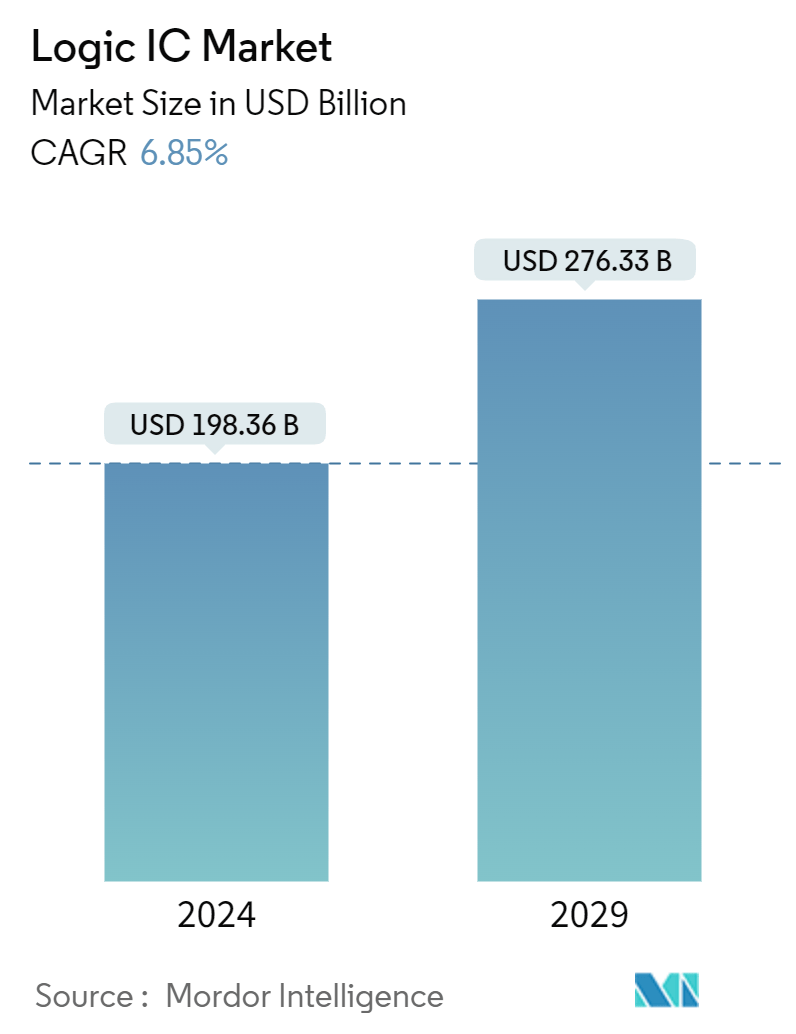

Market Size of Logic IC Industry

| Study Period | 2019 - 2029 |

| Market Size (2024) | USD 198.36 Billion |

| Market Size (2029) | USD 276.33 Billion |

| CAGR (2024 - 2029) | 6.85 % |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

Major Players

*Disclaimer: Major Players sorted in no particular order |

Need a report that reflects how COVID-19 has impacted this market and its growth?

Logic IC Market Analysis

The Logic IC Market size is estimated at USD 198.36 billion in 2024, and is expected to reach USD 276.33 billion by 2029, growing at a CAGR of 6.85% during the forecast period (2024-2029). In terms of shipment volume, the market is expected to grow from 65.24 billion units in 2024 to 80.10 billion units by 2029, at a CAGR of 4.19% during the forecast period (2024-2029).

Ongoing advancements in semiconductor manufacturing processes have led to the development of more complex and efficient logic ICs. Smaller transistor sizes, improved performance, and lower power consumption enable the creation of high-performance logic ICs for a wide range of applications. A logic IC is very flexible and can be used in various applications. One can configure them to perform multiple logical functions, such as AND, OR, NOT, and XOR. This flexibility allows for designing and developing intelligent circuits that meet requirements in different industries, such as consumer electronics, automotive, telecommunications, and industry automation.

- Logic ICs have significantly aided the miniaturization and integration of electronic devices. The development of the technology to manufacture semiconductors has produced small, more complex logic circuits on a single chip in recent years. This integration increases functionality while reducing electronic systems' physical size and energy consumption so that they can be used in portable devices, wireless technology, or space-constrained applications. Display drivers, general purpose logic, and MOS touch screen controllers are some of the logic components that have gained significant market traction in recent years.

- Furthermore, advances in end-user industries have created the need for small and robust semiconductor devices. For instance, nowadays, smartphones require a smaller PCB board, unlike traditional PCB boards. There has also been the advent of IoT devices, such as wearables with irregular and different shapes, which can only be achieved through miniaturization. This is expected to boost the need for miniaturized IC components significantly.

- The advent of the IoT and IIoT has largely impacted the design and size of electronics, with the introduction of technologies like smart homes, offices, wearables, remote monitoring, and control. Moreover, OEMs and designers consider miniaturization a primary focus while creating wearable technologies.

- Another advancement that demands miniaturized electronic components is portable electronic equipment, which requires smaller and thinner semiconductor systems for saving space and miniaturization. Due to highly integrated, high-speed applications like aerospace and electric vehicles, the demand for improved electrical performance to minimize noise effects is also evident. As a result of these considerations when designing end products, logic IC components are becoming increasingly important in developing advanced electronic systems.

- Logic ICs are expected to perform a wide range of complex functions. The demand for more state-of-the-art features and capabilities in electronic devices grows as technology advances. Designers need to incorporate complex logic circuits and algorithms to meet these requirements. This increased functionality leads to larger and more intricate designs, making it challenging to manage and optimize the complex interactions between different components.

- The market has undergone substantial changes due to the COVID-19 pandemic, impacting customer behavior, business revenues, and various aspects of corporate operations. The pandemic revealed previously unnoticed risks on the supply side, potentially resulting in shortages of essential parts and components. Consequently, semiconductor companies are proactively restructuring their supply chains to enhance resilience, and these adjustments may persist in the post-pandemic era.