Kenya Telecom Tower Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

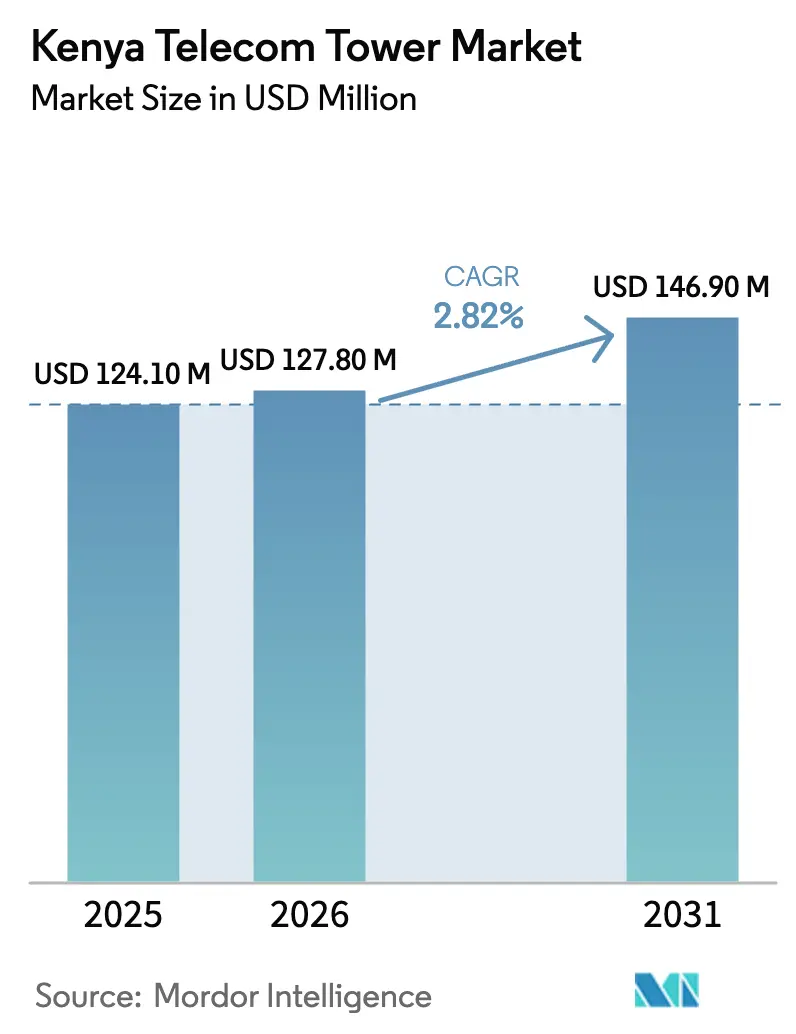

| Base Year Market Size (2025) | USD 124.10 Million |

| Market Size (2026) | USD 127.80 Million |

| Market Size (2031) | USD 146.90 Million |

| Growth Rate (2026 - 2031) | 2.82% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Kenya Telecom Tower Market Analysis by Mordor Intelligence

The Kenya telecom tower market size is expected to increase from USD 124.1 million in 2025 to USD 127.8 million in 2026 and reach USD 146.9 million by 2031, growing at a CAGR of 2.82% over 2026-2031. The measured advance reflects a structural shift toward asset-light tenancy models, rooftop densification, and renewable-energy retrofits that soften headline growth even as mobile data traffic rises steeply. Direct-to-device satellite partnerships, rapid fiber and fixed-wireless-access rollouts, and a volatile shilling all temper new build momentum, yet lattice and monopole towers remain indispensable for broad-area coverage. Independent towercos are responding with solar-hybrid power systems that trim off-grid operating costs by up to 35%, neutral-host smart-poles that meet aesthetic codes, and edge-ready designs that future-proof sites for 5G and beyond. These moves sustain a resilient, if not spectacular, expansion profile for the Kenya telecom tower market.

Key Report Takeaways

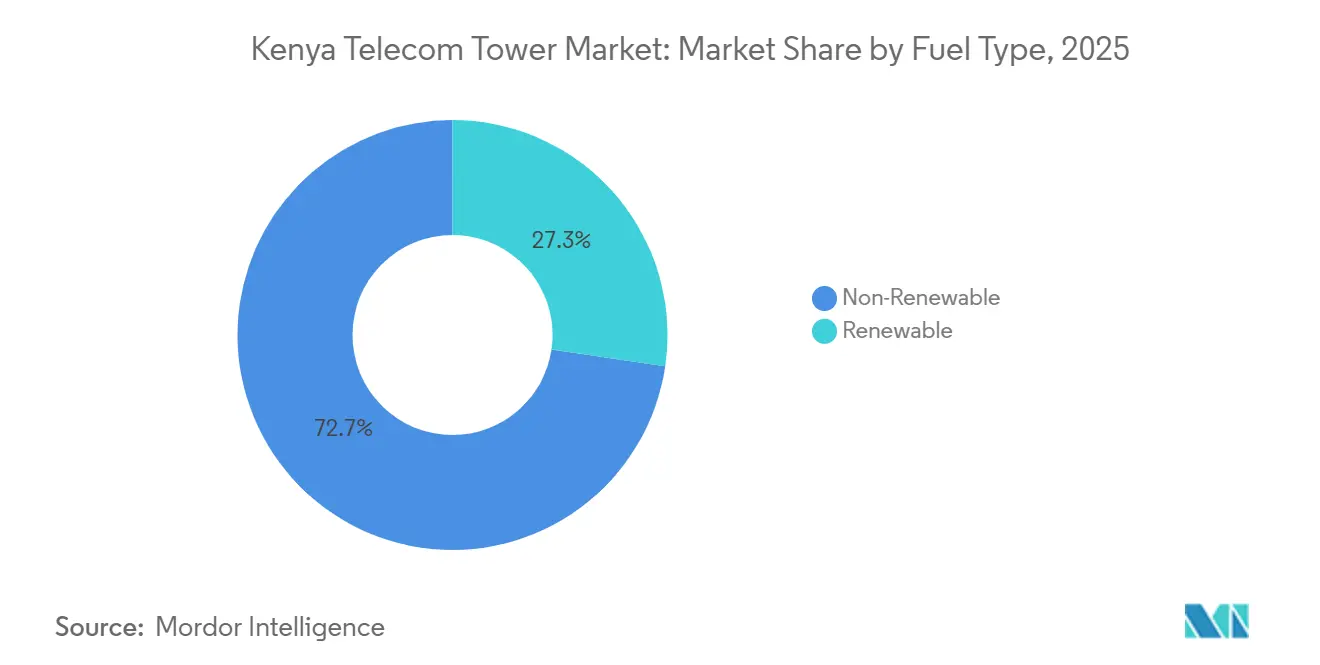

- By fuel type, non-renewable sources held 72.67% of the Kenya telecom tower market share in 2025, while renewable configurations are advancing at a 5.13% CAGR to 2031.

- By tower type, lattice structures led with a 43.17% revenue share in 2025, whereas stealth towers are projected to grow the fastest at a 4.76% CAGR through 2031.

