Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

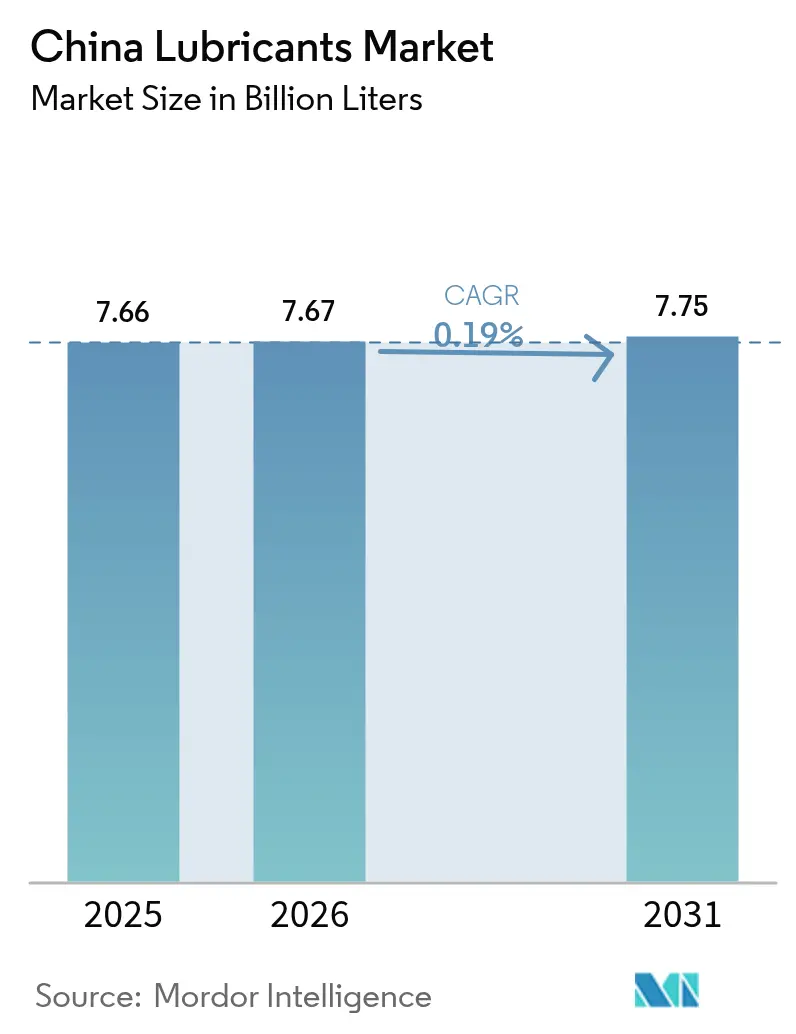

| Base Year Market Size (2025) | 7.66 Billion liters |

| Market Volume (2026) | 7.67 Billion liters |

| Market Volume (2031) | 7.75 Billion liters |

| Growth Rate (2026 - 2031) | 0.19% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

China Lubricants Market Analysis by Mordor Intelligence

The China lubricants market size was valued at 7.66 billion liters in 2025 and estimated to grow from 7.67 billion liters in 2026 to reach 7.75 billion liters by 2031, at a CAGR of 0.19% during the forecast period (2026-2031). China's lubricants market growth remains flat because the rapid adoption of electric vehicles erodes gasoline engine oil volumes, even as infrastructure spending supports demand for heavy-duty and industrial fluids. Competitive pressure increases as state-owned refiners integrate upstream base-oil production with downstream distribution while global majors push premium synthetics. OEM warranty extensions, longer drain intervals, and dual-carbon regulations accelerate the penetration of synthetic products. E-commerce broadens geographic reach but magnifies counterfeit risks, prompting brand owners to invest in traceability technologies.

Key Report Takeaways

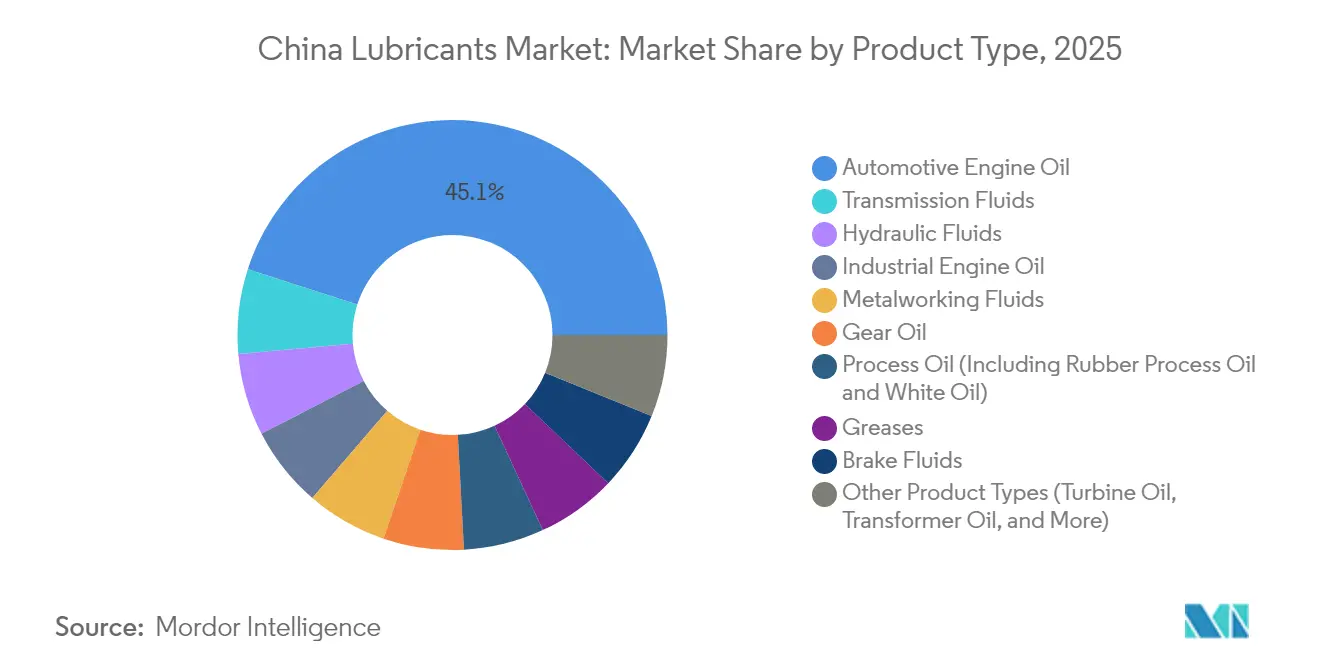

- By product type, Automotive Engine Oil led with 45.05% revenue share in 2025, while Transmission Fluids are projected to register a 1.03% CAGR through 2031.

- By end-user industry, the Automotive segment held 57.90% of China's lubricants market share in 2025; Heavy Equipment is forecast to expand at a 1.10% CAGR to 2031.

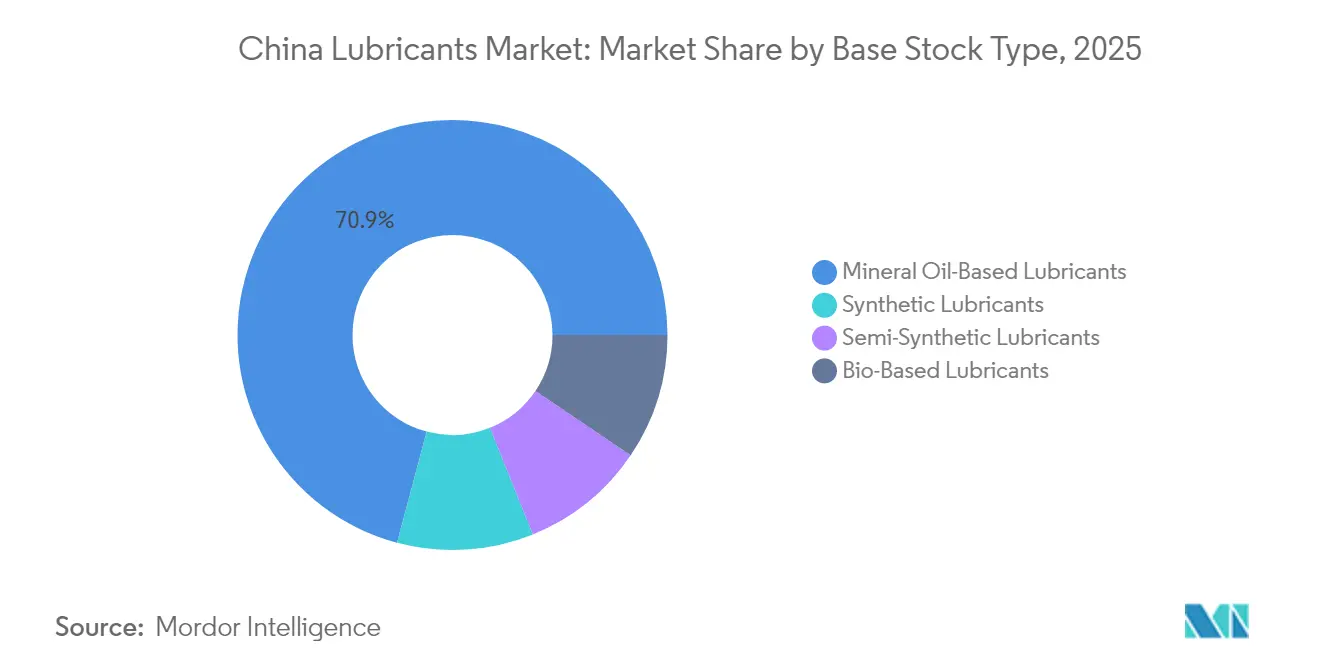

- By base stock type, Mineral Oil-Based fluids accounted for 70.85% share of the China lubricants market size in 2025, and Synthetic Lubricants are advancing at a 1.34% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

China Lubricants Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Diesel-truck parc rebound in post-COVID logistics | + 0.3% | National, with concentration in industrial corridors | Short term (≤ 2 years) |

| Restart of domestic base-oil projects improves supply stability | + 0.2% | National, particularly Northeast and East China | Medium term (2-4 years) |

| OEM warranty extension pushes demand for premium long-drain synthetics | + 0.15% | National, with premium segment focus in Tier 1 cities | Medium term (2-4 years) |

| Explosion of e-commerce channels for HDMO and PCMO | + 0.1% | National, with rural penetration acceleration | Short term (≤ 2 years) |

| Accelerated "dual-carbon" policy drives bio-lube adoption | + 0.1% | National, with pilot programs in key industrial zones | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Diesel-Truck Parc Recovery Stabilizes Commercial Lubricant Demand

Heavy-duty diesel truck registrations increased in early 2025 as logistics activity returned to normal, underpinning steady demand for high-viscosity engine oils and transmission fluids[1]Base Oils Report Editorial, “China Import Trends February 2025,” Base Oils Report, baseoilsreport.com. Infrastructure projects increased base-oil imports from Singapore by 15% in February 2025, highlighting the positive correlation between construction activity and lubricant consumption. However, the adoption of LNG trucks in long-haul freight reduces conventional diesel lubricant volumes because gas engines require different formulations and longer service intervals. The resulting split encourages suppliers to develop fluids tailored for both diesel and alternative-fuel drivetrains. Fleet owners prioritize total cost of ownership, favoring synthetics that enable extended drains and reduced downtime.

Domestic Base-Oil Production Restart Reduces Import Dependency

Refineries owned by PetroChina and Sinopec restarted their base-oil units, which had been idle during 2020-2022, reducing their reliance on imports from Singapore and South Korea[2]Energy Intelligence Desk, “China Restarts Base-Oil Units,” Energy Intelligence, energyintel.com. Domestic crude feedstock offers cost advantages and shortens supply chains for local blenders. Average refinery utilization fell to 75% in 2024, which paradoxically improved base-oil margins because lower competition for feedstock eased price pressure. Enhanced supply stability enables Chinese blenders to reduce working-capital requirements associated with imported inventories. Lower domestic costs may make Chinese base oils competitive in Southeast Asia, opening new export avenues.

OEM Warranty Extensions Accelerate Synthetic Lubricant Adoption

Automotive manufacturers have extended warranty periods to 8-10 years, mandating the use of synthetics to minimize warranty claims. Premium PAO and ester-based oils now support intervals of 15,000-20,000 kilometers, significantly surpassing the 5,000-7,500 kilometers typically achieved by mineral oils. Shell advanced GTL-derived e-fluids for electric vehicles, addressing thermal and electrical needs of new drivetrains. Longer intervals reduce consumer price sensitivity, helping suppliers capture higher margins per liter sold. Rising GB national standards reinforce this trend by specifying performance targets that can only be achieved with synthetic formulations.

E-Commerce Penetration Transforms Distribution While Enabling Counterfeits

Online platforms enable lubricant brands to directly reach rural mechanics and do-it-yourself consumers, thereby reducing distributor margins. Yet counterfeit products flourish on marketplace channels, undermining brand equity and squeezing authentic price points. Legitimate suppliers deploy QR-code traceability and tamper-proof seals to protect consumers. Balancing reach and risk requires robust channel management and consumer education. Regulators lag behind the digital retail shift, creating enforcement gaps that are exploited by sophisticated counterfeit networks.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid BEV penetration shrinks ICE engine-oil pool | -0.4% | National, with acceleration in Tier 1 cities and coastal regions | Medium term (2-4 years) |

| Longer OEM drain intervals cut service-fill volumes | -0.25% | National, affecting premium automotive segments and urban markets | Short term (≤ 2 years) |

| Volatile crude swings squeeze blender margins | -0.15% | National, with particular impact on independent blenders | Short term (≤ 2 years) |

| Persistent counterfeits undermine brand pricing power | -0.1% | National, concentrated in e-commerce channels and rural markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Electric Vehicle Adoption Accelerates ICE Lubricant Demand Destruction

Battery electric vehicles surpassed 40% of new car sales in early 2025, displacing annual engine oil consumption by 4-5 liters per vehicle and lowering gasoline demand projections. Refined-product consumption declined 1.7% in 2024, signaling a structural shift rather than a cyclical dip [SINOLUB.COM]. Oil majors responded by converting service stations into mixed-energy hubs with EV charging, but this pivot cannot replace lost lubricant volume. Reduced gasoline production also tightens base-oil supply for non-automotive segments, influencing price dynamics across the China lubricants market.

Extended Drain Intervals Compress Service Market Volumes

Synthetic formulations that allow for 15,000-20,000-kilometer drain intervals cut the annual lubricant need per vehicle by up to 50%. Quick-lube shops relying on frequent oil-change traffic face revenue pressure, triggering consolidation toward larger chains. Advanced engine designs with tighter tolerances reduce oil blow-by and contamination, further lowering top-up demand. Suppliers must shift focus from high-turnover mineral grades to lower-volume, higher-margin synthetics to balance revenue. Emissions regulations encourage the use of low-viscosity oils, which improve fuel economy and reinforce the extended-drain trend.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Transition from Engine Oils to Specialized Fluids

Automotive engine oil held 45.05% of China lubricants market share in 2025, yet faces decline as NEV adoption rises. Transmission Fluids are forecast to grow at a 1.03% CAGR, helped by the wider adoption of automatic gearboxes and dedicated e-axle fluids. Hydraulic Fluids and Greases serve construction machinery, which benefits from infrastructure programs. Brake Fluids show stable demand across ICE and EV platforms, though longer intervals limit volume growth. Gear Oil gains from mining and heavy-duty equipment that require extreme-pressure formulations.

Battery-electric drivetrains require thermal management and dielectric fluids, rather than engine oil, shifting the product mix toward specialty synthetics. Industrial Engine Oil targets power generation and marine engines where electrification remains limited. Process Oils and Metalworking Fluids correlate with manufacturing output, posting moderate gains as China upgrades industrial capacity. Turbine and Transformer Oils benefit from renewable-energy installations. The evolving portfolio indicates how China's lubricants market size redistributes from declining passenger-car engine oils to niche industrial and electric-vehicle fluids.

By End-User Industry: Heavy Equipment Becomes Growth Anchor

Automotive accounted for 57.90% of China lubricants market size in 2025, but its volume contracts as EV penetration rises. Heavy Equipment is projected to expand at a 1.10% CAGR through 2031, buoyed by infrastructure investments and resource extraction. Marine demand grows steadily with shipbuilding and offshore wind projects requiring cylinder and gear oils. Aerospace consumption expands with commercial aviation recovery and new space initiatives needing high-temperature greases.

Industrial users in power generation, metallurgy, and oil and gas maintain steady lubricant need, sheltered from electrification’s direct impact. Mining equipment demands extreme-pressure fluids and contributes to stable base-oil off-take. Urban rail and high-speed rail projects increase hydraulic fluid usage for construction machinery. Collectively, these trends position heavy equipment and industrial sectors as the core volume stabilizers for China lubricants market.

By Base Stock Type: Synthetics Capture Premium Value

Mineral oil-based products still commanded 70.85% of China's lubricants market share in 2025 due to cost efficiency. Synthetic Lubricants register the fastest 1.34% CAGR, propelled by stringent OEM specifications and dual-carbon incentives. Semi-Synthetic fluids offer a cost-performance compromise for price-sensitive segments. Bio-based lubricants, though small, gain traction under tax exemptions extended to 2027.

Performance requirements such as low volatility, high oxidation stability, and dielectric properties support the uptake of synthetic materials in EV and industrial automation applications. PAO and ester base stocks address longer drain intervals, high-temperature stability, and energy efficiency. Recycled base oils supported by excise relief create a domestic circular supply that improves sustainability credentials. As synthetic adoption spreads, mineral oil volumes will decline, but diversified applications in heavy equipment and process industries maintain baseline demand.

Geography Analysis

The eastern provinces, comprising Jiangsu, Zhejiang, and Guangdong, generate the largest share of China's lubricants market, driven by the presence of dense manufacturing clusters that consume industrial oils and metalworking fluids. Northern hubs such as Hebei and Shanxi depend on steel and energy, driving demand for turbine and gear oils. Western regions, including Xinjiang and Inner Mongolia, experience higher growth rates because mining and infrastructure projects utilize heavy-duty hydraulic and engine oils.

Tier 1 coastal cities adopt BEVs the fastest, resulting in a decline in passenger-car engine oil sales in Shanghai, Beijing, and Shenzhen. Smaller inland cities and rural counties still rely on ICE vehicles, preserving conventional automotive lubricant demand. Southern ports support marine lubricants through shipping lanes and offshore wind developments that need gear and hydraulic oils. Belt and Road logistics corridors from Yunnan into Southeast Asia spur cross-border truck traffic, sustaining demand for heavy-duty diesel oils.

Regional policy variations influence product mix. Coastal environmental regulations require low-sulfur, low-phosphorus additives, favoring synthetic and bio-based formulations. Interior provinces prioritize cost and thus maintain their dominance in the mineral-oil sector. Domestic base-oil refineries clustered in Liaoning and Shandong shorten supply lines for northeastern markets, while southwestern provinces rely on imported Group III stocks via coastal terminals. E-commerce penetration rises fastest in smaller cities, creating new distribution nodes for lubricant brands.

China lubricants market size shows differing regional sensitivities: coastal regions experience declining engine-oil volume but rising specialty synthetic demand, whereas inland regions sustain bulk mineral oil consumption. Markets in the Pearl River Delta pivot toward EV thermal fluids, while Bohai Bay petrochemical bases expand Group II and Group III capacities. Emerging economic zones along the Yangtze River promote green-manufacturing initiatives that incentivize low-carbon lubricants. This mosaic underscores the need for regionally tailored strategies by suppliers.

Competitive Landscape

The China lubricants market is moderately consolidated, with the top five companies occupying a significant market share. China's lubricants market exhibits a dual structure, combining upstream dominance by state-owned refiners with downstream premium competition from global majors. PetroChina and Sinopec control most base-oil production and nationwide fuel station networks, giving them a significant scale and logistical advantage. Their integrated model supports aggressive pricing in commodity grades while cross-selling lubricants through retail outlets and industrial supply contracts. International companies differentiate through technology and brand strength in synthetic and specialty fluids. Domestic independent companies invest in research and development to produce high-performance lubricants for niche industrial applications. These firms leverage local knowledge and agile operations to secure contracts in the mining and construction sectors. Brand holders battle counterfeiters by embedding QR-code traceability and partnering with marketplaces for enforcement. Heightened regulatory oversight on emissions and carbon drives all players to expand low-viscosity and bio-based portfolios, differentiating through sustainability claims.

China Lubricants Industry Leaders

PetroChina Company Limited

Sinopec (China Petrochemical Corporation)

Shell plc

ExxonMobil Corporation

ZHONGTIAN PETROCHEMICAL

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2024: Chevron Oronite announced an investment in lubricant additive production capabilities in China, targeting the growing synthetic lubricant market and OEM specification requirements for advanced engine oil formulations.

- July 2024: Quaker Houghton, a global leader in industrial process fluids, has commenced construction of a state-of-the-art manufacturing facility in Zhangjiagang, China. Scheduled to begin operations by the second quarter of 2026, the facility is designed to enhance production capabilities and support the Company's strategic growth objectives in the Asia-Pacific region.

China Lubricants Market Report Scope

By Product Type

| Automotive Engine Oil |

| Industrial Engine Oil |

| Transmission Fluids |

| Gear Oil |

| Brake Fluids |

| Hydraulic Fluids |

| Greases |

| Process Oil (Including Rubber Process Oil and White Oil) |

| Metalworking Fluids |

| Turbine Oil |

| Transformer Oil |

| Other Product Types |

By End-user Industry

| Automotive | Passenger Vehicles |

| Commercial Vehicles | |

| Two-Wheelers | |

| Marine | |

| Aerospace | |

| Heavy Equipment | Construction |

| Mining | |

| Agriculture | |

| Industrial | Power Generation |

| Metallurgy and Metalworking | |

| Textiles | |

| Oil and Gas | |

| Other End-Use Industries |

By Base Stock Type

| Mineral Oil-Based Lubricants |

| Synthetic Lubricants |

| Semi-Synthetic Lubricants |

| Bio-Based Lubricants |

| By Product Type | Automotive Engine Oil | |

| Industrial Engine Oil | ||

| Transmission Fluids | ||

| Gear Oil | ||

| Brake Fluids | ||

| Hydraulic Fluids | ||

| Greases | ||

| Process Oil (Including Rubber Process Oil and White Oil) | ||

| Metalworking Fluids | ||

| Turbine Oil | ||

| Transformer Oil | ||

| Other Product Types | ||

| By End-user Industry | Automotive | Passenger Vehicles |

| Commercial Vehicles | ||

| Two-Wheelers | ||

| Marine | ||

| Aerospace | ||

| Heavy Equipment | Construction | |

| Mining | ||

| Agriculture | ||

| Industrial | Power Generation | |

| Metallurgy and Metalworking | ||

| Textiles | ||

| Oil and Gas | ||

| Other End-Use Industries | ||

| By Base Stock Type | Mineral Oil-Based Lubricants | |

| Synthetic Lubricants | ||

| Semi-Synthetic Lubricants | ||

| Bio-Based Lubricants | ||

Key Questions Answered in the Report

What is the current volume of the China lubricants market?

China lubricants market size reached 7.67 billion liters in 2026 and is projected to reach 7.75 billion liters by 2031.

How fast is the market expected to grow?

The market posts a very low 0.19% CAGR from 2026 to 2031 as electric-vehicle adoption offsets industrial gains.

Which product category will grow the quickest?

Transmission Fluids are forecast to rise at 1.03% CAGR, supported by automatic transmissions and e-axle requirements.

Which end-user industry shows the highest growth potential?

Heavy Equipment is the fastest-growing end-user segment with a 1.10% CAGR driven by infrastructure investment and mining.

What drives the shift toward synthetic lubricants?

Longer OEM warranties, dual-carbon regulations, and performance needs push synthetic lubricants to a 1.34% CAGR through 2031.

How does electric-vehicle adoption affect lubricant demand?

Each BEV removes 4-5 liters of annual engine-oil need, leading to declining automotive lubricant volumes despite new specialty fluid opportunities.

Page last updated on: