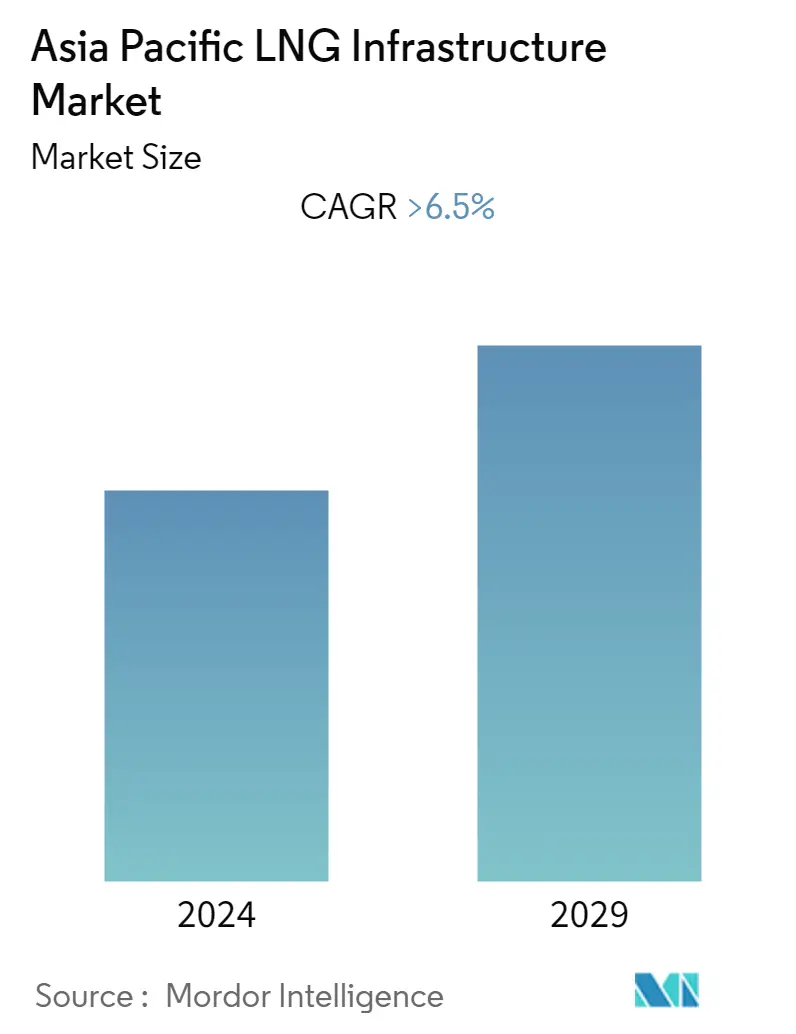

Market Size of Asia Pacific LNG Infrastructure Industry

| Study Period | 2020 - 2029 |

| Base Year For Estimation | 2023 |

| Forecast Data Period | 2024 - 2029 |

| Historical Data Period | 2020 - 2022 |

| CAGR | > 6.50 % |

| Market Concentration | Low |

Major Players

*Disclaimer: Major Players sorted in no particular order |

Need a report that reflects how COVID-19 has impacted this market and its growth?

APAC LNG infrastructure Market Analysis

The Asia Pacific LNG infrastructure market is projected to register a CAGR of over 6.5% during the forecast period (2022-2027).

The market was negatively impacted by COVID-19 in 2020. Presently the market has now reached pre-pandemic levels.

- Increasing demand for LNG in bunkering, road transportation, and off-grid power sectors, along with lower CAPEX requirements for LNG, is expected to drive the growth of the market studied.

- On the other hand, nuclear energy production and renewable technology developments in various regions are major restraints for the market.

- Nevertheless, as per the Energy Information Administration (EIA), non-OECD Asian countries like China, India, Bangladesh, Thailand, and Vietnam are expected to consume 120 billion cubic feet per day (bcf/d) of natural gas by 2050, outpacing regional natural gas production by 50 bcf/d. The supply imbalance in the region is likely to result in increasing dependency on the other regard ions, which is expected to create an excellent opportunity for the market players in the forecast period, as these projects are paving the way for the line pipe industry to grow more.

- China region dominates the market and is also likely to witness the highest CAGR during the forecast period. The LNG import was around 12 million tons in 2020, which increased to 79 million tons in 2021. Due to this surge in demand, China became the world's largest LNG importer, surpassing Japan. The increased demand is due to Chinese LNG buyers signing long-term contracts for more than 20 million tons a year.