Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

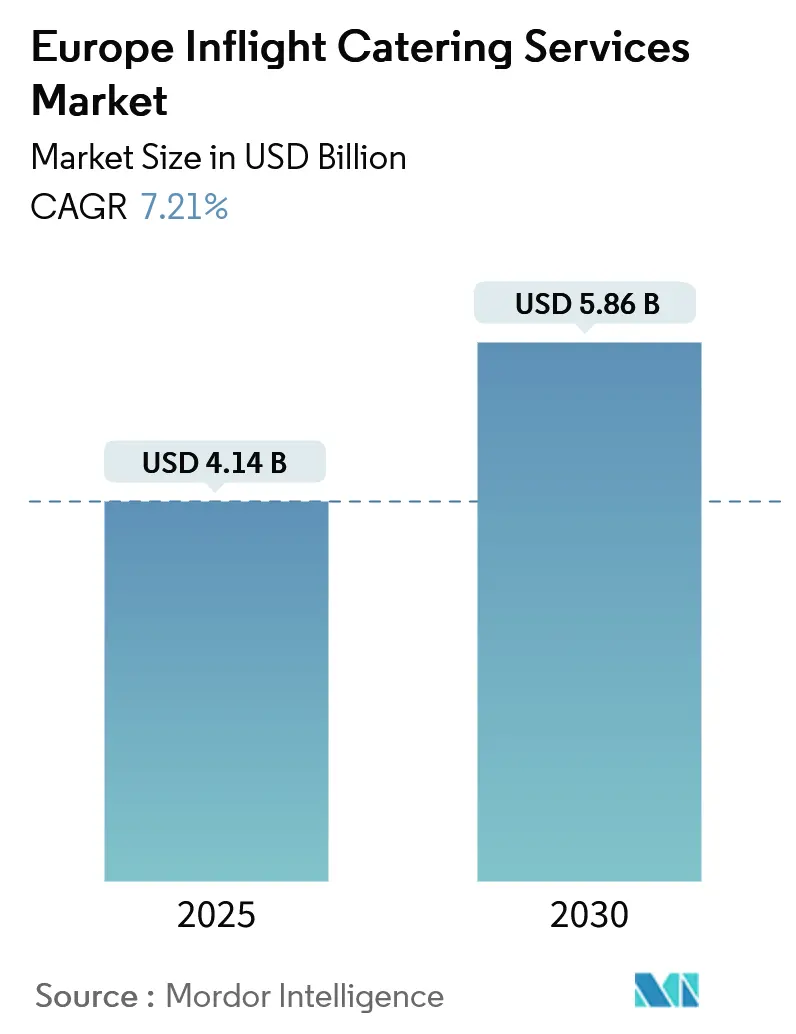

| Market Size (2025) | USD 4.14 Billion |

| Market Size (2030) | USD 5.86 Billion |

| Growth Rate (2025 - 2030) | 7.21% CAGR |

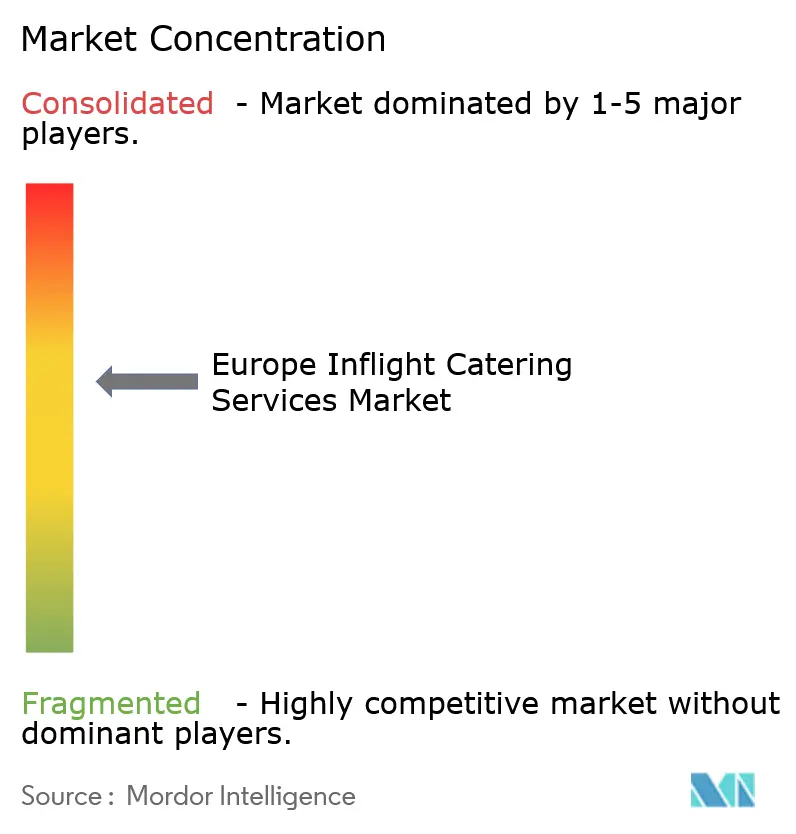

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Inflight Catering Services Market Analysis by Mordor Intelligence

The Europe Inflight Catering Services Market size is estimated at USD 4.14 billion in 2025, and is expected to reach USD 5.86 billion by 2030, at a CAGR of 7.21% during the forecast period (2025-2030).

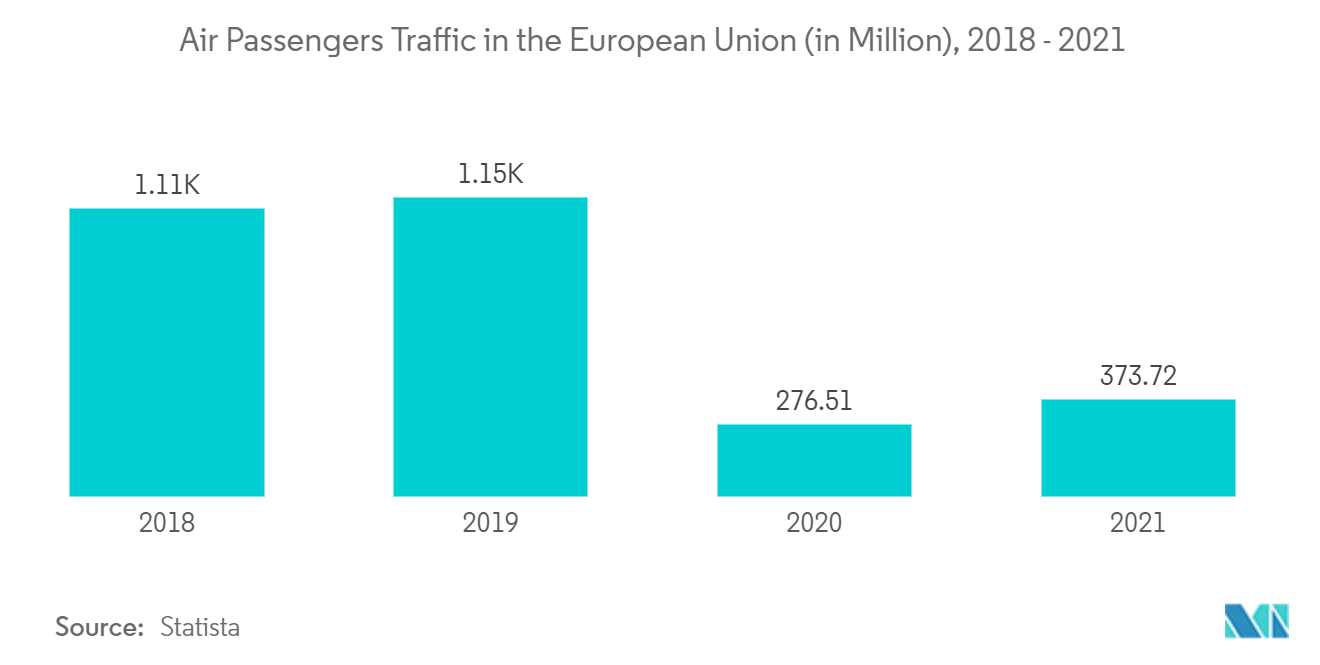

The European region is one of the major aviation industries that was severely impacted due to the COVID-19 pandemic. Airlines in the area significantly decreased their aircraft operations and restricted inflight services, including catering services. Nevertheless, in 2021, passenger traffic witnessed an increase compared to the previous year, and a full recovery is expected by 2024. As passenger traffic returned to pre-COVID-19 levels, the airlines in the region gradually reintroduced inflight catering menus.

In the European region, the focus on food quality and offerings are more pronounced toward the economy class of the airlines. Economy class passengers contribute to airline revenue, and they continue to be the most important class of passengers for carriers. To maintain their shares, most carriers are in the process of improving the quality of food served.

Due to growing competition in profitable long-distance routes, airlines are collaborating with famous chefs to differentiate their service offerings with specialized menu items. Partnering with star chefs can help airlines carve out special dishes to attract passengers and increase market share.

Europe Inflight Catering Services Market Trends and Insights

The Bakery and Confectionery Segment is Expected to Dominate the Market During the Forecast Period

- The bakery and confectionery segment dominates the European inflight catering market. It is expected to continue its dominance over the market during the forecast period as passengers from the region prefer bread and other baked items in most of their dining compared to the other regions.

- There was a notable rise in domestic and intra-Europe travel in 2021, with a total market share capturing more than 60%. This shift in operations changed the average flight duration from 45 to 60 minutes. In such short flights, changes in guest preference led to increased demand for bakery and confectionery items. Among bakery products, sweet and sour bread, flavored croissants, and cheese confectionaries witnessed the highest market share.

- However, some airlines in the region are converting complementary services into retail services, which may help the airlines increase their revenues and mitigate their pandemic losses. For instance, in December 2021, Lufthansa began to charge passengers in economy and premium economy on long-haul flights for mid-flight snacks and liquor as part of its recovery plans. Earlier in 2021, the airline removed free snacks and drinks for economy class passengers on short-haul routes to support onboard retail service. The introduction of new snacks and sweets on the menu is anticipated to propel the growth of the market.

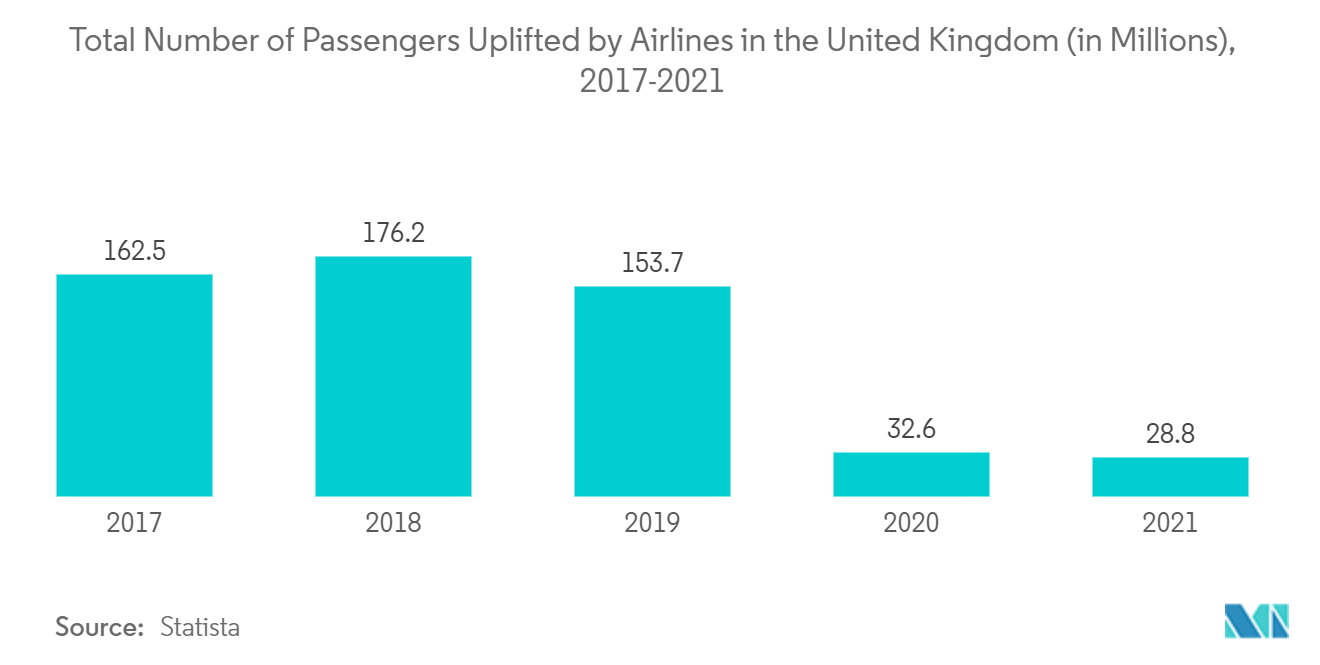

The United Kingdom is Expected to Witness Significant Growth During the Forecast Period

- According to the Advance Passenger Information (API) and Border and Immigration Transaction Data (BITD), United Kingdom air arrivals were 28.60 million in 2020 and 22.84 million in 2021. Though air arrivals decreased by 20.1% in 2021 compared to 2020, however, during the second half of 2021, air arrivals increased by approximately 88% compared to 2020.

- As the aviation industry in the country recovers gradually, major airlines like British Airways and EasyJet are increasing their global connectivity with the introduction of new destinations, which is expected to bring new menus onboard aircraft. Airlines in the country are looking to improve their food offerings based on season and flight destination. Partnering with star chefs is helping them modify dishes without incurring high costs. In this regard, in October 2021, Virgin Atlantic introduced its new autumn menu options and reintroduced onboard favorites across all its cabins, including new meal, beverage, and snack options.

- Major companies are investing significantly to strengthen their presence in the United Kingdom. For instance, in March 2022, dnata, a global ground services provider, was appointed to manage easyJet's inflight retail services across the airline's extensive network. Under the contract, the company will deliver an onboard retail program and advanced solutions for the airline and support it further to enhance its retail range onboard and customer satisfaction. Such developments are expected to help the growth of revenues from the country during the forecast period.

Competitive Landscape

The inflight catering market in Europe is moderately consolidated, and a few major players, such as Gategroup, KLM catering services, the Emirates Group, DO & CO Aktiengesellschaft, and Newrest Group Services SAS, primarily dominate it. These companies increased their market presence in the past through the acquisition of local restaurants and other smaller catering companies. The acquisition of LSG's European operations by Gategroup would result in Gategroup accounting for a major share of the European inflight catering market in the coming years.

In addition to this, catering companies are introducing new technologies to reduce overall operational costs and increase their operational efficiencies. For instance, KLM Catering Services (KCS) is more focused on technological integration to fight the crisis. The introduction of new cost-cutting measures, as well as partnerships with new airlines, is anticipated to help the companies increase their geographic presence in the region in the coming years.

Europe Inflight Catering Services Industry Leaders

Newrest Group Services SAS

DO & CO Aktiengesellschaf

The Emirates Group

KLM Catering Services

Gategroup

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2022: Scandinavian Airlines partnered with Newrest for its inflight catering services. Under the agreement, the company would provide inflight catering services to SAS in the capital cities of Sweden, Norway, and Denmark.

- July 2021: Gategroup acquired LSG Group's European operations from Deutsche Lufthansa AG (Lufthansa). The transaction comprised LSG's inflight catering operations in Germany, Switzerland, the Netherlands, Belgium, Italy, and Spain and the global equipment business trading under the SPIRIANT brand.

Europe Inflight Catering Services Market Report Scope

Inflight food is the food served to passengers onboard a commercial airliner. Specialist airline catering services prepare these meals and usually serve them to passengers using an airline service trolley.

The Europe inflight catering market is segmented by seating class, flight type, food type, and country. By seating class, the market is segmented into economy class, business class, and first class. By flight type, the market is segmented into full-service carriers (FSCS) and low-cost carriers (LCCs). By food type, the market is classified as meals, bakery and confectionery, beverages, and other food types.

The report offers the market size and forecasts by value (USD million) for all the above segments.

Food Type

| Meals |

| Bakery and Confectionary |

| Beverages |

| Other Food Types |

Flight Type

| Full-service Carriers |

| Low-cost Carriers |

Aircraft Seating Class

| Economy Class |

| Business Class |

| First Class |

Geography

| United Kingdom |

| Germany |

| France |

| Russia |

| Italy |

| Spain |

| Rest of Europe |

| Food Type | Meals |

| Bakery and Confectionary | |

| Beverages | |

| Other Food Types | |

| Flight Type | Full-service Carriers |

| Low-cost Carriers | |

| Aircraft Seating Class | Economy Class |

| Business Class | |

| First Class | |

| Geography | United Kingdom |

| Germany | |

| France | |

| Russia | |

| Italy | |

| Spain | |

| Rest of Europe |

Key Questions Answered in the Report

How big is the Europe Inflight Catering Market?

The Europe Inflight Catering Market size is expected to reach USD 4.14 billion in 2025 and grow at a CAGR of 7.21% to reach USD 5.86 billion by 2030.

What is the current Europe Inflight Catering Market size?

In 2025, the Europe Inflight Catering Market size is expected to reach USD 4.14 billion.

Who are the key players in Europe Inflight Catering Market?

Newrest Group Services SAS, DO & CO Aktiengesellschaf, The Emirates Group, KLM Catering Services and Gategroup are the major companies operating in the Europe Inflight Catering Market.

What years does this Europe Inflight Catering Market cover, and what was the market size in 2024?

In 2024, the Europe Inflight Catering Market size was estimated at USD 3.84 billion. The report covers the Europe Inflight Catering Market historical market size for years: 2019, 2020, 2021, 2022, 2023 and 2024. The report also forecasts the Europe Inflight Catering Market size for years: 2025, 2026, 2027, 2028, 2029 and 2030.

Page last updated on: