Market Trends of UK Commercial Real Estate Industry

Increasing rents of office spaces

- With approximately 143 million square feet of available office stock, London City had the most office real estate supply among the major office markets in the United Kingdom (UK) as of the second quarter of 2022. This accounted for almost 40 percent of the total available space in the market during that quarter. Outside of London, Manchester had the most available office stock.

- Despite the high office rental costs, vacancy rates in many of London's primary office markets were below six percent in 2022. This is good news for the office sector, as the share of vacant office space across all Central London districts spiked dramatically during the COVID-19 pandemic. Compared to other European cities, London was in the middle of the ranking, alongside Frankfurt and Lisbon.

- According to industry associates, transaction volumes for the office sector in the fourth quarter of 2022 were EUR 1.1 billion (USD 1.19 billion), down 74% from volumes in the third quarter of 2022, marking the lowest volumes reported since 2002. On a year-on-year basis, transaction volumes were down 86% from those in the fourth quarter of 2021. Only 77 office properties changed hands in the fourth quarter of 2022.

- The office sector experienced significant structural pressure as working habits underwent alterations following the COVID-19 pandemic. Secondary accommodation was at risk of obsolescence and asset stranding, while the capital requirements to ensure assets met minimum Environmental, Social, and Governance (ESG) requirements proved prohibitive to achieving positive returns within the sector. Limited transactional evidence toward the end of 2022 indicated that further pricing discovery was expected in the first half of 2023, according to experts.

Understand The Key Trends Shaping This Market

Download Sample

Office segment showing a significant growth in the market

- The office real estate sector in the United Kingdom has encountered several challenges in recent years, beginning with the United Kingdom's decision to leave the European Union in 2016, followed by years of lengthy negotiations, and culminating in the COVID-19 crisis that paralyzed the world economy in 2020. Despite these challenges, the UK still boasts one of the largest office real estate markets in Europe.

- Offices have consistently been the top choice for investors when it comes to commercial real estate investments in the United Kingdom, accounting for more than half of total investment volumes.

- According to industry sources, office investment across the United Kingdom totaled EUR 1.27 billion (USD 1.38 billion) during Q4 2022, marking a 71% decline from Q3 2022 and an 82% drop compared to Q3 2021, attributed to escalating borrowing costs and wider economic turbulence. Throughout 2022, UK office investment amounted to EUR 18.13 billion (USD 19.67 billion), the second lowest annual volume since 2012, surpassing only the pandemic-marred 2020.

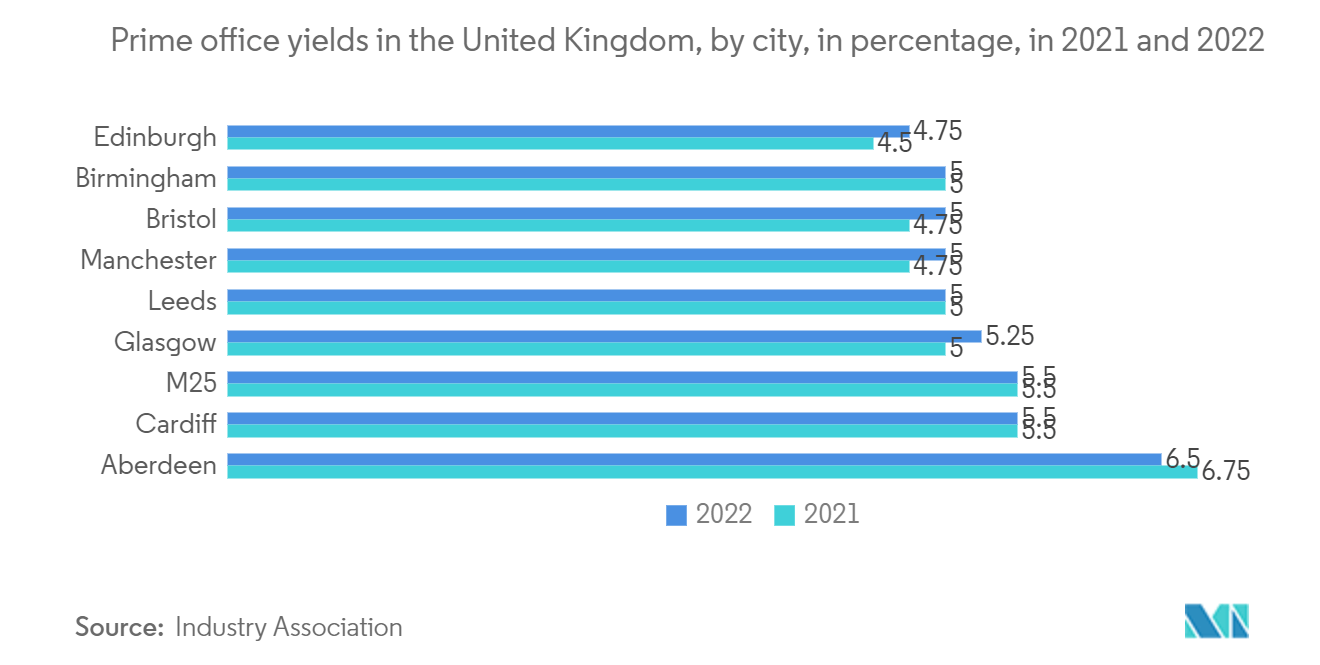

- The slowdown in activity and pricing shifts has led to yields expanding across all markets, with forecasts indicating further softening in 2023 and liquidity expected to return to the market during the first half of 2024.

- Five years of Brexit negotiations have significantly influenced the landscape of office space, and the coronavirus pandemic has added an extra layer of insecurity about the future of offices.

- Office take-up is experiencing a resurgence in 2023. High equity targeting the central London prime office market is driving recovery from the pandemic as uncertainties resolve. Flexibility, ESG considerations, and meeting employee lifestyle needs will guide development standards as organizations aim to future-proof their offices. Value-add opportunities are emerging from these trends in multiple UK cities.