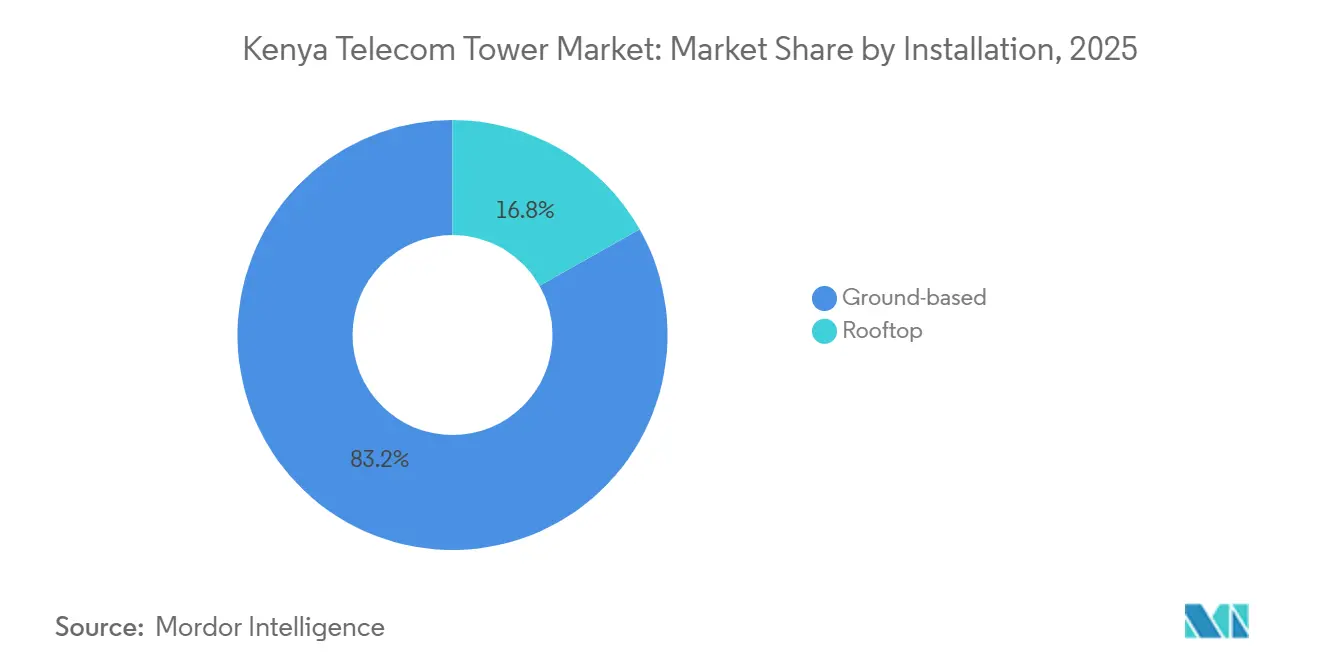

- By installation, ground-based sites accounted for 83.19% of the Kenya telecom tower market size in 2025 and rooftop sites are expanding at a 3.62% CAGR to 2031.

- By ownership, operator-controlled assets represented 43.67% of the total in 2025, yet privately owned infrastructure is growing at a 3.23% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Kenya Telecom Tower Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Accelerated 5G Standalone Rollout in Urban Centers | +0.8% | Nairobi County, Mombasa, Kisumu, Nakuru | Medium term (2-4 years) |

| Government-Led Rural Digitization via USF Phase II Grants | +0.6% | National, priority in Turkana, Mandera, Wajir | Long term (≥ 4 years) |

| Escalating Mobile Data Traffic Requiring Network Densification | +0.7% | National, urban and peri-urban | Short term (≤ 2 years) |

| Energy-as-a-Service Solar-Hybrid Models Cutting OPEX in Off-Grid Sites | +0.5% | Rift Valley, Western, Coastal regions | Medium term (2-4 years) |

| Emergence of Neutral-Host Smart-Pole Solutions for Smart Cities | +0.3% | Nairobi County, Konza Technopolis, Mombasa | Long term (≥ 4 years) |

| Low-Earth Orbit Backhaul Solutions Unlocking Ultra-Remote Coverage | +0.2% | Turkana, Marsabit, coastal hinterlands | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Accelerated 5G Standalone Rollout In Urban Centers

Safaricom lifted its 5G footprint from 803 active sites in fiscal 2024 to 1,700 by March 2025, and Airtel Kenya moved from pilot scale to 690 live sites by mid-2024, with both operators signalling site counts above 3,000 before 2029.[1]Safaricom PLC, “Annual Report and Financial Statements 2025,” safaricom.co.ke The surge drives immediate demand for tower reinforcement to bear massive-MIMO antennas and edge modules, yet most upgrades repurpose existing steel, muting greenfield orders. Kenya counted 1.5 million 5G subscribers in September 2025 who averaged 40 GB of data each month, nearly triple 4G usage, forcing backhaul upgrades that favour rooftop and small-cell infill over new macros. American Tower Corporation has redesigned 20% of its portfolio to host 5G radios and lithium-ion packs, shortening maintenance windows and widening urban leasing options.

Government-Led Rural Digitization Via USF Phase II Grants

Kenya’s Universal Service Fund earmarked KES 40 billion (USD 310 million) between 2023-2027 to finance 100,000 km of fiber, 25,000 Wi-Fi hotspots, and 1,450 ICT hubs in high-cost areas, releasing Phase 4 tenders for 136 sub-locations in March 2025.[2]Universal Service Fund Kenya, “USF Strategy 2023-2027,” usf.go.ke American Tower Corporation Kenya has 160 candidate sites aligned with these subsidies, lowering project risk where commercial returns are thin. Solar-hybrid designs add 15-20% upfront capex but slash diesel dependence by 90%, a vital trade-off in Mandera and Turkana where fuel logistics dominate opex. The funding gap of KES 12 billion (USD 93 million) tempers build velocity, stretching award-to-operation cycles to four years.

Escalating Mobile Data Traffic Requiring Network Densification

Mobile subscriptions reached 60.2 million in June 2025, and quarterly broadband payload hit 674,240 terabytes, up 12.8% sequentially, propelled by streaming video and mobile money.[3]Communications Authority of Kenya, “Quarterly Sector Statistics Report: Q4 FY 2024/2025,” ca.go.ke Operators split macro cells and deploy rooftop minis to stabilize quality-of-service, typically doubling site density without the six-month permitting drag of new macros. Safaricom invested KES 388.5 billion (USD 3 billion) during 2021-2025 in fiber backhaul and tower upgrades, but spectrum refarming and carrier aggregation allow demand to be served with fewer fresh structures. Consequently, each additional terabyte now calls for fewer macro towers than a decade earlier.

Energy-as-a-Service Solar-Hybrid Models Cutting OPEX In Off-Grid Sites

Safaricom operated 1,432 solar-hybrid sites in fiscal 2025 and targets 3,000 more by 2027, aiming for a 50% diesel cut. American Tower Corporation Kenya fits 99% of new builds with photovoltaics and 100% with lithium-ion batteries, trimming fuel and maintenance bills by 90%.[4]American Tower Corporation, “Kenya Operations Overview,” americantower.com GSMA modelling shows 35% opex and 25% capex savings over 15 years for hybrid systems relative to diesel-only designs. Energy-as-a-service contracts shift equipment risk to specialized vendors, suiting Rift Valley and Coast counties where grid outages are frequent. Payback periods of three years justify the medium-term uplift to the Kenya telecom tower market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Kenyan Shilling Depreciation Elevating USD-Denominated Lease Costs | -0.5% | National | Short term (≤ 2 years) |

| Prolonged Permit and Wayleave Approvals in County Governments | -0.4% | Nairobi, Mombasa, high-tenure counties | Medium term (2-4 years) |

| Direct-to-Device Satellite Broadband Substituting Rural Towers | -0.3% | Northern Kenya, ASAL regions | Medium term (2-4 years) |

| Rapid Fiber and 5G FWA Adoption Reducing Future Tenancies | -0.3% | Urban and peri-urban fiber corridors | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Kenyan Shilling Depreciation Elevating USD-Denominated Lease Costs

The shilling weakened from KES 129 per USD in 2023 to KES 155 in 2024, inflating tower rent obligations by more than 20% for operators paid in local currency. Airtel Kenya’s portfolio of 4,300 leases and Telkom Kenya’s KES 7.1 billion (USD 55 million) arrears dispute with American Tower Corporation in 2023 spotlight margin erosion and payment risk. Some towercos now quote shilling-linked rents with CPI escalators, but that flips forex exposure back to their balance sheets, tightening debt covenants. Short-term volatility therefore curtails new long-term tenancies and tempers the Kenya telecom tower market expansion.

