Market Trends of North America Satellite Manufacturing and Launch Systems Industry

This section covers the major market trends shaping the North America Satellite Manufacturing & Launch Systems Market according to our research experts:

The Advent of Reusable Launch Vehicles Driving Down Satellite Launch Costs

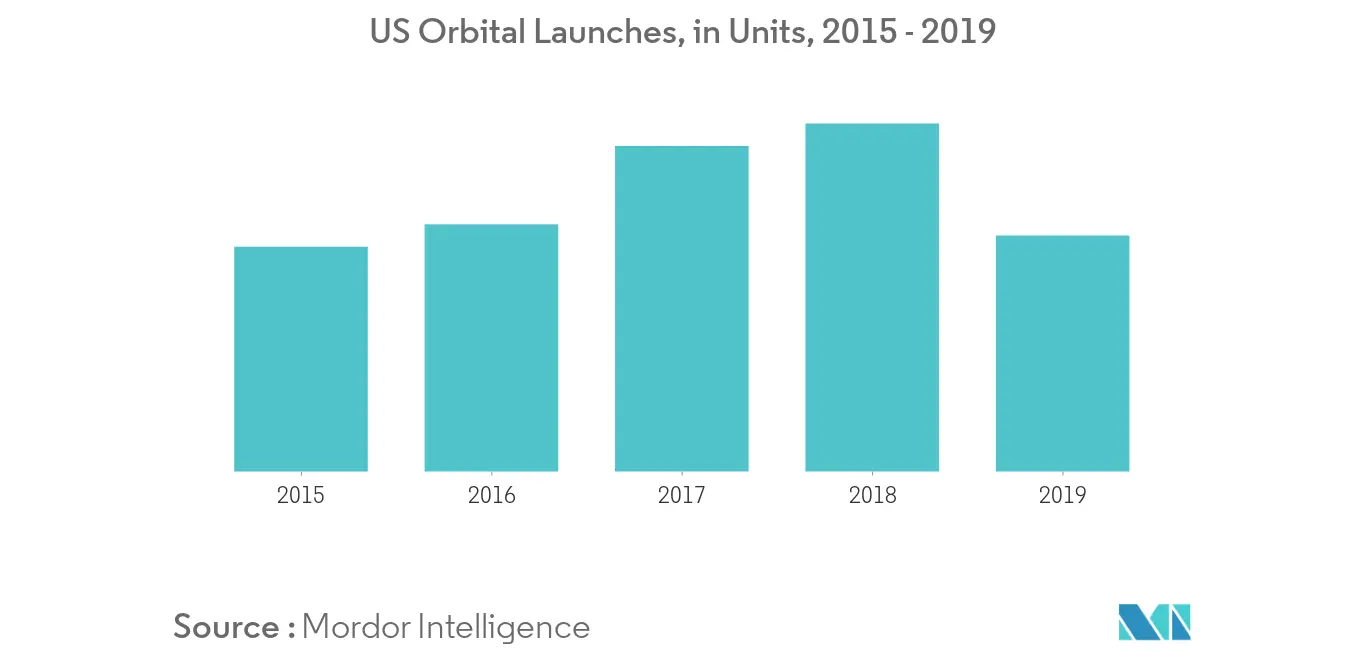

The associative costs of a satellite system are enormous and most of it accounts for launch and orbital placement. The relative positioning of a satellite is key for enhancing its effectiveness. Hence, proper considerations about critical mission parameters such as rocket type, payload size, and desired trajectory are vital to ensure a successful deployment. The development of all-electric satellites has resulted in the removal of conventional power systems that accounted for additional load for the launch vehicles. Thus, multiple all-electric satellites can be accommodated on a single launch vehicle such as Falcon 9, Ariane 5, Atlas 5, Proton, Soyuz, Sea Launch, and Delta IV, which has resulted in a drastic drop in associative launch costs. For instance, two Boeing 702 series satellites can be mounted on a single Ariane 5 launch module, which can account for a cost-saving up to 25% compared to the existing individual satellite launch options. Several companies offering launch services for satellites are investing in R&D of cost-effective launch systems. For instance, Rocket Lab, a US-based company has indigenously developed a rocket called 'Electron' which is expected to cut the cost and time to launch the satellites into space. The Electron is made up of advanced carbon composite materials for a strong and lightweight flight structure and features an oxygen/kerosene pump-fed engine that can provide a peak thrust of 192kN. It has a maximum payload capacity of 496lbs and hence, is typically suited for electric-powered small satellites. The unique structure and features, such as the innovative propulsion cycle reportedly offer significant launch cost savings. Moreover, since the critical propulsion unit of the launcher is recovered safely postorbital placement of the satellite, the launch vehicle can be attached to a fresh source of fuel in minimal time and flown for a certain number of upcoming missions. Thus, the decrease in prices will encourage the overall number of satellite launches and hence drive the revenues of the market in focus during the forecast period.

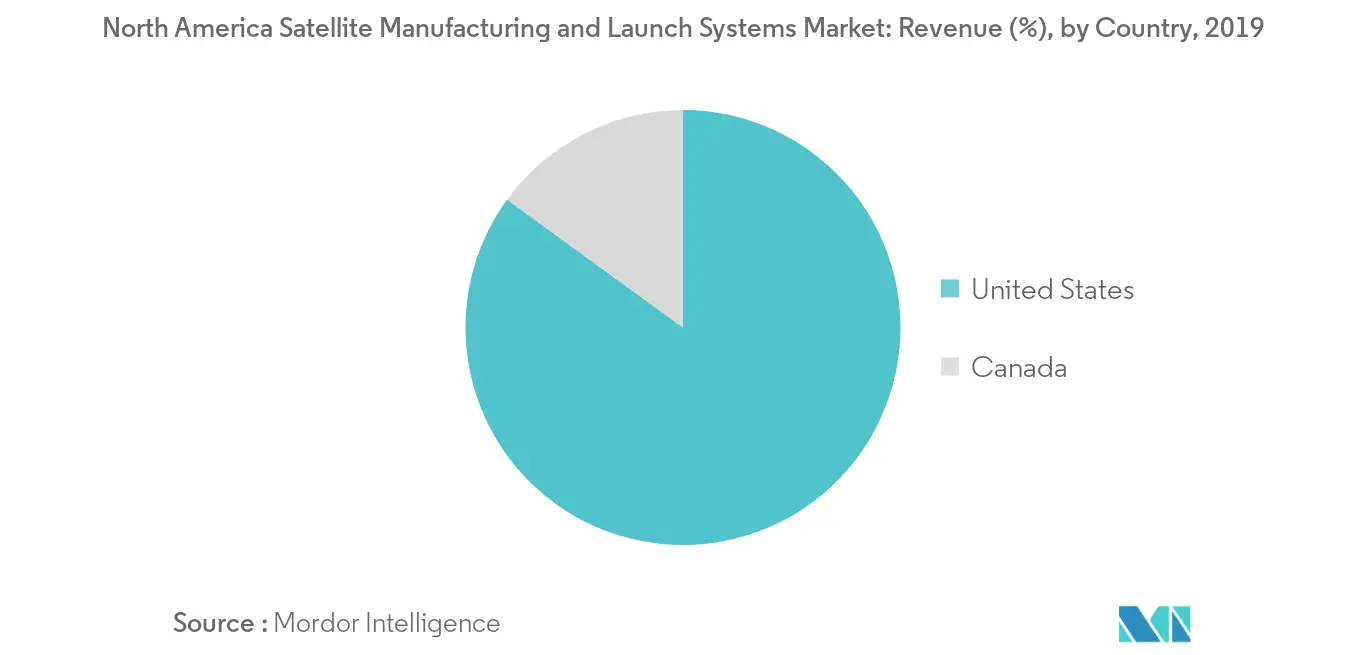

The United States to Dominate the Market During the Forecast Period

Owing to the plethora of potentials in several aspects of commercial and defense applications, the use of satellites has gained substantial acceptance in the US. Many small and private technology providers are investing in the design and launch of low-cost satellites. Also, the presence of prominent satellite manufacturing and launch firms such as NASA and SpaceX have bolstered the satellite industry in the country. To strengthen its defense capabilities, the US space agencies have initiated several R&D projects and are investing heavily in the development of advanced military satellites for communication and surveillance. For instance, in April 2019, Boeing was awarded a USD 605 million contract for the production of the US Air Force's 11th Wideband Global Satellite (WGS) communication satellite. The WGS constellation provides broadband communications to the US military and its allies and the manufacturing of the satellite is expected to be completed by November 2023. Through the WGS, the US Air Force aims to develop a more resilient architecture for its space missions. Also, in February 2019, United Launch Services, a subsidiary of the United Launch Alliance (ULA), was awarded a USD 441.7 million contract from the US DoD for launching military satellites into orbit. The contract includes launch vehicle production, mission integration, mission launch operations, and other activities pertaining to satellite launch. The contract also includes an option for additional launch services for the Space-Based Infrared System (SBIRS) GEO-6 program (due for launch in 2022) and the SBIRS GEO-5 program (due for launch in 2021), whose sensing capabilities are part of infrared surveillance and missile warning. Such developments are expected to foster the demand for satellites in the US during the forecast period.