Two-Wheeler/Motorcycles Insurance Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 134.31 Billion |

| Market Size (2031) | USD 180.55 Billion |

| Growth Rate (2026 - 2031) | 6.09% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

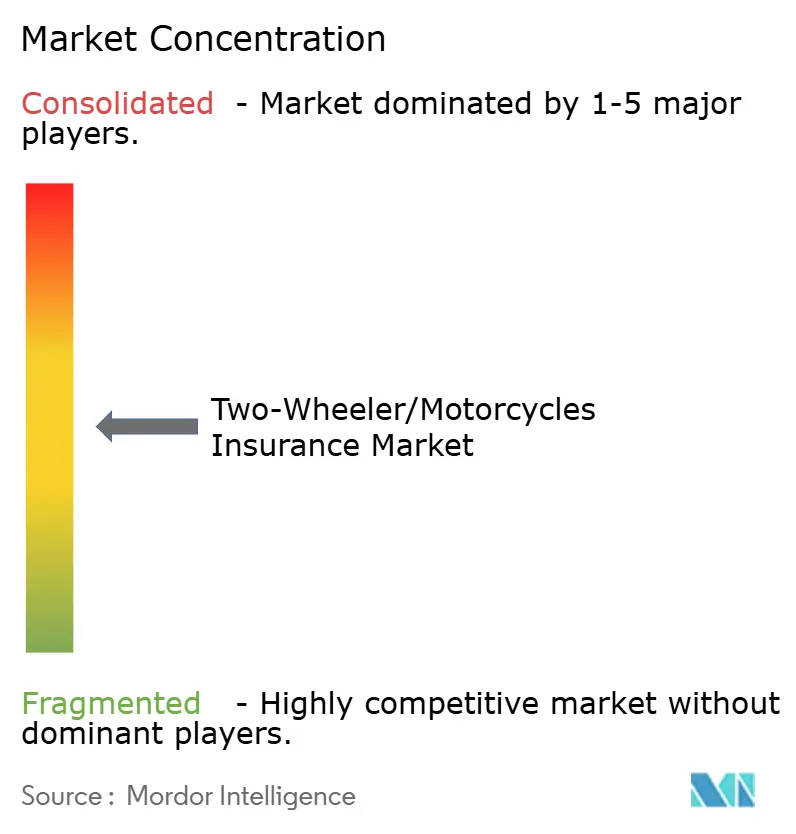

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Two-Wheeler/Motorcycles Insurance Market Analysis by Mordor Intelligence

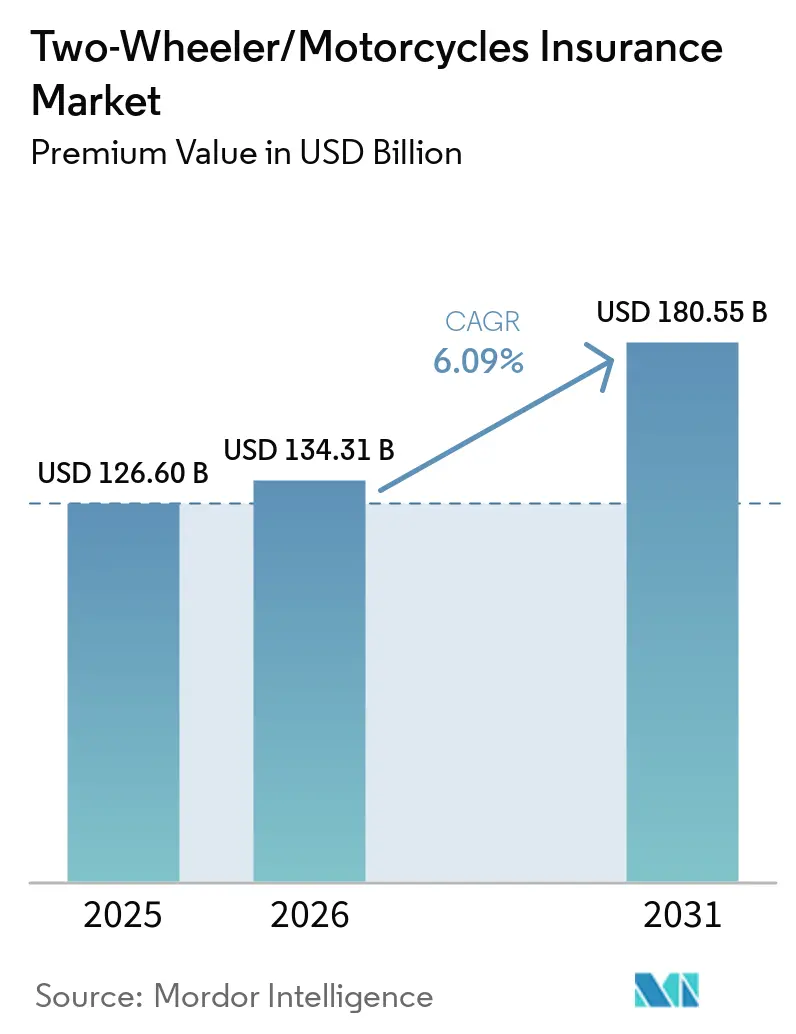

The Two-Wheeler/Motorcycles Insurance Market size in terms of premium value is expected to increase from USD 126.60 billion in 2025 to USD 134.31 billion in 2026 and reach USD 180.55 billion by 2031, growing at a CAGR of 6.09% over 2026-2031.

Surge in compulsory third-party coverage across emerging economies, steady premium rate filings in high-income jurisdictions, and growing digital distribution are propelling premium volumes. Regulatory moves such as Indonesia’s nationwide mandate for liability insurance and India’s 15-20% tariff increase on motorcycle third-party cover reinforce non-discretionary demand. Rising repair-part inflation and medical cost escalation further lift average premiums, while embedded insurance at the point of sale accelerates policy uptake, especially among first-time riders. Climate-related loss volatility has tightened underwriting discipline, prompting wider use of reinsurance and predictive analytics to safeguard margins.

Key Report Takeaways

- By geography, Asia-Pacific led with 38.12% of the two-wheeler/motorcycle insurance market share in 2025, while the region is projected to expand at a 5.34% CAGR through 2031.

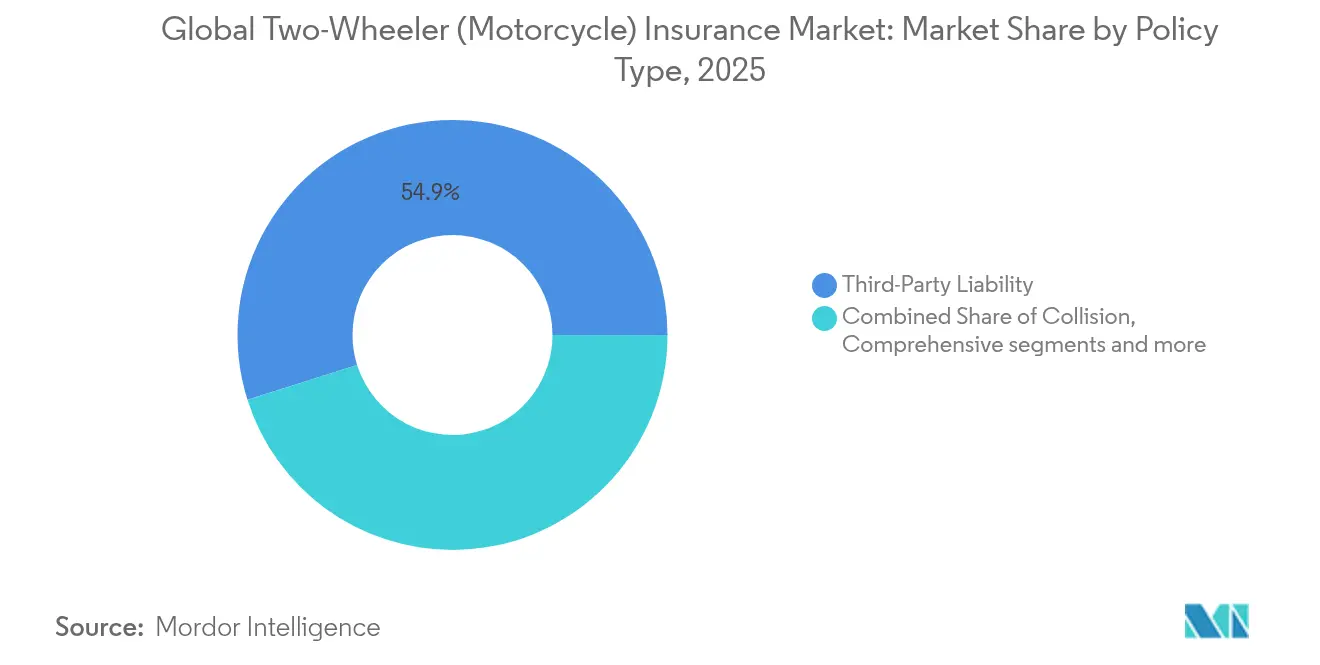

- By policy type, third-party liability captured 54.86% revenue share in 2025; comprehensive cover is advancing at a 6.15% CAGR to 2031.

- By distribution channel, direct-to-consumer held 35.37% of the two-wheeler/motorcycle insurance market size in 2025 and is growing fastest at 6.73% CAGR.

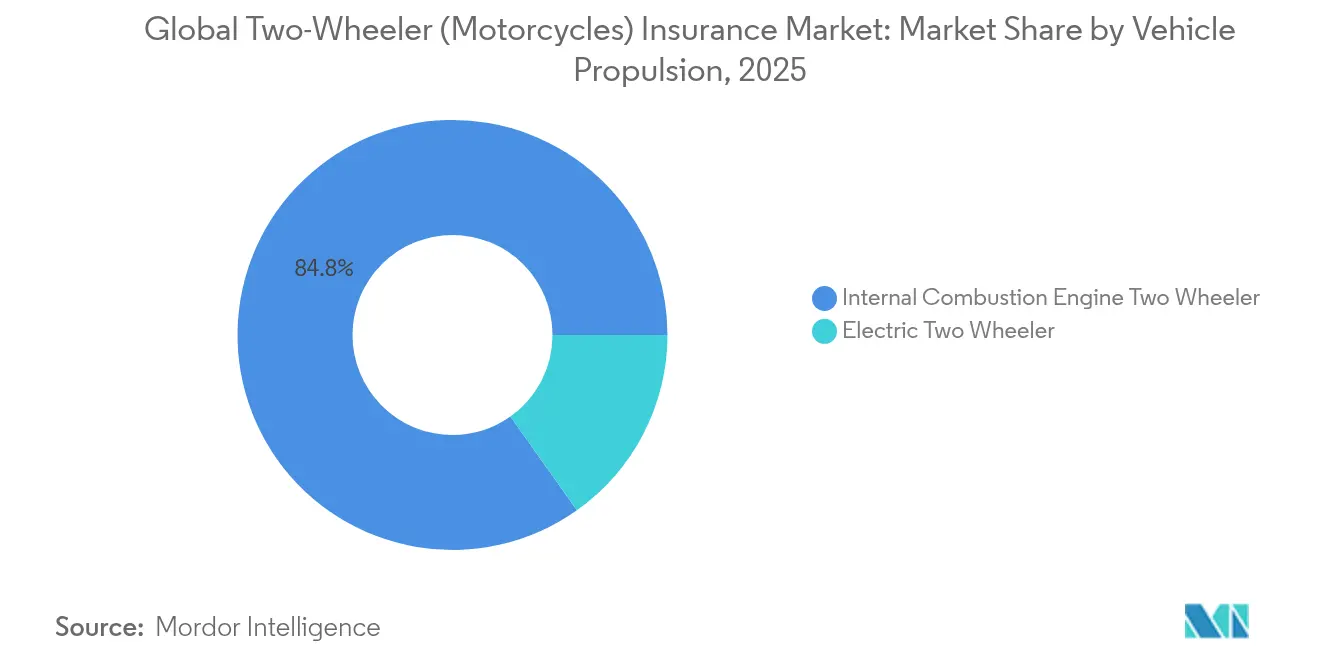

- By vehicle propulsion, electric two-wheelers represented 15.18% of premiums in 2025 and recorded the highest 8.09% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Two-Wheeler/Motorcycles Insurance Market Trends and Insights

Drivers Impact Analysis*

| Driver | ( ~ )% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Mandatory insurance requirements & rising two-wheeler parc | +1.8% | Global; strongest in Indonesia, India, Thailand | Medium term (2–4 years) |

| Escalating repair/medical costs | +1.2% | North America, EU; spill-over to APAC cities | Short term (≤ 2 years) |

| Rapid motorcycle sales growth in Asia-Pacific & South America | +1.5% | APAC core, LATAM emerging | Long term (≥ 4 years) |

| Usage-based/telematics premium models | +0.9% | North America, EU, select APAC | Medium term (2–4 years) |

| Mobile-first micro-duration policies & InsurTech platforms | +0.6% | Global tech-centric cities | Short term (≤ 2 years) |

| Embedded cover bundled with OEM/fintech checkout | +0.7% | Global; led by North America, China | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Mandatory insurance requirements & rising two-wheeler parc

Indonesia’s Financial Services Authority (OJK) has made third-party liability compulsory for all motor vehicles from January 2025, instantly expanding the addressable base for carriers[1]Financial Services Authority, “Regulation on Compulsory Motor Vehicle Liability Insurance,” ojk.go.id. Similar frameworks in Thailand and India consolidate a predictable premium pool, enabling insurers to allocate capital to product innovation and digital outreach. Motorbike density in congested megacities continues to climb, reinforcing steady policy growth as commuters seek agile mobility and regulators pursue safer roads. In India, opening the insurance sector to 100% foreign direct investment attracts global expertise and capital[2]Bajaj Finserv, “Revised Motor Third-Party Premiums Effective 2025,” bajajfinserv.in. Collectively, these levers underpin a stable growth runway for the two-wheeler/motorcycle insurance market.

Escalating repair/medical costs

Modern two-wheelers increasingly feature sensors, connectivity modules, and advanced safety electronics. Component complexity drives parts inflation well above headline CPI, while technician shortages lengthen repair cycles. LexisNexis reported 35% and 40% jumps in bodily injury and collision severity, respectively, trends that filter directly into motorcycle claims. Concurrently, medical cost inflation amplifies loss ratios, giving carriers a strong rationale to refine underwriting granularity and push telematics-based incentives for safer riding. These pressures also encourage closer collaboration between insurers and OEMs to monitor vehicle health and rider behavior in real time. As claims costs mount, actuarial models are being recalibrated to better reflect the risk dynamics of digitally enhanced motorcycles.

Rapid motorcycle sales growth in Asia-Pacific and South America

Urban households across Southeast Asia and South America continue to adopt motorcycles for cost-effective last-mile mobility. App-based ride-hailing platforms formalize informal “mototaxi” segments and require embedded coverage at dispatch, channeling previously uninsured riders into the formal risk pool. Government purchase incentives and expanding charging networks spur electric motorbike uptake, further enlarging policy demand in the two-wheeler/motorcycle insurance market. This transition is particularly pronounced in dense urban corridors, where two-wheelers offer a practical alternative to congested public transport. As fleets electrify, insurers are adapting products to cover battery degradation, charging infrastructure liability, and new maintenance risk profiles. Additionally, digital distribution and micro-premium models are being scaled to align with the affordability needs of gig workers and low-income riders.

Usage-based/telematics premium models

InsurTech innovators convert aggregated ride data into dynamic pricing. VOOM’s per-mile product, backed by a USD 15 million funding round, allows infrequent riders to cut premiums by up to 60% while preserving coverage[3]VOOM Insurance, “Series A Funding Announcement,” voominsurance.com. Cambridge Mobile Telematics reports a 20% drop in distracted riding and a 27% fall in speeding among highly engaged users, demonstrating tangible risk mitigation. Behavioral benefits loop back into reduced claims, supporting profitable growth. These models reward safer riding habits in real time, strengthening the feedback loop between user behavior and financial incentives. As adoption spreads, insurers gain access to granular risk profiles that enhance underwriting precision across diverse geographies. This data-centric approach is especially impactful in emerging markets, where traditional credit or claims histories are often lacking. Moreover, embedded sensors and smartphone integrations reduce barriers to telematics adoption, enabling wider rollout at scale.

Restraints Impact Analysis*

| Restraint | ( ~ )% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Complex multi-jurisdiction regulation & solvency rules | -0.8% | Global cross-border operations | Long term (≥ 4 years) |

| Premium affordability for high-performance & EV bikes | -1.1% | Emerging markets | Medium term (2–4 years) |

| Sparse driving-behaviour data hindering risk pricing | -0.6% | Developing markets | Short term (≤ 2 years) |

| Rising climate-related catastrophe losses | -1.3% | Coastal and wildfire regions | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Complex multi-jurisdiction regulation & solvency rules

Capital models vary widely across continents, compelling global insurers to maintain parallel compliance regimes. The NAIC’s 2025 risk-based capital framework revision in the United States adds extra reporting layers. Concurrently, Europe’s Solvency II update forces asset-liability adjustments, while the UAE shifts oversight to its central bank. Smaller players face the stiffest overhead, limiting their expansion bandwidth. These divergent regulatory landscapes increase administrative costs and complicate cross-border capital allocation. Larger insurers may absorb these costs through scale, but mid-sized players often struggle to justify new market entries. Additionally, misaligned solvency ratios across jurisdictions can distort reinsurance structures and delay group-level risk transfer. Regulatory harmonization remains limited, prompting insurers to rely heavily on localized compliance teams and specialized legal counsel.

Rising climate-related catastrophe losses

Extreme weather events damage motorcycles at scale and heighten rider accident risk. Global reinsurers note an upward trend in both severity and frequency of climate-driven events, prompting higher catastrophe loads and reinsurance spend. Carriers respond with stricter geographic underwriting guidelines, but elevated costs suppress policy affordability in exposed regions. This dynamic is particularly acute in flood-prone Southeast Asia and wildfire-affected parts of Southern Europe and California. Loss predictability remains low due to shifting climate baselines, challenging traditional actuarial models. As a result, some insurers are withdrawing from high-risk zones altogether or imposing sub-limits on natural catastrophe claims. These trends also accelerate interest in parametric insurance models, offering quicker payouts tied to measurable weather triggers. However, product awareness and regulatory alignment for such innovations remain limited in many developing markets.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Policy Type: Comprehensive coverage gains momentum

Third-party liability remained the backbone of the two-wheeler/motorcycle insurance market in 2025, owning 54.86% revenue share as statutory mandates fuel compulsory take-up. Comprehensive policies, however, are forecast to log a 6.15% CAGR, the quickest among all policy classes, as rising household income and higher-value electric bikes encourage riders to protect their assets fully. The two-wheeler/motorcycle insurance market size for comprehensive coverage is projected to widen significantly between 2026 and 2031, benefiting carriers with diversified product suites. Collision and specialty add-ons, such as gap or battery warranty coverage, cater to niche needs, especially in urban centers where parking accidents and theft remain prevalent.

Growing comprehensive adoption also mirrors technological progress in claims handling. Allianz has embedded generative AI across nearly 400 use cases to shorten settlement cycles, making broad coverage more palatable to cost-conscious riders. Electric bike owners are particularly receptive, as battery packs can represent more than half of vehicle value; a standalone battery replacement endorsement is therefore fast becoming a standard feature in comprehensive bundles.

By Distribution Channel: Digital transformation accelerates

Direct-to-consumer accounted for 35.37% of 2025 premiums and is projected to expand at a 6.73% CAGR, reflecting the structural pivot to online self-service and app-led policy management. The two-wheeler/motorcycle insurance market size captured by embedded flows is rising in tandem, underpinned by OEM webstores, neo-banks and ride-sharing apps integrating instant cover. Intermediated models retain a meaningful presence for complex risk consultations, but their growth pace trails fully digital competitors. As younger, tech-savvy riders dominate new policy origination, demand for 24/7 self-service features, real-time quotes, and in-app claims tracking is accelerating. Digital-first insurers are also leveraging behavioral data from embedded platforms to personalize pricing, further widening the gap from traditional agents.

The two-wheeler/motorcycle insurance market benefits from hybrid experiments, such as Bajaj Allianz’s bancassurance rollout through Axis Bank’s branches, which blends in-person advice with a digital backbone. For players, online origination slashes distribution expense ratios, enabling sharper price points that resonate with price-sensitive riders. This structural gain is expected to sustain margin expansion even as loss of costs rise. Additionally, hybrid models serve as a transition bridge for underbanked and digitally hesitant customers, expanding reach without sacrificing efficiency. As trust in digital channels improves, many of these hybrid-acquired customers eventually migrate toward fully digital servicing, supporting long-term retention.

By Vehicle Propulsion: Electric transition creates premium challenges

Internal combustion engine models still held 84.82% of 2025 premium volume, but battery-powered two-wheelers led growth with an 8.09% CAGR. High battery replacement expense and limited repair networks inflate electric motorbike premiums around 20% above conventional rates, yet government incentives and zero-emission zones underpin robust sales trajectories. The two-wheeler/motorcycle insurance market share for electric bikes is therefore set to climb steadily through 2031. As urban congestion charges and carbon taxes expand, more commuters are shifting toward e-mobility solutions despite higher initial insurance costs. Insurers are beginning to pilot tailored products for EV two-wheelers, incorporating coverage for charging infrastructure and software vulnerabilities.

Munich Re’s “Cyber for Auto” cover, launched in 2024, addresses new digital risks tied to connected powertrains and over-the-air updates. As carriers refine experience curves on battery degradation and parts sourcing, underwriters expect gradual premium normalization, which could unlock even faster adoption in price-sensitive economies. This normalization will also benefit shared mobility operators, where fleet electrification is a strategic priority. With growing exposure to digital threats, reinsurers are actively exploring bundled cyber and property-risk products specifically designed for connected electric motorcycles.

Geography Analysis

Asia Pacific delivered 38.12% of global premiums in 2025 and is tracking a 5.34% CAGR to 2031 as regulators standardize compulsory insurance and urban commuters favor two-wheelers for cost-efficient mobility. India’s 100% foreign direct investment allowance already spurred Zurich’s USD 670 million purchase of a majority stake in Kotak General Insurance, highlighting capital inflow momentum. Indonesia’s mandate is expected to formalize millions of riders, broadening the two-wheeler/motorcycle insurance market base across ASEAN.

North America is mature but remains technology-driven. Carriers dominate UBI penetration; LexisNexis estimates that over 68% of U.S. insurers see telematics as a decisive competitive lever. Progressive’s data-centric model helped lift its motor share to 16.73% in 2024, showing that even saturated markets permit share shifts through analytics excellence. However, wildfire-related losses in the West and hurricane clusters in the Gulf continue to inject volatility into combined ratios.

Europe’s market benefits from capital efficiency under Solvency II. Allianz reported EUR 44.8 billion in property-and-casualty volume for H1 2024, up 7.3%, confirming disciplined rate adequacy. Electric mobility regulations in Germany, France and the Nordics foster electric bike penetration, broadening policy demand. Conversely, Brexit-related licensing adjustments moderately raise frictional costs for U.K. domiciled underwriters active in continental territories.

South America and the Middle East & Africa remain under-penetrated but attractive. Telecom-linked micro-insurance pilots in Brazil and Nigeria demonstrate how mobile wallets can distribute low-ticket premium products, bringing first-time policyholders into the two wheeler/motorcycle insurance market. Regulatory modernization, including solvency reforms in the Gulf, is expected to unlock cross-border capacity and facilitate product transfers from mature markets.

Competitive Landscape

The two-wheeler/motorcycle insurance market is moderately concentrated; NAIC data show the top five property-and-casualty carriers controlled just above half of 2024 premiums. Scale brings data breadth and reinsurance leverage, yet niche underwriters harness InsurTech alliances to punch above their weight. Progressive lifted direct written premium by 24.5% in 2024, powered by sophisticated telematics scoring and frictionless digital servicing. Meanwhile, regional players are carving out defensible positions by specializing in underserved geographies and tailoring products to local rider behaviors. These dynamics create a competitive landscape where both scale and specialization can deliver strong underwriting performance.

Strategic M&A accelerates capability consolidation. Sentry Insurance’s USD 1.7 billion acquisition of The General broadens access to non-standard riders, while Gallagher’s pending purchase of AssuredPartners enhances middle-market distribution firepower. Technology remains the primary differentiator: carriers deploy AI for fraud detection, claims triage, and personalized marketing, shrinking expense ratios and elevating customer satisfaction. Many acquirers are also targeting tech-native MGAs and digital brokerages to accelerate digital transformation from within. As legacy players modernize through acquisition, integration speed and cultural alignment become critical to realizing synergies.

Emerging white space lies in embedded insurance, pay-as-you-ride models and dedicated electric bike products. VOOM’s per-mile proposition and OEM partnerships illustrate how agile startups can capture younger, tech-savvy customers before incumbents adapt. Large carriers are therefore investing in corporate venture arms and accelerator programs to stay ahead of the innovation curve. These partnerships not only offer early access to disruptive models but also help incumbents test new distribution and pricing strategies with lower operational risk. Over time, successful pilots may scale into core offerings, reshaping how motorcycle insurance is marketed and consumed.

Two-Wheeler/Motorcycles Insurance Industry Leaders

GEICO

Progressive

State Farm

Bajaj Allianz

AXA

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: VOOM raised USD 15 million in Series funding to scale its per-mile motorcycle insurance product across additional United States' states.

- January 2025: Sentry Insurance completed its USD 1.7 billion takeover of The General, significantly strengthening its presence in the non-standard motor insurance market. This acquisition expands Sentry’s portfolio by targeting higher-risk drivers, offering tailored products that address underserved segments with growth potential.

- December 2024: Gallagher entered an agreement to acquire AssuredPartners for USD 13.45 billion, significantly increasing its brokerage scale and market reach. This strategic move enhances Gallagher’s ability to offer a broader range of services and strengthens its position in the competitive insurance distribution landscape.

- June 2024: Zurich finalized the USD 670 million purchase of 70% of Kotak Mahindra General Insurance, marking the largest foreign investment in India’s general insurance market.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Mordor Intelligence defines the global two-wheeler insurance market as the gross written premiums generated by policies that protect street-legal motorcycles, scooters, mopeds, and electric two-wheelers against third-party liabilities, own-damage, theft, and accident-linked medical costs in every major geography.

Scope exclusion: off-road recreational vehicles, e-bikes below 250 W, and extended service contracts are not counted.

Segmentation Overview

- By Policy Type

- Third-Party Liability

- Collision

- Comprehensive

- Others

- By Distribution Channel

- Direct-to-Consumer (DTC)

- Intermediated (includes agents, brokers, bancassurance, and other traditional third-party channels)

- Embedded (insurance sold as an add-on within another purchase journey)

- By Vehicle Propulsion

- Internal-Combustion Two-Wheelers

- Electric Two-Wheelers

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Peru

- Chile

- Argentina

- Rest of South America

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- BENELUX (Belgium, Netherlands, and Luxembourg)

- Nordics (Sweden, Norway, Denmark, Finland)

- Rest of Europe

- Asia-Pacific

- China

- India

- Japan

- South Korea

- Australia

- South East Asia

- Indonesia

- Rest of Asia-Pacific

- Middle East & Africa

- United Arab Emirates

- Saudi Arabia

- South Africa

- Rest of Middle East & Africa

- North America

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interviewed underwriting managers, multi-brand brokers, digital aggregators, and road-safety officials across Asia-Pacific, Europe, the Americas, and MEA. Conversations clarified average premium shifts, emerging micro-duration products, electric-bike risk perceptions, and penetration ceilings, letting us refine assumptions that desk research could only hint at.

Desk Research

Our team began with credible public datasets such as OICA production volumes, World Bank vehicle-in-use series, insurance regulator filings from NAIC, IRDAI, and EIOPA, and accident statistics published by the WHO. Trade associations like ACEM and the Global Federation of Insurance Associations supplied policy mix ratios, while company 10-Ks, investor decks, and press releases offered premium disclosures and channel splits. To firm up financial benchmarks, we turned to paid platforms, D&B Hoovers for insurer revenue splits and Marklines for regional two-wheeler output trends. These and many other sources created the baseline against which primary insights were tested.

Market-Sizing & Forecasting

A top-down model converts country two-wheeler parc and new-registration flows into an insurable risk pool, applies region-specific compulsory-insurance penetration and average premium figures, and then rolls results up to the global level. Supplier roll-ups and sampled ASP × volume checks provide bottom-up guardrails before totals are locked. Key variables include active vehicle stock, new sales, average annual premium, mandated liability limits, electric share, claim frequency, and disposable income indices. Forecasts deploy multivariate regression blended with scenario analysis to reflect regulatory tightening, electrification, and digital-distribution uptake, all stress-tested with the expert panel. Data gaps, especially in emerging markets, are patched through proxy indicators such as import duty collections and smartphone-based policy issuance volumes.

Data Validation & Update Cycle

Outputs face automated variance scans against historical loss ratios, followed by senior analyst review. Anomalies trigger re-contact of sources. Reports refresh every twelve months, with interim revisions if legislation, currency swings, or mega-mergers materially shift premiums.

Why Mordor's Motorcycle Insurance Baseline Commands Reliability

Published figures often differ because publishers pick dissimilar vehicle classes, currency years, and refresh cadences.

Our disciplined scope setting, fresher 2025 base, and dual-route modeling narrow those gaps and give decision-makers a line of sight to every assumption.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 126.60 B (2025) | Mordor Intelligence | - |

| USD 115.51 B (2023) | Global Consultancy A | Older base year and limited Asia coverage omit embedded micro-policies |

| USD 91.60 B (2020) | Trade Journal B | Outdated data year and no inflation or electric-bike premiums included |

| USD 68.90 B (2023) | Data Publisher C | Narrow scope focused on developed-market premiums only |

The comparison shows how differing scopes and stale datasets can skew values. By anchoring estimates to the latest vehicle counts, regulatory mandates, and verified premium trends, Mordor Intelligence delivers a balanced, transparent baseline clients can readily audit and replicate.

Key Questions Answered in the Report

How big is the two wheeler/motorcycle insurance market today?

The market generated USD 134.31 billion in 2026 and is projected to reach USD 180.55 billion by 2031.

Which region leads premium generation?

Asia Pacific held 38.12% of global premiums in 2025, supported by compulsory insurance laws and expanding urban motorcycle fleets.

What policy type is growing the fastest?

Comprehensive cover records a 6.15% CAGR through 2031 as riders seek broader protection for higher-value and electric bikes.

How are insurers using telematics?

Players leverage ride-data to price per-mile policies, reward safe behavior and cut claims severity, especially in mature North American and European markets.

Why are electric motorcycle premiums higher?

Battery replacement costs, limited repair expertise and emerging cyber risks lift average premiums about 20% above conventional models.

Page last updated on: