丙烯酸市场规模

| 研究期 | 2019 - 2029 |

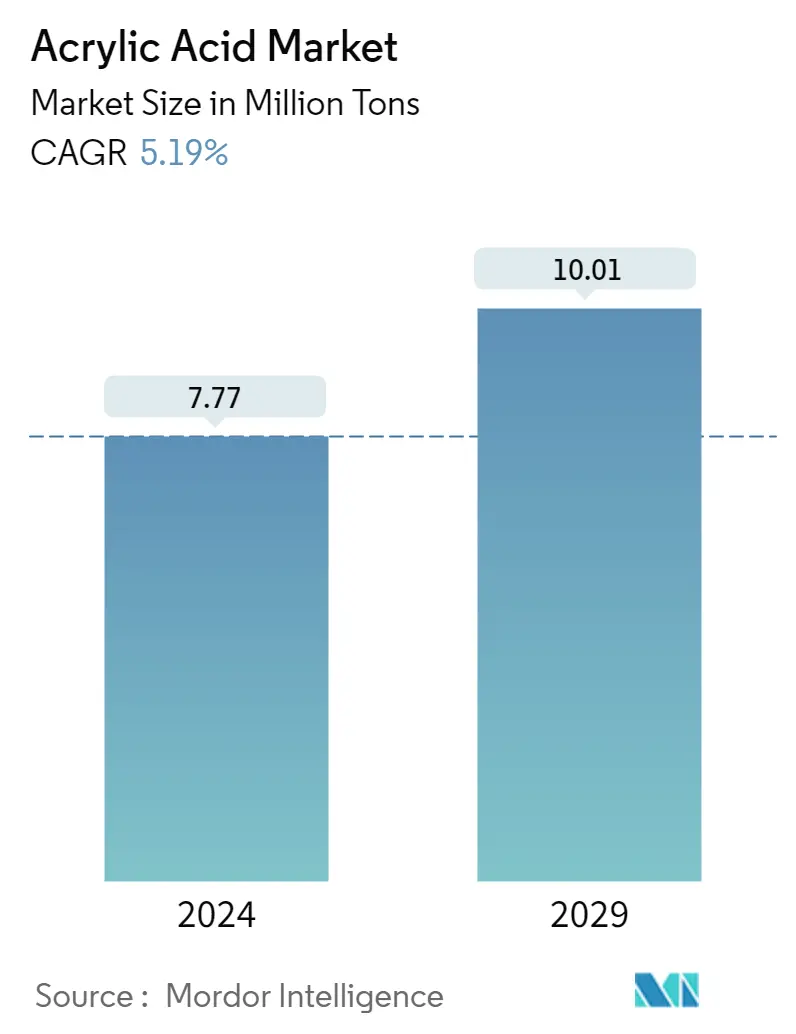

| 市场容量 (2024) | 777万吨 |

| 市场容量 (2029) | 1001万吨 |

| CAGR(2024 - 2029) | 5.19 % |

| 增长最快的市场 | 亚太地区 |

| 最大的市场 | 亚太地区 |

主要参与者

*免责声明:主要玩家排序不分先后 |

我们可以帮忙吗?

丙烯酸市场分析

丙烯酸市场规模预计到2024年为777万吨,预计到2029年将达到1001万吨,在预测期内(2024-2029年)复合年增长率为5.19%。

市场受到 COVID-19 大流行的负面影响。然而,2021年,由于人们对个人卫生和清洁环境的认识和意识增强,对洗衣护理产品的需求有所增加。丙烯酸用于生产液体洗衣粉,刺激了丙烯酸市场的需求。

- 短期内,丙烯酸类高吸水性聚合物的应用不断增加以及化学合成的使用不断增加预计将推动市场的增长。

- 与丙烯酸相关的健康危害可能会阻碍市场的增长。

- 对生物基聚合物的需求不断增长可能会成为预测期内市场增长的机会。

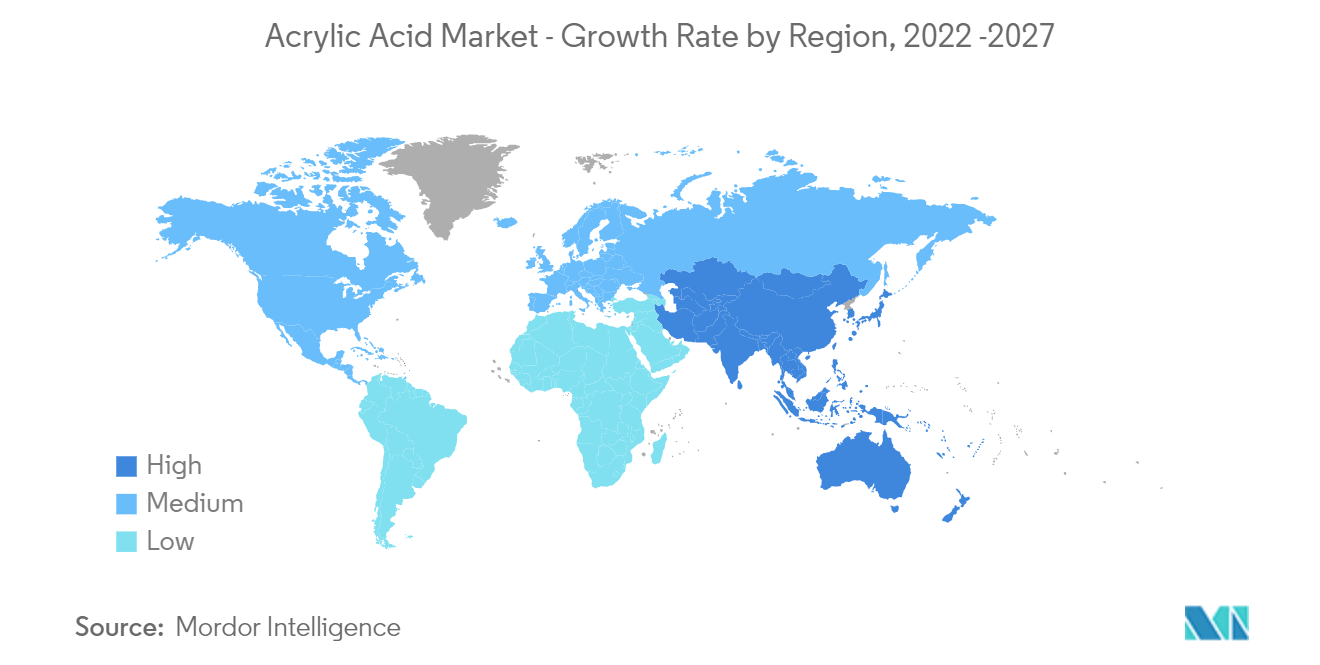

- 亚太地区占据最大的市场份额,并且很可能在预测期内主导市场。

丙烯酸市场趋势

增加油漆和涂料应用中的使用量

- 丙烯酸越来越多地用于制造丙烯酸酯,其用于各种应用,包括油漆和涂料。

- 丙烯酸用于建筑涂料、原始设备制造商产品的面漆,包括汽车 (OEM) 和修补漆以及特殊用途涂料。

- 丙烯酸粉末涂料已作为透明涂层应用于车身上。尽管它是许多应用的理想解决方案,但固化是在烤箱中的高温下实现的。因此,它并不普遍适用(例如,木材和塑料的涂漆)。

- 建筑涂料旨在保护和装饰表面特征,用于覆盖建筑物和房屋。大多数指定用于特定用途,例如屋顶涂料、墙面涂料或甲板饰面。每种建筑涂料无论使用何种用途,都必须提供一定的装饰性、耐用性和保护性功能。

- 大多数房主更喜欢在客厅和卧室墙壁上使用自己选择的颜色。丙烯酸涂料是首选,因为它们在颜色和色调方面提供多种选择。绝大多数天花板都漆成纯白色,这样可以反射房间内的大部分环境光,让住户感觉房间宽敞、轻松。地下室砖石墙经常会渗水。

- 2022 年 5 月,Grasim Industries(Aditya Birla Group)计划到 2025 财年为其涂料业务投资 1000 亿印度卢比(约合 12.0947 亿美元)。 2021 年 1 月,该公司宣布计划在未来三年内斥资 500 亿印度卢比(约合 6.0473 亿美元)进军涂料业务。该公司可能会在 2024 财年第四季度之前投产一家年产能为 13.32 亿升 (MLPA) 的涂料厂。

- 据日本经济产业省统计,2021年日本合成树脂涂料产量约为101万吨,涂料产量巨大。总体而言,2021年涂料产量增至近153万吨,而2020年为150万吨。

- 据美国涂料协会(Coatings Tech)统计,2020年美国油漆涂料行业产值达252.1亿美元,预计到2022年将达到280.6亿美元。 2020 年行业产量为 13.37 亿加仑,预计到 2022 年将达到 14.16 亿加仑。这可能会增加该国油漆和涂料行业对丙烯酸的需求。

- 总体而言,在经历了最初的复苏期之后,预计该地区丙烯酸需求将出现中高速增长。

预计亚太地区将主导市场

- 由于中国、印度和日本等国家的高需求,亚太地区主导了市场。

- 中国是亚太地区最大的丙烯酸消费国,预计其需求在预测期内将增长。由于建筑和基础设施领域的投资不断增长,中国对粘合剂、油漆和涂料的需求也在大幅增长。

- 此外,中国是全球个人卫生用品的主要消费国之一。该国对个人卫生产品的需求归因于婴儿人口众多和可支配收入的增加,导致个人和卫生护理支出增加。因此,预计在预测期内将提振丙烯酸市场。

- 中国以其工业化和制造业而闻名,广泛需要油漆和涂料。该国使用油漆和涂料的一些主要行业是汽车、工业和建筑行业等。中国占全球涂料市场的四分之一以上。据中国涂料工业协会统计,近年来该行业增长了7%,带动了丙烯酸在涂料应用市场的发展。

- 中国有近万家涂料生产商。大多数全球领先的涂料制造商,如立邦涂料、阿克苏诺贝尔、中国船舶涂料、PPG工业、BAF SE和艾仕得涂料,都在中国设有制造基地。油漆和涂料公司在该国的投资不断增加。这可能会刺激用于制造汽车油漆和涂料的丙烯酸市场。

- 杜邦等公司在粘合剂行业投资约 3000 万美元,在华东地区江苏省张家港市建立了新的制造工厂。该公司的新工厂生产粘合剂,为运输行业的客户提供服务,主要支持两大行业趋势:车辆电气化应用和轻量化。该设施于 2021 年第三季度开始施工,预计将于 2023 年初投入运营。

- 印度油漆和涂料业务的一些主要参与者包括亚洲涂料 (Asian Paints)、伯杰涂料 (Berger Paints)、关西 Nerolac 和阿克苏诺贝尔印度 (Akzo Nobel India)。近期,多家公司宣布扩建产能,这可能会增加国内油漆和涂料配方对丙烯酸的需求。

- 丙烯酸用于成人和女性卫生用品。在印度,缺乏经期卫生一直是一个挑战。据联合国教科文组织和 Whisper 统计,截至 2021 年 4 月,印度有 2300 万女孩因缺乏经期卫生和意识而辍学。印度约有 4 亿经期女性,其中不到 20% 使用卫生巾。在城市地区,这一数字仅高达 52%。

- 因此,由于这些因素,亚太地区可能在预测期内主导丙烯酸市场。

丙烯酸行业概况

丙烯酸市场本质上是整合的。该市场的主要参与者包括巴斯夫、阿科玛、日本触媒、LG 化学和上海华谊丙烯酸有限公司等。

丙烯酸市场领导者

-

BASF SE

-

Arkema

-

LG Chem

-

Shanghai Huayi Acrylic Acid Co. Ltd.

-

NIPPON SHOKUBAI CO., LTD.

*免责声明:主要玩家排序不分先后

丙烯酸市场新闻

- 2022年4月:万华宣布,公司将斥资36亿美元,到2024年在中国建设一座化工联合体。该联合体还将生产环氧丙烷、聚醚多元醇、丙烯酸、聚丙烯等。

- 2021 年 8 月:巴斯夫股份公司和中国石化决定扩建由巴斯夫扬子石化有限公司运营的一体化基地,该公司是两家公司在中国南京的 50:50 合资企业。其中包括几个下游化工厂的产能扩张,其中包括一座新的丙烯酸叔丁酯工厂,以支持不断增长的中国市场。丙烯酸叔丁酯工厂将是下游的延伸,使用现有一体化的丙烯酸和异丁烯作为原料。

丙烯酸市场报告 - 目录

1. 介绍

1.1 研究假设

1.2 研究范围

2. 研究方法论

3. 执行摘要

4. 市场动态

4.1 司机

4.1.1 高吸水性聚合物的应用不断增加

4.1.2 增加化学合成中的使用

4.2 限制

4.2.1 丙烯酸对健康的危害

4.3 行业价值链分析

4.4 波特五力分析

4.4.1 供应商的议价能力

4.4.2 买家的议价能力

4.4.3 新进入者的威胁

4.4.4 替代产品和服务的威胁

4.4.5 竞争程度

5. 市场细分(市场规模按数量计算)

5.1 按衍生品

5.1.1 丙烯酸甲酯

5.1.2 丙烯酸丁酯

5.1.3 丙烯酸乙酯

5.1.4 丙烯酸2-乙基己酯

5.1.5 冰丙烯酸

5.1.6 高吸水性聚合物

5.2 按申请

5.2.1 油漆和涂料

5.2.2 粘合剂和密封剂

5.2.3 表面活性剂

5.2.4 卫生用品

5.2.5 纺织品

5.2.6 其他应用

5.3 按地理

5.3.1 亚太

5.3.1.1 中国

5.3.1.2 印度

5.3.1.3 日本

5.3.1.4 韩国

5.3.1.5 东盟国家

5.3.1.6 亚太其他地区

5.3.2 北美

5.3.2.1 美国

5.3.2.2 加拿大

5.3.2.3 墨西哥

5.3.3 欧洲

5.3.3.1 德国

5.3.3.2 法国

5.3.3.3 英国

5.3.3.4 意大利

5.3.3.5 欧洲其他地区

5.3.4 南美洲

5.3.4.1 巴西

5.3.4.2 阿根廷

5.3.4.3 南美洲其他地区

5.3.5 中东和非洲

5.3.5.1 沙特阿拉伯

5.3.5.2 南非

5.3.5.3 中东和非洲其他地区

6. 竞争格局

6.1 合并、收购、合资、合作和协议

6.2 市场份额(%)分析

6.3 领先企业采取的策略

6.4 公司简介

6.4.1 Arkema

6.4.2 BASF SE

6.4.3 China Petroleum & Chemical Corporation (SINOPEC)

6.4.4 Dow

6.4.5 Formosa Plastics Corporation

6.4.6 LG Chem

6.4.7 Merck KGaA

6.4.8 Mitsubishi Chemical Corporation

6.4.9 NIPPON SHOKUBAI CO. LTD

6.4.10 Sasol

6.4.11 Shanghai Huayi Acrylic Acid Co. Ltd

6.4.12 Satellite Chemical Co. Ltd

6.4.13 Wanhua

7. 市场机会和未来趋势

7.1 对生物基聚合物的需求不断增加

丙烯酸行业细分

丙烯酸是一种无色不饱和羧酸,分子式C3H4O2,由丙烯两级催化氧化产生。它可以聚合形成均聚物,也可以与酯类和其他乙烯基单体共聚。因此,丙烯酸主要用于生产不同塑料制品的聚合物。它还可用于生产粘合剂、密封剂和表面活性剂。

丙烯酸市场按衍生物(丙烯酸甲酯、丙烯酸丁酯、丙烯酸乙酯、丙烯酸2-乙基己酯、冰丙烯酸、高吸水性聚合物)、应用(油漆和涂料、粘合剂和密封剂、表面活性剂、卫生产品、纺织品、其他应用)细分)和地理(亚太地区、北美、欧洲、南美洲、中东和非洲)。该报告还涵盖了主要地区15个国家丙烯酸市场的市场规模和预测。该报告提供了所有上述细分市场的市场规模和以千吨为单位的预测。

| 按衍生品 | ||

| ||

| ||

| ||

| ||

| ||

|

| 按申请 | ||

| ||

| ||

| ||

| ||

| ||

|

| 按地理 | ||||||||||||||

| ||||||||||||||

| ||||||||||||||

| ||||||||||||||

| ||||||||||||||

|

丙烯酸市场研究常见问题解答

丙烯酸市场有多大?

预计2024年丙烯酸市场规模将达到777万吨,到2029年将达到1001万吨,复合年增长率为5.19%。

目前丙烯酸市场规模有多大?

2024年,丙烯酸市场规模预计将达到777万吨。

丙烯酸市场的主要参与者有哪些?

BASF SE、Arkema、LG Chem、Shanghai Huayi Acrylic Acid Co. Ltd.、NIPPON SHOKUBAI CO., LTD. 是丙烯酸市场上运营的主要公司。

丙烯酸市场增长最快的地区是哪个?

预计亚太地区在预测期内(2024-2029 年)复合年增长率最高。

哪个地区丙烯酸市场份额最大?

2024年,亚太地区将占据丙烯酸市场最大的市场份额。

这个丙烯酸市场涵盖了哪些年份?2023年的市场规模是多少?

2023年,丙烯酸市场规模预计为739万吨。该报告涵盖了丙烯酸市场的历史市场规模:2019年、2020年、2021年、2022年和2023年。该报告还预测了丙烯酸市场的多年市场规模:2024年、2025年、2026年、2027年、2028年和2029年。

丙烯酸行业报告

Mordor Intelligence™ 行业报告创建的 2024 年丙烯酸市场份额、规模和收入增长率统计数据。丙烯酸分析包括对 2029 年的市场预测展望和历史概述。获取此行业分析的样本(免费下载 PDF 报告)。