Direct-to-Patient Healthcare Logistics Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Historical Data Period | 2020 - 2024 |

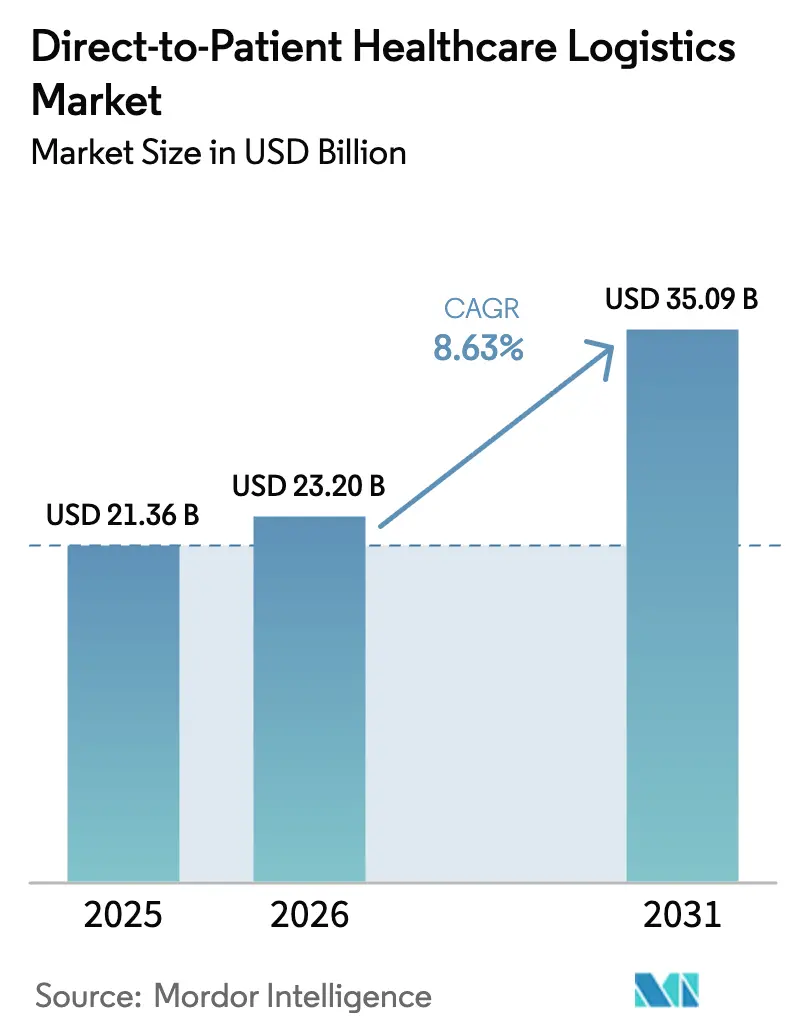

| Market Size (2026) | USD 23.2 Billion |

| Market Size (2031) | USD 35.09 Billion |

| Growth Rate (2026 - 2031) | 8.63% CAGR |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Direct-to-Patient Healthcare Logistics Market Analysis by Mordor Intelligence

The Direct-to-Patient Healthcare Logistics Market size was valued at USD 21.36 billion in 2025 and estimated to grow from USD 23.2 billion in 2026 to reach USD 35.09 billion by 2031, at a CAGR of 8.63% during the forecast period (2026-2031). Expanding adoption of decentralized and hybrid clinical trials, the surge in temperature-sensitive biologics, and the mainstreaming of e-pharmacies are reshaping distribution models toward doorstep delivery. Regulatory clarity, especially the FDA’s September 2024 decentralized clinical trial guidance, removes key barriers, allowing sponsors to ship investigational products directly to participants’ homes and spurring fresh investments in cold-chain infrastructure and digital visibility tools. Large logistics providers are deploying artificial-intelligence routing, IoT sensors, and blockchain tracking to improve compliance and reduce excursion risk, while smaller specialists carve out niches in labeling, kitting, and patient engagement platforms. Strategic outsourcing by pharma sponsors to qualified 3PL/4PL partners continues to accelerate market entry into emerging regions, widening access for hard-to-reach patient cohorts, and lowering fixed-cost burdens.

Key Report Takeaways

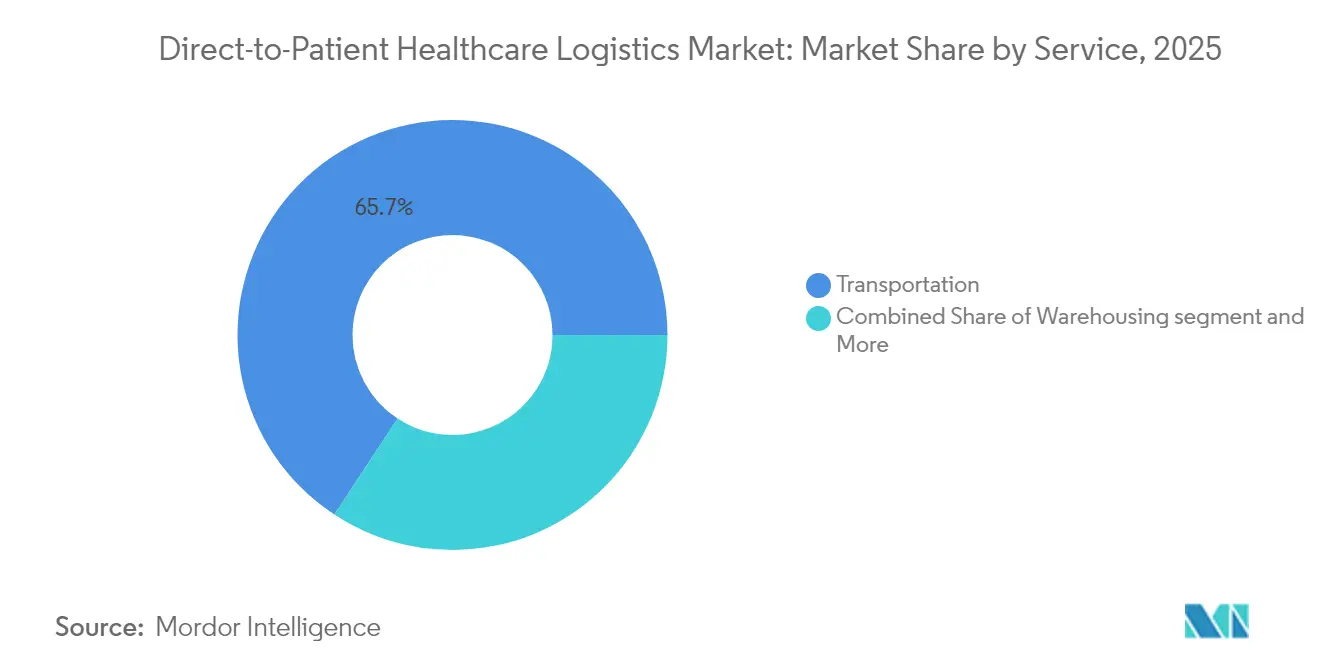

- By service, transportation held 65.74% revenue share of the direct-to-patient healthcare logistics market in 2025. The direct-to-patient healthcare logistics market for value-added services is projected to advance at an 11.02% CAGR between 2026-2031.

- By product, prescribed medicine delivery accounted for 47.88% of the direct-to-patient healthcare logistics market size in 2025. The direct-to-patient healthcare logistics market for home trial support services is forecast to expand at a 12.61% CAGR between 2026-2031.

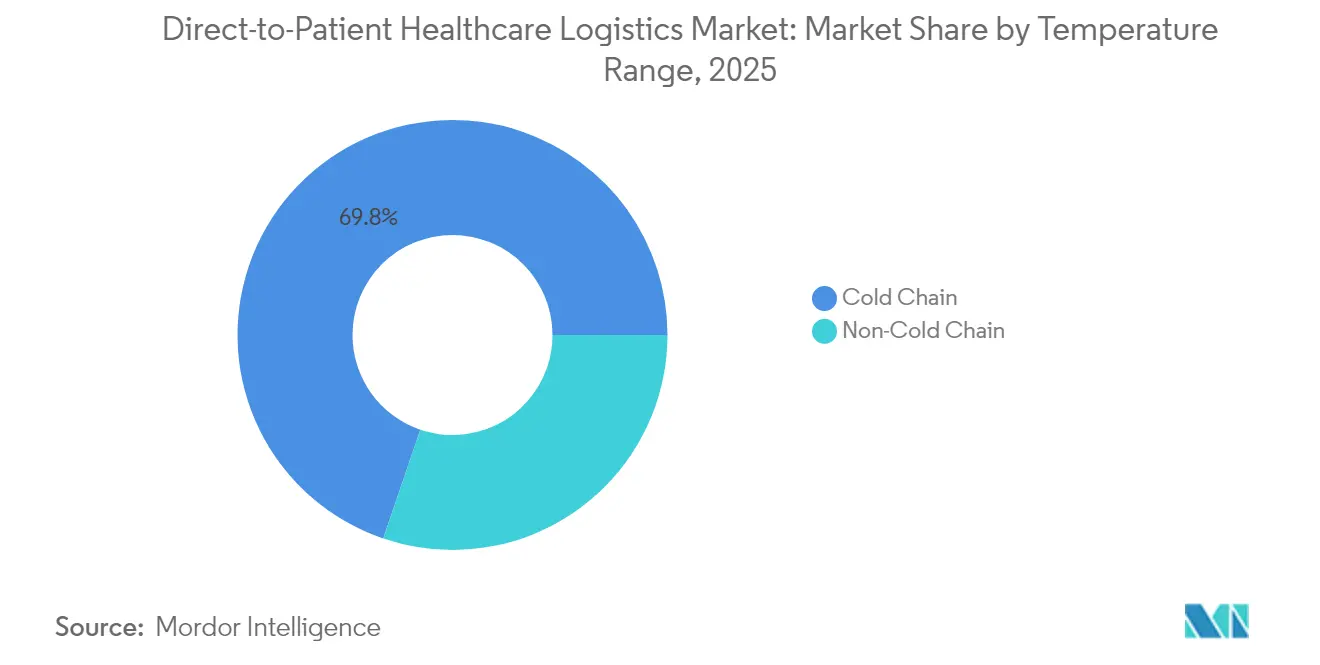

- By temperature range, cold chain captured 69.78% of the direct-to-patient healthcare logistics market share in 2025. The direct-to-patient healthcare logistics market for cold chain is growing at a 10.31% CAGR between 2026-2031.

- By end-user, pharma and biotech sponsors led with 44.62% of the direct-to-patient healthcare logistics market share in 2025. The direct-to-patient healthcare logistics market for home healthcare providers shows the fastest growth at 11.74% CAGR between 2026-2031.

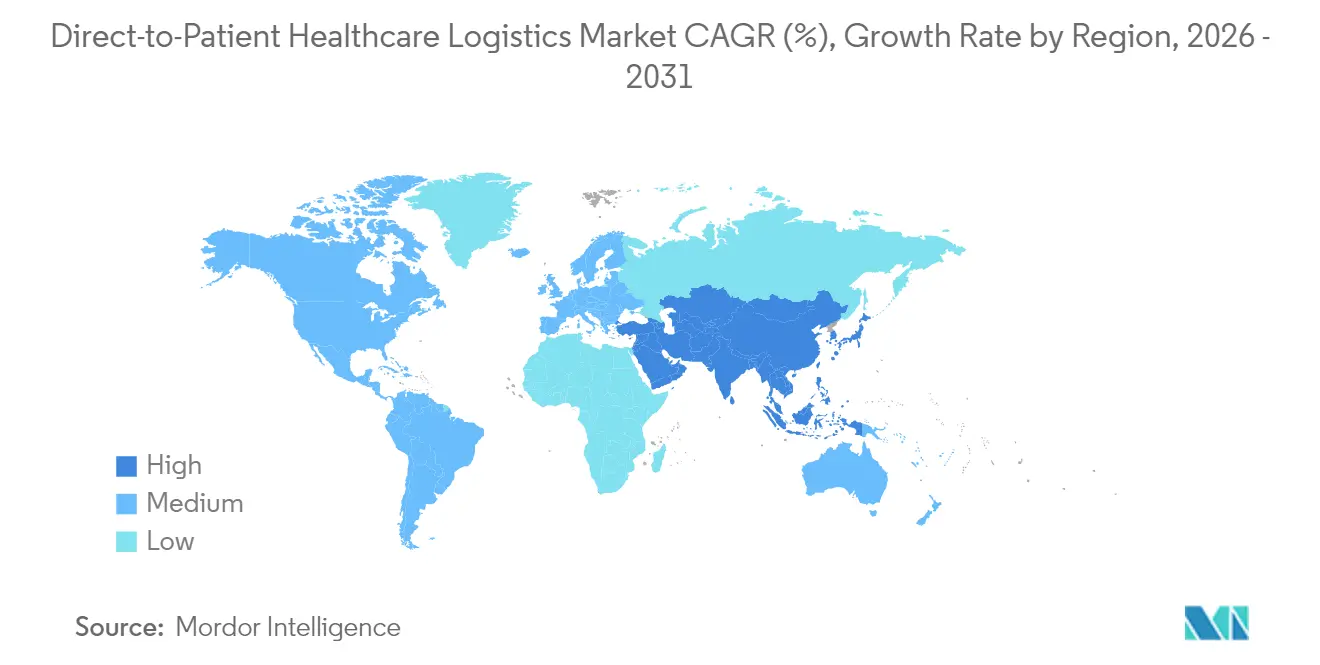

- By geography, North America commanded 39.95% of the direct-to-patient healthcare logistics market of 2025 revenues. The direct-to-patient healthcare logistics market for Asia-Pacific is projected to register an 10.69% CAGR between 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Direct-to-Patient Healthcare Logistics Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Accelerated Shift to Decentralized & Hybrid Clinical Trials Elevating At-Home Logistics Demand | +2.1% | Global, with early adoption in North America & Europe | Medium term (2-4 years) |

| Proliferation of High-Value Biologics and Cell & Gene Therapies Requiring Tight Cold-Chain DtP Delivery | +1.8% | North America & EU core, expanding to Asia-Pacific | Long term (≥ 4 years) |

| Mainstream Adoption of E-Pharmacies Driving Compliant Direct-to-Consumer Prescription Shipments | +1.5% | Global, with regulatory variations by region | Short term (≤ 2 years) |

| Demonstrated Improvement in Patient Adherence and Retention from Doorstep Medicine Delivery | +1.3% | Global, particularly effective in chronic disease management | Medium term (2-4 years) |

| IoT-Enabled End-to-End Temperature/Location Visibility Lowering Compliance Risk and Cost | +1.0% | Global, with faster adoption in developed markets | Short term (≤ 2 years) |

| Strategic Outsourcing to Specialist 3PL/4PL Providers Expanding Global DtP Reach at Lower Fixed Cost | +0.9% | Global, with emphasis on emerging markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Accelerated Shift to Decentralized & Hybrid Clinical Trials Elevating At-Home Logistics Demand

The FDA’s September 2024 guidance conclusively authorizes sponsors to ship investigational products directly to participants, framing clear rules on packaging, labeling, and accountability[1]Food and Drug Administration, “Decentralized Clinical Trials for Drugs, Biological Products, and Devices,” fda.gov. Sponsors now integrate telehealth visits, local nursing support, and home delivery to reduce patient burden and recruit diverse cohorts. Oncology trials benefit most because remote models mitigate travel fatigue for immunocompromised patients. Logistics providers have responded by adding real-time GPS- and temperature-enabled packaging; Patheon supports decentralized trials in more than 50 countries with cloud-connected smart kits. These advancements widen global reach while safeguarding product integrity.

Proliferation of High-Value Biologics and Cell & Gene Therapies Requiring Tight Cold-Chain DtP Delivery

Commercialization of cell and gene therapies demands cryogenic storage below –150 °C, driving capital investment in validated freezers, redundant power, and trained handlers. Chart MVE’s Fusion system offers 7-day hold times without sacrificial cryogen, a critical safeguard for last-mile risk mitigation. UPS Healthcare expanded capacity across six temperature zones by acquiring Frigo-Trans and BPL. Heightened FDA documentation on excursion management favors providers owning end-to-end chain-of-custody platforms, stimulating differentiation in a premium service tier.

