Market Trends of United States ICT Industry

This section covers the major market trends shaping the US ICT Market according to our research experts:

Rising Demand for Telecommunication

- The US telecom industry was moving forward with expanding its network capacity through new fiber and wireless deployments in 2021 to accommodate the rising demand for faster networks. The US telecom sector substantially expanded network capacity through fiber and wireless deployments. For over 20 years, AT&T, Verizon, and T-Mobile, the big three conventional companies in the United States, have been the backbone of the telecom infrastructure.

- The United States is home to most leading global telecom companies, who drive most of their telecom innovation by investing in R&D. Though the adoption of 5G technology is still in its early phases, AT&T, Verizon, T-Mobile, and U.S. Cellular are already creating a roadmap for the implementation of next-generation 6G via strategic alliances. The demand for services like OTT (over-the-top) media, communications, and e-commerce is growing. The United States has the most significant levels of digitization in the world, spurring more innovations and industry expansion.

- As discussed in the GSMA report, the mobile economy North America 2022, the overall consumer interest in upgrading to 5G is rising. Current 5G customers show increasing interest in expanding their 5G plans to include more content and services (such as live sports, music, gaming, and cloud storage). Interest in entertainment experiences and apps that use the high-bandwidth capabilities of 5G networks is also rising. 5G residential broadband is in high demand, though fixed wireless access (FWA) networks have been available for more than ten years.

- The COVID-19 pandemic profoundly affected the people of the United States in many spheres of life. Large segments of the population were compelled to spend time continuously at home, which increased the need for remote employment, telemedicine, online learning, and streaming entertainment. Network providers have been able to meet the surprisingly strong demand for mobile and home internet connectivity and capacity so far.

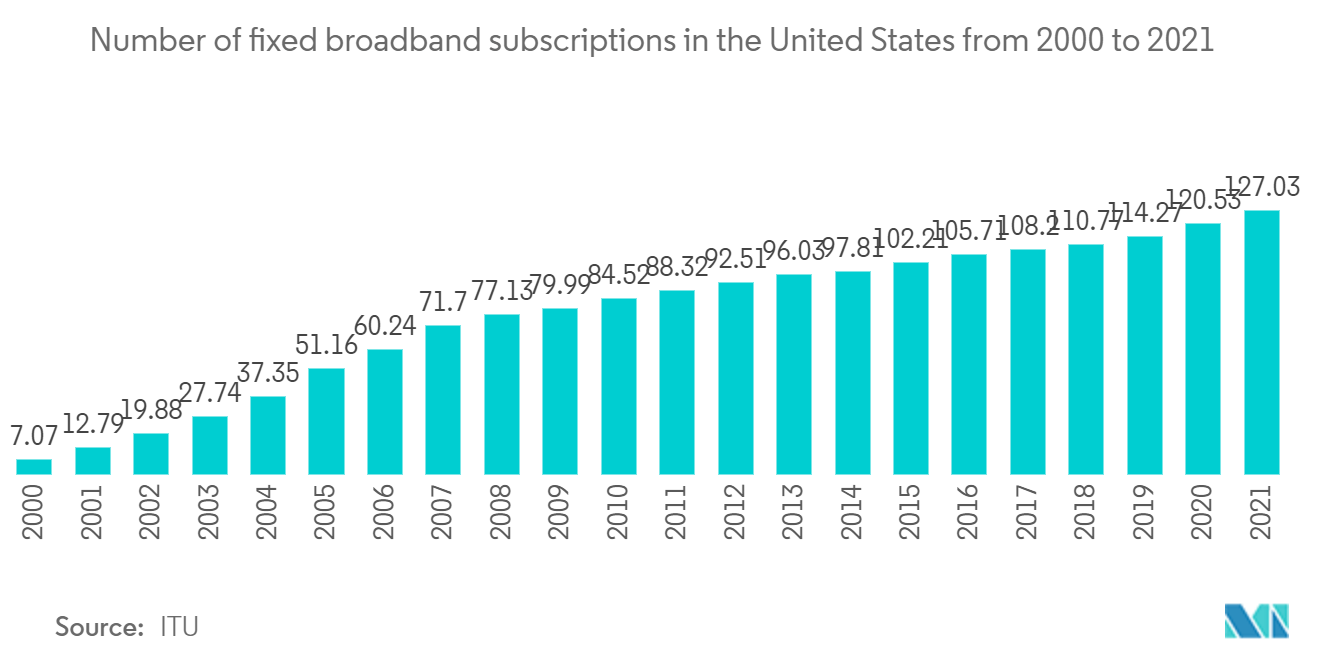

- Furthermore, the ever-increasing demand for internet access is largely dependent on fixed broadband networks. As per the International Telecommunication Union (ITU) report, there were 127 million fixed-broadband subscriptions in the United States in 2021, a modest rise from the year before. The number of fixed broadband subscriptions in the United States has risen steadily during the time under study.

