Market Trends of Wood Pulp Trade Analysis

This section covers the major market trends shaping the Wood Pulp Trade Analysis Market according to our research experts:

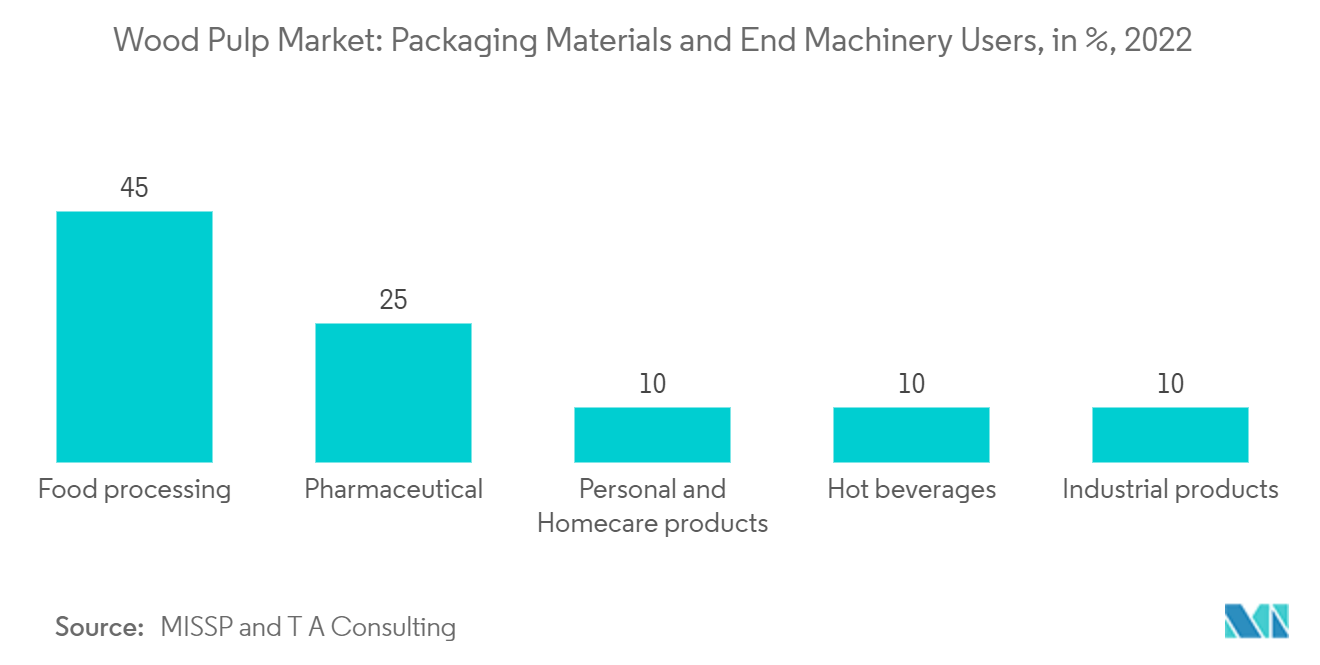

Huge Demand in Packaging and Industrial Papers

- The paper industry is constantly growing worldwide since paper consumption in the consumer market is endless. With new opportunities in industries like hoteling, packing, online markets, and personal hygiene awareness in people, the changing world and improving lifestyles of individuals make a difference in every industry. These changes will positively impact the pulp and paper industry. The market will expand as a result of the forecast period.

- Paper and pulp are produced in greater quantities in China than in any other country, with the United States producing the next highest amount. By the year 2030, the European Union (EU) intends to achieve its goal of collecting and recycling 55% of all plastic packaging. The demand for online shipping impacts paper and pulp production. There was a transition from using paper for printing to using materials for packaging. Productivity has increased as a direct result of the advent of new technologies.

- Recently, there has been a rise in demand for packaging that is resistant to grease. This component can be found in a wide range of different packaged goods and restaurants. Natural alternatives, rather than fluorochemicals, are used to produce grease-resistant packaging.

- Manufacturers are searching for alternatives to petroleum-based products that are both biodegradable and preferred environmentally and eco-friendly products due to consumers being more concerned about the environment due to technological improvements.

- Through its positive promotion of the Make in India policy, the Government of India has implemented a strategy to lower tax rates for new manufacturing companies to turn India into a global manufacturing hub. Furthermore, given the need for domestic firms to compete with MNCs, the government plans to further level the sector among players by launching various initiatives to promote packaging development, along with technological advancements. This will anticipate a growing market during the forecasting period.

Understand The Key Trends Shaping This Market

Download Sample

Asia-Pacific is the Largest Market

- Asia-Pacific is the largest wood pulp industry market globally, and China and India are the major countries boosting the market. India uses paper as a major packaging source, accounting for 5% of global production. Demand for paper continues to rise for FMCG products and ready-to-eat food packaging. Packaging-grade paper accounts for 55% of the main types of paper produced domestically in the paper and paperboard industry. This will encourage the paper market to grow and boost the market in the coming years.

- The development of China's pulp and paper industry is drawing increasing interest among scholars, policymakers, and international producers. The pulp and paper industry is one of the very few industries in China that have been experiencing shortages in supply.

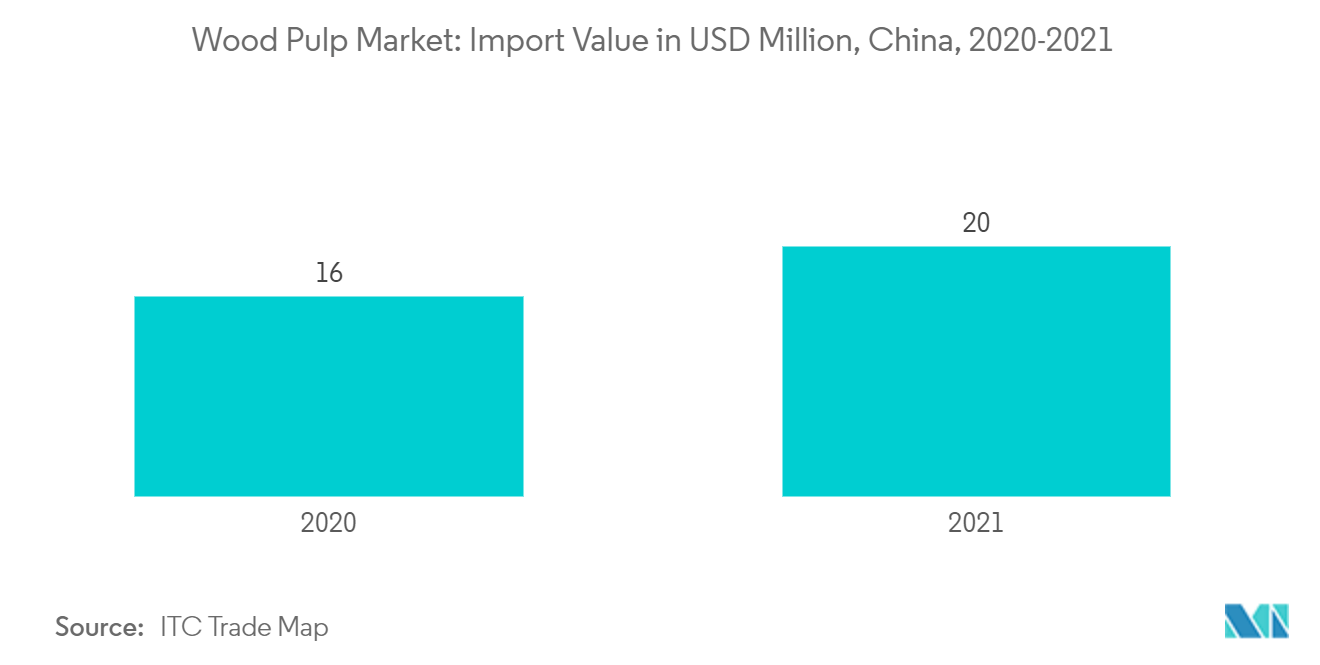

- Due to old production techniques and a lack of high-quality raw materials, domestic production cannot satisfy domestic consumption, especially for high-quality paper and paperboard products. Therefore, unlike other Chinese products, China has been importing more pulp and paper products than exporting. In 2021, China increased its chemical wood pulp imports with a share value of 33.5% of around USD 20.1 million, an increase from the previous year.

- Many pulp and paper companies have unveiled aggressive expansion plans to invest in new wood pulp capacity in China, which shows 30 wood pulp projects with more than 30 million tons of capacity announced between 2019 and 2021. More than 60% of the announced capacity is concentrated in the Guangxi Zhuang Autonomous Region and Hubei Province. In addition to forward integration benefits, which improve the economics of pulp production in China, favorable local government policies are key drivers behind the significant wave of capacity expansion.

Get Analysis on Important Geographic Markets

Download Sample