Mainstream Adoption of E-Pharmacies Driving Compliant Direct-to-Consumer Prescription Shipments

The FDA’s January 2025 ACNU rule lets mobile apps guide over-the-counter drug selection, aligning digital retail with home deliveries. State pharmacy licensing still varies, but standardized good distribution practice frameworks reduce complexity for large mail-order hubs. DEA reporting obligations under 21 CFR 1304 elevate compliance costs, steering volume toward specialists fluent in controlled-substance telemetry. LillyDirect illustrates manufacturer-direct fulfillment that bypasses traditional PBM layers, pairing web ordering with overnight temperature-controlled shipping[2]Lilly, “LillyDirect: A Direct-to-Consumer Care Platform,” lillydirect.com.

Demonstrated Improvement in Patient Adherence and Retention from Doorstep Medicine Delivery

Peer-reviewed studies confirm higher refill persistence among home-delivery users; 64% report better quality of life through synchronized shipments and pharmacist follow-ups. AI-driven reminder engines personalize notifications, reducing alert fatigue that undermined earlier apps. COVID-19 pilot programs in Thailand showed lower drug-related problems when hospitals shifted to door-to-door distribution. These results underpin payer support for direct-to-patient models as cost-effective disease-management interventions.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Fragmented and Evolving Regulatory Requirements for Direct Dispensing and Cross-Border Shipments | -1.4% | Global, with particular complexity in Europe and emerging markets | Long term (≥ 4 years) |

| High Capital and Operating Costs of Validated Cryogenic Last-Mile Infrastructure | -1.1% | Global, with higher impact in cost-sensitive emerging markets | Medium term (2-4 years) |

| Rising Cyber-Security and Data-Privacy Risks Linked to Real-Time, Patient-Identifiable Telemetry | -0.8% | Global, with stricter enforcement in Europe and developed markets | Short term (≤ 2 years) |

| Liability Exposure from Temperature Excursions Across Fragmented Local Courier Networks | -0.6% | Global, with higher impact in regions with limited specialized infrastructure | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Fragmented and Evolving Regulatory Requirements for Direct Dispensing and Cross-Border Shipments

EU member states continue to enforce country-specific licensing and labeling rules despite EMA efforts to harmonize practices, complicating multi-country programs[3]European Medicines Agency, “2024 Guidance on Supply Chain Resilience,” ema.europa.eu. In the United States, multistate operations must juggle pharmacist-in-charge statutes and separate controlled-substance registrations, elevating legal overhead. Asia-Pacific adds language localization and in-country testing mandates; Thailand and Indonesia require local manufacturing partnerships before import approval. Large providers absorb compliance through dedicated regulatory teams, but smaller entrants face high entry hurdles.

High Capital and Operating Costs of Validated Cryogenic Last-Mile Infrastructure

Ultra-low freezers, back-up generators, 24/7 monitoring, and GDP-certified drivers raise both capital and running expenses. A single automated cryogenic vault can exceed USD 3 million, excluding ongoing calibration and re-validation outlays. DHL earmarked EUR 2 billion through 2030 for temperature-controlled vehicles and Pharma Hubs, a scale smaller firms cannot match. Insurance premiums rise alongside product values, and redundant systems—essential for cell therapy safety—inflate cost per shipment, pressuring margins outside high-income regions.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service: Transportation Dominance Faces Value-Added Services Disruption

Transportation services contributed 65.74% of 2025 revenue, anchoring the direct-to-patient healthcare logistics market through comprehensive road, air, and specialized courier networks. Growth now tilts toward service complexity over volume, as pharma sponsors demand six-zone temperature management and real-time telemetry. UPS Healthcare invested EUR 20 million to expand cold-chain fleets and attain CEIV Pharma accreditation in New York and Shanghai. Parallelly, value-added services—labeling, kitting, multilingual instructions, and nurse-coordinated adherence calls—are scaling fastest at an 11.02% CAGR because sponsors seek end-to-end patient engagement rather than isolated parcel drops. This evolution unlocks higher revenue per shipment while compressing cycle times between prescription, fulfillment, and outcome reporting.

Warehousing and distribution remain indispensable for buffer inventory, but their role shifts toward micro-fulfilment centers positioned closer to patients to shorten transit windows. Schreiner MediPharm’s smart e-labels embed NFC chips that relay dosing data, illustrating how labeling is morphing into a digital compliance node. Competitive intensity therefore migrates from pure haulage toward integrated platforms linking inventory control, data analytics, and patient support.

By Product: Prescribed Medicine Delivery Leads While Home Trial Support Accelerates

Prescribed medicine delivery held 47.88% of 2025 revenue, underpinned by chronic disease programs that ship monthly refills with synchronized delivery calendars. This base drives stable cash flows and reinforces the direct-to-patient healthcare logistics market’s resilience to macro shocks. Regulatory certainty on pharmacy-to-patient shipments and inclusion in payer formularies bolster uptake among diabetology and cardiovascular segments. Pre-clinical supplies, sample collections, and medical device dispatches add complementary revenue but grow at mid-single-digit rates.

Home trial support services register a 12.61% CAGR, propelled by the FDA’s endorsement of decentralized trial logistics. Sponsors increasingly outsource investigational product delivery, remote nursing kits, and reverse logistics for unused medication returns. Academic centers such as Johns Hopkins deploy dedicated depots for oncology studies, engaging specialist couriers for same-day cryogenic drop-offs.

By Temperature Range: Cold Chain Supremacy Driven by Biologics Expansion

Cold chain accounted for 69.78% of direct-to-patient healthcare logistics market share in 2025, reflecting soaring biologics volumes and strict stability profiles. Within this, the 2-8 °C band dominates, serving monoclonal antibodies, vaccines, and insulin analogues. However, the ultra-cold subset below –80 °C posts double-digit expansion as autologous cell therapies launch commercially. Innovations like Chart MVE’s Fusion freezer cut liquid-nitrogen reliance and extend hold times, reducing excursion risk during airport dwell phases. Ambient segments still serve small-molecule generics and OTC goods, but their proportional contribution declines as therapy portfolios skew biologic.

IoT-equipped payload trackers powered by 5G now predict temperature deviations before they occur, allowing proactive courier rerouting. Identec Solutions’ real-time dashboards integrate telemetry with customs documentation, trimming clearance delays and aligning with emerging traceability mandates. These technologies elevate compliance and help justify premium pricing on cold-chain tariffs within the direct-to-patient healthcare logistics market.

By End-User: Pharma Sponsors Lead While Home Healthcare Providers Surge

Pharma and biotech sponsors generated 44.62% of 2025 revenue, relying on direct-to-patient networks for patient support programs, compassionate-use shipments, and de-risked clinical supplies. Outsourced logistics reduces capital tied up in inventory and infrastructure, letting sponsors focus on R&D and commercialization. Contract research organizations leverage similar networks, but their growth moderates as sponsors internalize some decentralized trial logistics.

Home healthcare providers deliver the strongest trajectory at 11.74% CAGR as payers and health systems shift infusions, injections, and diagnostics into living rooms. UPS Healthcare’s Louisville Lab Port processes point-of-care tests and triggers same-day medication dispatches, demonstrating integrated diagnostics-to-therapy loops. Telemedicine platforms layer prescription and courier modules into virtual consults, aligning with value-based care metrics that reward reduced hospital readmissions.

Geography Analysis

North America generated 39.95% of 2025 revenue thanks to FDA guidance clarity, advanced cold-chain hubs, and mature reimbursement ecosystems. Canada’s universal coverage and Mexico’s near-shoring of fill-finish operations contribute incremental volumes. Cross-border harmonization under USMCA eases customs handling, curtailing dwell times at land gateways.

Europe follows, leveraging EMA supply-chain resilience initiatives but wrestling with member-state variance in pharmacist supervision, controlled-substance quotas, and data-privacy enforcement. GDP-certified depots cluster around Frankfurt, Liege, and Amsterdam for airfreight connectivity, feeding final-mile courier networks with real-time GDP audit trails.

Asia-Pacific is the fastest growing, clocking an 10.69% CAGR, driven by Japan’s relaxed home-delivery prescriptions, South Korea’s telehealth expansion, and Singapore’s push for regional cold-chain leadership. China invests in bonded pharma zones with integrated customs and quarantine labs, whereas India’s National Logistics Policy promotes multimodal temperature-controlled corridors. Diverse regulatory baselines slow pan-regional programs, yet harmonization via ASEAN joint assessments is making headway.

South America’s uptake centers on Brazil, where ANVISA updates have streamlined biologic import clearances and favored home-based care for oncology. Argentina and Colombia replicate pilot tele-oncology programs that hinge on assured last-mile delivery.

The Middle East and Africa remain nascent but attractive; Dubai’s Jebel Ali Free Zone and Saudi Arabia’s Vision 2030 investments fund GDP-graded warehousing and drone corridors for remote-area coverage.

Note: Segments share of all individual segments available upon report purchase

Competitive Landscape

The direct-to-patient healthcare logistics market is moderately fragmented. Global integrators—UPS Healthcare, DHL Group, and FedEx Health—consolidate transportation and warehousing, while niche firms specialize in cryogenic couriering, clinical-trial labeling, or patient-centric IT platforms. M&A momentum is high: UPS bought Andlauer Healthcare Group for USD 1.6 billion to deepen Canadian reach; DHL acquired CRYOPDP to add 600,000 annual specialty shipments. Vertical integration trends encompass pharmacy dispensing, telehealth, and data analytics, aiming to create seamless patient journeys from prescription to outcome.

Technology is the key differentiator. Providers deploy blockchain-anchored chain-of-custody ledgers, AI route optimizers, and machine-learning excursion predictors to gain payer and sponsor confidence. Start-ups focus on patient experience—offering two-hour delivery windows, multilingual chatbots, and biometric authentication—to edge out incumbents on service quality. Entry barriers rise as regulators impose GDP audits, data-privacy certifications, and evidence of validated multi-temperature lanes, favoring capital-intensive players.

Direct-to-Patient Healthcare Logistics Industry Leaders

Marken

World Courier (AmerisourceBergen)

DHL Supply Chain

FedEx Healthcare

Kuehne + Nagel

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: DHL Group launched a EUR 2 billion program to add GDP-certified Pharma Hubs, multi-temperature vehicle fleets, and AI-driven visibility tools worldwide.

- April 2025: UPS completed the USD 1.6 billion acquisition of Andlauer Healthcare Group, scaling cold-chain coverage across Canada.

- March 2025: DHL Group purchased CRYOPDP, integrating 15-country specialty-courier operations into its global network.

- February 2025: McKesson bought an 80% stake in PRISM Vision Holdings for USD 850 million to expand retina specialty logistics and clinical services.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the direct-to-patient (DtP) healthcare logistics market as every paid movement, storage, and ancillary service that delivers prescription medicines, clinical-trial supplies, medical devices, or diagnostic kits straight from a licensed depot or pharmacy to an identified patient or study participant's home, workplace, or care facility. Movements may be ambient, refrigerated, or frozen and are counted at the invoice value of logistics services, not the drug itself.

Scope exclusion: Standard wholesale deliveries to retail pharmacies, over-the-counter consumer parcels, and non-medical home deliveries are outside the frame of this analysis.

Segmentation Overview

- By Service

- Transportation

- Road

- Air

- Other Mode of Transport

- Warehousing & Distribution

- Value-Added Services (Labelling, Kitting, etc.)

- Transportation

- By Product

- Prescribed Medicine Delivery

- Pre-Clinical Supplies

- Home Trial Support Services

- Test-Sample Collection & Return

- Others

- By Temperature Range

- Cold Chain

- Ambient (15-25 °C)

- Refrigerated (2–8 °C)

- Frozen (0 °C to -20 °C)

- Ultra-Cold / Cryogenic (-20 °C to -150 °C)

- Non Cold Chain

- Cold Chain

- By End-User

- Pharma & Biotech Sponsors

- Contract Research Organisations (CROs)

- Home-Healthcare Providers

- Retail & Online Pharmacies

- Other End Users

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Peru

- Chile

- Argentina

- Rest of South America

- Asia-Pacific

- India

- China

- Japan

- Australia

- South Korea

- South East Asia (Singapore, Malaysia, Thailand, Indonesia, Vietnam, and Philippines)

- Rest of Asia-Pacific

- Europe

- United Kingdom

- Germany

- France

- Spain

- Italy

- BENELUX (Belgium, Netherlands, and Luxembourg)

- NORDICS (Denmark, Finland, Iceland, Norway, and Sweden)

- Rest of Europe

- Middle East And Africa

- United Arab Emirates

- Saudi Arabia

- South Africa

- Nigeria

- Rest of Middle East And Africa

- North America

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interviewed hospital pharmacists, clinical operations managers, last-mile carriers, and packaging engineers across North America, Europe, and Asia. These discussions tested initial model outputs, filled price-per-parcel gaps, and clarified how cold-pack durability or doorstep failure rates shift costs in real life.

