Market Size of ASEAN Waste Management Industry

| Study Period | 2020 - 2029 |

| Base Year For Estimation | 2023 |

| Forecast Data Period | 2024 - 2029 |

| Historical Data Period | 2020 - 2022 |

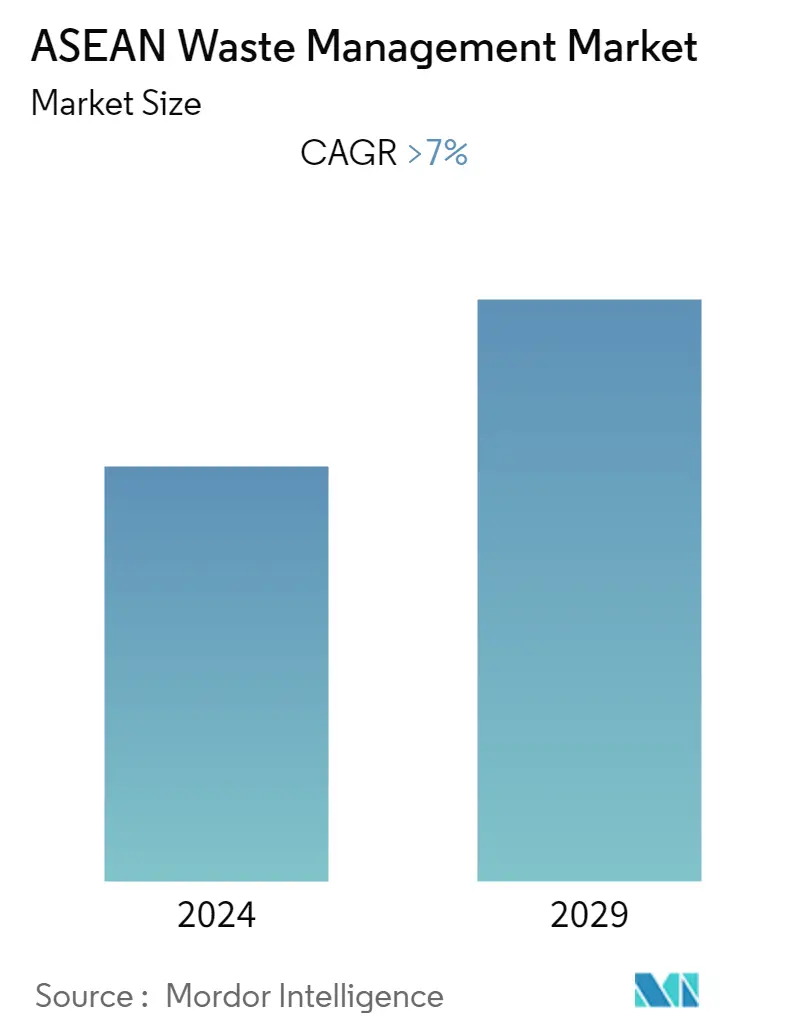

| CAGR | > 7.00 % |

| Market Concentration | Low |

Major Players

*Disclaimer: Major Players sorted in no particular order |

Need a report that reflects how COVID-19 has impacted this market and its growth?

ASEAN Waste Management Market Analysis

The size of the ASEAN Waste Management Market is valued at about USD 18 billion in the current year and is anticipated to register a CAGR of over 7% during the forecast period. ASEAN's waste management is growing at a healthy rate owing to the fast-growing economies with the growing population, increased economic activity, urbanization, and industrialization.

- In recent years, Malaysia, Vietnam, Thailand, and Indonesia have become the top destinations in Southeast Asia for the inflow of both legal and illegal waste from the US, Japan, the UK, the European Union (EU) and other countries. The sudden and sharp increase in waste imports has proved challenging for the countries in Southeast Asia, which have responded by returning containers of waste to the countries of origin, announcing bans on the import of some types of waste and tightening regulations and increasing enforcement. These measures resulted in a reduction in the amount of waste entering their countries.

- Despite current efforts, illegal waste continues to reach Southeast Asian countries. Uncontrolled and illicit waste flows are frequently hidden behind controlled or legal transboundary movements of goods - the boundaries between licit and illicit waste trafficking activities can be very thin, and the activities, actors, and modes of operation involved frequently overlap. The impact is magnified when destination countries lack enforcement capacity and/or adequate sanctions for illegal waste trade activities.

- With the increased waste generation in the region, open dumping and open burning of waste are highly prevalent in the majority of the ASEAN countries. Composting and anaerobic digestion of organic wastes, and recovery of valuable recyclables such as plastic, metal, and paper are quite common in ASEAN. Recycling, however, is more in the hands of the informal sector. Nevertheless, Singapore stands as an exception to other ASEAN countries, as it has a sound and well-structured waste management system in place. Singapore opts for waste to energy (WTE) through incineration as the major waste management option, due to its limited land resources.

- Southeast Asia's current production and consumption trajectory, as a result of its rapid growth, is increasingly putting a strain on the environment. Measures to contain the pandemic have exacerbated environmental pressures due to increased volumes of medical waste, plastics, and packaging as a result of the e-commerce boom, as well as other resource stresses. As the region's countries embark on their green recovery agenda in the aftermath of COVID-19, there is an urgent need to shift from the linear economic model of "take, make, waste" to a circular system. A circular economy is based on three principles: (i) reducing waste and pollution; (ii) reusing products and materials; and (iii) regenerating natural ecosystems.

- The region has created a framework that emphasises the importance of trade, technological innovation, and financial markets in accelerating circular transformation. The five strategic priorities outlined below will pave the way for a smooth transition to a circular economy. Standardization and mutual recognition of circular products and services.

- ASEAN countries must review existing arrangements in various sectors and harmonise standards in order to enable the trade of circular products and services and facilitate value chain integration. To mainstream and scale circularity, a widely accepted definition of circular products and services should be established through the development of a taxonomy, which can help businesses reduce compliance costs and unnecessary regulatory burdens.