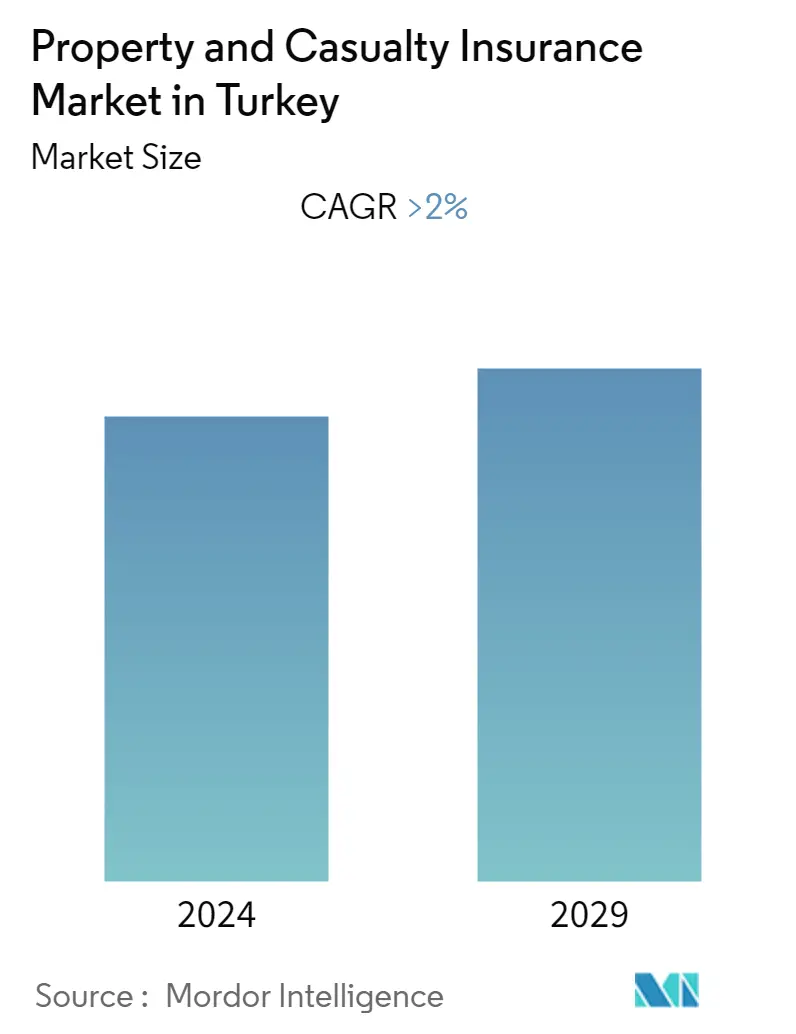

Market Size of Property and Casualty Insurance Industry in Turkey

| Study Period | 2020 - 2029 |

| Base Year For Estimation | 2023 |

| Forecast Data Period | 2024 - 2029 |

| Historical Data Period | 2020 - 2022 |

| CAGR | > 2.00 % |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order |

Need a report that reflects how COVID-19 has impacted this market and its growth?

Property and Casualty Insurance in Turkey Market Analysis

The property and casualty insurance market in Turkey is estimated at approximately USD 8.8 billion in the current year and is poised to grow at a CAGR of greater than 2% during the forecast period.

All functions of the insurance value chain have been impacted by the COVID-19 pandemic. The only differences can perhaps be found in the scale and in timelines - immediate (during the pandemic), near term (as the pandemic subsides, but economic slowdown continues) and long term (as the economy rebounds). The primary needs include process changes in the claims function and replacing site visits with electronic inputs from customers. In the scenario that the pandemic continues unabated beyond spring, the Sales & Marketing, Underwriting and Actuarial functions will also need to address the impact of remote working, social distancing, and intra-city movement restrictions. The sales teams require enablers for remote meeting with customers, digital forms for new business, while Underwriting teams need to perform remote assessments and Actuarial teams need to factor in pandemic and its related risks in product pricing. While the immediate direct impact of COVID-19 on Insurance claims is obvious, insurers will need to focus on actively managing their investment portfolios.

While pandemic cover is typically explicitly excluded in certain policies, and treated under 'force majeure' in certain others, instances of governments and regulatory authorities issuing advisory to insurers to consider the COVID-19 related claims compassionately have started to trickle in. This will add complexity into the claims process and will also be an unplanned drain on reserves.

Motor insurance was the largest line of business in 2020 followed by property insurance, non-life personal accident and health (PA&H) insurance, marine, aviation and transit (MAT) insurance, liability insurance, financial lines, and other segments, respectively. Marine, aviation and transit (MAT) insurance and liability insurance lines of business are expected to exhibit significant growth during the projected period.

Around 39.1% of customers in the country preferred purchasing home building and contents insurance from banks. It was the most demanded channel for all groups of customers except 18-24 years age group. It had a 62.5% preference rate among customers aged between 55-64, which was indicative of a strong preference for co-ordination with the banks. The second most-preferred channel were insurers, followed by insurance brokers.

There is potential for further growth in non-life insurance, as non-life insurance penetration currently stands at only 1.3% of GDP much lower than the average for OECD countries. Most insurers operating in the segment are foreign-owned or partnered, showing it is a popular area of investment for foreign companies.