Desk Research

We gathered foundational numbers from open datasets such as United States FDA Drug Supply Chain Security Act serialization filings, Eurostat extra-EU pharmaceutical trade tables, and Japan's PMDA cold-chain guidance updates. Insights on shipment volumes and parcel mix came from trade bodies like the Parenteral Drug Association and the Global Cold Chain Alliance, while peer-reviewed journals in Clinical Trials and Therapeutics outlined adoption rates for decentralized studies. Our team also mined listed company 10-Ks, investor decks, and healthcare logistics tender portals, then verified firmographics through D&B Hoovers and news flows on Dow Jones Factiva. The sources cited illustrate typical inputs; many additional publications and databases informed the desk work.

Market-Sizing & Forecasting

The model starts with a top-down reconstruction of the global healthcare spend funneled through home delivery and decentralized trials, using indicators such as chronic prescription e-fill percentages, active decentralized trial count, average parcels per patient, cold-chain share, and inflation-adjusted freight indices. Supplier roll-ups of sampled lane volumes and average service prices provide a bottom-up sense check that allows us to tune key coefficients. Forecasts rely on a multivariate regression where parcel growth is explained by internet penetration, chronic disease prevalence, and regulatory deadlines like DSCSA, before an ARIMA overlay smooths short-term shocks. When country-level bottoms-up data are thin, gaps are bridged with validated regional penetration ratios obtained from expert calls.

Data Validation & Update Cycle

Outputs pass three-layer reviews: automated variance scans, peer cross-checks, and a lead analyst sign-off. We refresh each dataset annually, triggering interim updates if policy shifts, material M&A, or supply disruptions alter baselines. Clients therefore receive a model that is current to within the last quarter.

Why Mordor's Direct-to-Patient Healthcare Logistics Baseline Earns Trust

Published values rarely match because firms pick different service buckets, price bases, or refresh cadences. Sponsors sometimes quote only medicine parcels, whereas others mix in clinical-trial kits or value-added services.

Key gap drivers include scope width (our definition folds in cold-chain and device returns; many studies ignore these), assumption rigor around doorstep success rates, currency year normalization, and whether the analyst adjusts for rising biologic payload sizes. Mordor's annual refresh and dual-approach modeling help us avoid over or under stating the opportunity.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 21.36 B (2025) | Mordor Intelligence | |

| USD 9.12 B (2024) | Regional Consultancy A | Excludes clinical-trial flows and device deliveries; older base year; lower parcel-per-patient ratio |

| USD 19.10 B (2024) | Global Consultancy B | Counts only prescribed medicines and keeps prices in constant 2020 USD without inflation lift |

| USD 2.14 B (2024) | Industry Association C | Focuses solely on DtP clinical-trial logistics, omitting commercial home pharmacy shipments |

In short, while other publishers offer useful snapshots, Mordor's disciplined scope choices, blended modeling, and timely updates provide a balanced, transparent baseline that decision-makers can trace back to real-world variables and replicate with confidence.

Key Questions Answered in the Report

What is the current value of the direct-to-patient healthcare logistics market?

The market is valued at USD 23.2 billion in 2026 and is projected to hit USD 35.09 billion by 2031.

Which service segment dominates the direct-to-patient healthcare logistics market?

Transportation services dominate with 65.74% revenue share in 2025, primarily due to cold-chain requirements.

Why is cold chain logistics growing faster than ambient services?

The commercialization of biologics and cell & gene therapies requires tight temperature control, pushing cold chain volumes and infrastructure investment.

Which region shows the fastest growth through 2031?

Asia Pacific leads with an 10.69% CAGR, supported by regulatory harmonization and expanding healthcare access.

What are the main barriers to entry for new logistics providers?

High capital costs for validated cryogenic infrastructure and fragmented international regulations pose significant hurdles.

How are logistics firms improving patient adherence?

They combine doorstep delivery with AI-driven reminders, pharmacist follow-ups, and smart packaging that tracks dosing behavior.

Page last updated on: