Market Size of Australia Cold Chain Logistics Industry

| Study Period | 2020 - 2029 |

| Base Year For Estimation | 2023 |

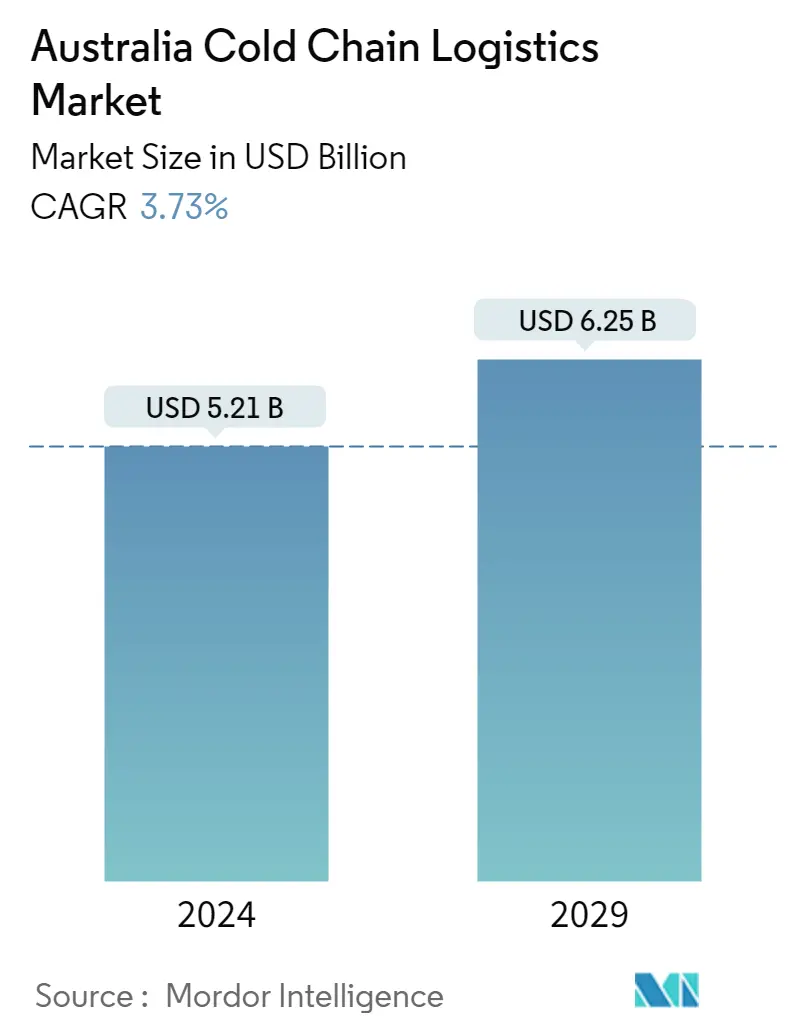

| Market Size (2024) | USD 5.21 Billion |

| Market Size (2029) | USD 6.25 Billion |

| CAGR (2024 - 2029) | 3.73 % |

| Market Concentration | Low |

Major Players

*Disclaimer: Major Players sorted in no particular order |

Need a report that reflects how COVID-19 has impacted this market and its growth?

Cold Chain Logistics Australia Market Analysis

The Australia Cold Chain Logistics Market size is estimated at USD 5.21 billion in 2024, and is expected to reach USD 6.25 billion by 2029, growing at a CAGR of 3.73% during the forecast period (2024-2029).

- The Australian cold chain logistics market was severely impacted by the pandemic. Not only did the abrupt closure of Australia's borders and subsequent closure of passenger routes result in a halt in human movement, but it also impacted transport cargo capacity in and out of Australia. The previous routes were no longer as easily accessible for businesses looking to move goods in and out of the country, and prices for the limited opportunities available were at a premium. Australia is a major player in the production and export of perishable goods, with the largest share of the country's cold chain logistics market.

- According to the data from the Australian Bureau of Statistics, more than a third of all businesses (37%) experienced supply chain disruptions in February 2022. This latest data shows that supply chain issues had decreased since January, when nearly half of all businesses (47%) reported having them, but have remained elevated since the survey was last collected in April 2021. According to the report, the most common supply chain issue facing businesses is domestic and international delivery delays (88%), followed by supply constraints (80%) and price increases (75%).

- Every year, 7.6 million tonnes of food are wasted in Australia, costing USD 37 billion, with flaws in the cold chain playing a significant role. Food demand will increase by 50% over the next ten years, while energy demand will increase by 50%, and water demand will increase by 30%. The National Construction Code (NCC) specifies insulation for everything, and there is no standard or regulation for insulation in the cold chain followed. One area where Australia falls far short is in necessities such as standardized truck widths and pallet sizes. The rest of the world uses 2.6-meter pallets, while Australians use 2.5-meter pallets, which causes overloading, reduced airflow, and other issues.

- Despite the rising challenges in the market, cold chain logistics is experiencing growth in Australia due to the surge in demand for food products, meat, pharmaceuticals, and other goods which require temperature requirement and end-to-end delivery. Furthermore, there is growth in the market because of the supply of vaccines which require temperature controlled environment until it is administered to the citizens.

- One more trend in the market is the growth of e-commerce in the sector; this has created opportunities for wholesalers and retailers to deliver their products directly to customers. Many products which are sold through e-commerce distribution channels require cold chain logistics, and the ease of product availability has propelled the logistics partners to provide facilities for the smooth movement of these products to the consumers without any damage. These trends, along with some others, are expected to drive the market in the forecast period despite the challenges rising in the industry.

Cold Chain Logistics Australia Industry Segmentation

A cold chain is a temperature-controlled supply chain. Cold chain logistics is the technology and process that allows the safe transport of temperature-sensitive goods and products along the supply chain. A complete background analysis of the Australia Cold Chain Logistics Market, including the assessment of the economy and contribution of sectors in the economy, market overview, market size estimation for key segments, and emerging trends in the market segments, market dynamics, and geographical trends, and COVID-19 impact is included in the report.

The Australia cold chain logistics market is segmented by service (storage, transportation, and value-added services), temperature type (chilled and frozen), and application (fruits and vegetables, dairy products, meat and seafood, processed food, pharmaceuticals (include biopharma), bakery and confectionery, and other applications). The report offers market sizes and forecasts in values (USD billion) for all the above segments.

| By Services | |

| Storage | |

| Transportation | |

| Value-added Services (Blast Freezing, Labeling, Inventory Management, etc.) |

| By Temperature Type | |

| Chilled | |

| Frozen |

| By Application | |

| Fruits & Vegetables | |

| Dairy Products | |

| Meat and Seafood | |

| Processed Food | |

| Pharmaceuticals (Include Biopharma) | |

| Bakery and Confectionery | |

| Other Applications |

Australia Cold Chain Logistics Market Size Summary

The Australian cold chain logistics market is anticipated to expand in the forecast period, driven by a surge in demand for temperature-sensitive goods such as food products, meat, and pharmaceuticals. The market growth is also fueled by the supply of vaccines that necessitate a temperature-controlled environment. Additionally, the e-commerce sector's expansion has created opportunities for wholesalers and retailers to deliver their products directly to customers, many of which require cold chain logistics. Despite challenges such as supply chain disruptions and delivery delays, the market is expected to grow. The Australian cold chain logistics market is fragmented, with numerous local players catering to the rising demand. Key players include Americold, Newcold Advanced Cold Logistics, Karras Cold Logistics, and Auscold Logistics PTY Ltd. The market also features other significant players such as MFR Cool Logistics, AGRO Merchants Group LLC, PakCan, ChillFreeze Logistics & Storage, and Chill WA. While international players are attempting to enter the market, the dominance of local companies and market challenges pose obstacles. However, the opportunities in the sector are expected to pave the way for their entry.

Explore MoreAustralia Cold Chain Logistics Market Size - Table of Contents

-

1. MARKET SEGMENTATION

-

1.1 By Services

-

1.1.1 Storage

-

1.1.2 Transportation

-

1.1.3 Value-added Services (Blast Freezing, Labeling, Inventory Management, etc.)

-

-

1.2 By Temperature Type

-

1.2.1 Chilled

-

1.2.2 Frozen

-

-

1.3 By Application

-

1.3.1 Fruits & Vegetables

-

1.3.2 Dairy Products

-

1.3.3 Meat and Seafood

-

1.3.4 Processed Food

-

1.3.5 Pharmaceuticals (Include Biopharma)

-

1.3.6 Bakery and Confectionery

-

1.3.7 Other Applications

-

-

Australia Cold Chain Logistics Market Size FAQs

How big is the Australia Cold Chain Logistics Market?

The Australia Cold Chain Logistics Market size is expected to reach USD 5.21 billion in 2024 and grow at a CAGR of 3.73% to reach USD 6.25 billion by 2029.

What is the current Australia Cold Chain Logistics Market size?

In 2024, the Australia Cold Chain Logistics Market size is expected to reach USD 5.21 billion.