Market Size of Display Panel Industry

| Study Period | 2019 - 2029 |

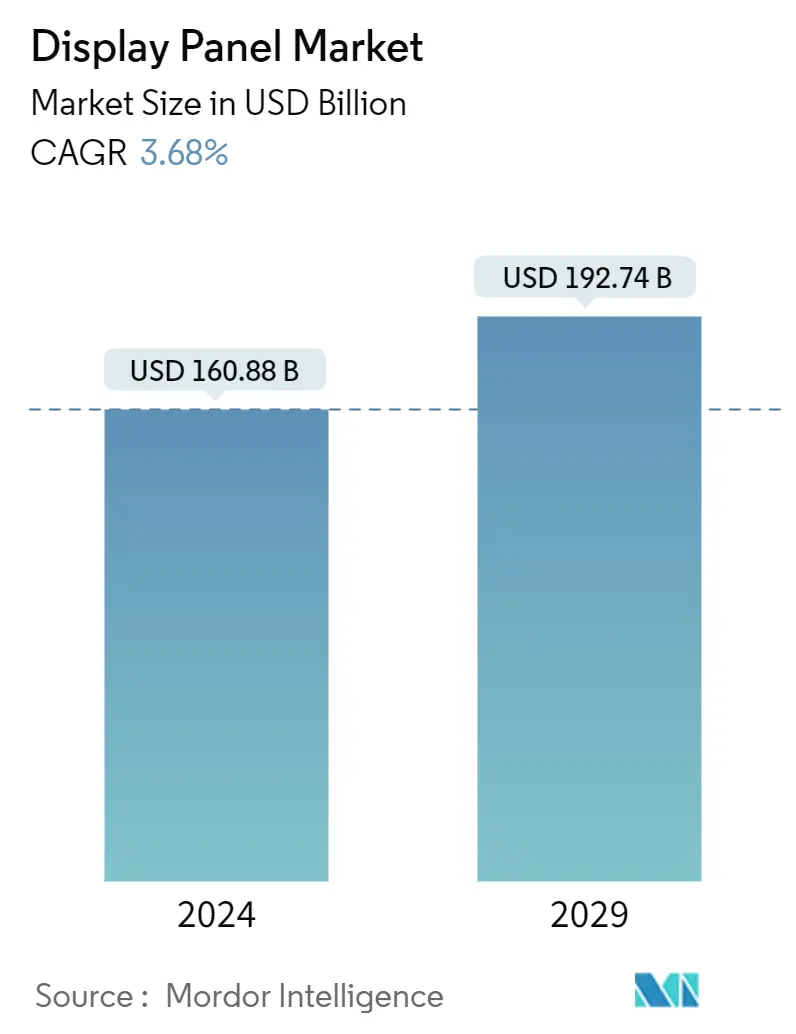

| Market Size (2024) | USD 160.88 Billion |

| Market Size (2029) | USD 192.74 Billion |

| CAGR (2024 - 2029) | 3.68 % |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

Major Players

*Disclaimer: Major Players sorted in no particular order |

Need a report that reflects how COVID-19 has impacted this market and its growth?

Display Panel Market Analysis

The Display Panel Market size is estimated at USD 160.88 billion in 2024, and is expected to reach USD 192.74 billion by 2029, growing at a CAGR of 3.68% during the forecast period (2024-2029).

Display technologies, aided by technological developments, have evolved over the years to offer higher resolution and lower power consumption. The developments in nanoparticles and transparent sensors in the electronic circuit have boosted the progression of the transparent display market. In the present scenario, development is progressing on replacing hard square panels with flexible displays that are more interactive to the consumer. This is expected to provide a substantial opportunity for the growth of the transparent display market.

The display market is driven by the growing demand for enhanced displays, such as OLED and PMOLED, augmented displays, and rollable transparent displays. OLED technology enables bright, efficient, and thin displays and lighting panels. They are currently used in numerous mobile devices, TVs, and lighting fixtures. OLED displays provide better image quality than LCD or Plasma displays - and can be made transparent and flexible.

Moreover, a significant application area of displays has been the heads-up display devices. These devices have witnessed strong demand from AR/VR, military and defense, and automotive markets, thereby driving the market for display panels. A device with a transparent display has a much higher resolution and displays much more realistic augmented reality than video augmented reality.

The growing demand for oxide TFT has encouraged players to increase their production capacity to compensate for the market demand. For instance, in December 2021, China Star Optoelectronics Technology (CSOT), a China-based display panel maker belonging to the TCL Group, announced setting up an 8.6G oxide TFT-LCD production line, with production scheduled to begin in first-quarter 2023.

Out of the hardware sales, head-mounted displays dominated the market. This results from the rising demand for higher-quality HMDs to support the ongoing demand for high-quality content and functionality improvements and provide an improved immersive experience to consumers, which can be achieved through transparent displays. This is expected to drive the market.

DriveAR platform from Nvidia uses a dashboard-mounted display overlaying graphics based on camera footage around the car, using a transparent display. This system points out everything from hazards to historic landmarks along the way. Following the platform's success, automotive manufacturing giants like Audi, Mercedes-Benz, Tesla, Toyota, and Volvo have signed up with the company to work with the technology.

In April 2023, Samsung announced to supply premium, next-generation display panels to Ferrari models. Through this, the company aims to expand beyond television and smartphones and target the fastest automotive market.

Due to the COVID-19 pandemic, Sony's business was impacted by factors such as restrictions on the movement of people across national borders, making it difficult for the company to send engineers to manufacturing hubs such as China and countries in Southeast Asia to help with new product launches or give instructions on manufacturing. Moreover, sales of Sony's products were also affected by global lockdowns and retailer closings.