Prolonged Permit And Wayleave Approvals In County Governments

Kenya’s 47 counties apply divergent planning rules, stretching approvals for new sites to 6-12 months, especially in Nairobi and Mombasa where land tenure is complex and community opposition vocal. Environmental impact assessments add further delay near water catchments and heritage zones. American Tower Corporation and Atlas Towers both cite permitting as the single biggest schedule slippage factor, forcing larger candidate pipelines and higher working capital locks. The Communications Authority proposes a one-stop digital portal, yet until tested, medium-term drag persists for the Kenya telecom tower market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Fuel Type: Renewable Uptake Gains Momentum

Non-renewable generators held 72.67% of the Kenya telecom tower market share in 2025, underscoring the historical dominance of diesel-powered sites that still anchor national coverage. Renewable configurations are expanding at a 5.13% CAGR through 2031 and are steadily enlarging their slice of the Kenya telecom tower market size as solar-hybrid kits prove cost-effective in fuel-scarce areas. Safaricom’s plan to retrofit 3,000 additional renewable sites by 2027 exemplifies anchor-tenant pressure for greener leases.

Tower companies now specify lithium-ion batteries and photovoltaic arrays on nearly every new build, cutting operating outlays by up to one-third and shrinking carbon footprints. Anchor tenants such as Safaricom have tethered lease renewals to progress on green power, accelerating the retrofit cycle across Rift Valley, Western, and Coastal regions. Feed-in tariff and net-metering policies add a modest revenue tailwind, yet administrative bottlenecks still curb widespread grid sell-back. As diesel logistics grow pricier and environmental disclosure rules tighten, renewable hybrids are poised to approach parity with legacy gensets before the end of the forecast window.

By Tower Type: Urban Codes Propel Stealth Installations

Lattice structures commanded 43.17% of the Kenya telecom tower market share in 2025, favored for ruggedness and low fabrication cost in rural tracts. Stealth towers, however, are advancing at a 4.76% CAGR as Nairobi, Mombasa, and Kisumu embed visual-impact clauses in their zoning ordinances, forcing operators to camouflage antennas within flagpoles, tree-masts, or façade-mounted pods.

The 20%-plus cost premium tied to custom cladding is increasingly offset by faster permits and reduced community pushback. Smart-city pilots at Konza Technopolis further elevate demand for neutral-host smart poles that meld 5G radios, lighting, and IoT sensors into a single column, creating new tenancy revenue streams. Guyed towers are relegated to ultra-tall microwave links, while monopoles serve land-constrained peri-urban corridors where aesthetic strictness falls between lattice and full stealth. The design mix therefore tilts toward structures that balance load capacity with low visual intrusion, realigning capital budgets throughout the Kenya telecom tower market.

By Installation: Rooftop Densification Accelerates

Ground-based sites represented 83.19% of the Kenya telecom tower market size in 2025, reflecting two decades of macro coverage builds across open land parcels. Rooftop placements are growing at a 3.62% CAGR to 2031 as landlords monetize vertical real estate and mobile network operators bypass protracted land acquisition cycles. Safaricom and Airtel both anchor rooftop micro-cells in Nairobi’s CBD and along Mombasa’s high-rise coast to fill 4G and 5G capacity holes.

