Market Trends of US Caps and Closure Industry

This section covers the major market trends shaping the US Caps & Closure Market according to our research experts:

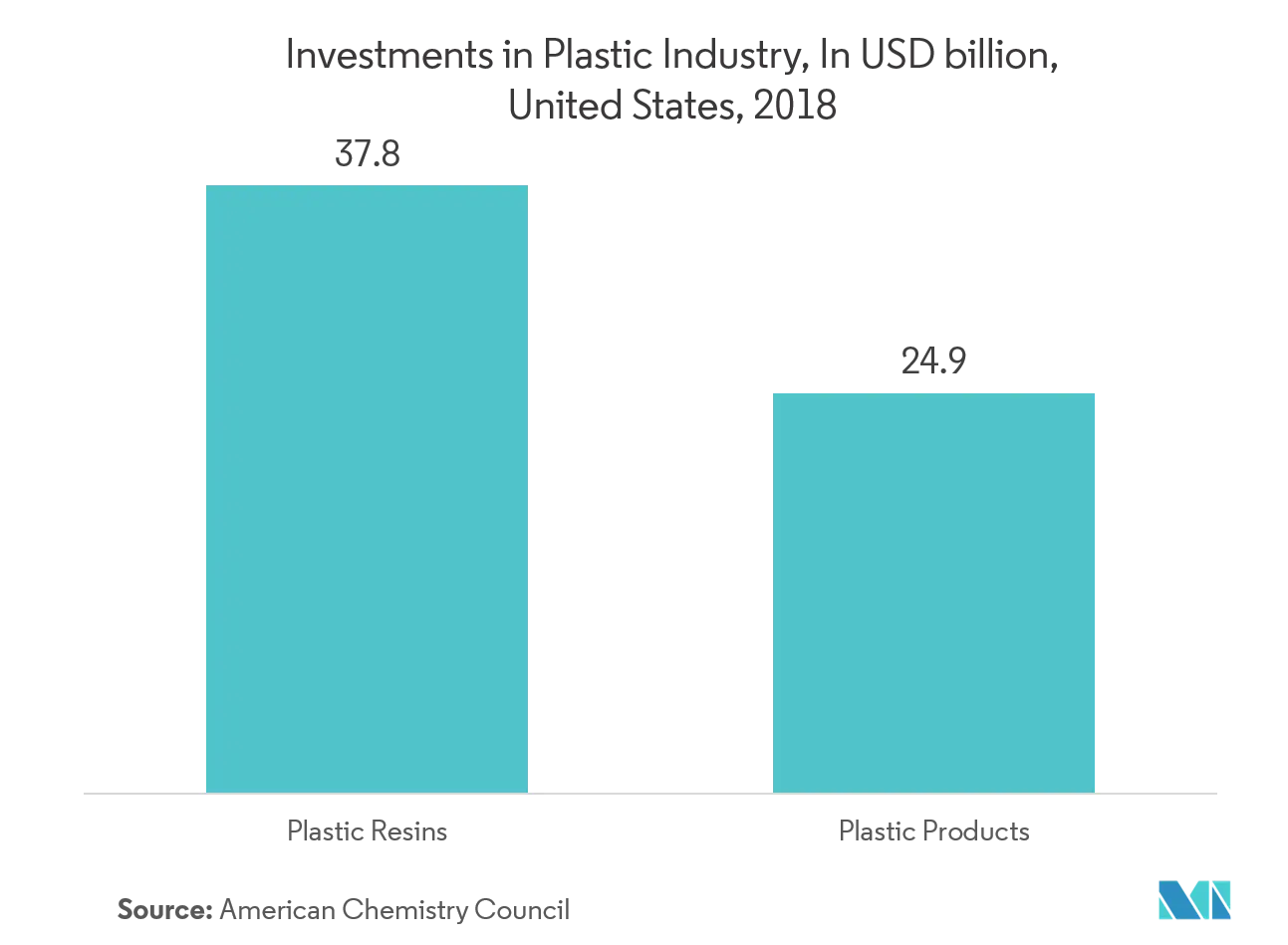

Plastic to Witness a Highest Growth

- According to American Chemistry Council, in 2018, out of USD 37.8 billion investment in plastic resins, USD 24.9 billion investment is used for plastic products, which shows the demand for plastic packaging in the overall products. The food and beverage industry is one of the major contributors to the caps and closures market in the United States. Majority of the manufactured food products are packaged in PET containers, which are mostly covered with plastic enclosures, to protect them from contamination. As PET had been approved as safe for contact with food and beverage (F&B) by the FDA and health-safety agencies, due to which PET caps and closures are increasingly being used for dairy products, convenience food, and other food service applications.

- Polypropylene (PP) has inherent properties, like excellent tensile strength, inertness toward acids, alkalis, and solvents, and has a cost advantage over other thermoplastic polymers. These properties positioned PP across a wide range of consumer products, which are manufactured by high-volume forming methods.

- Some of the prominent players in the industry through research and developments have been instrumental in further innovating their offerings and coming up with product developments with a next generation random polypropylene (PP). For instance, in October 2019, Borealis announced the commercial launch of BorPure RF777MO based on the proprietary Borstar Nucleation Technology (BNT). The BorPure RF777MO is designed for use in flip-top caps where the new resin enables the manufacturer to reduce cycle times for certain caps applications.

- Moroever to provide impact strength, combined with stiffness and a low potential for stress whitening, High-density polyethylene (HDPE) and LDPE are best suited in it. According to Borealis, the growth in the HDPE caps and closures is mainly due to the replacement of metal caps used on glass bottles (replaced by PET), and a change in the consumption pattern as more refreshments are consumed from small bottles.

- As HDPE caps are more compatible with the geometries of the PET thread, these are being increasingly used in the PET bottling. The increasing consumption of the bottled water is expected to fuel the adoption of the HDPE caps over the forecast period.

Understand The Key Trends Shaping This Market

Download Sample

Beverage Accounted to Hold a Major Market Growth

- As the US beverage market is growing, following with higher consumption of wine and beer, the packaging components and materials are also adding value differentiation with evolving demands. According to the report by the Wine Institute of America, released in April 2019, almost 1 billion gallons of wine were produced in the United States in 2017. The United States is the highest consumer of wine, with a 15% global share. Owing to such high consumption of beverages, the demand for caps and closures is expected to increase in the United States.

- United States is one of the largest wine consuming country. According to Wines and Vines Analytics, 2019, the total dollar value of the US wine market in 2018 was USD 70.5. A key trend for the market growth that can be seen in this market is the growing preference for plastic/synthetic corks and screw caps over natural corks.

- As artificial corks, technical and synthetic corks are replacing natural corks, as it shows cork taint or TCA (2,4,6-trichloroanisole) chemical that leeches out of a natural cork into the wine, but the synthetic corks can also pick up TCA contamination from the external environment.

- To address this issue, according to SevenFifty Daily,the world's largest cork producer,Amorim, is focusing to eliminate TCA from corks by 2020, using cutting-edge technology, and it focuses to manufacture cork with zero TCA.

- Moreover, the most conventional packaging material for single-serve, non-carbonated bottled water in the United States is polyethylene terephthalate (PET) plastic. According to the International Bottled Water Association (IBWA), in 2018, the total sales of bottled water were USD 18.5 billion, an increase of 8.8% from previous years. The average American consumes 167 plastic bottles of water per year. Owing to such demand for packaged drinking water in the region, there is an increasing demand for especially PET plastic caps and enclosures.

- Furthermore, the innovation pertaining to temper resistant caps and closures is also gaining significant traction due to anti-counterfeiting properties.

- For instance, in May 2019, Guala Closures won Alufoil Trophy 2019 for its e-WAK technology; the e-WAK from Guala Closures is the first NFC aluminum closure which is based on a new smart technology that allows every bottle of wine to become a connected bottle. A chip is positioned inside the closure that can be read by enabled smartphones, providing consumers authenticity certification and extensive product information.

.webp)