Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

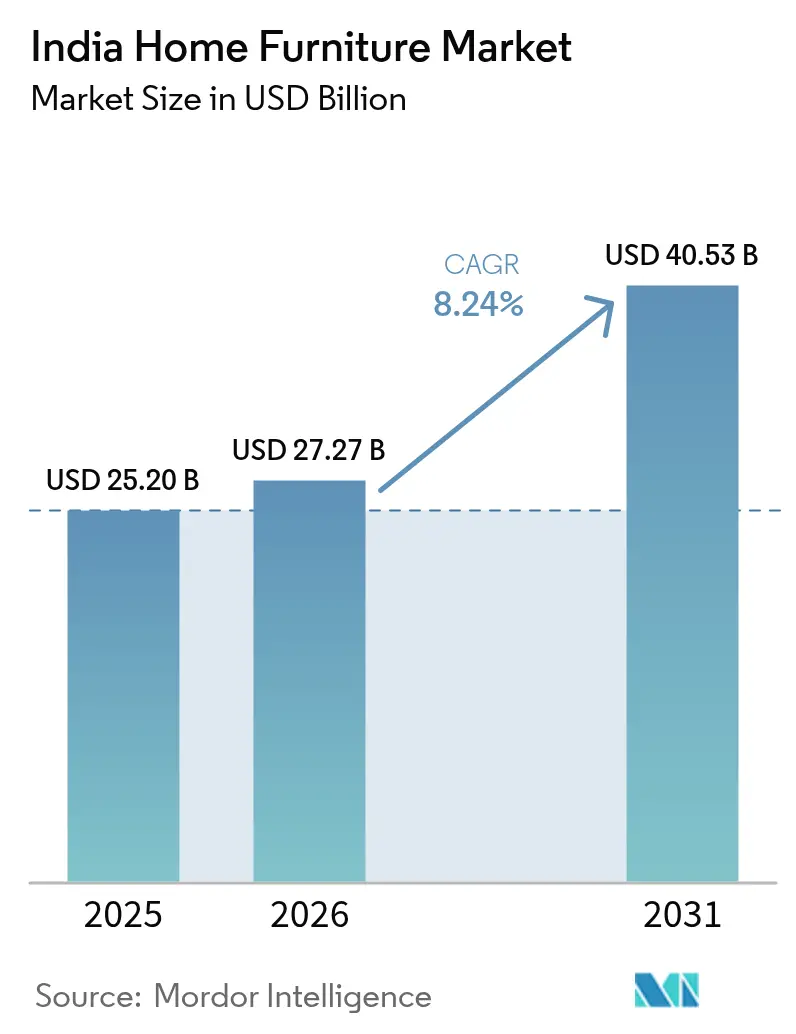

| Base Year Market Size (2025) | USD 25.20 Billion |

| Market Size (2026) | USD 27.27 Billion |

| Market Size (2031) | USD 40.53 Billion |

| Growth Rate (2026 - 2031) | 8.24% CAGR |

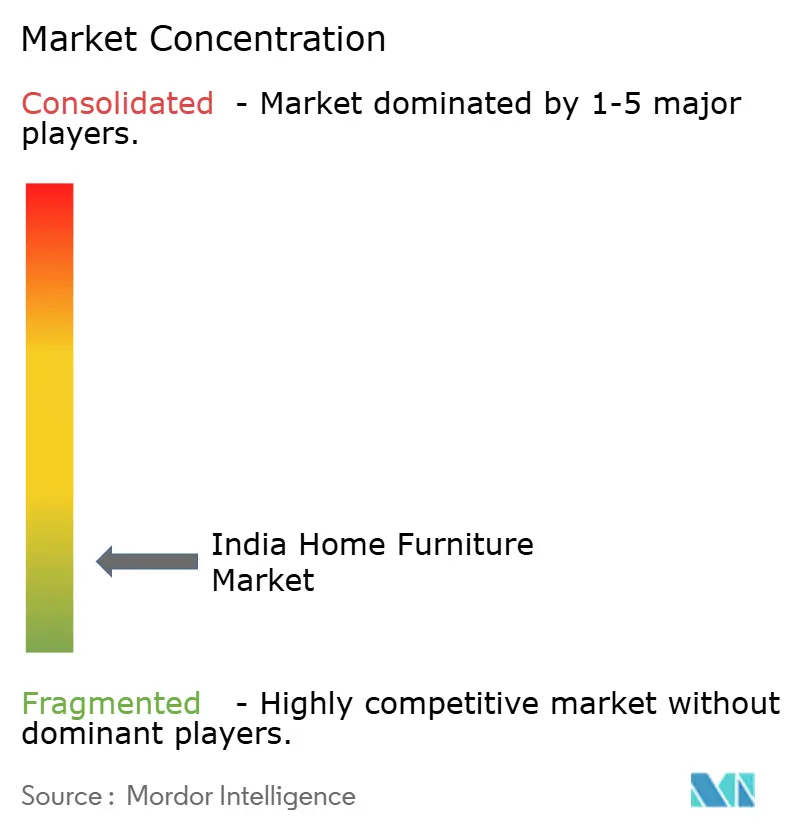

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

India Home Furniture Market Analysis by Mordor Intelligence

The India home furniture market size is expected to increase from USD 25.20 billion in 2025 to USD 27.27 billion in 2026 and reach USD 40.53 billion by 2031, growing at a CAGR of 8.24% over 2026-2031. This growth outlook reflects formalization gains as the Furniture Quality Control Order took effect in February 2026, which elevates product standards and nudges demand toward certified and branded assortments across seating, tables, storage units, and beds. New-home formation is sustaining demand as urban and rural housing completions under PMAY delivered 96.02 lakh urban homes and created a steady base of first-time furniture buyers[1]Editorial Desk, “Economic Survey: More than 96 lakh homes delivered to beneficiaries under PMAY-U,” Hindustan Times, hindustantimes.com. Financialization also underpins upgrades since housing credit more than tripled over the decade to March 2025, which is supporting discretionary home upgrades from entry models to mid-range and premium assortments. On the distribution side, omnichannel models are expanding reach as IKEA reports that online sales already contribute above 30% of India revenue, while it accelerates store expansion to lift access and speed. Competitive intensity remains elevated as international entrants step up investment and domestic leaders scale omnichannel footprints with design-led formats, while D2C specialists expand assortments and coverage to tap younger buyers across metros and tier-II cities.

Key Report Takeaways

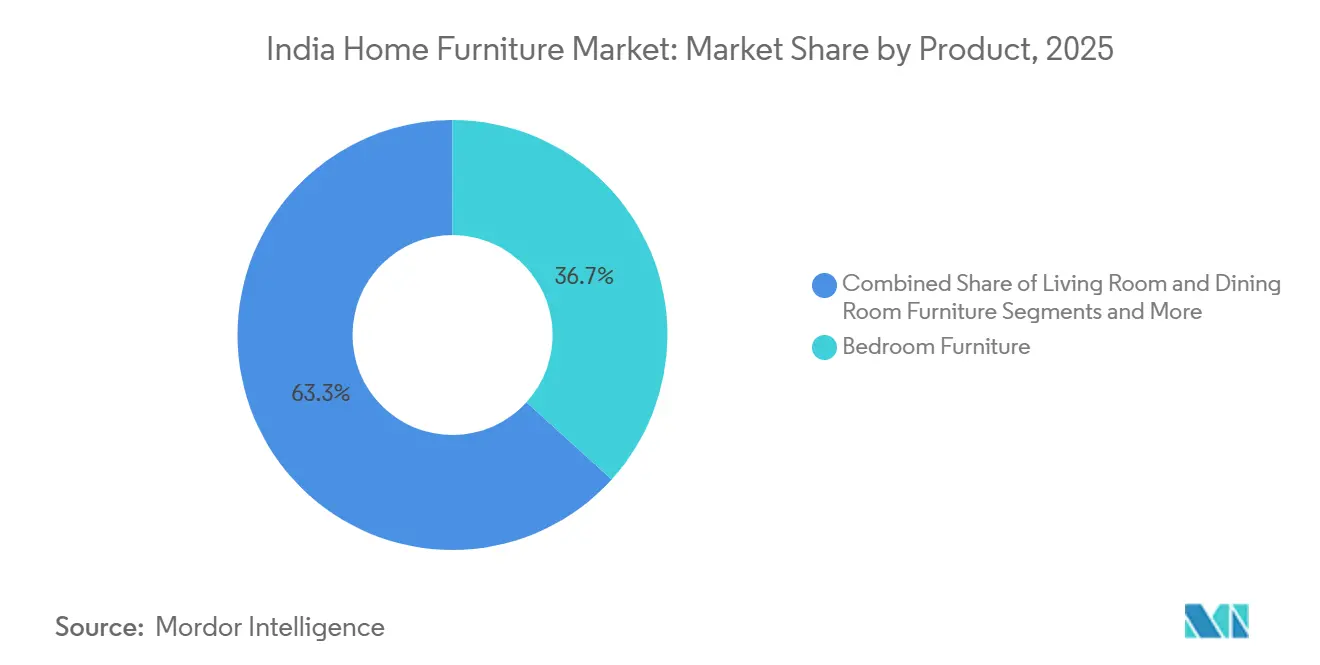

- By product type, living room and dining room furniture led with 36.72% of the India home furniture market share in 2025, while home office furniture is projected to expand at an 11.60% CAGR through 2031.

- By material, wood held 61.95% of the India home furniture market share in 2025, whereas metal is forecast to grow at a 13.73% CAGR through 2031.

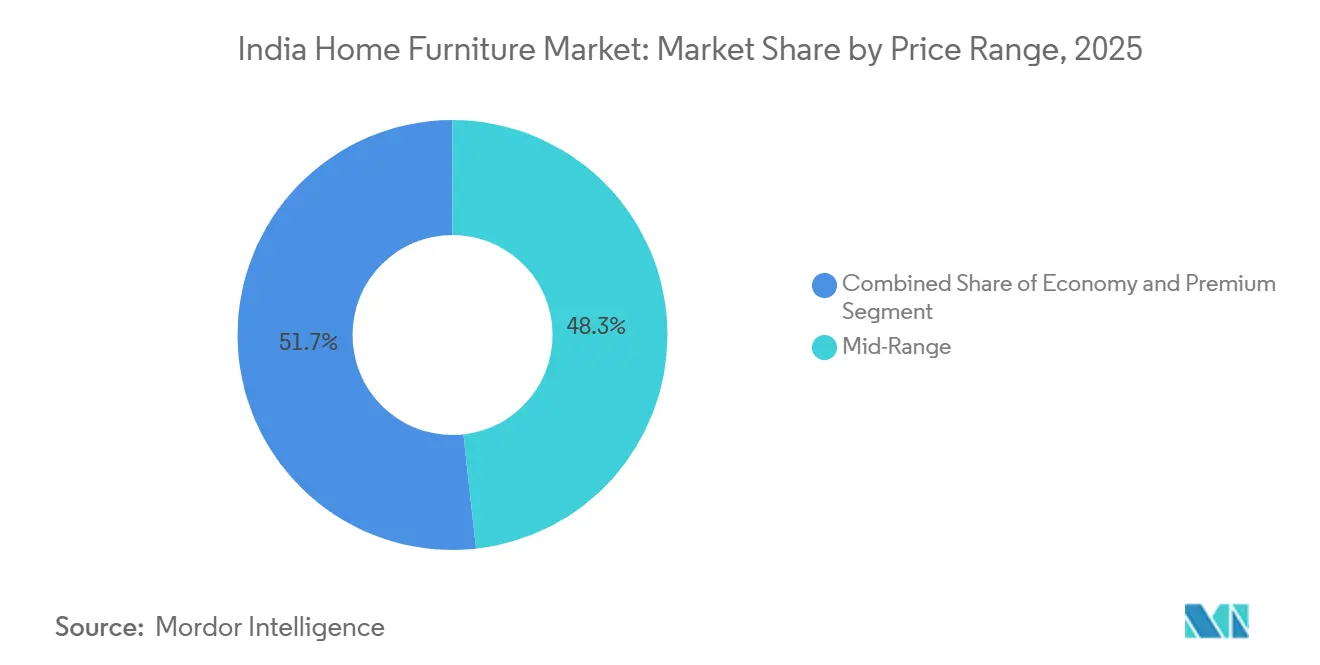

- By price range, mid-range captured 48.25% of the India home furniture market share in 2025, while premium is expected to advance at an 11.34% CAGR through 2031.

- By distribution channel, specialty furniture stores accounted for 74.85% of the India home furniture market share in 2025, whereas online channels are projected to grow at a 13.62% CAGR through 2031.

- By geography, North India held 28.90% of the India home furniture market share in 2025, while East India is projected to expand at a 9.45% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

India Home Furniture Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Compact Urban Homes Are Driving Modular, Space-Saving Purchases | +1.8% | Global, with early gains in Mumbai, Bengaluru, Delhi NCR, Pune | Medium term (2-4 years) |

| Omnichannel Expansion (Experience Centers + E-Commerce) Lifting Organized Penetration | +1.5% | APAC core, spill-over to tier-II cities nationwide | Short term (≤ 2 years) |

| Government-Backed Housing Completions Sustaining New-Home Furnishing Cycles | +2.2% | National, concentrated in PMAY-U metros and PMAY-G rural clusters | Long term (≥ 4 years) |

| Premiumization Within Mid-Range Through Financing (EMI/BNPL), Improving Ticket Sizes | +1.3% | North America & EU adoption trends mirrored in Indian tier-I cities | Medium term (2-4 years) |

| BIS QCO Rollout (Furniture, Plywood, Boards), Raising Quality Baseline And Formalization | +0.9% | National regulatory influence, strongest compliance in organized hubs | Medium term (2-4 years) |

| Coastal Humidity/Monsoon Durability Needs Expanding Outdoor/Polymer Wicker Adoption | +0.5% | Coastal South & East India (Kerala, Tamil Nadu, West Bengal, Odisha) | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Compact Urban Homes Driving Modular, Space-Saving Purchases

Space constraints in major metros are pushing households to prioritize modular solutions such as hydraulic-lift beds, sliding wardrobes, fold-out desks, and nested tables that deliver storage and flexibility without adding bulk. Organized brands are responding with configurable ranges that standardize dimensions and load-bearing capacities to ensure predictable fit and safe installation across compact apartments. Capital-backed specialists are scaling capacity to meet demand as Spacewood secured Rs 300 crore (USD 33.0 million) to expand modular kitchens, wardrobes, and multi-functional systems across more cities[2]Business News This Week, “Spacewood Raises INR300 Crore from A91 Partners to Accelerate Growth,” Business News This Week, businessnewsthisweek.com. Materials innovation is also shaping purchase criteria as brands incorporate bamboo veneers and recyclable inputs to pair sustainability with compact form factors that fit smaller rooms. The national rollout of the Furniture Quality Control Order in February 2026 standardized safety and performance baselines for modular categories, which will support organized adoption and strengthen consumer trust in certified products.

Omnichannel Expansion (Experience Centers + E-Commerce) Lifting Organized Penetration

Omnichannel models reduce friction by pairing online discovery with tactile validation at studios and experience centers where shoppers test finishes, ergonomics, and configurations before ordering. IKEA reported online sales contribute above 30% of India's revenue and is targeting a higher mix while opening more small and medium format locations to improve access and delivery speed across cities. Pepperfry’s network of 200+ studios across 100+ cities further illustrates how offline touchpoints build trust and lower return rates for bulky ticket sizes that buyers want to test in person[3]Pepperfry Corporate, “About Pepperfry,” Pepperfry, pepperfry.ltd. HTL International’s 17,000 sq ft flagship in Bengaluru demonstrates the role of co-creation, offering multiple leather and fabric choices with modular configurability to let customers personalize living and bedroom systems before purchase. Visualization is also improving conversion as AR-enabled tools reduce return rates and post-purchase friction for complex items that are hard to assess online, which supports the growth trajectory of the Indian home furniture market. Godrej Interio’s 3D kitchen configurator connects design to delivery by letting customers create room-accurate modular plans and then hand off to a dealer network for installation within defined time windows, which aligns product choice with execution certainty.

Government-Backed Housing Completions Sustaining New-Home Furnishing Cycles

PMAY-Urban delivered 96.02 lakh homes to beneficiaries by November 2025, with 122.06 lakh sanctioned across both phases, which continues to create first-time furnishing demand and a replacement cycle for essential bedroom, dining, and storage categories as beneficiaries take possession. The Union Cabinet’s approval of additional support for both PMAY-Urban and PMAY-Gramin provides a multi-year demand outlook that favors the economy and mid-range price tiers for basic furnishing kits suited to nuclear family lifestyles. As women constitute a high share of PMAY-Gramin beneficiaries, purchase decisions now tend to emphasize compact storage, modular kitchens, and multi-purpose living furniture that deliver practical utility in smaller spaces[4]Editorial Bureau, “Budget 2026–27: PM Awas Yojana in focus,” The Times of India, timesofindia.indiatimes.com. A larger mortgage base and deeper bank penetration are supporting incremental upgrades beyond bare essentials, which helps organized brands extend warranties and service coverages into new cohorts. Tier-II cities such as Surat, Indore, Lucknow, and Jaipur are absorbing this momentum, lifting sales contribution shares for organized retailers as local housing formation accelerates.

Premiumization Within Mid-Range Through Financing (EMI/BNPL) Improving Ticket Sizes

Financing options like no-cost EMI and BNPL are unlocking access to higher-spec configurations by spreading payments for items such as modular kitchens and plush sectional sofas over longer tenures, which is lifting the average spend per order across organized channels. The strategy is most visible in major metros where nuclear families prioritize coordinated sets and comfort features, and where branded warranties and service plans are valued alongside design. In kitchens, Godrej Interio’s mid-premium Steel Chef and other modular ranges start at around INR 1.25 lakh (USD 1,374) and demonstrate how guided design and financing can shift buyers into better finishes and hardware within the same budget envelope. Investor activity reinforces the trajectory at the top end as Stanley Lifestyles expanded its store base with proceeds from its public offering and continues to grow in metropolitan clusters where the appetite for curated finishes and artisanal craftsmanship is strongest. The combined effect is a rising share of mid-range purchases with premium cues that bridge affordability with style and durability inside the Indian home furniture market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Dominance of the Unorganized Sector Is Suppressing Standardization And Pricing Power | -1.9% | National, concentrated in rural UP, Bihar, Rajasthan clusters | Long term (≥ 4 years) |

| High Reverse-Logistics and Last-Mile Costs for Bulky Items | -0.8% | Tier-II & Tier-III cities, with acute pain in Eastern/North-Eastern corridors | Short term (≤ 2 years) |

| Imported Timber and Board Inputs Expose Margins to FX And Compliance Timelines | -0.7% | National, acute for Kerala/North India timber importers | Medium term (2-4 years) |

| New BIS Compliance Costs/Time for Mses During The 2026 Transition | -0.4% | National regulatory burden is heaviest in manufacturing hubs (Nagpur, Saharanpur) | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Dominance of the Unorganized Sector Suppresses Standardization and Pricing Power

The unorganized channel remains the primary volume outlet in many districts, which fragments pricing and quality outcomes, and holds back warranty adoption for mass-market purchases that are still made through local workshops. Organized leaders must therefore balance price competitiveness against costs tied to certification, formal logistics, and service infrastructure, which supports value but narrows headroom to discount heavily in price-sensitive clusters. While formal taxes and electronic invoicing have nudged micro workshops toward compliance or partnerships, progress is uneven in rural belts and parts of tier-III towns. Cultural preference for bespoke carpentry also persists in joint-family households, where custom dimensions are prioritized over standardized SKUs. As a result, brand-led standardization moves forward in metros and tier-II corridors but faces slower adoption in legacy carpentry hubs, which tempers price discipline in category segments where like-for-like comparisons are difficult. The combined effect reduces near-term pricing power for organized sellers in parts of the India home furniture market while formalization gradually expands addressable pools over time.

High Reverse-Logistics and Last-Mile Costs for Bulky Items

Bulky parcels impose heavy handling loads and wider delivery windows, which drive up reverse-logistics costs when returns occur from dispersed markets with variable road infrastructure. Company experience suggests that managing returns for sofas, beds, and wardrobes from tier-II and tier-III locations can take a sizable share of total operating expenses, particularly when multi-person assembly, damage claims, and reshipments are involved. Studio-led trial and in-person fabric or finish validation can lower return rates but add fixed costs in rent and staffing, so retailers must calibrate footprints and assortment complexity to their delivery network. Reported revenue swings at some omni-native players show that logistics overheads and network density still shape unit economics even as losses narrow through operational discipline. Distributed warehousing and better routing software mitigate a portion of these frictions, although volatile fuel prices and longer last-mile legs in certain corridors still compress margins. These realities continue to influence category mix and packaging choices across the Indian home furniture market as sellers balance speed, damage control, and return elasticity.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Home Office Surges Amid Hybrid-Work Permanence

Living room & dining room furniture commands 36.72% of India's home furniture market share in 2025, while home office furniture is the fastest-growing product group at an 11.60% CAGR through 2031. The shift reflects open-plan layouts in newly delivered housing and the desire for coordinated sets that align with apartment aesthetics in metros and growing tier-II cities. Shorter replacement cycles for sofas and seating, driven by design refreshes and lifestyle upgrades, are reinforcing repeat purchases across upholstery and occasional tables. India's home furniture market demand also benefits from modular formats that fit compact rooms with integrated storage, especially in bedrooms where hydraulic beds and sliding wardrobes reclaim floor space. Kitchen systems continue to migrate toward modular designs that compress installation times and standardize hardware for better durability under daily use.

India's home furniture market size for home office furniture is projected to expand at an 11.60% CAGR between 2026 and 2031 as hybrid work persists in knowledge centers and expands to second-tier cities. Ergonomic seating, height-adjustable desks, and storage add-ons are moving from discretionary to planned purchases as households invest in long-term setups that align with employer flexibility norms. Specialty retailers and omni-native players have broadened home office assortments with mid-range SKUs, while enterprise-focused brands introduce consumer-friendly variants with quicker delivery. As buyers test comfort and adjustability in showrooms and then compare finishes and specs online, conversion improves through transparent pricing and faster assembly services. This balanced path across experience centers and digital journeys supports durable momentum for the segment in the India home furniture market.

By Material: Engineered Boards Challenge Wood’s Cultural Primacy

Wood retained a 61.95% share in 2025 on the back of durable species and long-held preferences for natural finishes that signal longevity in dining and bedroom sets. That said, supply dynamics and compliance timelines are steering a gradual shift toward engineered substrates that meet standardized load-bearing thresholds and speed mass manufacturing. India home furniture market size for metal furniture is projected to expand at a 13.73% CAGR through 2031 as powder-coated aluminum and stainless steel win in humid and coastal zones and as clean-lined forms fit compact floor plans. Polymer wicker and weatherable plastics are also gaining share outdoors, where UV resistance and easy cleaning are priorities for balconies and garden settings.

Within the India home furniture industry, engineered boards increase design flexibility, reduce waste, and align with quality and safety benchmarks tightened under QCO schedules, which collectively shorten installation lead times and raise uniformity. A wider acceptance of MDF and particleboard in wardrobes, TV units, and storage modules helps brands scale SKUs with predictable performance while still offering finish variety. Outdoor sets in polymer wicker and rope constructions address mildew and corrosion challenges, especially in coastal belts, where materials must withstand salt spray and high humidity. Brands that marry compact design with durable materials benefit from repeat referrals in urban apartments where buyers value space optimization. These shifts are gradually diversifying the materials mix across the India home furniture market as consumers weigh aesthetics, durability, maintenance, and price.

By Price Range: EMI Schemes Propel Premium Growth Above Mid-Range Baseline

The mid-range tier held a 48.25% share in 2025 as households balanced branded warranties, finish variety, and delivery-installation services within defined budgets. Entry-level SKUs remain relevant in rural and tier-III areas for first-time PMAY beneficiaries who prioritize essential beds, dining sets, and storage units. At the same time, Premium is the fastest-growing bracket with an 11.34% CAGR through 2031, aided by EMI plans that stretch payments for modular kitchens and curated living-room sets. India home furniture market participants that combine transparent pricing, guided design journeys, and quick installation are pulling buyers upward within the same order to higher-spec options. Premium specialists’ expansion in metros further validates the willingness of affluent cohorts to invest in craftsmanship, finishes, and long warranty cover.

EMI and BNPL models have increased average ticket sizes in core metros where households prefer coordinated room sets and multi-functional storage over piecemeal purchases. The India home furniture industry is also seeing “affordable luxury” cues permeate mid-range SKUs through sustainable materials, smart charging modules, and modularity that once sat above the price ladder. Where omnichannel footprints widen, buyers access premium-like experiences at mid-range prices, supported by visualization tools that reduce decision friction. Premium’s outperformance is likely to persist in clusters where format density, financing access, and faster fulfillment combine. These conditions shape a laddered value proposition that advances the overall mix within the India home furniture market.

By Distribution Channel: Specialty Stores Defend Share as Online Scales at 13.62% CAGR

Specialty furniture stores commanded a 74.85% share in 2025 as buyers sought tactile checks for upholstery comfort, finish quality, and hardware action before committing to big-ticket purchases. Store-led models are densifying in urban corridors where mixed-use developments anchor captive footfall and where service infrastructure supports quick assembly. Online channels are projected to grow at a 13.62% CAGR through 2031 as improved visualization, better delivery transparency, and clear return policies build buyer confidence across cities and tier-II townships. India's home furniture market size for Online channels is set to expand at this pace as large-format players and D2C brands invest in showrooms that work alongside e-commerce to validate purchases. AR-powered configurators at leading retailers reduce fitting anxiety and cut return risk, which protects unit economics and supports growth.

Alternative channels, including home centers and rentals, address niche needs for transient professionals and flexible living arrangements. As omnichannel density rises, shoppers research online, trial in person, and transact across whichever path offers the best mix of availability, installation speed, and value. The India home furniture industry increasingly treats online and offline as a single demand funnel with operations geared for cross-channel handoffs. In this model, visualization tools, store advisors, and reliable last-mile services drive conversion. The resulting balance of online scale and offline trust is now a key differentiator in the Indian home furniture market.

Geography Analysis

North India held 28.90% of India home furniture market share in 2025, led by Delhi-NCR’s dense housing formation and active trade clusters across Uttar Pradesh, Rajasthan, and Haryana. Growing student and professional migration into Noida, Gurugram, and Chandigarh supports compact formats for co-living and rental units where storage and modular designs are favored. Large-format retail and planned store openings by global brands signal strong, continued demand for coordinated living and bedroom sets that reflect contemporary metro preferences. Wholesale hubs and design centers in Delhi also serve as feeders for national distribution, extending North India’s influence into builder and interior channels. Organized brands leverage format density and logistics infrastructure to offer faster fulfillment and after-sales coverage across priority districts within the region.

South India remains a key engine for modular kitchen and contemporary living-room solutions centered in Bengaluru, Hyderabad, Chennai, and Kochi. Knowledge-industry hubs sustain demand for ergonomic home office setups, while an expanding premium segment favors curated leather and fabric assortments with customization. Experience centers that allow co-creation and material selection underline the region’s appetite for design-led purchases, which is deepened by strong mall infrastructure and urban expansion. Coastal belts in Kerala and Tamil Nadu prioritize materials that resist humidity and salt spray, which supports outdoor polymer wicker and powder-coated aluminum sets. Retailers that blend visualization with in-store trial continue to gain share as hybrid buying journeys mature in these cities.

East India is projected to grow the fastest at a 9.45% CAGR through 2031 as infrastructure upgrades and concentrated PMAY-Gramin disbursements in West Bengal and Odisha lift first-time furnishing cycles across Kolkata, Guwahati, Bhubaneswar, and Patna. Urban transport improvements and new housing launches are creating pockets of concentrated demand for modular kitchens, bedroom sets, and ergonomic seating. Local manufacturing investments, retail expansion, and events that connect buyers to suppliers are also improving ecosystem depth for materials and hardware. Formats with flexible price points and rapid installation appeal to households upgrading from unorganized alternatives, which brings more buyers into organized channels. As omnichannel penetration increases, the India home furniture market will see a rising share of East India in national sales, supported by logistics improvements that reduce last-mile friction.

Competitive Landscape

The competitive field is fragmented, with rapid gains by organized players as they expand omnichannel density, invest in design tooling, and prepare for QCO compliance that sets a higher quality baseline for certified assortments. IKEA plans to more than double its India investment to over Rs 20,000 crore (USD 2200 million) over five years to accelerate from 6 to 30 stores and to grow online’s contribution alongside physical formats. Godrej Interio targets Rs 10,000 crore revenue by FY29 through a 1,500-store omnichannel footprint and design-centered offerings that move buyers up the value curve with reliable service and installation. Digital-native challengers like Wakefit have broadened from sleep solutions into furniture and decor while scaling company-owned stores and online reach to capture younger cohorts that expect speed and transparency.

Strategic themes center on three moves. First is omnichannel integration, in which digital discovery pairs with studios and experience centers to boost conversion and reduce returns in the Indian home furniture market. Second is modular specialization supported by capital raises and factory upgrades to expand kitchens, wardrobes, and multi-functional systems at scale, as seen in Spacewood’s Rs 300 crore (USD 33.0 million) expansion plan. Third is regulatory readiness, as early BIS certification and process alignment give organized brands a head start before quality marks become mandatory across key furniture categories in February 2026. Together, these strategies compound advantages in assortment breadth, installation reliability, and long-term service, helping brands win share from unorganized workshops in fast-formalizing city clusters.

Regulatory changes and supply dynamics are also shaping product strategy and procurement. The QCO timeline will favor certified inputs and boards that meet Indian Standards, which narrows options for uncertified imports and accelerates the pivot to domestic or fully documented supply lines. At the same time, FX-linked input volatility for timber and engineered panels is driving SKU rationalization and mix shifts toward materials with more predictable pricing, including metal frames and polymer furniture in specific use cases. Brands that invest in AR-guided visualization, route optimization, and distributed warehousing are reducing delivery costs and return incidence, which helps unit economics as online mixes rise. These operational levers, combined with design-led differentiation and compliance readiness, underpin competitive momentum across the India home furniture market.

India Home Furniture Industry Leaders

Godrej Interio

IKEA India

Wakefit

Spacewood Furnishers

Royaloak

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: Godrej Interio announced a refreshed soft furnishings collection focused on craft, comfort, and responsible design, expanding its lifestyle portfolio beyond core furniture categories. Separately, the company disclosed its Godrej Design Lab Fellows for 2026, reinforcing its commitment to design-led innovation and talent development.

- January 2026: IKEA India inaugurated its first Delhi store at Pacific Mall, Tagore Garden, featuring 15000 sq ft and over 2000 home furnishing products, marking a strategic expansion into north India's capital market.

- November 2025: Spacewood Furnishers raised INR 300 crore from private equity firm A91 Partners at an INR 1200 crore valuation to accelerate expansion in modular kitchens, wardrobes, home and office furniture, and doors.

- September 2025: TCC Concept acquired Pepperfry for INR 1200 crore, expanding its presence in India's digital furniture market. Separately, AFC Furniture Solutions became the first Indian manufacturer to achieve BIFMA Level® 3 certification, establishing sustainability leadership and compliance with global eco-standards.

India Home Furniture Market Report Scope

The Indian home furniture market encompasses the manufacturing, distribution, and retail of residential and commercial furniture. It features diverse products catering to varied consumer preferences influenced by cultural, economic, and lifestyle factors.

The Indian home furniture market is segmented into product type, type of market, and distribution channel. By product type, the market is segmented into modular and semi-modular kitchen furniture with L shape modular kitchen, u shape modular kitchen, parallel shape modular kitchen, straight shape modular kitchen, and other modular kitchen furniture, bedroom furniture with beds, dresser/dressing tables, bedside tables, and other bedroom furniture with chest of drawers, floor mirror, etc., bathroom furniture with bathroom furniture, and other bathroom furniture, and wardrobes with single-door wardrobes, double-door wardrobes, three-door wardrobes, four-door wardrobes, other wardrobes (almirah, etc.), and other home furniture products with living room furniture, kids furniture, home office furniture, etc. By type of market, the market is segmented into organized and unorganized. By distribution channel, the market is segmented into home centers, specialty stores, online, and other distribution channels. The report offers market size and forecasts for the Indian home furniture market in terms of value in USD for all the above segments.

By Product

| Living Room & Dining Room Furniture |

| Bedroom Furniture |

| Kitchen Furniture |

| Home Office Furniture |

| Bathroom Furniture |

| Outdoor Furniture |

| Other Furniture |

By Material

| Wood |

| Metal |

| Plastic & Polymer |

| Others |

By Price Range

| Economy |

| Mid-Range |

| Premium |

By Distribution Channel

| Home Centers |

| Specialty Furniture Stores |

| Online |

| Other Distribution Channels |

By Geography

| North |

| South |

| East |

| West |

| By Product | Living Room & Dining Room Furniture |

| Bedroom Furniture | |

| Kitchen Furniture | |

| Home Office Furniture | |

| Bathroom Furniture | |

| Outdoor Furniture | |

| Other Furniture | |

| By Material | Wood |

| Metal | |

| Plastic & Polymer | |

| Others | |

| By Price Range | Economy |

| Mid-Range | |

| Premium | |

| By Distribution Channel | Home Centers |

| Specialty Furniture Stores | |

| Online | |

| Other Distribution Channels | |

| By Geography | North |

| South | |

| East | |

| West |

Key Questions Answered in the Report

What is the current size and outlook for the India home furniture market?

The India home furniture market size is expected to increase from USD 25.20 billion in 2025 to USD 27.27 billion in 2026 and reach USD 40.53 billion by 2031, at an 8.24% CAGR over 2026-2031.

Which product categories lead and which are growing the fastest in India?

Living room & dining room furniture led with 36.72% in 2025, while home office furniture has the fastest growth outlook at an 11.60% CAGR through 2031.

How will regulations affect competition in India’s home furniture space?

The BIS furniture quality control order, effective February 13, 2026, mandates certification for key furniture categories, which raises standards and favors organized brands ready with certified inputs and processes.

Which regions show the strongest demand and fastest growth?

North India holds 28.90%, led by Delhi-NCR, with strong modular demand, and East India is projected to grow the fastest at a 9.45% CAGR through 2031.

How are omnichannel strategies changing buying behavior in India?

Online discovery paired with studios and experience centers reduces returns and speeds decisions, with IKEA reporting online shares above 30% of India revenue while it expands small and medium format stores.

What cost and supply chain issues matter most for sellers in India?

Reverse logistics for bulky parcels and FX-linked input volatility on timber and engineered boards pressure margins, so brands deploy distributed warehousing, routing software, and material mix shifts for stability.

Page last updated on: