Market Trends of Middle-East and Africa Defense Aircraft Aviation Fuel Industry

Aviation Turbine Fuel (ATF) to Dominate the Market

- Aviation turbine fuel, or jet fuel, is available in various grades and forms, including Jet B, JP-8, JP-5, etc., which are ideal for military aircraft.

- For military jets, the main fuel is JP-8, which is the military equivalent of Jet A-1 with the addition of corrosion inhibitors and anti-icing additives. Jet B is primarily used in military aircraft for cold weather performance, and JP-5 is also a jet fuel that has a higher flash point than JP-8.

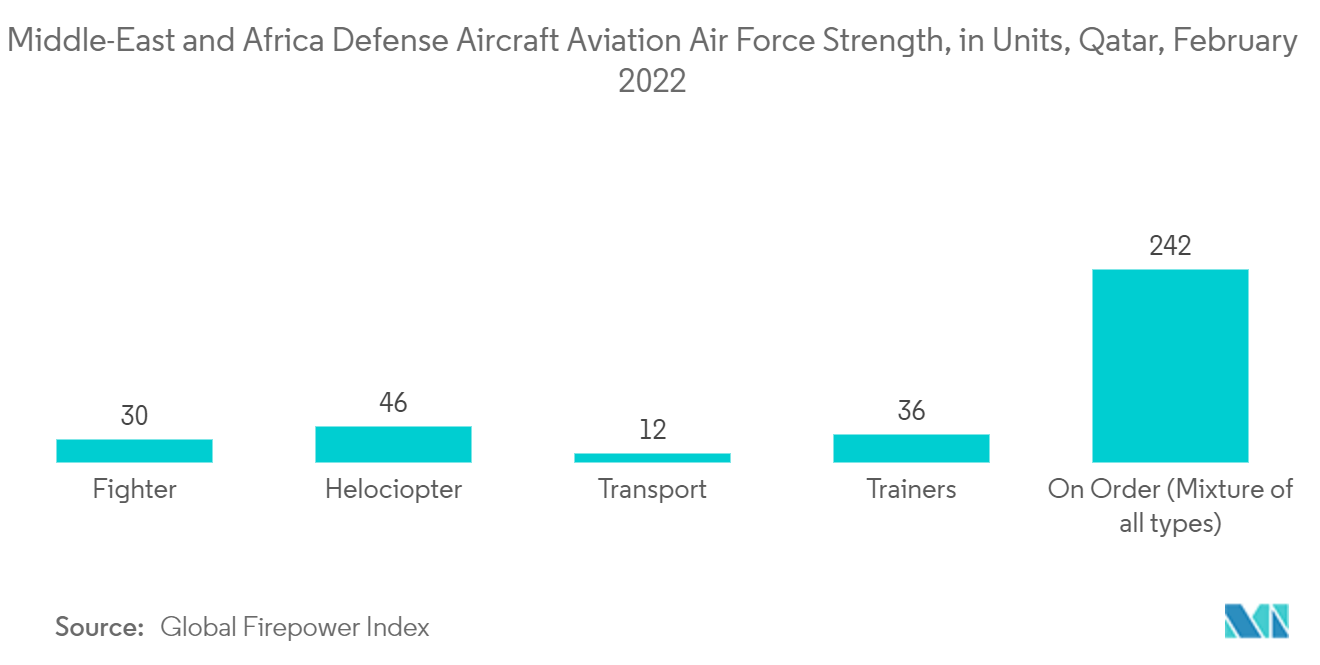

- Iran, Qatar, Saudi Arabia, and the United Arab Emirates (UAE) had high levels of military expenditure as a share of their gross domestic product in 2021.

- Qatar placed an order for 34 of the 777X, a sizable, twin-engine aircraft, in January 2022, as well as options for 16 additional aircraft.

- Furthermore, the Republic of Mali Air Force added various military transport aircraft and announced plans to add another 21 fighter jets to increase the military power of the country.

- Therefore, factors such as increasing investment and new aircraft additions in defense applications are expected to create demand for air turbine fuel in the Middle East and Africa defense aircraft aviation fuel market.

Understand The Key Trends Shaping This Market

Download Sample

Saudi Arabia to Dominate the Market

- The Royal Saudi Air Force (RSAF) is continuously developing and modernizing its air systems and is keen on acquiring modern fighters to provide the flexibility of rapid deployment and the ability to intervene quickly.

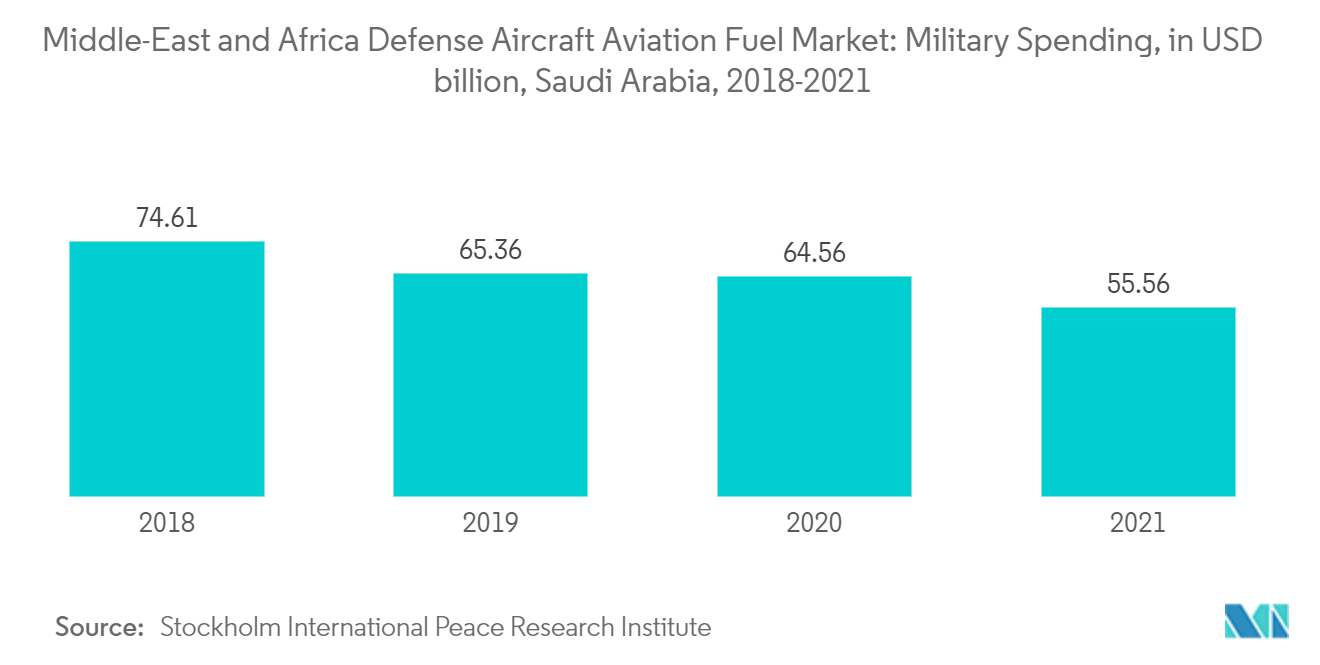

- In 2021, Saudi Arabia's military spending amounted to an estimated USD 55.564 billion, down from 64.558 billion in 2020. It was the third-largest military spender globally and by far the largest military spender in the Gulf region.

- In 2021, Saudi Arabia signed a financing agreement worth USD 3 billion to partially finance the requirements for aircraft it ordered. The amount covers the airline's aircraft financing requirements until mid-2024, helping finance the purchases of 73 aircraft previously ordered, it said in a statement. The airline has ordered Airbus A320neo, A321neo, A321XLR, and Boeing 787-10 jets.

- Fighter jets account for a large share of the total Saudi Arabian Air Force fleet-about 54%-followed by trainers and helicopters.

- Furthermore, Saudi Arabia's air defenses are undergoing realignment to provide a 360-degree air defense umbrella that could counter threats emerging from all sides, especially drone attacks.

- Therefore, with the increasing military activities and increasing defense expenditure, the market for defense aircraft aviation fuel in Saudi Arabia is expected to dominate during the forecast period.

Get Analysis on Important Geographic Markets

Download Sample