Perimeter Security Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

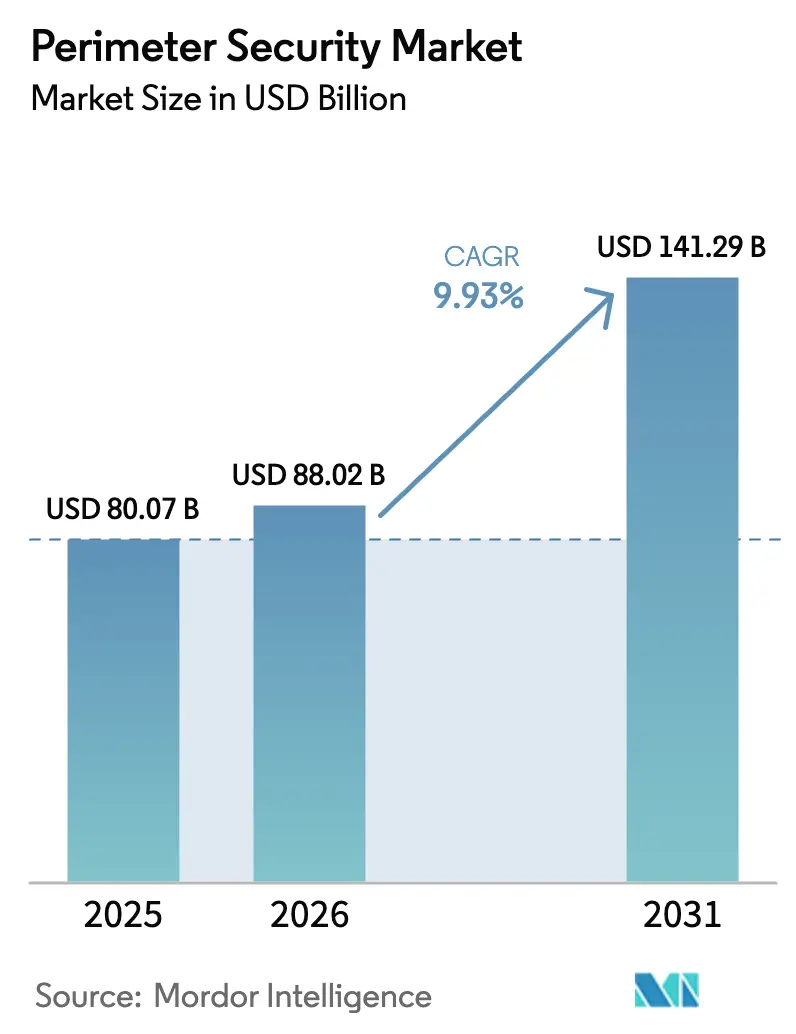

| Market Size (2026) | USD 88.02 Billion |

| Market Size (2031) | USD 141.29 Billion |

| Growth Rate (2026 - 2031) | 9.93% CAGR |

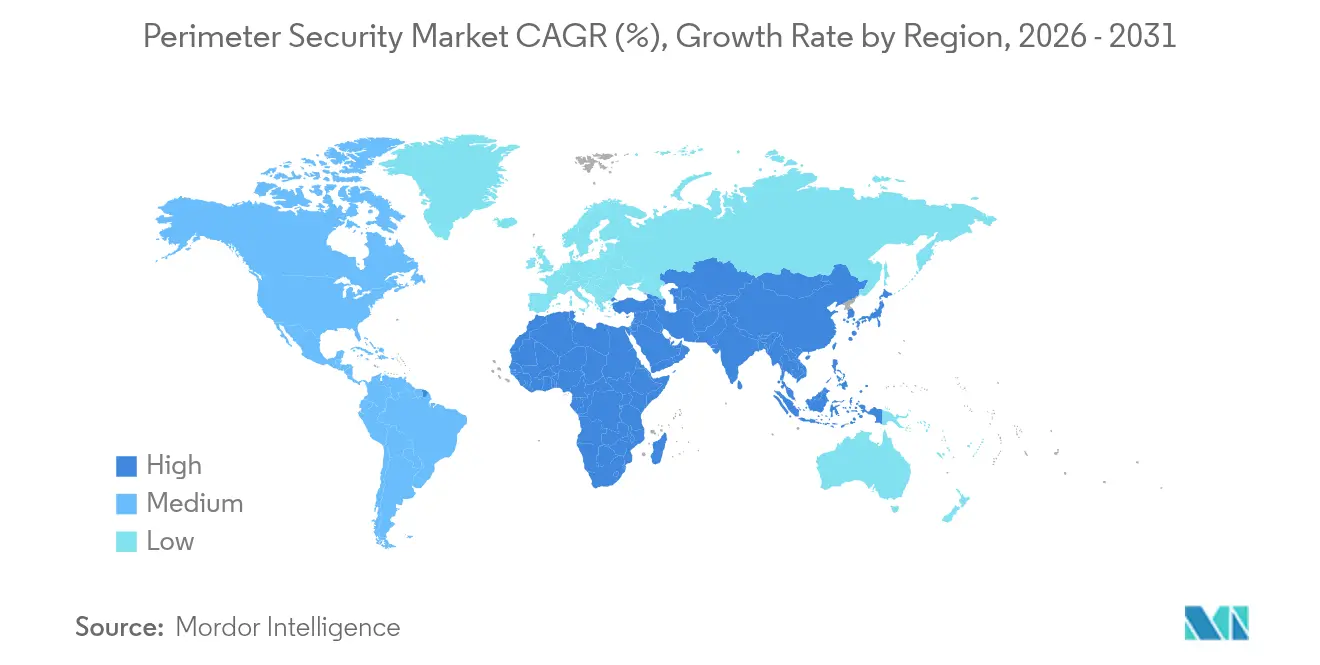

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Perimeter Security Market Analysis by Mordor Intelligence

The perimeter security market size is expected to grow from USD 80.07 billion in 2025 to USD 88.02 billion in 2026 and is forecast to reach USD 141.29 billion by 2031 at 9.93% CAGR over 2026-2031. Rising geopolitical risk, AI-driven analytics, and stricter critical-infrastructure mandates are the primary engines of this growth trajectory. The market’s scale-up is reinforced by the limitations of legacy fence-line systems, the proliferation of low-cost drones, and a regulatory pivot toward demonstrable resilience metrics. Providers that deliver predictive threat intelligence, integrate cyber and physical controls, and supply outcome-based service models are gaining pricing power in the perimeter security market. Capital spending is also flowing toward software-centric architectures that compress detection latency and create higher switching costs for customers. Demand visibility remains strong because refresh cycles are tied to statutory compliance timelines as well as the need to secure large-scale data-center and energy assets that cannot tolerate unplanned downtime.

Key Report Takeaways

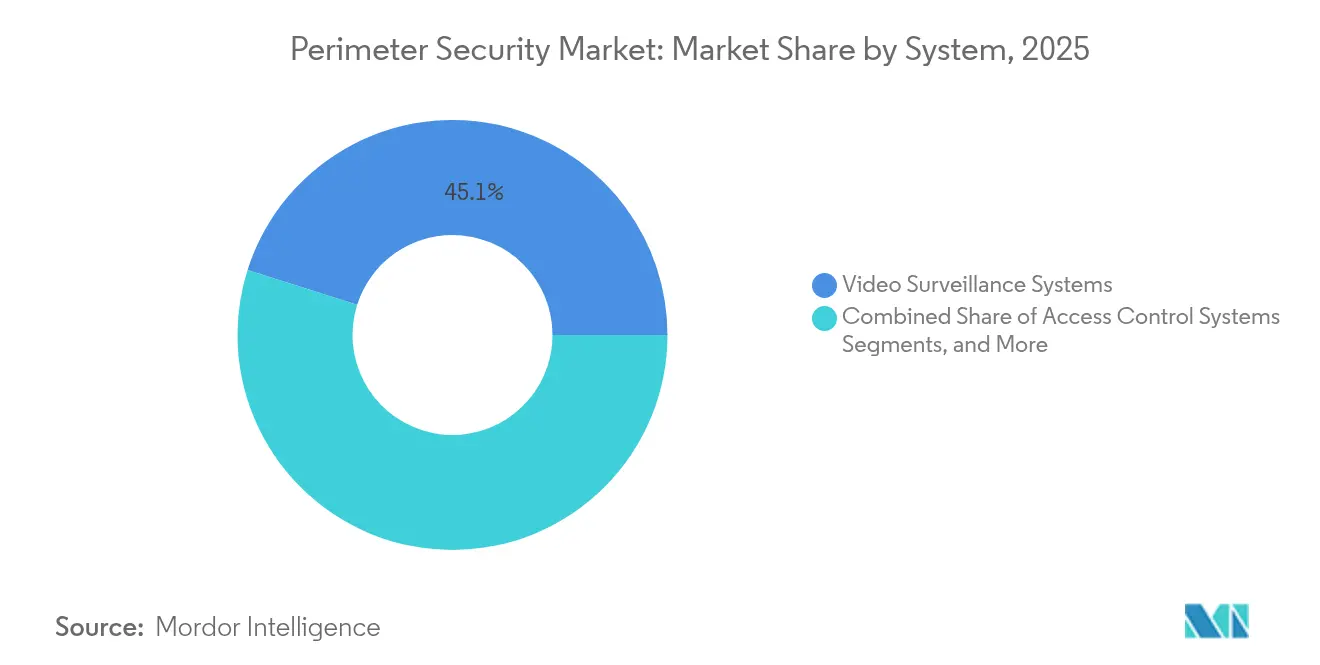

- By system, video surveillance led with 45.12% revenue share in 2025; perimeter intrusion detection is forecast to grow at a 10.12% CAGR through 2031.

- By service, system integration and consulting held 50.32% of the perimeter security market share in 2025, while managed security services record the highest projected CAGR at 10.28% through 2031.

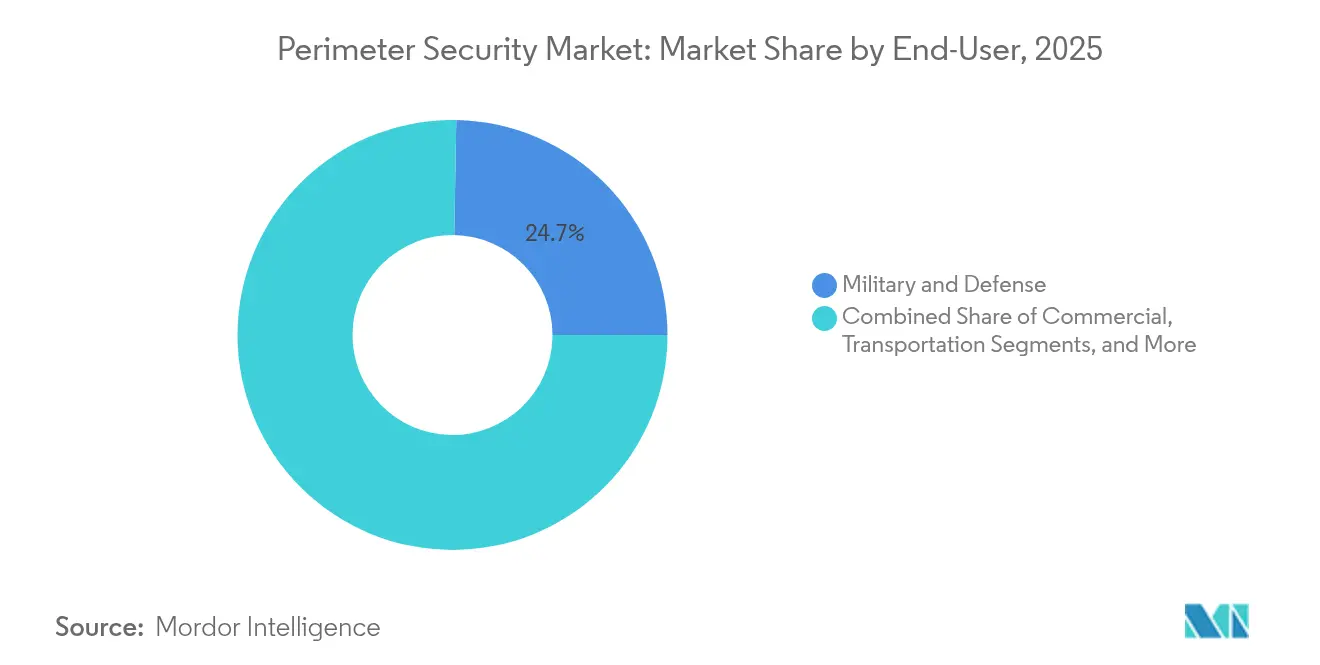

- By end-user, military and defense accounted for 24.72% share of the perimeter security market size in 2025; the commercial sector is advancing at a 10.65% CAGR to 2031.

- By deployment type, ground-based solutions captured 53.62% of the perimeter security market size in 2025 and are expanding at a 10.12% CAGR through 2031.

- By region, North America led with 28.08% market share in 2025, whereas Asia Pacific is expected to register the fastest 11.6% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Perimeter Security Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| AI-enabled Video Analytics Adoption in North American and European Critical Infrastructure | +2.8% | North America & Europe | Medium term (2-4 years) |

| EU CER Directive 2022/2557 Mandates for Utilities and Water Operators | +1.9% | Europe, spillover to APAC | Short term (≤ 2 years) |

| Data-Center Build-out in South-East Asia Boosting Fiber-Optic Fence Detection Demand | +2.1% | APAC core, spillover to MEA | Medium term (2-4 years) |

| Drone-Assisted Smuggling at Latin-American Prisons Driving Radar-based Surveillance | +1.4% | Latin America, global adoption | Long term (≥ 4 years) |

| Remote Pipeline Expansion in MEA Requiring Seismic PIDS Integrated with SCADA | +1.2% | MEA, North America shale regions | Long term (≥ 4 years) |

| AI-Driven Sensor Fusion for Autonomous Security Patrol Robots | +1.1% | APAC & North America | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

AI-enabled Video Analytics Adoption in North American and European Critical Infrastructure

Operators are migrating from passive camera networks to AI-infused analytics engines that flag loitering, crawlers, and coordinated breaches with 95% accuracy while cutting nuisance alarms by 60%. Edge-based inferencing brings real-time decision-making directly to the fence line, eliminating cloud-round-trip latency. Thermal sensors fused with computer vision extend coverage to zero-light environments typical of energy hubs and ports, enhancing operational continuity. Vendors embedding open APIs can monetise data exhaust through threat-intelligence subscriptions, deepening account lock-in. The result is a secular shift toward software maintenance revenue inside the perimeter security market.

EU CER Directive 2022/2557 Mandates for Utilities and Water Operators

The Directive obligates 27 EU states to complete multi-layered perimeter programs by 2025, forcing utilities to invest in fiber-optic sensing, biometric access, and integrated OT-IT dashboards.[1]European Commission, “The Critical Entities Resilience Directive,” critical-entities-resilience-directive.com Quadrennial risk assessments institutionalise recurring spend and shorten sales cycles. Standardised protocols reduce vendor complexity, but also raise the compliance bar, favouring full-stack incumbents able to certify entire solution suites. Early movers in the perimeter security market can leverage proven reference sites to win pan-regional frameworks.

Data-Center Build-out in Southeast Asia Boosting Fiber-Optic Fence Detection Demand

Malaysia and Indonesia together attract more than USD 10 billion per year in hyperscale capacity, pushing demand for kilometre-scale fiber-optic intrusion lines that double as condition-monitoring sensors. AI-enriched acoustic analytics mitigate tropical weather noise, increasing detection fidelity and lowering manual patrol headcount. Cloud providers prefer unified systems that route alarms into their SOCs, creating multi-year managed-service contracts. Supply ecosystems in the perimeter security market are responding with pre-terminated cable kits that accelerate brownfield retrofits.

Drone-Assisted Smuggling at Latin-American Prisons Driving Radar-based Surveillance

Correctional authorities report a surge in quad-rotor contraband flights, exposing the vertical blind side of legacy fences. 3D radar coupled with RF jamming neutralises low-slow-small drones without collateral disruption to civil aviation. The threat vector is propagating to border crossings and logistics yards, expanding total addressable demand for counter-UAS modules within the perimeter security market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High False-Alarm Rates on Wildlife-Heavy Australian Mining Sites | -1.7% | Australia, Africa mining regions | Short term (≤ 2 years) |

| Fragmented Certification Regimes (UL-1076 / EN-50131 / SAC-Norms) Slowing Roll-outs | -2.3% | Global, acute in cross-border projects | Medium term (2-4 years) |

| Skilled-Installer Shortage for Fiber-Optic and Radar Systems in Emerging Markets | -1.8% | APAC emerging markets, Latin America | Medium term (2-4 years) |

| GDPR Article 35 Litigation Over High-Res Surveillance in EU | -1.5% | Europe, spillover to privacy-conscious regions | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High False-Alarm Rates on Wildlife-Heavy Australian Mining Sites

Kangaroos, wombats, and large birds trigger more than half of perimeter alerts at remote mines, eroding operator trust and inflating response budgets by USD 1.8 billion annually. AI classifiers that distinguish fauna from humans exist but carry higher upfront cost, deterring smaller concessions. Persistent false activations also jeopardise insurance cover, adding a hidden premium to total cost of ownership in the perimeter security market.

Fragmented Certification Regimes (UL-1076 / EN-50131 / SAC Norms) Slowing Roll-outs

Divergent testing protocols compel manufacturers to engineer region-specific variants, stretching development cycles and inflating compliance overhead by up to 25%.[2]Acre Security, “Certification for Intrusion Detection Systems,” acresecurity.com For AI and cloud modules, certification bodies have yet to codify repeatable benchmarks, creating go-to-market latency. Multinationals therefore face 6- 12-month procurement delays that dilute the addressable near-term revenue of the perimeter security market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By System: AI Integration Fuels Surveillance Supremacy

Video surveillance accounts for 45.12% of 2025 revenue and sets the reference architecture for predictive perimeter intelligence. Deep-learning classifiers combined with thermal imagers deliver 95% human-vehicle identification accuracy and shrink nuisance alarms by 60%. The perimeter security market size for video surveillance is projected to reach USD 63.7 billion by 2031, sustaining relevance through software-led upgrades that lift lifetime value. In parallel, perimeter intrusion detection is forecast to clock the quickest 10.12% CAGR as fiber-optic and seismic sensors extend coverage across remote pipelines and utility corridors.

Complementary technologies are being woven into modular suites. Access-control platforms integrate biometric readers and mobile credentials to streamline throughput without eroding security. Barriers, bollards, and drone detection subsystems embed adaptive materials and AI to counter vehicular ramming and swarm threats. Market leaders therefore package cameras, sensors, and counter-UAS assets as an interoperable stack, reinforcing ecosystem lock-in across the perimeter security market.

By Services: Managed Operations Capture Share of Wallet

System integration and consulting held 50.32% share in 2025 as enterprises sought turnkey orchestration of multi-vendor estates. However, managed security operations are scaling at a 10.28% CAGR, shifting cash flows from capex to opex. Under outcome-based contracts, providers guarantee mean-time-to-detect and false-alarm thresholds, aligning economics with risk transfer. The perimeter security market size for managed services is forecast to exceed USD 22.6 billion by 2031.

Predictive maintenance models built on IoT telemetry now pre-empt sensor failures, protecting service level agreements and sustaining annuity streams. Cloud-native platforms such as CCURE Cloud converge video, access, and threat intelligence into a unified dashboard that slashes administrative labour. Cross-domain offerings that bundle cyber and physical remediation are becoming table stakes in the perimeter security industry.

By End-User : Commercial Enterprises Accelerate Outlays

The perimeter security market share of military and defense stood at 24.72% in 2025, but commercial enterprises are raising spend at a 10.65% CAGR as boardrooms treat resilience as an operating KPI. Data-center operators, airports, and industrial conglomerates all face revenue loss from even minute-long outages, compelling investment in layered perimeter safeguards.

Transportation hubs deploy radar, thermal, and AI behavioural analytics in concert to secure passenger throughput. Industrial operators integrate acoustic fiber sensors that double for structural health monitoring, monetising their security capex. Government sites adopt interoperable standards to future-proof procurement, while gated communities demand privacy-conscious aesthetics, demonstrating the breadth of application driving the perimeter security market.

By Deployment Type: Ground-Based Configurations Dominate

Ground-based arrays represented 53.62% of 2025 revenue and are growing at 10.12% CAGR as users seek early-warning zones beyond hard fences. Distributed acoustic sensing stretches detection envelopes kilometres away from assets, giving operators valuable reaction time. Radar and LIDAR overlays further improve situational awareness at critical junctions.

Barrier-mounted approaches retain relevance in prisons and high-security campuses, where physical delay is indispensable. Hybrid solutions are emerging that tie smart bollards to ground-wave radars, offering cohesive deterrence and detection at lower total cost of ownership. This fluid design palette underlines the systems-integration premium embedded in the perimeter security market.

Geography Analysis

North America captured 28.08% revenue in 2025, underpinned by federal stimulus for grid hardening and stringent sector-specific mandates. Edge analytics adoption is comparatively mature, creating software-upgrade tailwinds. Asia Pacific is projected to deliver an 11.6% CAGR, the fastest worldwide, powered by hyperscale cloud construction, smart-city roll-outs, and expanding manufacturing footprints. The perimeter security market size for Asia Pacific is expected to surpass USD 49.2 billion by 2031.

The GCC surveillance market alone is targeting 6.2% CAGR, leveraging higher oil receipts and FDI inflows that fund public-space monitoring. Europe’s CER Directive synchronises procurement across 27 economies, reducing vendor dilution and encouraging pan-regional tenders. Latin America faces novel aerial threats, accelerating radar-based surveillance deployments in correctional and border infrastructures.

Meanwhile, pipeline expansion across the Middle East and Africa necessitates seismic sensors integrated with SCADA, blurring traditional segment boundaries and elevating cyber-physical convergence requirements. Cloud-hosted command platforms are gaining favour as operators centralise dispersed sites, enhancing recurring revenue visibility in the perimeter security market.

Competitive Landscape

The perimeter security market is moderately fragmented but turning more consolidated as incumbents buy to fill capability gaps. Honeywell’s USD 4.95 billion acquisition of Carrier’s Global Access Solutions deepens vertical integration and strengthens recurring software revenue streams. [4]SecurityInformed, “2024 Was a Big Year for M&A in the Security Market,” securityinformed.com GardaWorld’s acquisition of Stealth Monitoring enhances its capabilities with AI-powered video analytics and 100,000 cameras under management, positioning the firm for outcome-based service contracts.

Disruptors such as Sauron Industries,Inc., push AI-native, zero-false-positive residential platforms, challenging legacy DVR vendors. Axis Communications counters by opening its camera-to-cloud stack, courting third-party developers, and reinforcing ecosystem stickiness.

Strategically, incumbents focus on scale and lifecycle economics, while challengers differentiate through software velocity and cloud elasticity. Partnerships, such as ASSA ABLOY’s tie-up with Boston Dynamics for autonomous patrols, signal a convergence between robotics and access control that could re-segment the perimeter security industry.

Perimeter Security Industry Leaders

Honeywell International Inc.

Dahua Technology Co., Ltd.

Bosch Security Systems

Hikvision Digital Technology Co., Ltd.

Axis Communications AB

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Johnson Controls announced the IQ Panel 5 security panel featuring Qualcomm DragonWing processor and Android 14 operating system Johnson Controls.

- February 2025: Vitaprotech Group finalized its acquisition of Identiv's security and identity reader business Vigilance Security Magazine.

- January 2025: Gallagher Security showcased its Controller 7000 Enhanced at the 26th Intersec Dubai event Gallagher Security.

- January 2025: Swann announced the MaxRanger4K Camera expansion suite at CES 2025 Swann.

Global Perimeter Security Market Report Scope

Perimeter security or perimeter protection are security solutions that utilize physical and software technology systems to protect from unauthorized access and intrusion, aiming to safeguard people, places, and property.

The perimeter security market is segmented by system (access control systems, alarms & notification systems, intrusion detection systems, video surveillance systems, other systems), by services (system integration & consulting, risk assessment & analysis, managed security services, maintenance & support), by end-user (commercial, military and defense, transportation, industrial, government, other end-users), by geography (North America, Europe, Asia-Pacific, Latin America, Middle East and Africa). The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

| Video Surveillance Systems | Cameras (IP, Thermal, Pan-Tilt-Zoom) |

| Video Analytics and VMS | |

| Access Control Systems | Biometric Readers |

| Card and Mobile Credential Readers | |

| Perimeter Intrusion Detection Systems (PIDS) | Fiber-Optic Sensors |

| Seismic and Magnetic Sensors | |

| Microwave and Radar Sensors | |

| Alarms and Notification Systems | |

| Barriers and Bollards (Fences, Gates, Vehicle Blockers) | |

| Lighting and Deterrent Systems | |

| Drone Detection and Counter-UAS |

| System Integration and Consulting |

| Risk Assessment and Analysis |

| Managed Security Services |

| Maintenance, Upgrade and Support |

| Commercial |

| Military and Defense |

| Transportation |

| Industrial |

| Government and Public Sector |

| Residential Estates and Smart Communities |

| Barrier-Mounted |

| Ground-Based / Open-Area |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| ASEAN | ||

| Australia | ||

| New Zealand | ||

| Rest of Asia Pacific | ||

| Middle East and Africa | Middle East | GCC |

| Turkey | ||

| Israel | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Egypt | ||

| Rest of Africa | ||

| By System | Video Surveillance Systems | Cameras (IP, Thermal, Pan-Tilt-Zoom) | |

| Video Analytics and VMS | |||

| Access Control Systems | Biometric Readers | ||

| Card and Mobile Credential Readers | |||

| Perimeter Intrusion Detection Systems (PIDS) | Fiber-Optic Sensors | ||

| Seismic and Magnetic Sensors | |||

| Microwave and Radar Sensors | |||

| Alarms and Notification Systems | |||

| Barriers and Bollards (Fences, Gates, Vehicle Blockers) | |||

| Lighting and Deterrent Systems | |||

| Drone Detection and Counter-UAS | |||

| By Services | System Integration and Consulting | ||

| Risk Assessment and Analysis | |||

| Managed Security Services | |||

| Maintenance, Upgrade and Support | |||

| By End-User | Commercial | ||

| Military and Defense | |||

| Transportation | |||

| Industrial | |||

| Government and Public Sector | |||

| Residential Estates and Smart Communities | |||

| By Deployment Type | Barrier-Mounted | ||

| Ground-Based / Open-Area | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Rest of Europe | |||

| Asia Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| ASEAN | |||

| Australia | |||

| New Zealand | |||

| Rest of Asia Pacific | |||

| Middle East and Africa | Middle East | GCC | |

| Turkey | |||

| Israel | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Egypt | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the current perimeter security market size and expected growth?

The perimeter security market stands at USD 88.02 billion in 2026 and is forecast to reach USD 141.29 billion by 2031, posting a 9.93% CAGR over the period.

Which system category generates the highest revenue?

Video surveillance systems lead with 45.12% revenue share in 2025, driven by AI-enabled analytics that convert passive footage into proactive threat intelligence.

Why are managed security services growing faster than traditional integration work?

Enterprises seek outcome-based contracts that include 24/7 monitoring, predictive maintenance, and guaranteed detection latencies, resulting in a 10.28% CAGR for managed services through 2031.

Which region represents the fastest demand expansion for perimeter solutions?

Asia Pacific is projected to record an 11.6% CAGR as data-center build-out, smart-city projects, and infrastructure upgrades accelerate adoption.

How are drones influencing perimeter security strategies?

The rise of drone-enabled contraband drops and reconnaissance missions is pushing facilities to install 3D radar, RF jamming, and AI classification modules, broadening the technology stack across the perimeter security market.

Page last updated on: