Market Size of Cancer Vaccines Industry

| Study Period | 2019 - 2029 |

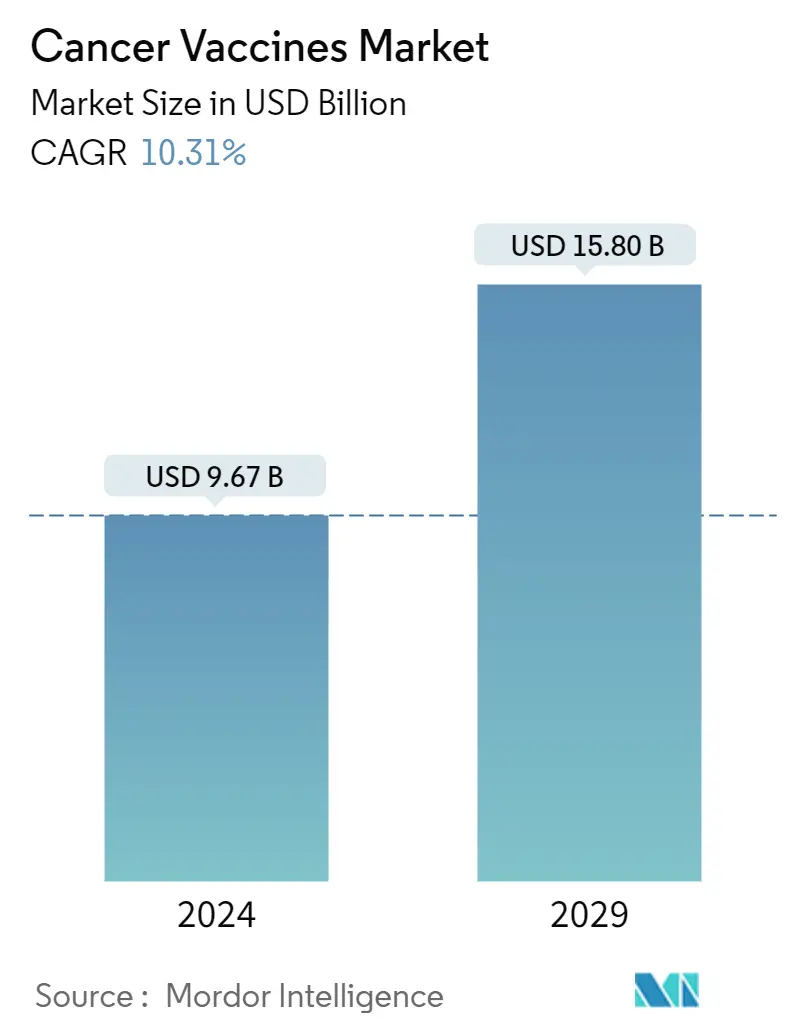

| Market Size (2024) | USD 9.67 Billion |

| Market Size (2029) | USD 15.80 Billion |

| CAGR (2024 - 2029) | 10.31 % |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

Major Players

*Disclaimer: Major Players sorted in no particular order |

Need a report that reflects how COVID-19 has impacted this market and its growth?

Cancer Vaccines Market Analysis

The Cancer Vaccines Market size is estimated at USD 9.67 billion in 2024, and is expected to reach USD 15.80 billion by 2029, growing at a CAGR of 10.31% during the forecast period (2024-2029).

The COVID-19 pandemic had an adverse effect on the global economy and healthcare system. Pharmaceuticals, medical gadgets, and biotechnological items were all affected by the worldwide lockdown. Research and development, on the other hand, took center stage. Many countries stopped their asymptomatic cancer screening programs due to the need to divert medical personnel and resources to the pandemic response. In March 2020, the governments of Wales and Scotland stopped funding breast, cervical, and bowel cancer screening programs. The Centers for Medicare & Medicaid Services in the United States encouraged healthcare institutions to delay screenings because they were a low-priority service. Several clinical experiments were put on hold due to COVID-19, at least during the pandemic's peak. Apart from the potential health benefits for those currently enrolled in studies, a phase 3 cancer clinical study typically costs at least USD 20 million. As a result, the production of cancer vaccines and other current clinical trials was suspended throughout the pandemic, and it is predicted that the market suffered as a result.

On the other hand, according to a JCO Global Oncology Journal article published in October 2021, the Dubai Health Authority reviewed and adjusted all center-specific guidelines and policies for each center-specific cohort to maintain high-quality oncology care throughout the nation. Other quality requirements included preventing interruptions of IV chemotherapy services, increasing the use of granulocyte colony-stimulating factor support, and providing coverage for antibiotics. The expansion of the industry is also being fueled by such government initiatives. Therefore, the market first witnessed a short-term negative impact due to the shift in research focus toward the development of COVID-19 vaccines. However, the relaxation of strict regulations during the post-pandemic period is expected to contribute to the growth of the market.

Certain factors driving the growth of the cancer vaccine market include the increasing number of cancer cases, rising investments and government funding in developing cancer vaccines, and technological developments in cancer vaccines. As per the International Agency for Research on Cancer's published GLOBOCAN 2020 report, which estimated the incidence and mortality of 36 cancers in 185 countries globally, there were an estimated 19,292,789 new cases of cancer diagnosed in 2020, and about 9,958,133 people died due to cancer all over the world. From the total number of diagnosed cancer cases, 10,065,305 cases were reported in males and 9,227,484 cases were reported in females. The incidence of cancer cases in males was expected to reach 15,585,096 by 2040 and 13,302,846 in females by 2040. Such an increasing incidence of cancer among the global population is expected to drive the growth of the market. Similarly, as per the data published by the European Cancer Information System in 2020, the estimated incidence of non-melanoma skin cancer in 2020 was 2,681,958 and was expected to be 3,244,076 by 2040. Such an increasing incidence of cancer in various countries is expected to drive the demand for cancer vaccines, which is expected to propel market growth over the forecast period.

Cancer vaccines play a vital role in the maintenance of the immune system, as they are considered to be biological response modifiers. These cancer vaccines target the infectious agents that may cause cancer through the production of antibodies. Moreover, as the number of cancer cases increases, the development of new cancer vaccines is also increasing for the treatment and prevention of the disease. For instance, in March 2021, eTheRNA, a Belgian-based immunotherapy company, received a USD 6.87 million grant from the European Commission to accelerate the clinical development of mRNA-based vaccines for cervical cancers. Furthermore, in November 2020, Moderna Inc. released interim data from the expansion cohort of its ongoing Phase 1 study of its mRNA personalized cancer vaccine (PCV), mRNA-4157, in combination with Merck's Keytruda, and results demonstrated that the vaccine candidate is well tolerated at all dose levels and produced responses as measured by tumor shrinkage in HPV-negative head and neck squamous cell carcinoma (HNSCC) patients.

However, the stringent regulatory issues, along with longer timelines in manufacturing vaccines and the availability of alternative therapies such as immunotherapy, act as major hindering factors in the cancer vaccine market's growth.