Structural audits and reinforcement works raise upfront costs by roughly one-tenth, yet these expenses are outweighed by faster approvals and proximity to user clusters inside Nairobi’s CBD and Mombasa’s coastal high-rises. Rooftops also enable targeted small-cell overlays that relieve 4G congestion and host early 5G radios without disturbing street-level aesthetics. While ground-based lattice and monopole towers will continue to blanket rural and peri-urban terrain, the share of rooftop nodes is set to climb toward one-fifth of active assets by 2031, embedding a more vertical dimension into the Kenya telecom tower market.

By Ownership: Independents Capture Growing Slice

Operator-controlled assets accounted for 43.67% of the Kenya telecom tower market share in 2025, yet the private segment is moving ahead at a 3.23% CAGR as carriers unlock capital through sale-and-leaseback transactions. Independent towercos already oversee the single largest block of the national grid and offer multi-tenant economics that lower per-site rent for each occupant. American Tower Corporation Kenya already controls more than one-third of passive infrastructure, offering multi-tenant economics and currency-hedged leases.

Airtel’s long-term renewal with American Tower Corporation and Atlas Towers’ equity infusion earmarked for greenfield builds illustrate the momentum behind the outsourced model. Private owners bundle energy-as-a-service contracts, remote monitoring, and currency-hedged leases, relieving operators of non-core burdens while protecting towerco cash flows. Telkom Kenya’s lease arrears and subsequent site disconnections highlight the risks of retaining steel on balance sheets when revenues falter. As scale, diversification, and capital-market access tilt the playing field, independent platforms are on course to hold a majority share of the Kenya telecom tower market by 2031.

Geography Analysis

Urban counties, led by the Nairobi Metropolitan Area, capture the largest portion of the Kenya telecom tower market share as dense population, high data traffic, and stringent quality-of-service targets compel continual densification. Nairobi’s cluster of high-rise offices and residential towers accelerates demand for rooftop and stealth formats, while a tightening visual-impact code channels new macros toward disguised smart poles. Mombasa mirrors this pattern along its tourism-driven coastline, adding corrosion-resistant solar-hybrid kits that lessen diesel logistics and meet county sustainability goals.

Rift Valley and Western regions host a fast-growing roster of lattice towers financed under Universal Service Fund tranches, filling voice and mobile money coverage gaps across agrarian belts. Solar-hybrid power dominates these builds because grid feeds are intermittent and fuel deliveries are costly. Kisumu and Nakuru, the lakefront and mid-rift commercial hubs, blend ground-based macros on municipal land with rooftop pods atop shopping centers, balancing reach with community acceptance.

Northern arid and semi-arid lands such as Turkana and Marsabit remain the country’s thinnest served zones, where harsh weather and sparse populations weigh on macro tower economics. Here, low-earth-orbit satellite backhaul and next-generation fixed wireless pilots present alternative access routes, yet subsidy-backed solar-hybrid monopoles are still slated to roll out through 2027. Collectively, these geographic contrasts ensure that growth pockets coexist with saturation points, shaping a regionally diverse Kenya telecom tower market size outlook.

Competitive Landscape

American Tower Corporation Kenya leads the field with a 38.81% installed base, but remains safely below the dominance line that would trigger aggressive antitrust remedies. Its blueprint rests on three pillars: universal service builds in subsidy regions, near-universal solar integration on new sites, and an expanding edge-compute module program that attracts high-bandwidth tenants. The company’s 12-year master lease renewal with Airtel locked in predictable escalators while freeing the operator’s balance sheet for 5G spectrum purchases.

Atlas Towers, fortified by an October 2025 equity injection from STOA Infra, is racing to light up 400 greenfield sites across underserved counties, pairing compact lattice kits with lithium-ion battery packs to win cost-of-service tenders. Sealtowers differentiates through rapid-deploy lattice designs that arrive pre-assembled, enabling same-week installations on remote ridgelines and reducing diesel truck-rolls by bundling battery as a service.

