Market Trends of Ballast Water Treatment Industry

This section covers the major market trends shaping the Ballast Water Treatment Market according to our research experts:

Bulk Carriers by Fleet Type to Drive the Market

- A bulk carrier, also known as a bulker, is a merchant ship specifically intended to transport unpackaged bulk goods in its cargo holds, such as grains, coal, ore, steel coils, and cement. Bulk carriers are vital to the shipping industry because of the ease of transporting vast volumes of goods.

- The bulk carriers' segment is anticipated to observe a notable extension in the Ballast water treatment market during the forecast period. Today's bulk carriers are specially designed to maximize capacity, safety, efficiency, and durability. Japan, the Republic of Korea, and China account for the world's primary bulk carrier production countries.

- The ballast water treatment market is facing increased demand for treatment technologies ahead of an International Maritime Organization (IMO) compliance deadline in 2024.

- The United Nations Conference on Trade and Development, in its review of the Maritime Transport 2022 report, stated the fact that since 2017, the Marine Environmental Protection Committee (MEPC) established an experience-building phase (EBP) associated with the Ballast Water Management (BWM) Convention, 2004, to carry out a systematic and evidence-based review of this Convention. Following a data analysis report on the EBP, the MEPC, in June 2022, agreed in principle to develop a BWM Convention Review Plan. As of 15 July 2022, the BWM Convention had 91 contracting states representing 92% of the gross tonnage of the world's merchant fleet.

- According to the UNCTAD report, as of January 2022, the top five ship-owning economies accounted for 53% of global fleet tonnage. Greece accounted for 18% of the 55market, followed by China (13%), Japan (11%), Singapore (6%), and Hong Kong SAR (5%). 94% of global shipbuilding occurred in China, the Republic of Korea, and Japan in 2021.

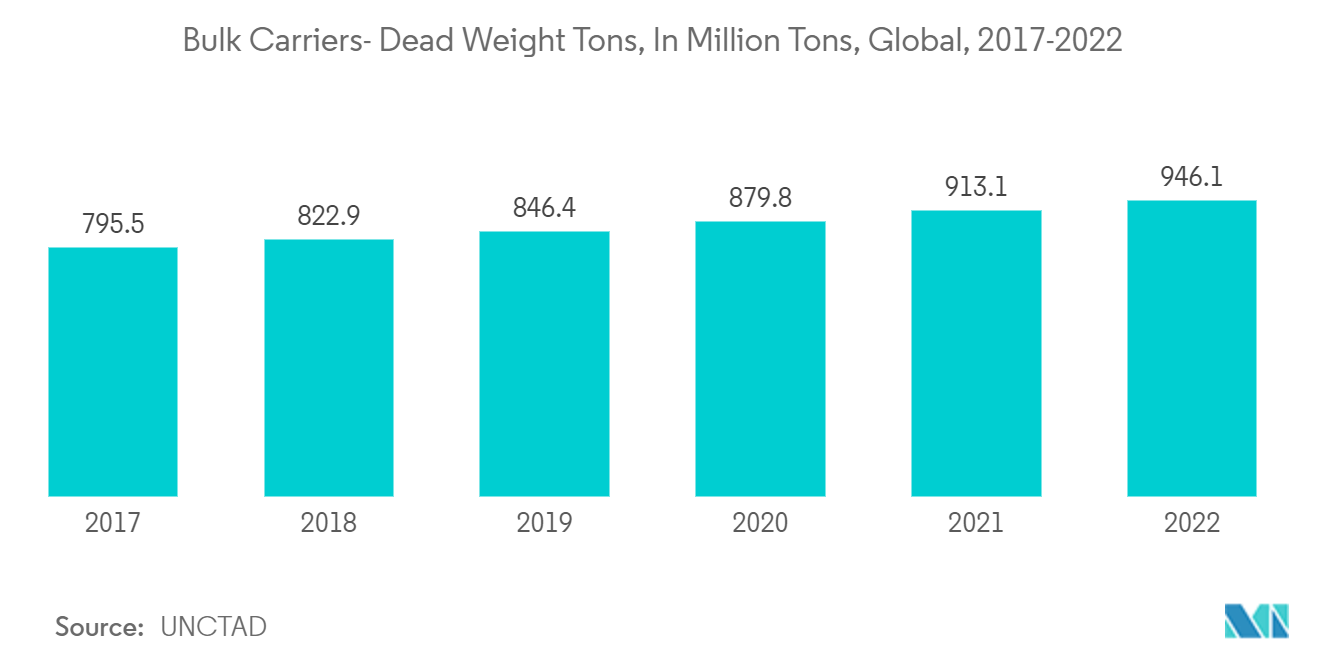

- It is also anticipated that bulk carriers had the largest deadweight cargo in 2022, around 946 million dwt, approximately 3.5% more than the previous year's value. Bulk carriers also had the largest market share in 2022, accounting for around 43% of total dead weight tonnage worldwide.

- The growing number of bulk carriers with increasing technological advancements, as well as safety procedures to reduce the number of dangerous emissions from such a large number of ships, are predicted to propel the ballast water treatment industry forward.

Understand The Key Trends Shaping This Market

Download Sample

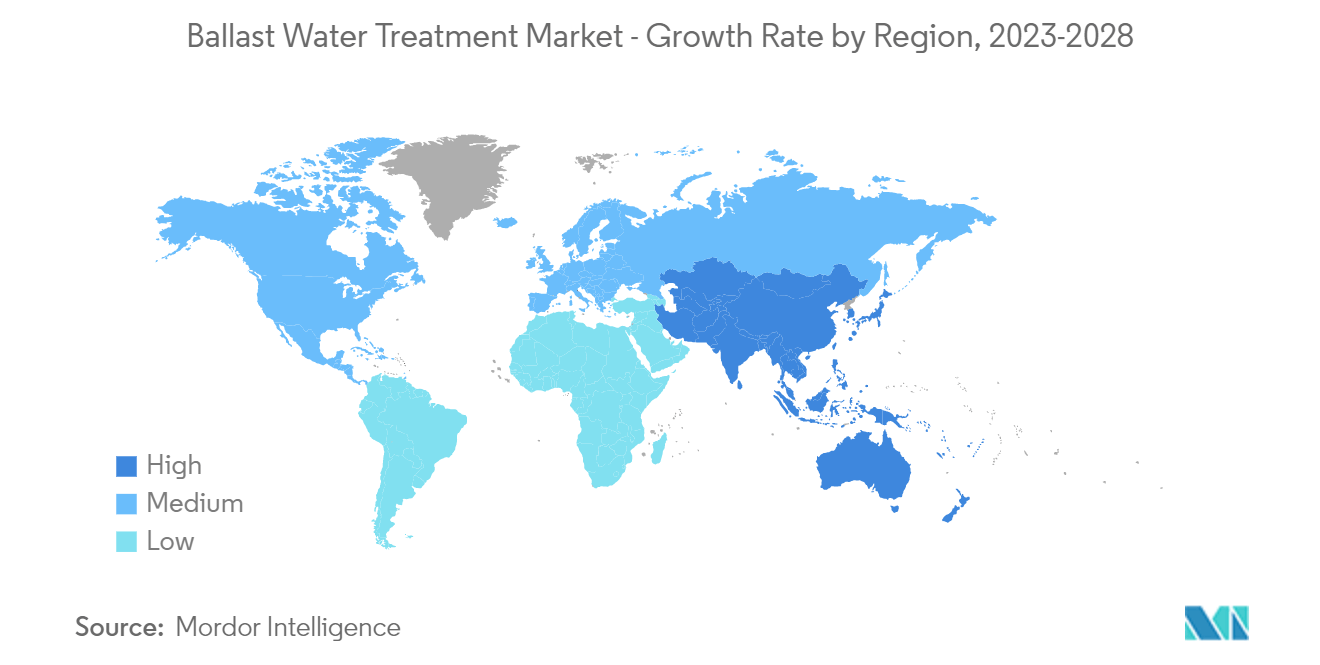

Asia-Pacific to Dominate the Market

- During the projected period, Asia-Pacific is expected to have the biggest ballast water treatment market share. A significant number of ports and harbors for the trade of oil and chemicals, automotive components, electronic components, and devices, among other things, add to Asia-Pacific market growth.

- The region further offers different types of vessels, such as containers, tankers, and other cargo ships. Since the IMO made it compulsory to install BWT systems in the vessel, it is presumed to drive BWT systems demand. Moreover, current trade volumes and stringent IMO regulations have encouraged the growth of this industry in the region.

- The United Nations Conference on Trade and Development (UNCTAD) stated in its report that the Asia Pacific region had a total of about 957 million dwt, out of which the major share was of bulk carriers with about 45% or close to 438 million dwt of the total share. The dwt of the total fleet saw a minor increase of about 2% in the year 2022 when compared with the previous year.

- According to the UNCTAD assessment, China had the largest share of dead weight tonnage in the whole fleet in 2022. China's share was approximately 115 million dwt or 13% of the total dwt. Bulk carriers were the largest shareholder, accounting for around 68 million deadweight tonnes, or 60% of total dwt.

- According to the Ministry of Industry and Information Technology (MIIT), China placed first in new orders in the first half of 2022, with a share of 50.8% along with the fact that China's shipbuilding industry completed 18.5 million deadweight tons (DWT) worth of orders during the period.

- In March 2021, the Indian government also launched the Maritime India Vision 2030 (MIV) 2030 (a Sagarmala venture) to boost the Indian maritime sector. The country intends to boost cargo flow from 73 million tons per annum (MTPA) to more than 200 MTPA with the MIV 2030 initiative.

- With an increase in ocean freight volumes from numerous nations such as China, India, and South Korea to other areas, this region remains a significant growing market for Ballast Water Treatment. It is projected that future expansion in maritime freight will result in higher acceptance of the Marine Environmental Protection program, which will support market growth.

- An increasing number of container tankers & ships and substantial trade volume in the region further supplement the regional growth.

Get Analysis on Important Geographic Markets

Download Sample