial plants and offices, resulting in stricter lockdowns. The lockdown significantly influenced the power sector as power demand from commercial and industrial sectors reduced significantly. For most businesses worldwide, the recovery phase following large losses during the pandemic was nearly completed.

According to Wind Europe, delays were expected in many new wind farm projects, causing developers to miss the deployment deadlines in the auction systems and face financial penalties due to COVID-19, The International Renewable Energy Agency stated that despite the pandemic threatening global supply chains in the power sector, it would not stop the industry from transitioning to net-zero CO2 emissions. The pandemic also showed how essential manufacturing automation was to modern industry functioning, with some fueled by social distancing and some by cyber threats. Social distancing measures had a greater impact as they led the manufacturers to restructure their operations to rely more on robotics.

However, the latest iterations of DCS systems provide marked improvements over their predecessors regarding security, compatibility with the newest technology, and operator effectiveness, a market driver for distributed control systems. Modern DCSs include new capabilities, such as asset diagnostics, performance monitoring, fleet management, alarm handling during the fault, prioritizing messages, and simplifying actions to be taken in the event of a failure. The purpose of the newer DCSs is to serve the entire lifetime of the power plant. The DCSs can be updated online, where updates and security patches are installed, and new features can be added without shutting down the plant.

Moreover, DCS is often employed in batch-oriented or continuous method operations, such as oil purification, power generation, organic compound manufacturing, craft, food and drink manufacturing, pharmaceutical production, and cement. DCSs can control various instrumentality types, including variable speed drives, quality control systems, motor control centers (MCC), kilns, manufacturing equipment, and mining equipment.

One of the significant benefits of DCS systems is that the digital communication between distributed controllers, workstations, and other computing elements follows the peer-to-peer access principle. To achieve greater precision and control in process industries, like the petrochemical, nuclear, and oil and gas industries, there is an increasing demand for controllers which offer specified process tolerance around an identified set point.

These requirements have driven the adoption of DCS, as these systems provide lower operational complexity, project risk, and functionalities, like flexibility for agile manufacturing in highly demanding applications. The ability of DCS to integrate PLCs, turbomachinery controls, safety systems, third-party controls, and various other plant process controls for heat exchangers, feedwater heaters, and water quality, among others, further drives the adoption of DCS in the energy sector.