Market Size of China Paper Packaging Industry

| Study Period | 2019 - 2029 |

| Base Year For Estimation | 2023 |

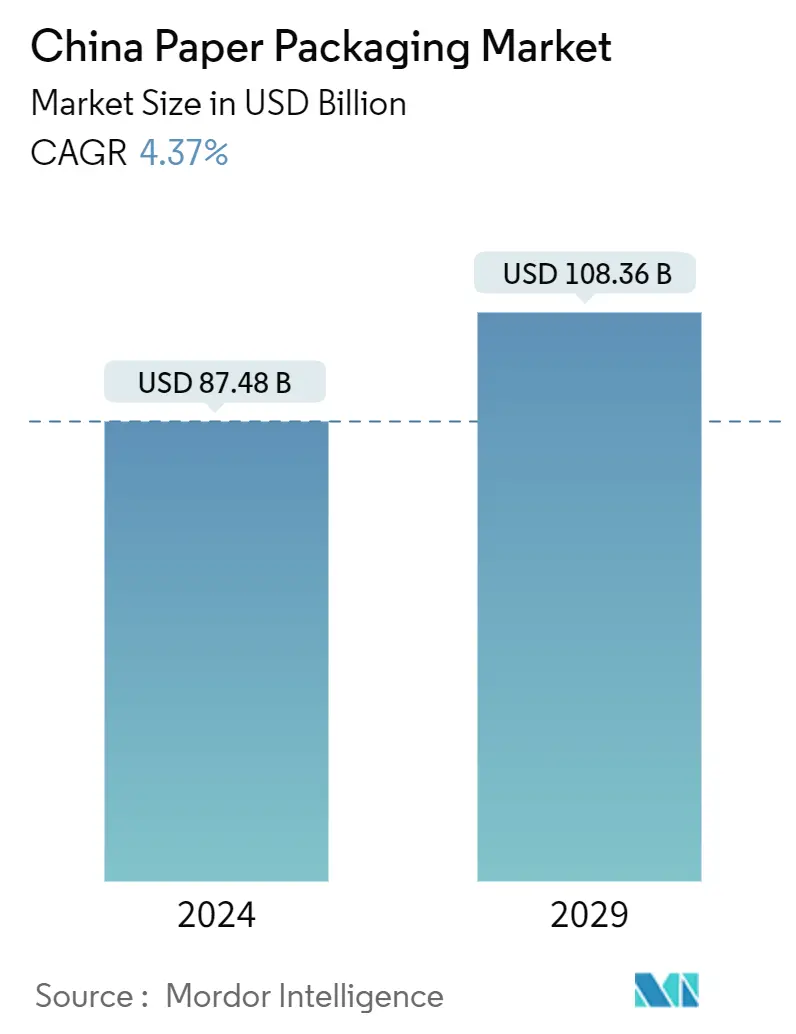

| Market Size (2024) | USD 87.48 Billion |

| Market Size (2029) | USD 108.36 Billion |

| CAGR (2024 - 2029) | 4.37 % |

| Market Concentration | Low |

Major Players*Disclaimer: Major Players sorted in no particular order |

Need a report that reflects how COVID-19 has impacted this market and its growth?

China Paper Packaging Market Analysis

The China Paper Packaging Market size is estimated at USD 87.48 billion in 2024, and is expected to reach USD 108.36 billion by 2029, growing at a CAGR of 4.37% during the forecast period (2024-2029).

The Chinese pulp and paper industry is the largest in terms of production and demand in the world. Domestic industries like e-commerce, food delivery services, etc., would continue to grow, and so will the consumption of pulp and paper products. This presents significant market entry and investment opportunities across the country.

- Packaging paper makes up the largest share of paper products produced and consumed in China. The most common types of paper used for packaging are folding cartons and corrugated boxes. The growth of paper production is driven by the constant demand for paper packaging from the end-user industries across the country.

- The Chinese e-commerce industry has experienced rapid growth in the past few years. Innovations by e-commerce technologies drive entrepreneurship to benefit small and medium enterprises (SMEs). With the emergence of IT, e-commerce has become one of the most prominent business and economic trends in China in just a short period. The advantages of e-commerce include 24/7 availability, fast access, a greater variety of products and services, ease of access, and global reach. The requirement for different modes of packaging shows positive trends.

- The Chinese foodservice market is primarily driven by the rising frequency of dining out amid the time-pressed schedules of the young and working population and the increasing influence of Western dietary patterns with the presence of global companies, mainly in urban areas. The working population's accessibility to restaurants that offer quality food and services is also expected to drive the market. These factors have also led to the rapid growth of the fast-food sector in China, expanding more food chains in the quick-service sector, thus benefitting the overall market studied.

- One of the challenges encountered in the paper manufacturing industry is contamination. If paper is contaminated with other materials, such as food waste and plastic, it can make it difficult and costly to recycle and decrease the quality of the recycled product. This contamination can happen at any point in the recycling process, from collection to processing, resulting in additional costs for the industry.

- Owing to the COVID-19 pandemic, consumers are now more concerned about hygiene, disability, and the sustainability of products. The changing needs of the consumers and the need for a consumer-centric approach will continue to be important as the pandemic continues. Consumer behavior is expected to evolve as the market adapts to the current situation. As a result, the demand for paper packaging in the post-pandemic era is expected to grow.