Mobile network operators remain pivotal as both anchor tenants and partial competitors. Safaricom’s captive East Africa Tower Company Limited manages 1,700 5G-ready sites, maintaining strategic control of high-traffic corridors while leasing incremental coverage from independents. Airtel targets a 33% capacity jump to roughly 5,700 sites by 2028, leaning heavily on rooftop conversions to compress lead times in Nairobi and Mombasa. Telkom Kenya’s financial distress, punctuated by nearly 900 site disconnections, has opened swap-in opportunities for towercos willing to assume stranded leases. Meanwhile, the advent of direct-to-device satellite links and fixed-wireless-access collaborations presses incumbents to diversify revenue via neutral-host smart poles and managed energy services, keeping rivalry lively within the Kenya telecom tower market.

Kenya Telecom Tower Industry Leaders

American Tower Corporation Kenya (ATC Kenya)

Atlas Towers Kenya

Sealtowers Limited

Safaricom PLC

Airtel Kenya Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Airtel Kenya and Starlink confirmed testing of direct-to-device satellite links ahead of commercial launch later in 2026, targeting unserved northern counties.

- December 2025: Airtel Kenya and Starlink unveiled a direct-to-consumer satellite partnership to enable standard 4G phones to latch onto low-earth-orbit signals, reducing the need for rural macro towers.

- October 2025: STOA Infra invested in Atlas Towers Kenya to accelerate greenfield builds and solar-hybrid deployment in underserved regions.

- June 2025: Tarana Wireless and Microsoft partnered to roll out next-generation fixed-wireless-access across Kenya, offering fiber-grade speeds over unlicensed spectrum.

Kenya Telecom Tower Market Report Scope

The telecommunication market is largely concerned with the operations and provision of infrastructure for transmitting data - voice, image, sound, text, and video. To expand its network and services, the telecommunication market relies on towers, which are used to mount telecommunication networking and power equipment.

The Kenya Telecom Tower Market Report is Segmented by Fuel Type (Renewable, and Non-Renewable), Tower Type (Lattice Tower, Guyed Tower, Monopole Tower, and Stealth Tower), Installation (Rooftop, and Ground-based), Ownership (Operator-owned, Joint Venture, Private-owned, and MNO Captive), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

| Renewable |

| Non-Renewable |

| Lattice Tower |

| Guyed Tower |

| Monopole Tower |

| Stealth Tower |

| Rooftop |

| Ground-based |

| Operator-owned |

| Joint Venture |

| Private-owned |

| MNO Captive |

| By Fuel Type | Renewable |

| Non-Renewable | |

| By Tower Type | Lattice Tower |

| Guyed Tower | |

| Monopole Tower | |

| Stealth Tower | |

| By Installation | Rooftop |

| Ground-based | |

| By Ownership | Operator-owned |

| Joint Venture | |

| Private-owned | |

| MNO Captive |

Key Questions Answered in the Report

How large is the Kenya telecom tower market today?

The Kenya telecom tower market size is USD 127.8 million in 2026 and is projected to reach USD 146.9 million by 2031.

What is the expected compound growth rate for towers in Kenya?

The market is forecast to grow at a 2.82% CAGR between 2026 and 2031.

Which segment is expanding fastest within the tower ecosystem?

Renewable-powered sites register the highest growth, advancing at a 5.13% CAGR as operators embrace solar-hybrid energy models.

Who is the leading independent tower company in Kenya?

American Tower Corporation Kenya leads with about 38.81% of passive infrastructure.

How is 5G rollout affecting tower demand?

Rapid 5G standalone expansion in urban centers is lifting upgrade activity, yet operators favor densifying existing poles over extensive greenfield builds, moderating overall tower growth.

Will satellite connectivity reduce future tower builds?

Direct-to-device satellite partnerships could displace some rural tower demand, but dense urban and peri-urban coverage still relies on terrestrial structures for capacity and latency needs.

Page last updated on: