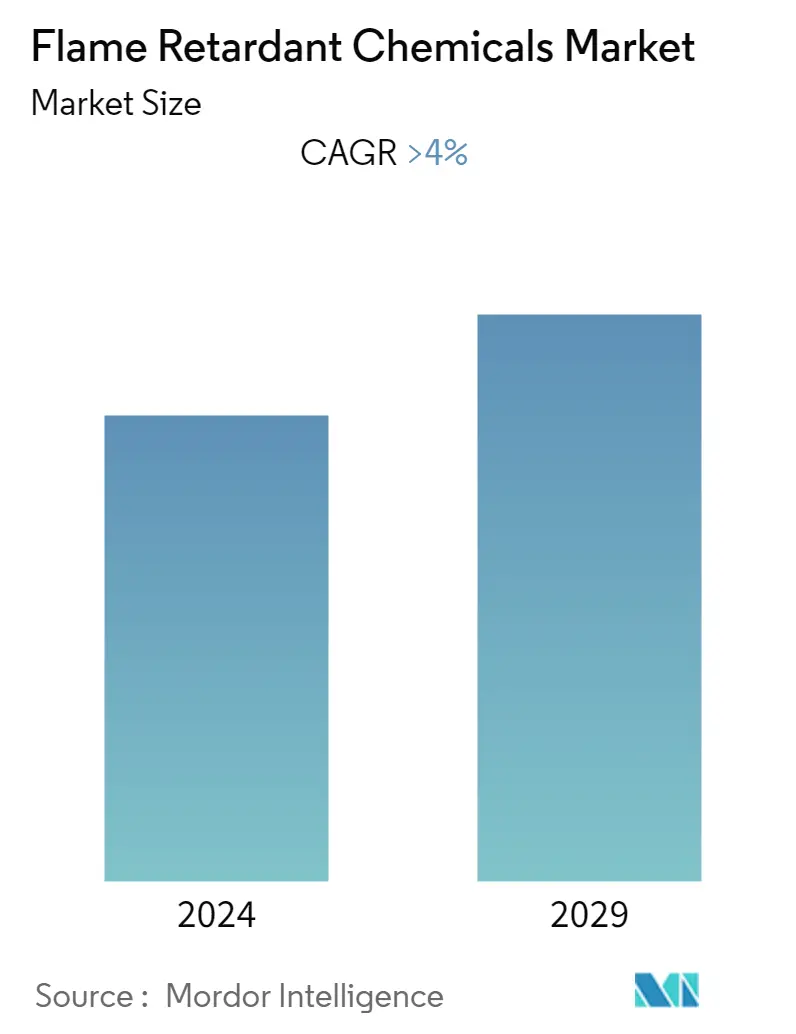

阻燃化学品市场规模

| 研究期 | 2019 - 2029 |

| 估计的基准年 | 2023 |

| CAGR | > 4.00 % |

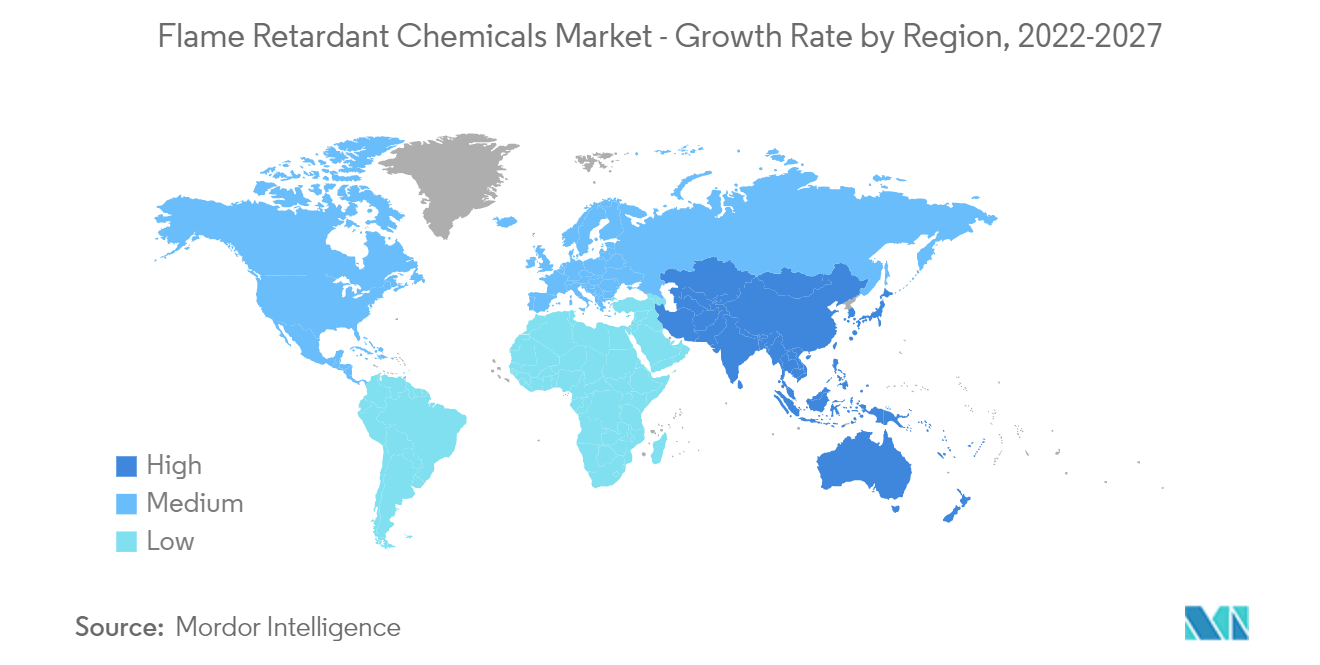

| 增长最快的市场 | 亚太地区 |

| 最大的市场 | 亚太地区 |

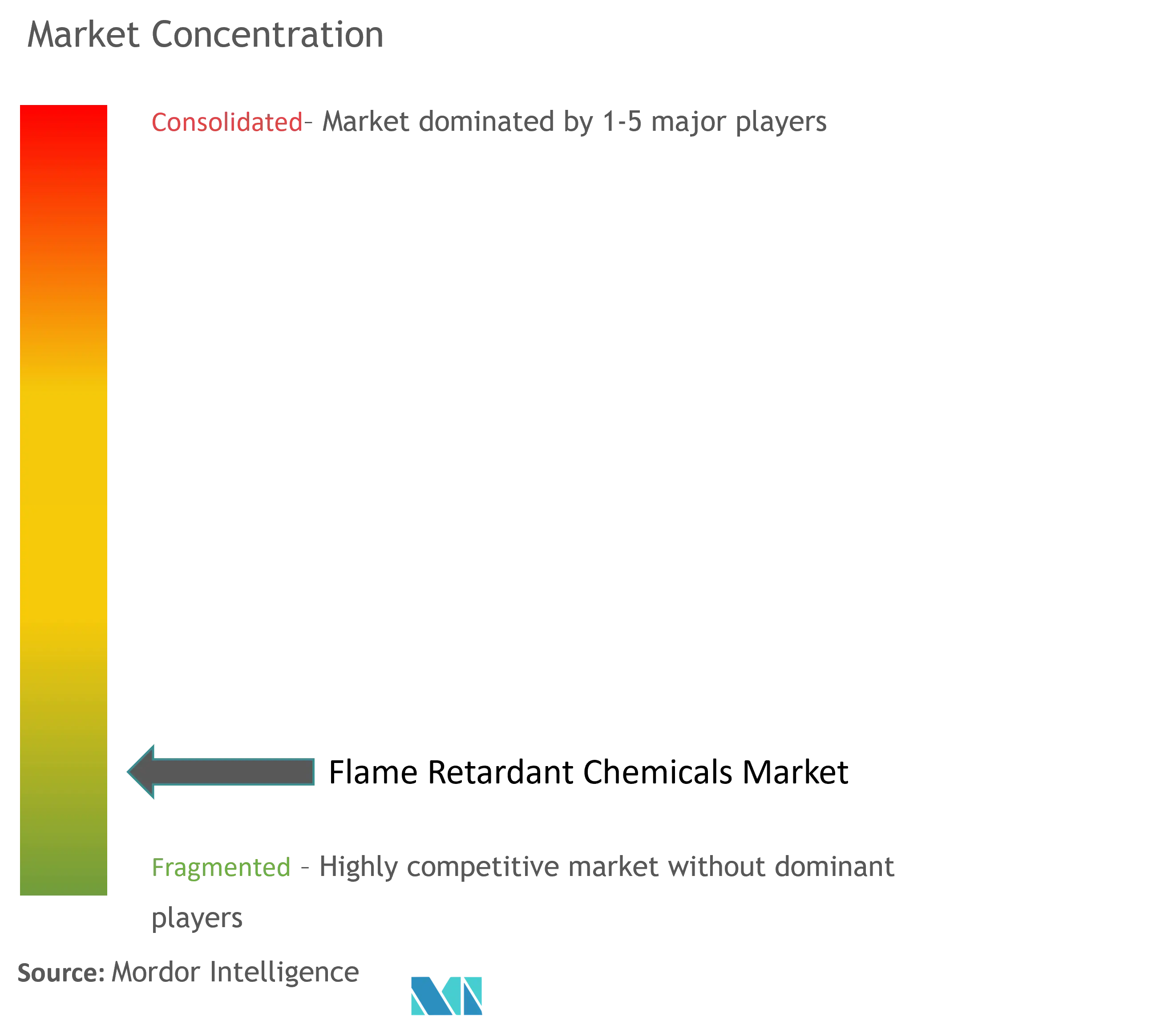

| 市场集中度 | 低的 |

主要参与者

*免责声明:主要玩家排序不分先后 |

我们可以帮忙吗?

阻燃化学品市场分析

预计阻燃化学品市场在预测期内的复合年增长率将超过 4%。

COVID-19对2020年市场产生了负面影响。然而,建筑行业正在快速复苏,预计未来几年将出现增长,这将刺激阻燃化学品市场的需求。

- 短期内,亚太地区基础设施活动的增加、建筑安全标准的提高以及消费电气和电子产品制造的增长预计将推动市场的增长。

- 有关卤化阻燃剂的环境和健康问题以及氢氧化物不适合高温应用预计将阻碍市场的增长。

- 人们对环保阻燃剂的认识不断提高,以及对非卤化阻燃剂的积极研发,预计将成为市场机会。

- 由于该地区的建筑活动频繁,亚太地区在全球市场中占据主导地位。

阻燃化学品市场趋势

建筑施工领域将主导市场

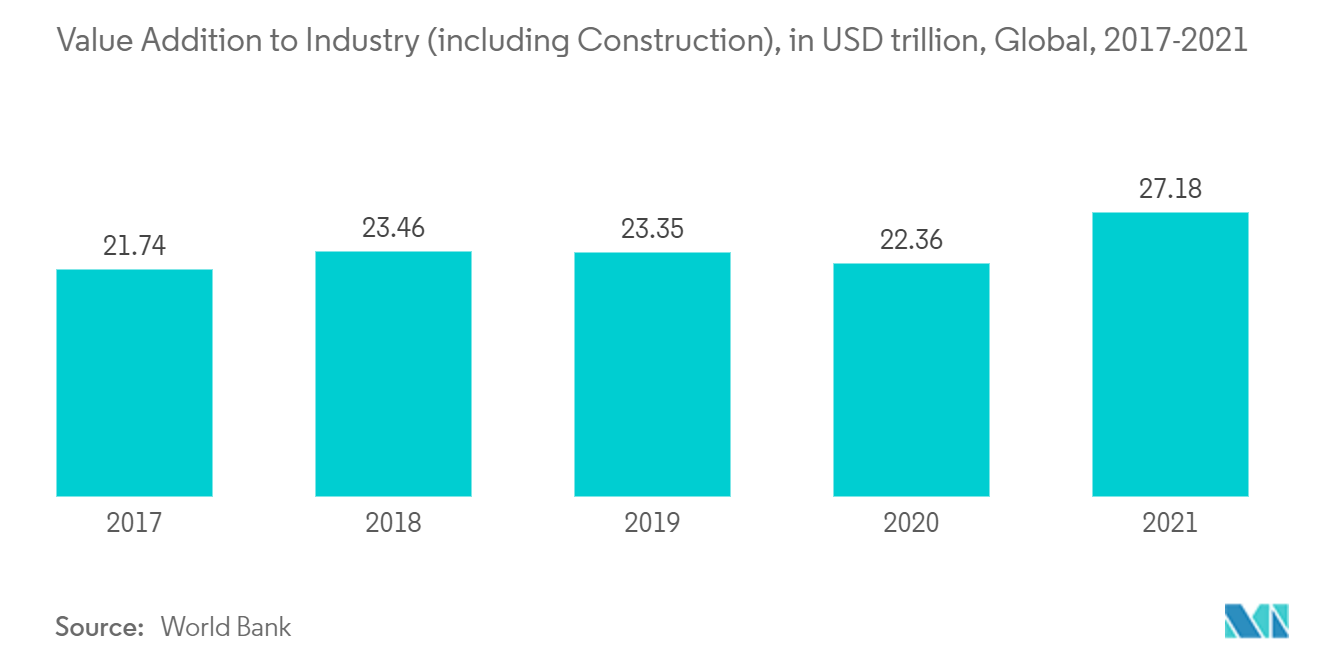

- 家庭火灾是造成人员伤亡的最大原因之一。由于严格的消防安全法规,阻燃剂被用于建筑材料和产品中。在建筑物中,阻燃剂主要用于结构保温。住宅和其他建筑物中使用隔热材料来保持舒适的温度并节省能源。

- 预计预测期内中国建筑业整体将实际增长4.6%。中国国家统计局发布的报告显示,2022年上半年建筑业投资增长6.7%。

- 印度政府于2021年启动国家基础设施管道(NIP),计划投资1.4万亿美元,其中可再生能源占比24%,公路和高速公路占比19%,铁路占比13%,铁路占比16%。城市基础设施。

- 美国拥有庞大的建筑业,在商业、工业、机构、住宅、基础设施、能源和公用事业建设中发挥着重要作用。 2022 年 1 月的建筑支出经季节调整后的年增长率估计为 16,772 亿美元。此外,美国 2 月份建筑支出增长 1.3%,而 2022 年 1 月经季节性调整后的年增长率为 1.677 万亿美元。

- 预计未来几年中东和非洲等地区的全球建筑业增长速度将会加快。这反映了沙特阿拉伯、阿拉伯联合酋长国和卡塔尔对建筑和基础设施的巨额投资。为了减少对石油经济的依赖,沙特阿拉伯启动了各种建设和城市发展项目,作为2030年愿景的一部分。

- 德国拥有欧洲最大的建筑业。该国的建筑业一直在缓慢增长,主要是由新住宅建设活动的增加推动的。预计该国的非住宅和商业建筑在预测期内将出现显着的增长前景。这一增长可能受到较低利率、实际可支配收入增加以及欧盟和德国政府大量投资的支持。

亚太地区将主导市场

- 亚太地区在全球市场份额中占据主导地位。在亚太地区,中国和印度由于在建筑、交通等关键领域的大量投资,预计将主导市场的增长。

- 中国航空航天业在经历前几年的大幅下滑后,预计将于 2022 年恢复盈利。中国民航局(CAAC)预计,航空业国内运输量将恢复至疫情前水平的85%左右。

- 印度亚太航空中心 (CAPA) 在一份题为2022 年印度航空公司展望的报告中指出,预计 2022 年国内航空运输量将激增 52%,国际航空运输量将激增 60%。 2022财年,全国航空客运量为4822万人次。此外,2021 年印度旅客通过航空运输的支出估计为 1,360 亿美元。政府正试图通过增加该国机场的数量来满足空中交通的需求。

- 根据日本汽车经销商协会的数据,660 CC 以上的新车销量下滑 2.9%,至 2,795,818 辆。日本轻型汽车和摩托车协会报告称,同年微型汽车销量下降 3.8%,至 1,652,522 辆。

- 根据国际贸易管理局的数据,2021年,韩国本土医疗器械产值达112.57亿美元。医疗器械出口86.29亿美元,自美国进口53.53亿美元。

- 随着2030年国家航空航天工业蓝图的实施,马来西亚航空航天工业的增长势头强劲。过去十年,该行业已经以平均5%的速度增长。空客预计马来西亚仍将是其供应链中的焦点,在该地区对飞机的强劲需求的推动下,该公司希望到 2023 年将其供应、采购和 MRO 业务的价值增加到每年 5.5 亿美元。航空航天业的这种压倒性情况预计将有助于低摩擦涂料市场在预测期内实现非常健康的增长率。

阻燃化学品行业概况

阻燃化学品市场是一个分散的市场,前五名参与者在所研究的市场中占据了相当大的份额。主要企业(排名不分先后)包括ICL集团、朗盛、巴斯夫、雅保公司、江苏约科科技有限公司。

阻燃化学品市场领导者

-

ICL Group

-

LANXESS

-

Albemarle Corporation

-

BASF SE

-

Jiangsu Yoke Technology Co. Ltd

*免责声明:主要玩家排序不分先后

阻燃化学品市场新闻

- 2022年9月,朗盛推出了新型磷基阻燃剂,该阻燃剂具有热稳定性和机械稳定性等独特性能,并且与工程塑料相容。

- 2022 年 7 月,巴斯夫欧洲公司与消防产品公司 THOR GmBH 合作。这一战略举措将加强非卤阻燃添加剂的产品组合。

- 2022年4月,巴斯夫推出了面向电子行业的全新阻燃产品系列。这些是具有独特耐腐蚀性能的聚邻苯二甲酰胺。

阻燃化学品市场报告 - 目录

1. 介绍

1.1 研究假设

1.2 研究范围

2. 研究方法论

3. 执行摘要

4. 市场动态

4.1 司机

4.1.1 增加亚太地区的基础设施活动

4.1.2 建筑施工安全标准的提高

4.1.3 消费电气和电子产品制造业的崛起

4.2 限制

4.2.1 关于溴化和卤化阻燃剂的环境和健康问题

4.3 行业价值链分析

4.4 波特五力分析

4.4.1 供应商的议价能力

4.4.2 消费者的议价能力

4.4.3 新进入者的威胁

4.4.4 替代产品和服务的威胁

4.4.5 竞争程度

4.5 监管政策分析

4.6 原材料分析

4.7 技术快照

5. 市场细分

5.1 产品类别

5.1.1 无卤阻燃化学品

5.1.1.1 无机

5.1.1.1.1 氢氧化铝

5.1.1.1.2 氢氧化镁

5.1.1.1.3 硼化合物

5.1.1.2 磷

5.1.1.3 氮

5.1.1.4 其他产品类型

5.1.2 卤化阻燃剂化学品

5.1.2.1 溴化物

5.1.2.2 氯化物

5.2 最终用户行业

5.2.1 电气和电子

5.2.2 建筑物和建筑

5.2.3 运输

5.2.4 纺织品和家具

5.3 地理

5.3.1 亚太

5.3.1.1 中国

5.3.1.2 印度

5.3.1.3 日本

5.3.1.4 韩国

5.3.1.5 澳大利亚和新西兰

5.3.1.6 亚太其他地区

5.3.2 北美

5.3.2.1 美国

5.3.2.2 加拿大

5.3.2.3 墨西哥

5.3.2.4 北美其他地区

5.3.3 欧洲

5.3.3.1 德国

5.3.3.2 英国

5.3.3.3 意大利

5.3.3.4 法国

5.3.3.5 西班牙

5.3.3.6 欧洲其他地区

5.3.4 南美洲

5.3.4.1 巴西

5.3.4.2 阿根廷

5.3.4.3 南美洲其他地区

5.3.5 中东和非洲

5.3.5.1 沙特阿拉伯

5.3.5.2 南非

5.3.5.3 卡塔尔

5.3.5.4 中东和非洲其他地区

6. 竞争格局

6.1 并购、合资、合作和协议

6.2 市场排名分析

6.3 领先企业采取的策略

6.4 公司简介

6.4.1 Albemarle Corporation

6.4.2 Apexical Inc.

6.4.3 BASF SE

6.4.4 Clariant

6.4.5 DAIHACHI CHEMICAL INDUSTRY CO. LTD

6.4.6 DIC CORPORATION

6.4.7 Dow

6.4.8 Eti Maden

6.4.9 ICL Group

6.4.10 Italmatch Chemicals SpA

6.4.11 J.M. Huber Corporation

6.4.12 Jiangsu Jacques Technology Co. Ltd

6.4.13 Kemipex

6.4.14 LANXESS

6.4.15 MPI Chemie BV

6.4.16 Nabaltec AG

6.4.17 Nyacol Nano Technologies Inc.

6.4.18 RIN KAGAKU KOGYO Co. Ltd

6.4.19 RTP Company

6.4.20 Sanwa Chemical Co. Ltd

6.4.21 Shandong Brother Sci. & Tech. Co. Ltd

6.4.22 Thor

6.4.23 Tor Minerals International Inc.

6.4.24 Tosoh Corporation

6.4.25 UFP Industries Inc.

7. 市场机会和未来趋势

7.1 人们对环保阻燃剂的认识不断提高

7.2 积极研发无卤阻燃剂

阻燃化学品行业细分

阻燃化学品是添加或以其他方式掺入化合物中以减缓火势蔓延或防止火灾的化合物,主要用于建筑材料、电子和电气设备、家具和运输。阻燃化学品市场按产品类型、最终用户行业和地理位置进行细分。按产品类型划分,市场分为非卤化阻燃化学品和卤化阻燃化学品。按最终用户行业划分,市场分为电气和电子、建筑、交通、纺织和家具。该报告还涵盖了主要地区15个国家阻燃化学品市场的市场规模和预测。对于每个细分市场,市场规模和预测都是根据收入(百万美元)进行的。

| 产品类别 | ||||||||||||||||

| ||||||||||||||||

|

| 最终用户行业 | ||

| ||

| ||

| ||

|

| 地理 | ||||||||||||||

| ||||||||||||||

| ||||||||||||||

| ||||||||||||||

| ||||||||||||||

|

阻燃化学品市场研究常见问题解答

目前阻燃化学品市场规模有多大?

阻燃化学品市场预计在预测期内(2024-2029)复合年增长率将超过 4%

谁是阻燃化学品市场的主要参与者?

ICL Group、LANXESS、Albemarle Corporation、BASF SE、Jiangsu Yoke Technology Co. Ltd 是阻燃化学品市场的主要公司。

阻燃化学品市场增长最快的地区是哪个?

预计亚太地区在预测期内(2024-2029 年)复合年增长率最高。

哪个地区在阻燃化学品市场中占有最大份额?

2024年,亚太地区将占据阻燃化学品市场最大的市场份额。

该阻燃化学品市场涵盖哪些年份?

该报告涵盖了阻燃化学品市场的历史市场规模:2019年、2020年、2021年、2022年和2023年。该报告还预测了阻燃化学品市场的多年市场规模:2024年、2025年、2026年、2027年、2028年和2029年。

阻燃剂行业报告

Mordor Intelligence™ 行业报告创建的 2024 年阻燃剂市场份额、规模和收入增长率统计数据。阻燃剂分析包括 2029 年的市场预测展望和历史概述。获取此行业分析的样本(免费下载 PDF 报告)。