弹性体市场规模

| 研究期 | 2019 - 2029 |

| 估计的基准年 | 2023 |

| CAGR | > 5.00 % |

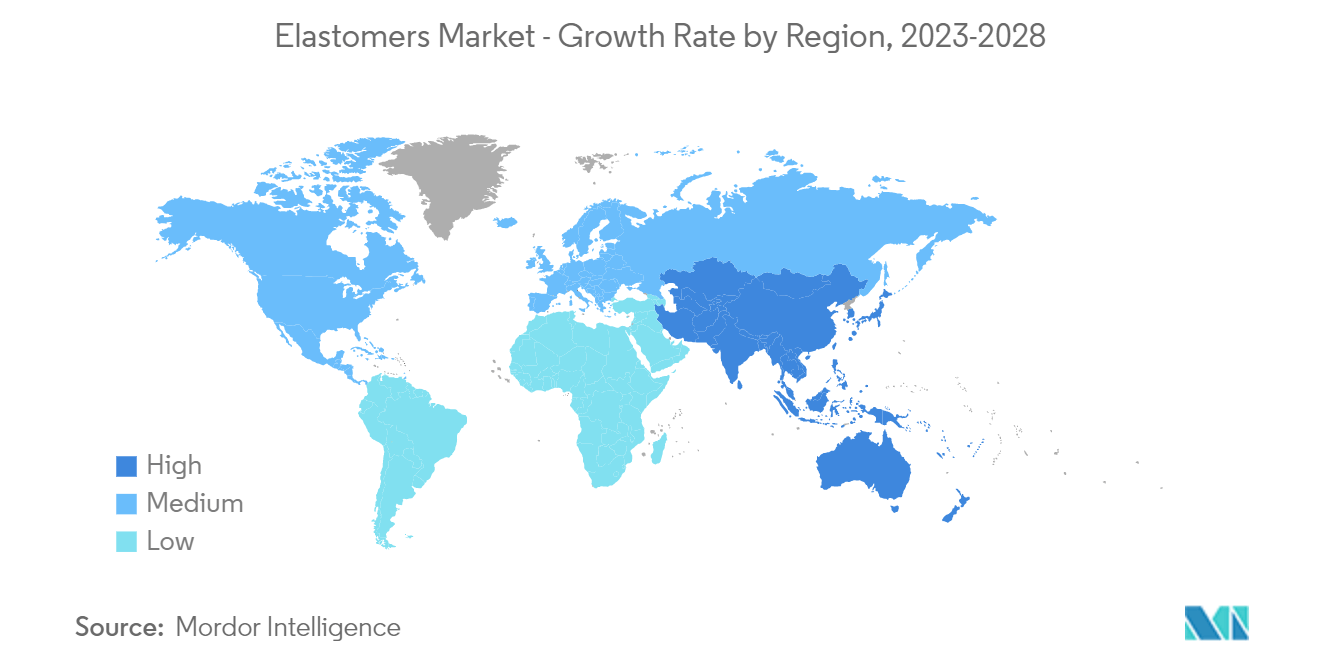

| 增长最快的市场 | 亚太 |

| 最大的市场 | 北美 |

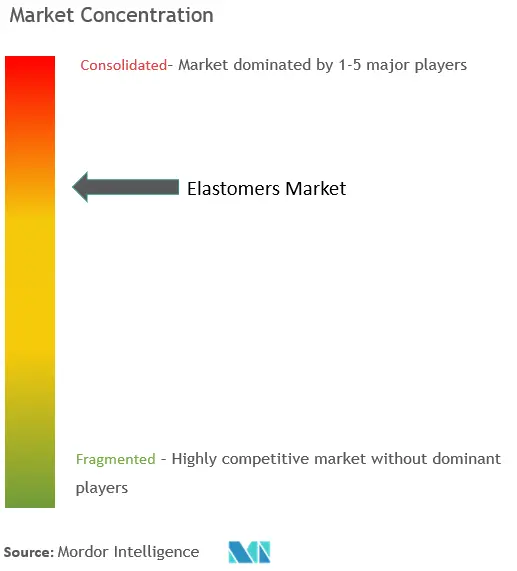

| 市场集中度 | 高的 |

主要参与者

*免责声明:主要玩家排序不分先后 |

我们可以帮忙吗?

弹性体市场分析

预计全球弹性体市场在预测期内的复合年增长率将超过 5%。 2020年,市场受到了COVID-19的负面影响。不过,目前估计市场已达到大流行前的水平,预计未来将稳定增长。

- 该市场预计将增长,因为汽车行业需要更多的弹性体,建筑行业需要更多的弹性体来制造粘合剂、管材、涂料和其他材料等。

- 对弹性体在医学中的使用方式的生物相容性担忧可能会减缓市场的增长。

- 机会可能来自于投入更多精力生产生物基产品并将其更多地用于制造医疗器械。

- 亚太地区是世界上最大的市场,印度、中国等国家使用最多。

弹性体市场趋势

汽车领域的使用量不断增加

- 弹性体用于皮带和软管、波纹管、垫圈、车内声音管理、地板和仪表板表皮。此外,在汽车之外,它还可用于轮胎(基胎、胎侧和胎面)、电线、电缆以及几乎所有汽车部件的涂层。

- 汽车工业的发展在一定程度上是因为制造了更多的汽车,并且每辆汽车使用了更多的聚丙烯。使用热塑性烯烃 (TPO) 化合物代替柔性 PVC 来覆盖仪表板和其他内饰用途。

- 汽车和运输行业大量使用热塑性弹性体 (TPE),因为它们重量轻、易于加工、为设计人员提供了更多自由、用途广泛且可以回收利用。而热固性橡胶是弹性体的一种,主要用于制造汽车轮胎。

- 全球消耗的所有 TPE 产品中约有 40% 用于汽车制造。因此,汽车和运输行业及其零部件和OEM供应商的发展是未来TPE需求的重要指标。

- 2021年全球汽车产量超过8000万辆,与上年相比增长约3%。因此,这对弹性体市场的增长产生了积极影响。

- TPE 市场正在不断增长,因为汽车行业需要更轻的材料来提高汽车的效率,并为设计师提供更多的制造选择。高性能热塑性弹性体使制造商能够设计产品并赋予其与钢相同的强度。这有助于减轻整个物体的重量并控制温室气体排放。

