Market Trends of Spent Fuel and Nuclear Waste Management Industry

This section covers the major market trends shaping the Spent Fuel & Nuclear Waste Management Market according to our research experts:

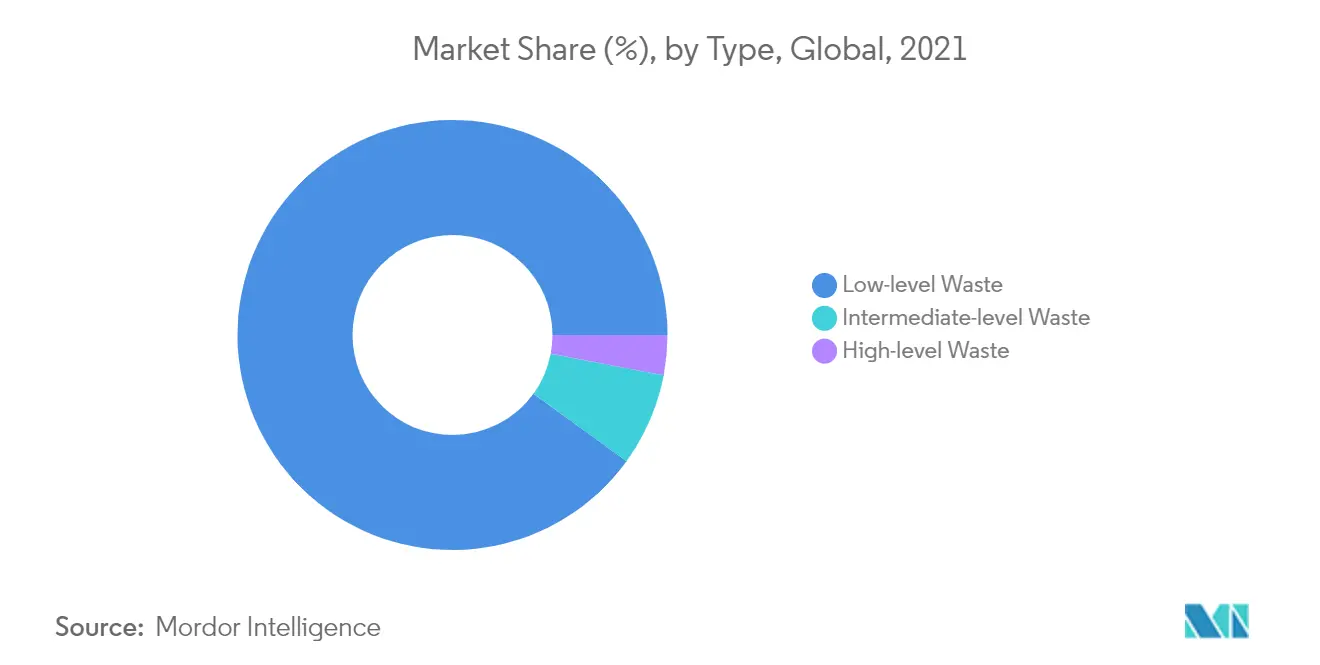

Low-level Waste Expected to Dominate the Market

- Radioactive nuclear waste includes any material that is intrinsically radioactive or contaminated by radioactivity and deemed to have no further use. Low-level waste (LLW) generated from the nuclear fuel cycle has a radioactive content not exceeding 4 giga-becquerels per ton (GBq/t) of the alpha activity or 12 GBq/t beta-gamma activity. To reduce its volume, LLW is often compacted or incinerated before disposal.

- It does not require shielding during handling and transport, and it is suitable for disposal in near-surface facilities.

- The market studied is dominated by LLW, which comprises 90% of the volume but only 1% of the radioactivity of all radioactive waste. Management practices for the disposal of LLW (adopted or under consideration) encompass three main options, such as near-surface disposal, disposal in caverns at intermediate depth, and disposal in deep geological formations.

- As more than 90% of nuclear waste comes under the LLW category, more infrastructure is needed to store the radioactive waste properly and safely. Moreover, as nuclear power is getting popular due to clean and sustainable sources of energy, various countries are investing in nuclear power plants and related facilities, which is expected to drive the spent fuel and nuclear waste management market.

- Therefore, the long durability and a promising alternative for power generation in the form of nuclear-based power generation have been tremendously inflicting the demand for nuclear power plants globally.

- Furthermore, various power plants are under construction across the Asia-Pacific region, owing to the advantage and reliability offered by nuclear-based power generation. This, in turn, is driving the demand for the spent fuel and nuclear waste market.

- Therefore, owing to the above points, the low-level waste segment is expected to dominate the market during the forecast period.

Understand The Key Trends Shaping This Market

Download Sample

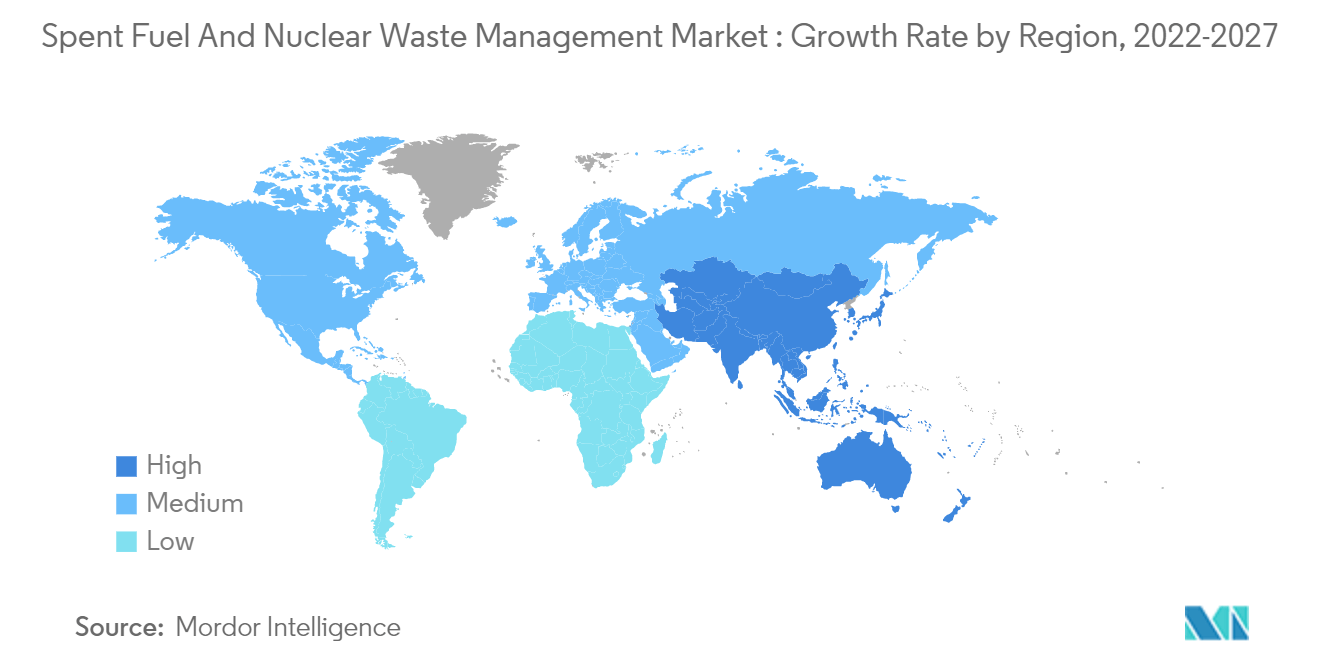

Asia-Pacific Expected to Witness Significant Growth

- Asia-Pacific is expected to be the fastest-growing market during the forecast period. In contrast to North America and Europe, where growth in electricity generating capacity, particularly nuclear power, has been limited for many years. Several countries in Asia are planning and building new nuclear power reactors to meet their increasing demand for clean electricity. China, Japan, South Korea, and India are the major countries that are expected to drive the spent fuel and nuclear waste management market in Asia-Pacific during the forecast period.

- China uses the most advanced technology and the most stringent standards for the development of nuclear power, and it strictly manages the entire life cycle of nuclear facilities from siting, design, construction, and operation, to waste management. As of February 2022, China has 54 nuclear power reactors in operation, 14 under construction, and more about to start construction. The combined capacity of operating nuclear power reactors in 2021 was 50.71 Gwe, which generated around 375 TWh of electricity in the same year, representing 4.9% of the total electricity generation in the country.

- The country plans to expand its nuclear reactors fleet in the coming years. As of June 2020, China had around 12 reactors with a combined capacity of 12.24 GWe and more than 50 GWe under construction and planned phases. In April 2020, the director of the Nuclear Safety Inspection Department at the Ministry of Ecology and Environment stated that all the 15 unfinished reactor units had resumed construction, and reactors that were already in operation were not affected due to the COVID-19 outbreak.

- The Chinese nuclear sector is expected to continue to expand at robust rates, with capacity increasing by an annual average of 10.3% between 2018 and 2027, resulting in more than 95GW of installed nuclear capacity by the end of the next decade. This is in line with the ambitious aims of China to decarbonize its baseload generation and amass nuclear expertise to export. Hence, the volumes of waste are expected to be significantly greater than the existing waste from nuclear power plants, which may drive the market during the forecast period.

- Furthermore, according to the World Nuclear Association, the demand for uranium in the country is expected to be over 11,000 TU (with 58 reactors operating) in 2020, about 18,500 TU (for 100 reactors) in 2025, and about 24,000 TU (for 130 reactors) in 2030. As China rapidly increases the number of new reactors, a long-term policy is expected to be in place for fuel reprocessing and spent fuel storage, providing an impetus to the market studied.

- India had 6.885 GW of installed nuclear capacity at the end of 2021 and around 4.2 GW of net capacity under construction. India has shown significant interest in expanding its domestic nuclear sector as a means to meet the rapidly growing demand for electricity, lower emissions through the adoption of low-carbon power sources, and capitalize on its indigenous reserves of uranium and thorium.

- Therefore, owing to the above points, Asia-Pacific is expected to witness significant growth in the spent fuel and nuclear waste management market during the forecast period.

Get Analysis on Important Geographic Markets

Download Sample