Understand The Key Trends Shaping This Market

Download Sample

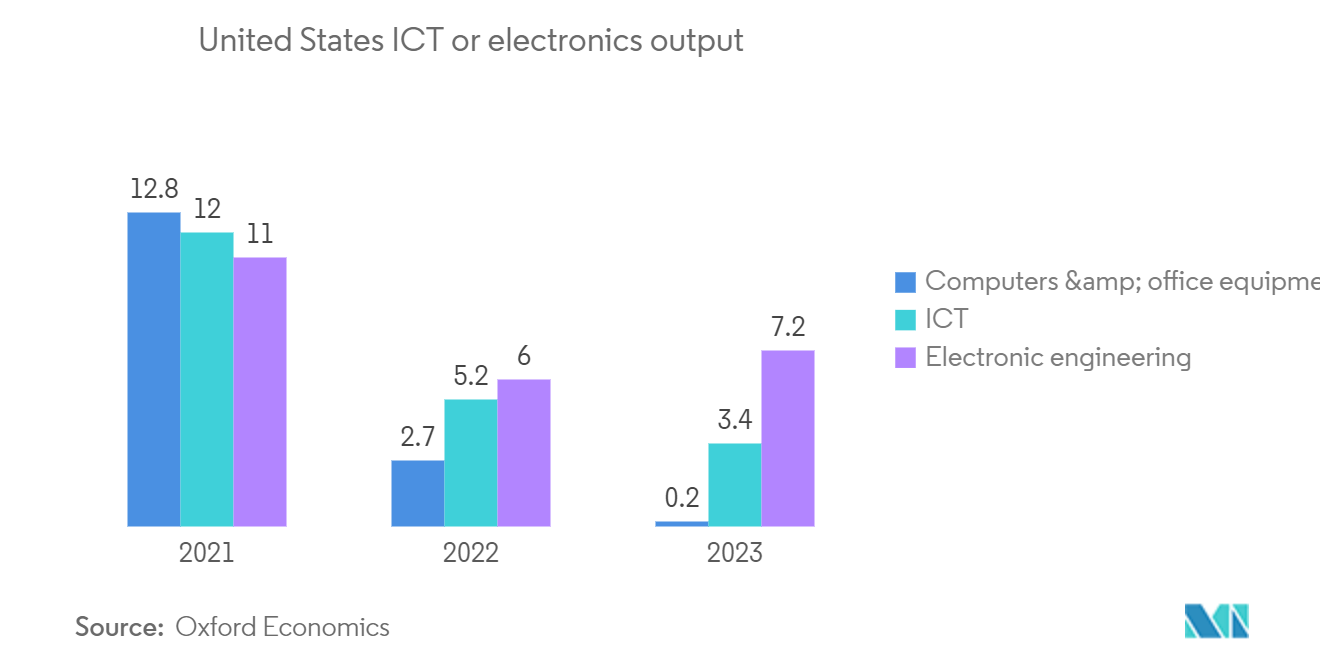

Sales and Production Growth is a bit Slow but Nevertheless Significant

- Despite a little predicted slowdown in growth from the previous year, ICT production and sales in the United States remain solid. Home office equipment, connectivity-related accessories, cloud services, mobility solutions, and network security products continue outperforming the market. However, persistently rising inflation may have a detrimental effect on families' discretionary spending, which would probably lead to fewer purchases of devices. A report by Atradius anticipates that after a robust 11.5% growth in 2021, the output of consumer electronics in the country will only expand by 1.5% in 2022.

- Chips are increasingly required for data production, transport, processing, and storage due to the exponential expansion of data. China and the United States lead digital technology advancements. However, China does not play a significant role in the semiconductor business. According to the UNCTAD report, in 2020, the United States accounted for 47% of all sales. The production of computers, telecommunications equipment, and consumer electronics decreased because of the prolonged semiconductor scarcity. However, electronic components (including chips) are anticipated to rise by 8.5% in 2022.

- Meanwhile, the demand for chips is likely to outpace supply through 2023. The war in Ukraine has an unfavorable effect on chip producers, especially since two of Ukraine's biggest makers of neon gas stopped generation. However, prime US chip producers tend to keep a large amount of reserve to combat the situation.

- As per the Atradius report, semiconductor sales prices rose by 15% on average in 2021. ICT businesses confront higher vitality and transport costs (especially, charges for shipping holders have expanded considerably). Some firms may have to bear the high expenses of airfreight to satisfy customer demand on time due to supply-time delays. The profit margins of US ICT companies grew considerably due to the high demand in 2021. In the upcoming twelve months, profit is expected to remain at the same level as demand for all main product categories slow slightly, and market competition remains fierce.

- Underfunding the domestic ICT workforce and STEM education endangers the industry's capacity to meet the rising demand for essential ICT goods, influencing the execution of federal and state-funded projects and policies to boost domestic manufacturing. Government investment in 2022 would devote a sizeable portion to improving technology systems, communication services, and cyber security. The key areas of federal ICT investments include funding the US workforce, aiming to advance science and technology, and, most importantly, creating a better broadband workforce.