Market Trends of GCC Dangerous Goods Logistics Industry

Recovery of Chemical Industry

The chemicals and petrochemicals industry in the GCC is poised for growth, as the regional and global economy is forecast to recover in the aftermath of the COVID-19 outbreak.

According to the Gulf Petrochemicals and Chemicals Association (GPCA), the region's chemicals industry is anticipated to see growth across all key indicators including chemical sales revenue, production output, and international trade on the back of an increase in regional economic activity, supported by a rapid vaccination rollout and the global economic rebound.

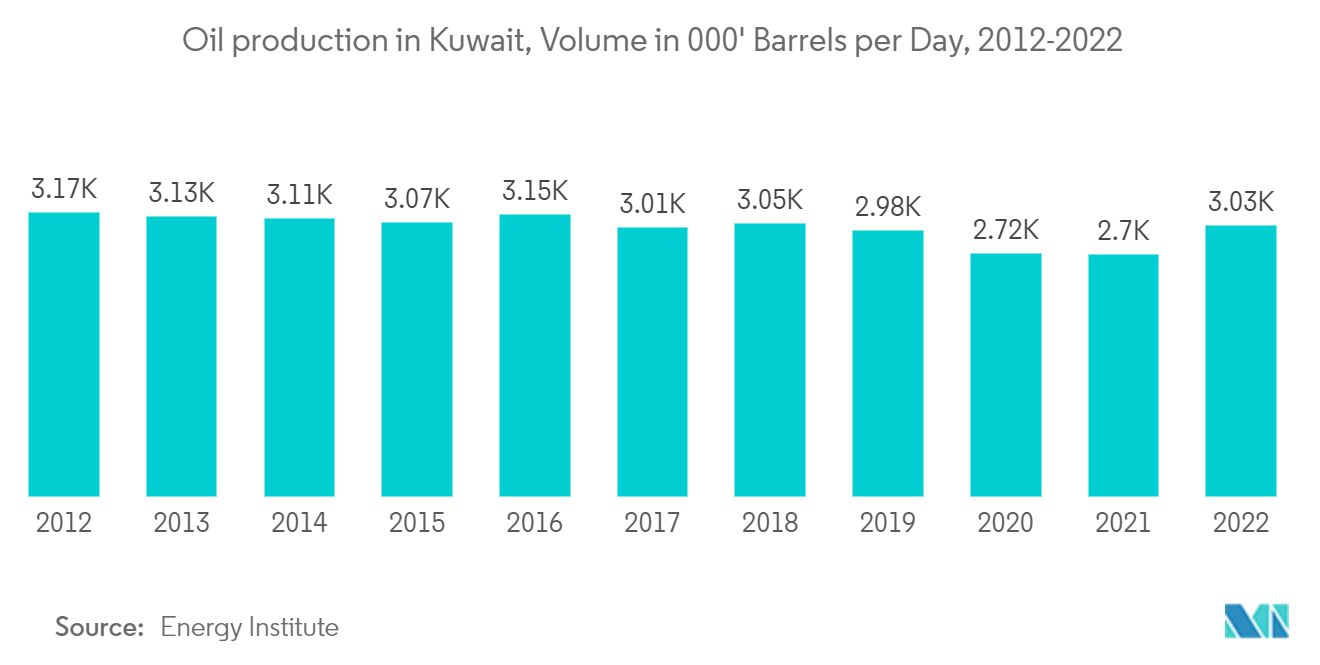

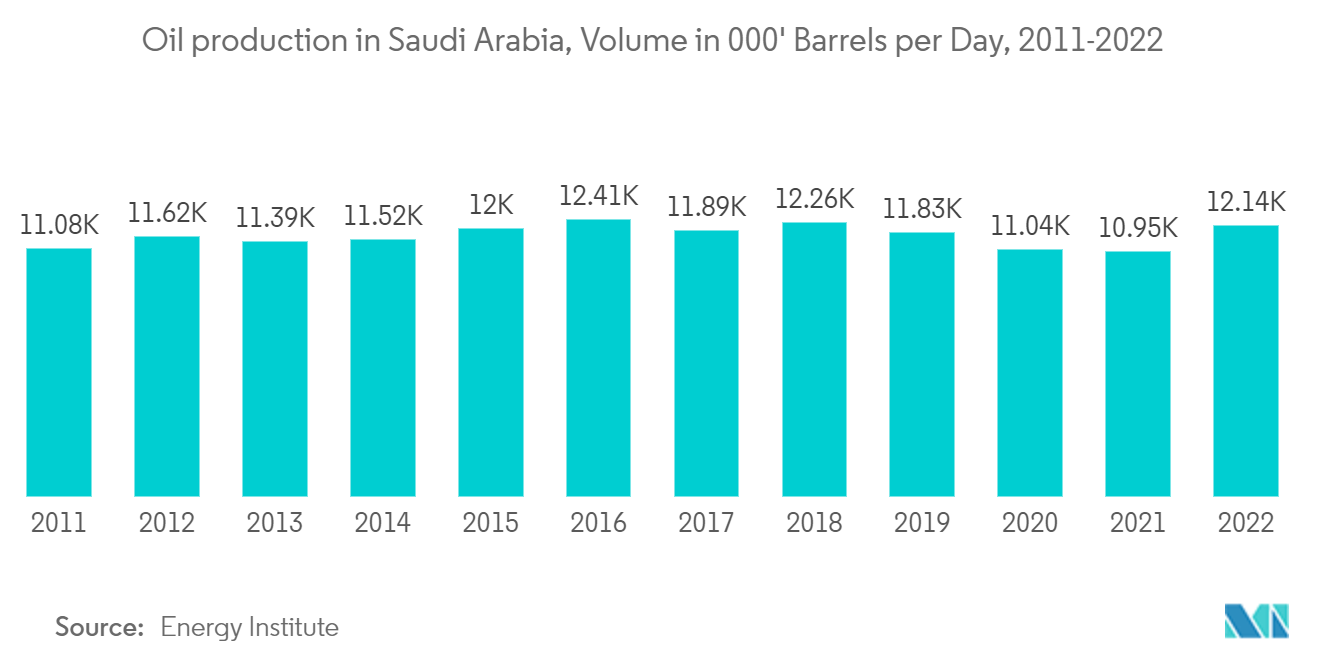

In the GCC region, Saudi Arabia dominates the entire region's chemical output, and the Kingdom-based companies are accounting for more than 75 - 80 % of total GCC chemical sales by value. In addition, the increasing oil production in Saudi Arabia also complements the chemical industry growth. Meanwhile, in 2023, the GCC chemical industry planned to invest more than USD 61 billion until 2025 to increase production and sales along with focusing on environmental factors. Thus, the growing chemical industry across the region is expected to drive the logistics industry.

New Investments in the Market

Strong oil and gas prices in 2022 have helped energy producers in the Middle East and North Africa (MENA) area, which is evident in both their profitability and capital spending budgets for the year. In the first half of 2022, contracts for oil and gas worth about USD 14.1 billion were given, with the Saudi Arabian market accounting for almost half of that amount thanks to contracts for the development of the Zuluf oil field. With a USD 82.5 billion capital expenditure budget set aside for 2021-25 by its state company, Qatar, which is also in the spending mood, is in second place. Saudi Aramco and QatarEnergy collectively accounted for nearly 60%, or USD 5.5 billion, of the contracts awarded in the first half of 2022.

Upstream investment has been driven by the need to meet growing domestic and international demand and to replace supplies lost due to the use of up natural resources. As international oil firms shift their portfolios towards gas production, which is viewed as a greener alternative to oil, investment in gas projects has increased during the past five years. The prospects for the Mena region are still stronger than they were two years ago because of the region's oil exporters, particularly the GCC, Iraq, and Algeria, even though the rate of global development is expected to decline in the coming years. Additionally, Mena nations will bear the bulk of future global investments in oil and gas. Over the next five years, the Arab Petroleum Investments Corporation anticipates that investments in Mena energy (oil, gas, petrochemicals, and power) will rise by 9% to more than USD 875 billion.