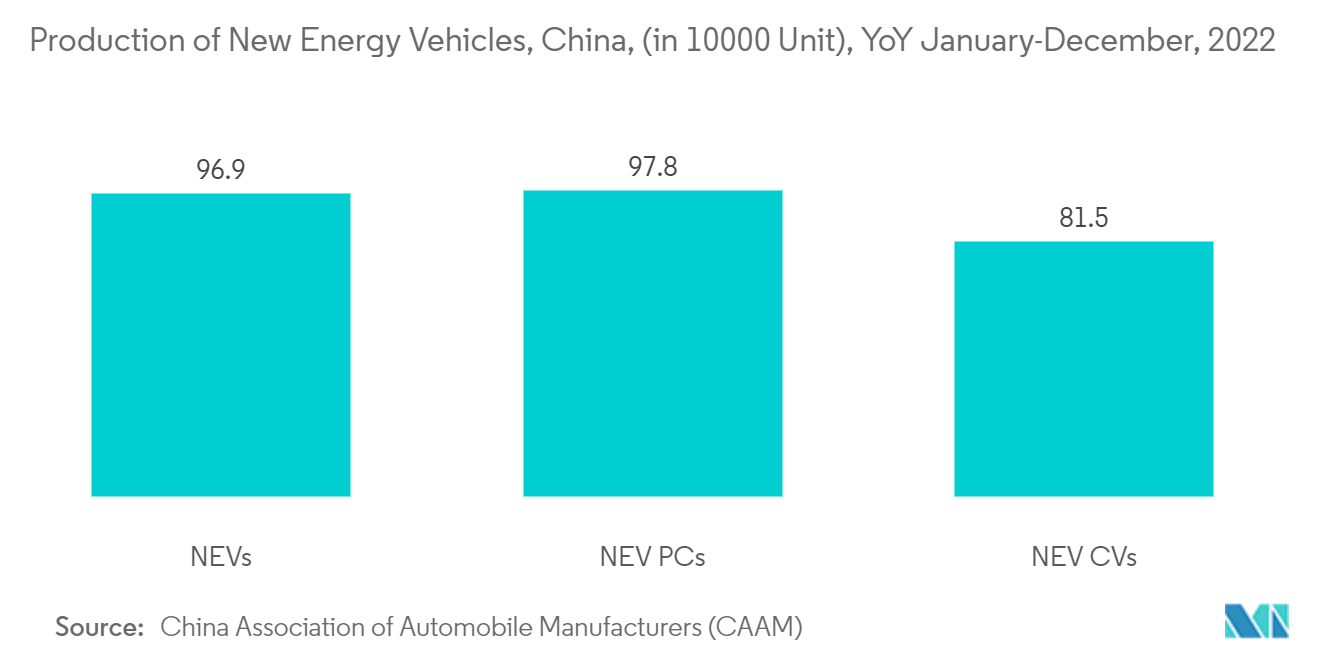

- 中国是电动汽车市场的全球领导者。据中国汽车工业协会统计,2022年12月,中国新能源汽车产量同比增长96.9%,电动汽车市场的不断扩大预计将增加对弹性体的需求。

- 因此,由于上述因素,预计弹性体市场在预测期内将大幅增长。

亚太地区主导市场

- 亚太地区预计将成为市场的佼佼者,因为中国、印度、台湾、泰国和印度尼西亚等国家正在制造和销售更多的汽车。

- 在建筑、汽车、电气电子和制鞋行业,中国是弹性体的最大市场。

- 汽车工业是弹性体的主要消费者之一。中国电动汽车市场大幅扩张,新型电动汽车销量大幅增长。 2021年中国电动汽车销量达330万辆,较2020年的130万辆增长154%。因此,对轮胎、皮带、软管等汽车零部件的需求增加等因素对弹性体的市场需求产生积极影响。

- 此外,印度的汽车工业正在崛起。该国乘用车产量大幅增长。例如,2021-2022财年乘用车产量达到3,650,698辆,比2020-21财年增长19%。

- 弹性体用于制造各种建筑材料,例如粘合剂、密封剂和填缝剂。据国家统计局数据,2021年全国建筑工程产值25.92万亿元,较2020年增长11%以上,市场需求增加。

- 韩国统计局还表示,2021年,国内外当地建筑商收到的建筑订单总额为2459亿美元。这与去年相比有很大的跃升。

- 此外,预计将在日本举办的活动将推动那里的建筑业。东京将于2020年举办奥运会(因疫情推迟至2021年),大阪将于2025年举办世博会。

- 由于这些和其他因素,预计亚太地区将在未来几年引领弹性体市场。

弹性体行业概况

弹性体市场本质上是部分整合的。该市场的一些主要参与者包括巴斯夫股份公司、陶氏化学、科思创股份公司、可乐丽有限公司和亨斯曼国际有限责任公司等(排名不分先后)。

弹性体市场领导者

-

BASF SE

-

Dow

-

Convestro AG

-

KURARAY CO., LTD.

-

Huntsman International LLC

*免责声明:主要玩家排序不分先后

弹性体市场新闻

- 2023年2月:可乐丽株式会社宣布其新的异戊二烯相关工厂竣工,预计很快将分阶段投入运营。新的泰国工厂预计将通过增强全球供应体系并满足全球对 3-甲基-1.5-戊二醇 (MPD)、SEPTON 氢化苯乙烯嵌段共聚物 (HSBC) 和 GENESTAR 耐热材料不断增长的需求,帮助异戊二烯相关行业蓬勃发展聚酰胺-9T。

- 2022 年 7 月:科思创两座新生产工厂在上海破土动工。该公司建立了生产聚氨酯分散体和弹性体的新生产线,以满足不断增长的需求。

弹性体市场报告 - 目录

1. 介绍

1.1 研究假设

1.2 研究范围

2. 研究方法论

3. 执行摘要

4. 市场动态

4.1 司机

4.1.1 汽车行业需求不断增长

4.1.2 建筑业需求不断增长

4.2 限制

4.2.1 一些医用弹性体的生物相容性问题

4.2.2 其他限制

4.3 行业价值链分析

4.4 波特五力分析

4.4.1 供应商的议价能力

4.4.2 消费者的议价能力

4.4.3 新进入者的威胁

4.4.4 替代产品和服务的威胁

4.4.5 竞争程度

5. 市场细分(市场规模价值)

5.1 产品类别

5.1.1 热固性弹性体

5.1.2 热塑性弹性体

5.2 应用

5.2.1 汽车

5.2.2 运动的

5.2.3 电子产品

5.2.4 工业的

5.2.5 粘合剂

5.2.6 其他应用

5.3 地理

5.3.1 亚太

5.3.1.1 中国

5.3.1.2 印度

5.3.1.3 日本

5.3.1.4 韩国

5.3.1.5 亚太其他地区

5.3.2 北美

5.3.2.1 美国

5.3.2.2 加拿大

5.3.2.3 墨西哥

5.3.2.4 北美其他地区

5.3.3 欧洲

5.3.3.1 德国

5.3.3.2 英国

5.3.3.3 意大利

5.3.3.4 法国

5.3.3.5 欧洲其他地区

5.3.4 南美洲

5.3.4.1 巴西

5.3.4.2 阿根廷

5.3.4.3 南美洲其他地区

5.3.5 中东和非洲

5.3.5.1 沙特阿拉伯

5.3.5.2 南非

5.3.5.3 中东和非洲其他地区

6. 竞争格局

6.1 并购、合资、合作和协议

6.2 市场占有率(%)**/排名分析

6.3 领先企业采取的策略

6.4 公司简介

6.4.1 Ace Elastomer

6.4.2 Avient Corporation

6.4.3 Arkema

6.4.4 BASF SE

6.4.5 Exxon Mobil Corporation

6.4.6 Covestro AG

6.4.7 DingZing Advanced Materials Inc.

6.4.8 Dow

6.4.9 HEXPOL AB

6.4.10 Huntsman International LLC

6.4.11 KURARAY CO., LTD.

6.4.12 Miracll Chemicals Co., Ltd.

6.4.13 Sirmax S.p.A

6.4.14 Suzhou Austin Novel Materials Technology Co. Ltd.

6.4.15 Trinseo

6.4.16 The Lubrizol Corporation

7. 市场机会和未来趋势

7.1 将重点转向生物基产品的开发

7.2 在医疗器械制造中的应用不断增加

弹性体行业细分

弹性体是一种高摩尔质量的聚合材料,具有弹性特性,使其在变形后能够恢复原来的形状。热固性弹性体广泛用于轮胎橡胶的生产,热塑性弹性体用于通过注射成型制造密封剂、软管和内胎。弹性体市场按产品类型、应用和地理位置进行细分。按产品类型,市场分为热固性弹性体和热塑性弹性体。按应用划分,市场分为汽车、体育、电子、工业、粘合剂和其他应用。该报告还涵盖了主要地区15个国家的市场规模和市场预测。对于每个细分市场,市场规模和预测都是根据收入(百万美元)进行的。

| 产品类别 | ||

| ||

|

| 应用 | ||

| ||

| ||

| ||

| ||

| ||

|

| 地理 | ||||||||||||

| ||||||||||||

| ||||||||||||

| ||||||||||||

| ||||||||||||

|

弹性体市场研究常见问题解答

目前的弹性体市场规模有多大?

预计在预测期内(2024-2029 年),弹性体市场的复合年增长率将超过 5%

谁是弹性体市场的主要参与者?

BASF SE、Dow、Convestro AG、KURARAY CO., LTD.、Huntsman International LLC 是弹性体市场运营的主要公司。

弹性体市场增长最快的地区是哪个?

预计亚太地区在预测期内(2024-2029 年)复合年增长率最高。

哪个地区在弹性体市场中占有最大份额?

2024年,北美将占据弹性体市场最大的市场份额。

该弹性体市场涵盖哪些年份?

该报告涵盖了以下年份的弹性体市场历史市场规模:2019年、2020年、2021年、2022年和2023年。该报告还预测了以下年份的弹性体市场规模:2024年、2025年、2026年、2027年、2028年和2029年。

弹性体行业报告

Mordor Intelligence™ 行业报告创建的 2024 年弹性体市场份额、规模和收入增长率统计数据。弹性体分析包括 2029 年的市场预测展望和历史概述。获取此行业分析的样本(免费下载 PDF 报告)。