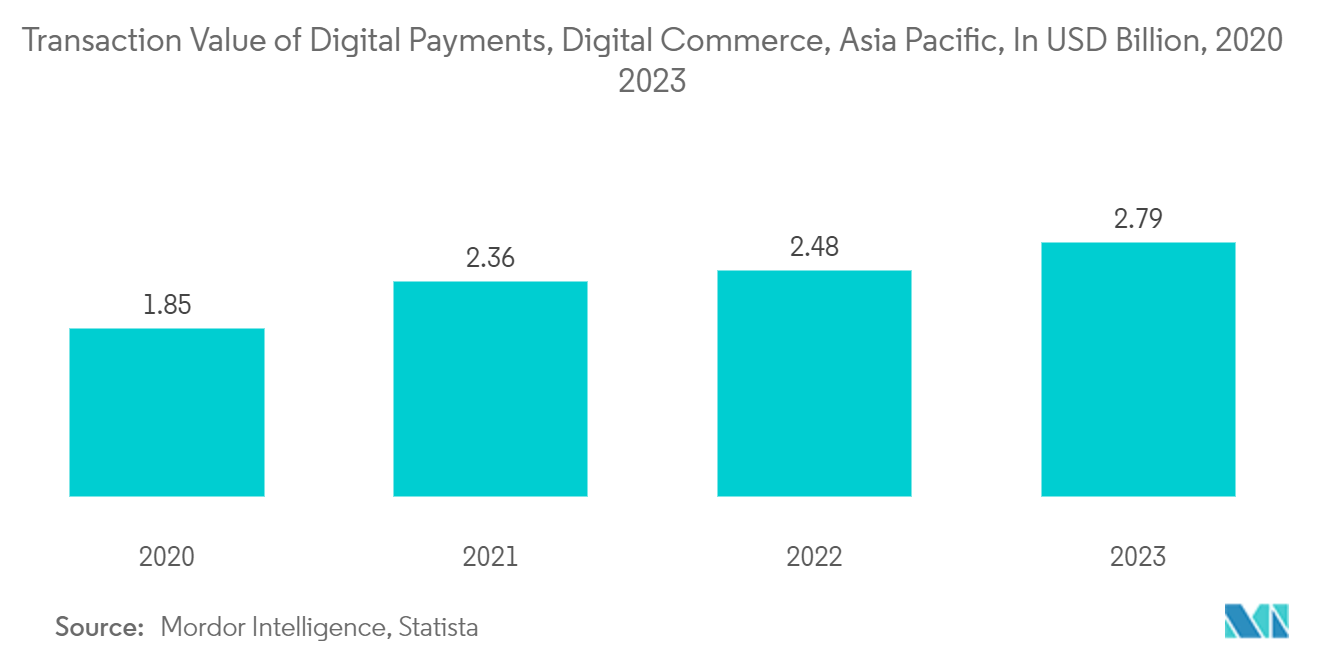

Market Trends of Asia-Pacific Fintech Industry

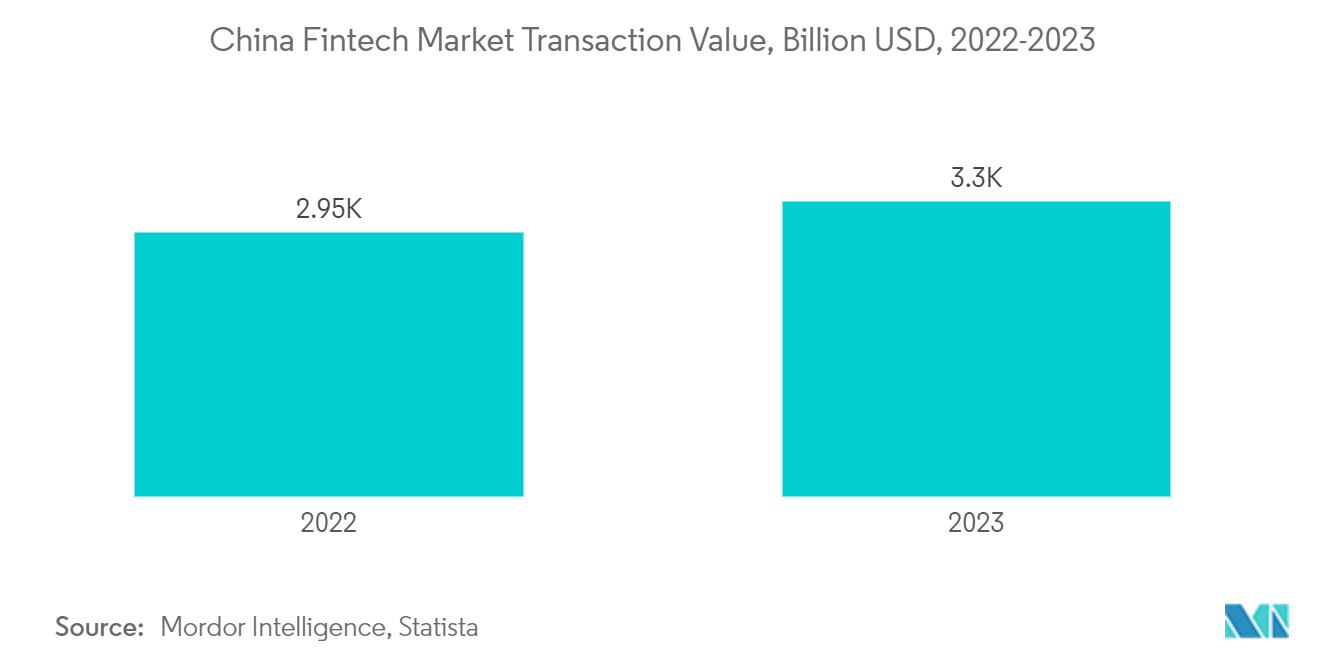

China Dominates the Asia-Pacific Fintech Market

- In Asia, China continues to set the tone for FinTech innovation. FinTech services are now deeply integrated into the lives of Chinese consumers, free of outdated technology and supported by their integration with China's powerful and omnipresent e-commerce and social media platforms, like Alibaba and WeChat.

- Payment firms were eventually regulated. Restrictions were put on the size of wealth management products. The increased availability of digital finance products and tools has positively impacted millions of Chinese individuals and businesses. China leads in consumer and SME-focused financial services innovation, but in other Asian markets, Chinese investments, and the inspiration of their example to local entrepreneurs, are driving rapid market penetration and innovation.

- The People's Bank of China has issued a three-year strategy to help the country's fintech industry grow. There have already been a lot of steps taken in the direction of implementation since then. A fintech sandbox, for example, is being developed and is currently being tested in Beijing. This plan is likely to aid future fintech investment, particularly in key areas such as risk management, cybersecurity, big data, artificial intelligence, distributed databases, and authentication.

Launch Of Cloud Computing Technology Enabling Flexibility In Operations

The introduction of cloud computing technology in Asia Pacific’s fintech market helped with flexibility and scalability in operations. By using cloud computing technology, fintech companies in the Asia Pacific can support virtualized resources and services provided through the Internet. Flexibility is offered by cloud computing in resource allocation. Fintech companies can easily shift their operations according to the changing demand which helps in managing workloads and optimizing costs efficiently. Fintech companies in Asia Pacific are continuously developing and launching innovative solutions, responding quickly to market changes. Therefore, fintech companies are increasingly adopting cloud computing technology to introduce new services and ensure secure and reliable operations