Market Size of Europe Water Automation and Instrumentation Industry

| Study Period | 2019 - 2029 |

| Base Year For Estimation | 2023 |

| Forecast Data Period | 2024 - 2029 |

| Historical Data Period | 2019 - 2022 |

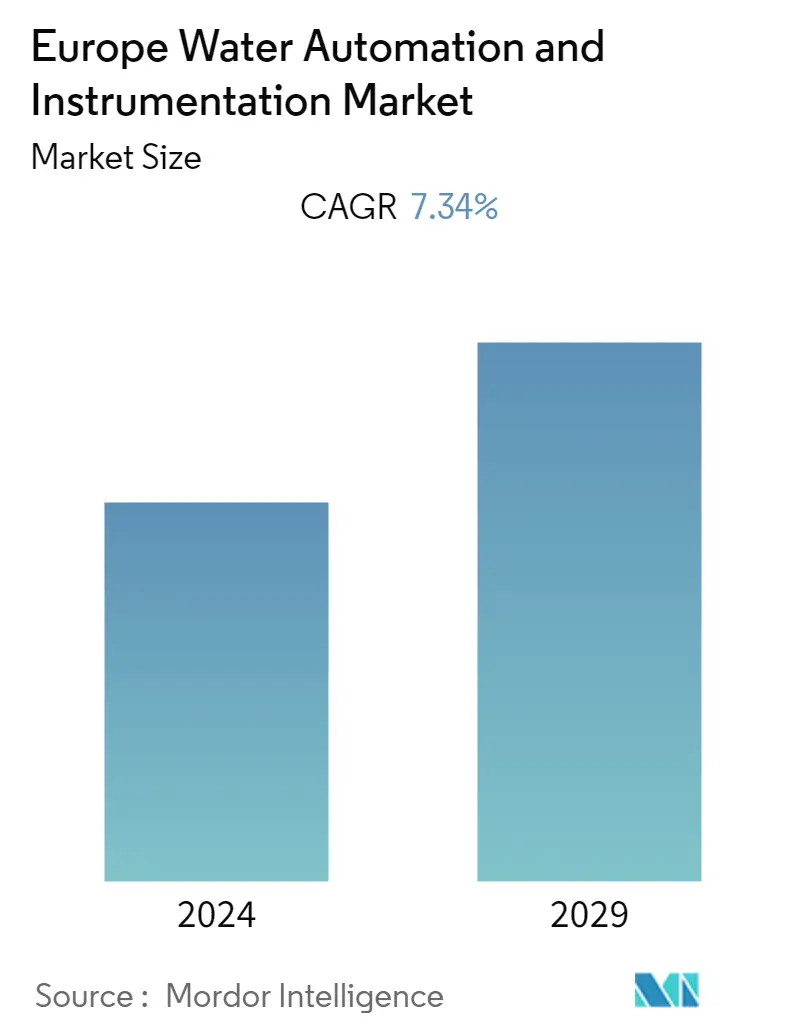

| CAGR | 7.34 % |

| Market Concentration | Low |

Major Players

*Disclaimer: Major Players sorted in no particular order |

Need a report that reflects how COVID-19 has impacted this market and its growth?

Europe Water Automation & Instrumentation Market Analysis

Europe Water Automation and Instrumentation Market is anticipated to witness a CAGR of 7.34% over the forecast period 2021 - 2026. Europe's water automation and instrumentation market are estimated to increase in the years to come. This increase is because of a variety of factors, including increased usage of water in sectors like the generation of electricity, wastewater treatment plants, the supply of clean water, etc.

- Managing operational costs emerged as one of the biggest challenges posed by stakeholders of the water industry, as the governments are imposing regulations, along with depletion of potable water resources. Expenses relating to labor and energy constitute the largest share in OPEX for water utilities.

- Several water automation-related technology developments currently being explored in the market include smart monitoring technologies using pressure and acoustic sensors to detect, report, and reduce water loss via wireless monitoring systems; and recent advances in water management through optimizing wastewater processing and recycling, as tracking data and scientific understanding continues to improve.

- Non-revenue water (NRW) is known as water lost before it reaches a customer. Losses can occur from leaks in the distribution network, during a theft, etc. According to the World Bank, the total cost to water utilities is from non-revenue water worldwide can be conservatively estimated at USD 141 billion per year, with a third of it occurring in the developing world. The rising demand to reduce non-revenue water losses led water utilities to adopt advanced water management solutions.

- The instrumentation and automation solutions involved in the water industry need periodic maintenance. Therefore, the pressure lies on the end-user of the equipment, who must bear the maintenance expenses throughout the product's lifetime. Also, their maintenance and handling require high skill. Consequently, manufacturers face difficulties while operating automation and control systems due to a lack of qualified and skilled applicants.

- The outbreak of COVID-19 halted the production and disrupted the supply chain, which led to weakened industrial output growth and the decline in the production of multiple types of equipment, such as transmitters, and affected the use of HMI SCADA systems and distributed control systems.