White Biotechnology Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

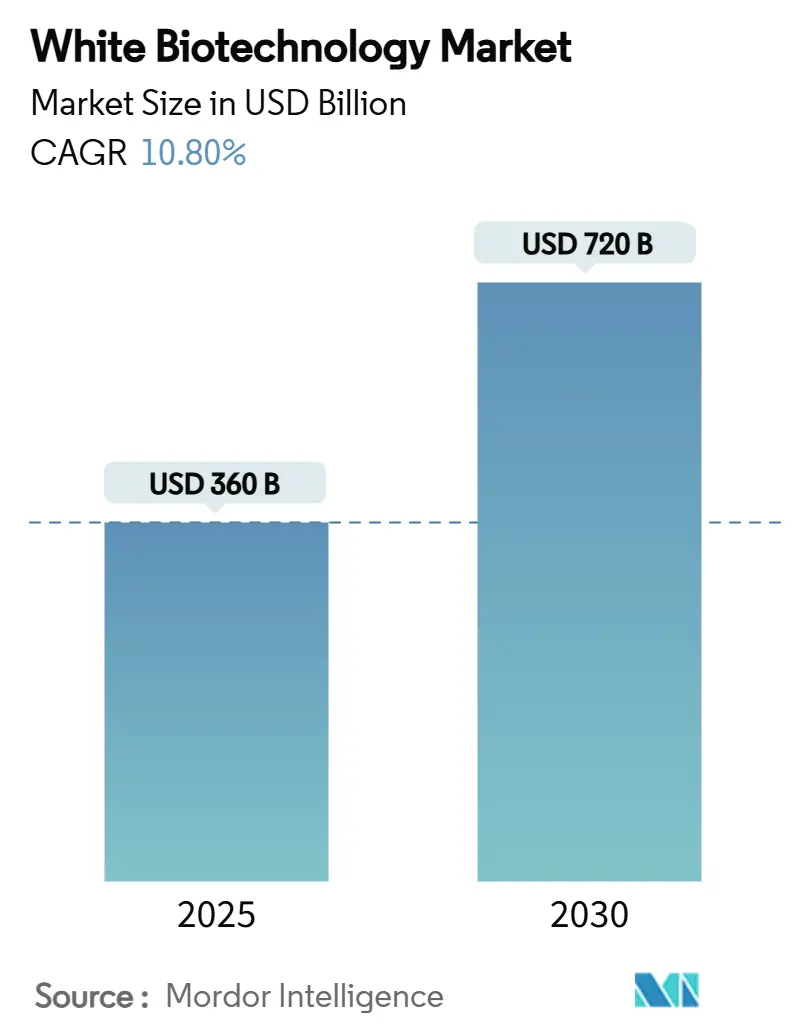

| Market Size (2025) | USD 360 Billion |

| Market Size (2030) | USD 720 Billion |

| Growth Rate (2025 - 2030) | 10.80% CAGR |

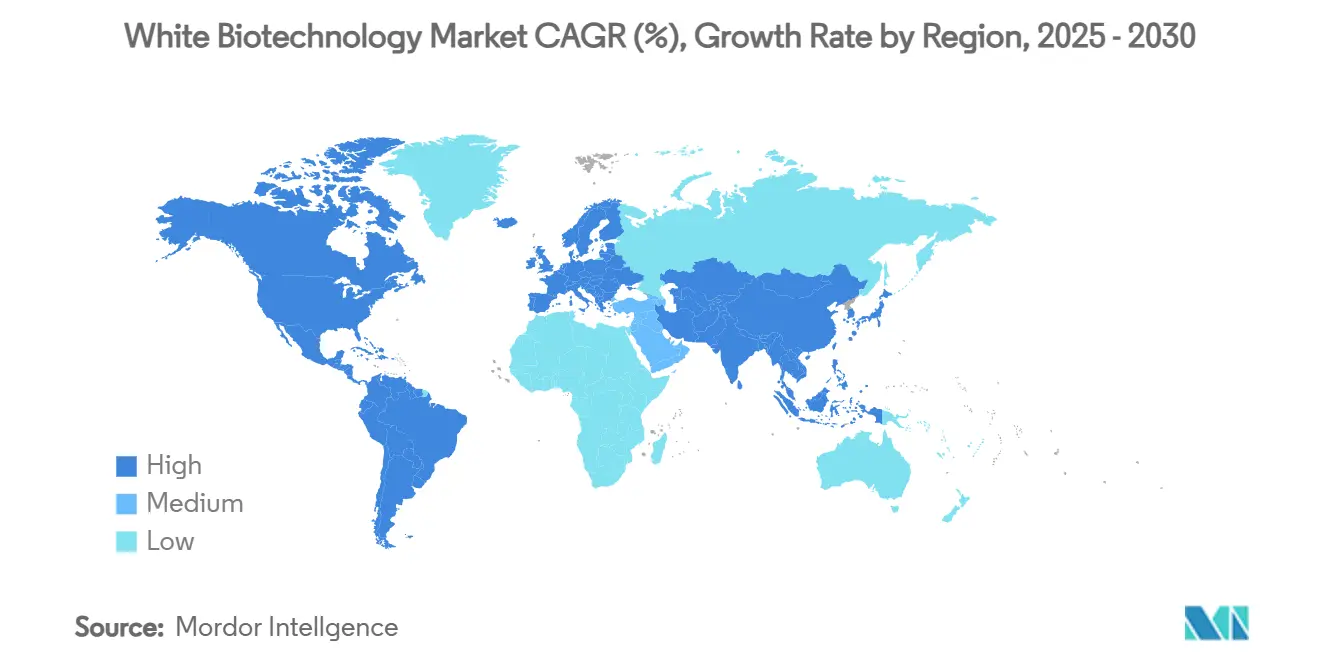

| Fastest Growing Market | Europe |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

White Biotechnology Market Analysis by Mordor Intelligence

The white biotechnology market size stands at USD 360 billion in 2025 and is projected to reach USD 720 billion by 2030, implying a healthy 10.8% CAGR over the forecast period. This outlook reflects the technology’s transition from specialty use-cases to mainstream industrial adoption, driven by corporate decarbonization commitments, supportive policy frameworks, and rapid progress in synthetic biology. Precision fermentation platforms now produce high-value molecules without the land or resource intensity of conventional agriculture, while the growing availability of low-carbon feedstocks is easing cost barriers. Industrial producers view biological routes not merely as an environmental upgrade but as a hedge against fossil-price volatility and future carbon border levies that raise the cost of conventional production. The resulting demand pull is amplified by advances in AI-assisted protein engineering, which shorten development cycles and widen the range of molecules that microbes can synthesise.

Key Report Takeaways

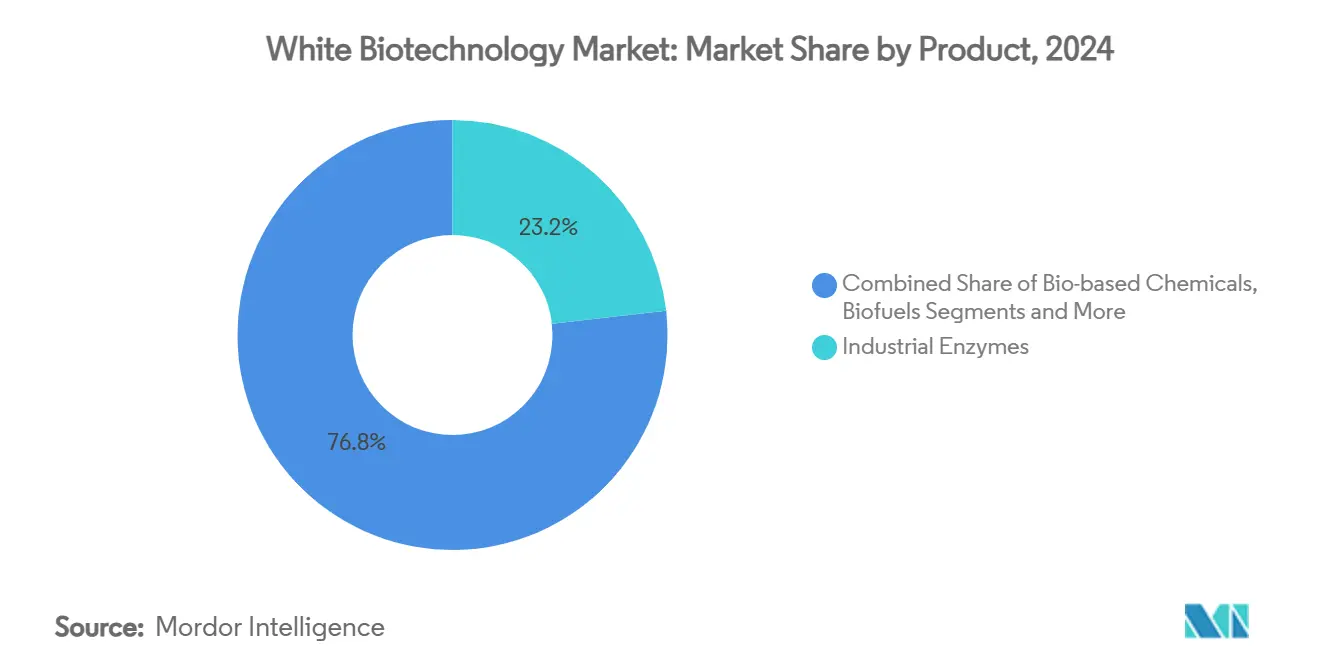

- By product type, industrial enzymes led the white biotechnology market with 23.2% of the share in 2024; bioplastics and bio-polymers are forecast to expand at a 15.3% CAGR through 2030.

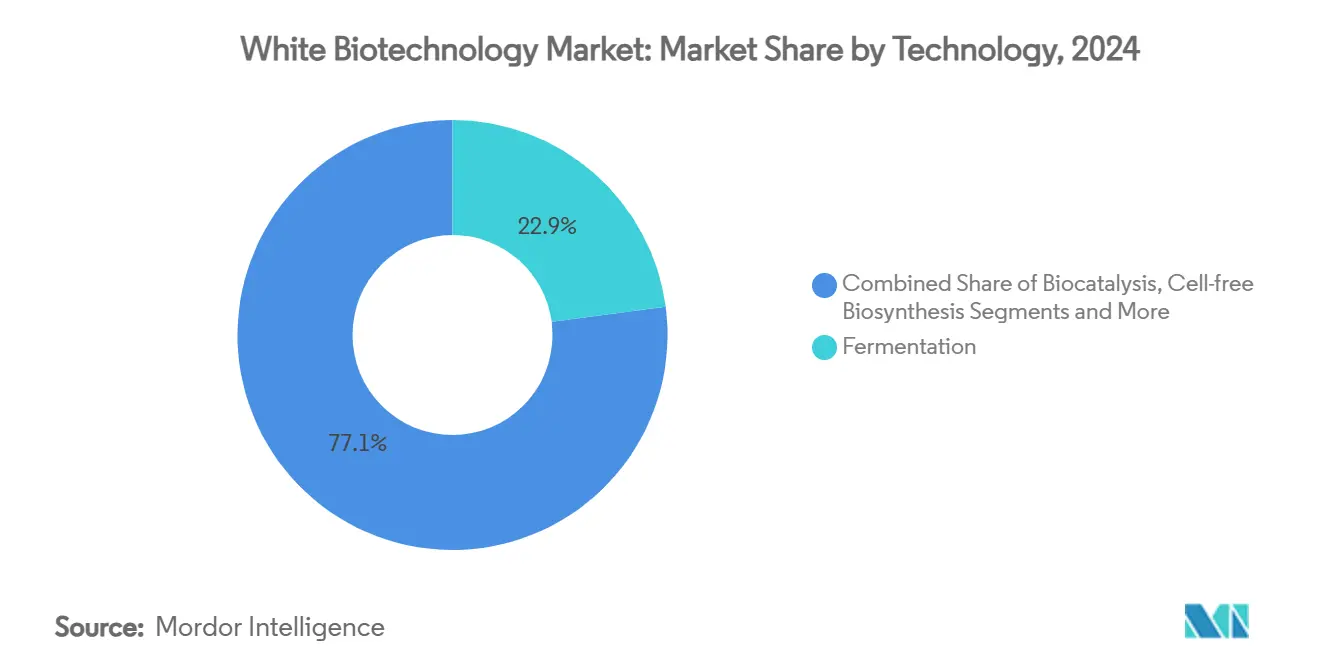

- By technology, traditional fermentation held 22.9% of the white biotechnology market share in 2024, whereas precision fermentation and synthetic biology are projected to rise at a 28.6% CAGR to 2030.

- By application, food and beverage processing commanded 20.3% of the white biotechnology market size in 2024, while home and personal care is the fastest-growing application with an 11.9% CAGR to 2030.

- By geography, Europe captured 23.8% of the white biotechnology market share in 2024; Asia-Pacific is forecast to lead growth with a 9.8% CAGR between 2025-2030.

Global White Biotechnology Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Global decarbonization and net-zero policy frameworks | +2.30% | EU, North America, global spillover | Long term (≥ 4 years) |

| Corporate sustainability and circular-economy commitments | +1.80% | Multinational operations worldwide | Medium term (2-4 years) |

| Advances in synthetic biology and precision fermentation | +1.50% | North America, Europe, Asia-Pacific | Medium term (2-4 years) |

| Rising demand for bio-based chemicals, polymers, and fuels | +1.20% | Developed markets first, global next | Short term (≤ 2 years) |

| Surge in green investment and public funding for biomanufacturing | +0.90% | North America, EU, APAC spillover | Short term (≤ 2 years) |

| Cross-industry feedstock partnerships unlocking new biomass streams | +0.80% | Agricultural regions worldwide | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Global Decarbonization and Net-Zero Policy Frameworks

Government road-maps such as the EU Green Deal and the United States’ Inflation Reduction Act are embedding life-cycle carbon in procurement decisions, effectively guaranteeing long-term off-take for bio-based intermediates. Carbon border adjustment mechanisms further raise the competitiveness of domestic bio-manufacturing by penalizing imports with higher embedded emissions, shifting the white biotechnology market from optional to obligatory in many heavy industries.[1]European Commission, “Fit for 55 Package,” europa.eu

Corporate Sustainability and Circular-Economy Commitments

Science-based net-zero pledges cover the bulk of listed multinationals by revenue, pushing buyers to secure renewable raw materials many years in advance. Consumer-facing giants have begun signing multi-year supply contracts for bio-based surfactants and aroma molecules, sending clear volume signals that underpin green-field biorefinery projects.

Advances in Synthetic Biology and Precision Fermentation

CRISPR-enabled strain engineering now allows yeast and bacterial hosts to synthesise cyclic peptides, fatty alcohols, and rare musks that previously required petrochemicals or animal sources. AI-guided protein folding shortens design loops from months to days, while modular bioreactors permit distributed production close to demand centres, lowering logistics emissions and inventory risk.[2]Science Editors, “Metabolic Engineering Costs and Yields,” science.org

Surge in Green Investment and Public Funding for Biomanufacturing

More than USD 2 billion in US federal grants and low-interest loans are earmarked for biorefinery scale-up, complemented by sizeable EU Innovation Fund disbursements. These funds de-risk first-of-a-kind plants whose capex cannot yet be justified on pure market pricing alone.[3]U.S. Department of Energy, “Biorefinery, Renewable Chemical, and Biobased Product Manufacturing Assistance Program,” energy.gov

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Cost Competitiveness Vs. Fossil-Based Incumbents | -1.40% | Global, with highest impact in price-sensitive markets | Short term (≤ 2 years) |

| Limited Large-Scale Supply Of Sustainable Non-Food Biomass | -0.90% | Global, with acute challenges in developing regions | Long term (≥ 4 years) |

| Fragmented & Evolving Bio-Product Regulations | -0.60% | Global, with complexity in multi-jurisdictional markets | Medium term (2-4 years) |

| Technological Scale-Up Risks In Next-Generation Bioprocesses | -0.40% | North America & Europe, with spillover to APAC | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Cost Competitiveness vs. Fossil-Based Incumbents

Production costs for common bio-based intermediates can exceed petrochemical analogues by 20-50% owing to expensive nutrients and downstream purification. The gap narrows only when carbon prices, renewable-content mandates, or consumer premiums offset biology’s higher fixed costs. Advanced synthetic-biology hosts promise higher titres, but true parity remains dependent on oil-price cycles and larger bioreactor trains.

Limited Large-Scale Supply of Sustainable Non-Food Biomass

The sector competes with food and feed for land, yet residue recovery suffers from fragmented logistics and seasonal variation. While dedicated energy crops on marginal land offer theoretical relief, real-world cultivation often clashes with water use and biodiversity concerns. Policy incentives for agricultural waste valorisation and improvements in pre-treatment technologies will determine how quickly this bottleneck eases.

Segment Analysis

By Product Type: Industrial Enzymes Maintain Lead as Bioplastics Accelerate

Industrial enzymes accounted for 23.2% of the white biotechnology market share in 2024, reflecting their decades-long integration into brewing, baking, textile desizing, and detergent formulations. Novozymes, IFF, and DSM-Firmenich exploit high-throughput strain libraries and global application labs to optimise both cost and performance for brand-owners. Enzyme use is set to broaden with emerging thermostable variants that unlock harsher process conditions, lifting overall throughput and pushing the white biotechnology market toward higher value-added niches. In contrast, bio-based chemicals—organic acids, polyols, and solvents—occupy the second-largest revenue slot but face continued margin pressure from fossil-price swings.

The bioplastics segment is projected to grow at a 15.3% CAGR, supported by EU single-use restrictions and major brands’ packaging pledges. Companies such as NatureWorks (PLA) and Danimer Scientific (PHA) have passed pivotal capacity milestones, signalling that scale economies are arriving. Price parity with fossil plastics remains elusive, yet landfill levies and extended producer responsibility fees are narrowing the gap. By 2030, bioplastics could capture 8-10 million tonnes of annual demand, translating into roughly USD 21 billion in the white biotechnology market size for polymer applications. Biofuels exhibit divergent regional trajectories: Brazil and Indonesia expand ethanol and biodiesel output under blending rules, whereas Europe’s cap on crop-based fuels curbs near-term growth.

Note: Segment shares of all individual segments available upon report purchase

By Application: Food Processing Dominance Faces Personal-Care Upswing

Food and beverage processing held 20.3% of the white biotechnology market size in 2024, grounded in enzymes for starch conversion, dairy texturisation, and brewing clarification. Regulatory familiarity and clear functionality advantages secure stable offtake. Nonetheless, home and personal-care products are slated for an 11.9% CAGR to 2030, propelled by consumers willing to pay price premiums for plant-derived surfactants, emollients, and active ingredients. Ingredient specialists leverage biosurfactants like rhamnolipids to deliver comparable foaming while meeting vegan and micro-plastic-free label claims.

Chemicals and materials applications follow close behind, where polymers, coatings, and solvents face tightening VOC rules and carbon-footprint disclosures. The shift is buoyed by downstream OEMs, including automotive and electronics producers that integrate bio-based inputs to comply with Scope 3 targets. Animal-feed enzymes grow steadily as livestock producers cut antibiotic usage, and agriculture bio-stimulants emerge as a crossover category. Smaller but important, wastewater/bioresource treatment exemplifies the circular-economy promise: microbes treat effluent while producing biogas, monetising what was once a pure cost centre.

By Technology: Fermentation Dominance Gives Way to Precision Platforms

Conventional fermentation occupied 22.9% of the white biotechnology market share in 2024, underpinned by decades of fine-tuned processes and fully amortised assets. However, precision fermentation and broader synthetic-biology toolkits are poised to log a 28.6% CAGR, redefining how and where molecules are made. The emerging stack combines cloud-based DNA design, robotics-enabled strain construction, and advanced process-control software that boosts titres and yields, shortening tech-transfer timelines to weeks.

Biocatalysis remains critical for stereoselective transformations, especially in pharmaceutical intermediates where purity is paramount. Cell-free biosynthesis—enzyme cascades in solution without living cells—delivers high volumetric productivity for small, toxic molecules that kill whole-cell hosts. Downstream purification, historically a bottleneck, benefits from novel membrane materials and affinity resins tailored to specific product classes, trimming overall variable cost. By 2030, multi-platform biocampuses able to toggle among fermentation, enzymatic, and cell-free modules are expected to dominate the white biotechnology market.

Note: Segment shares of all individual segments available upon report purchase

Geography Analysis

Europe led the white biotechnology market with a 23.8% revenue share in 2024, anchored by stringent sustainability directives, integrated chemical clusters, and world-class research institutions. Germany’s National Bioeconomy Strategy funds flagship biorefineries, while France, the Netherlands, and the Nordic region leverage logistics and forestry biomass to feed advanced materials projects. The impending EU Carbon Border Adjustment Mechanism adds further impetus, as exporters into the bloc must decarbonize or pay levies, indirectly enlarging domestic bio-based demand. Regulatory certainty and innovation grants keep start-ups and corporates aligned on long-term scale-up road maps.

Asia-Pacific is set to be the fastest-growing region at a 9.8% CAGR to 2030, driven by China’s USD 4.17 billion public-private investment program and state goals to localise high-value chemicals. These projects range from alternative proteins to bio-based nylon monomers, relying on abundant agricultural residues that lower feedstock costs. India positions itself as a supply-chain alternative, buoyed by skilled human capital and supportive bio-economy missions, while Australia eyes its sugar and forestry residues for bio-jet fuel. Japan and South Korea blend robust IP protection with coordinated R&D funding, fostering regional clusters that share end-markets with electronics and automotive incumbents. Southeast Asia leverages plentiful palm and cassava residues, though infrastructure for year-round biomass aggregation remains a challenge.

North America represents a pivotal growth engine as US policy targets 30% of all chemicals via bio-manufacturing within two decades. Over USD 2 billion in BARDA and DOE grants lowers early-stage risk, while the Department of Defense backs distributed biomanufacturing to secure a domestic supply of critical inputs. Canada supports a talent pipeline through BioTalent programs and uses its canola surplus for renewable diesel feedstock. Mexico capitalises on shale-gas constraints by courting bio-based investors for industrial parks along the Gulf coast. Venture funding remains abundant, though IPO windows have narrowed, pushing start-ups toward strategic partnerships with established agri-commodities majors for scale capital.

Competitive Landscape

The white biotechnology market shows moderate fragmentation. Legacy chemical multinationals—BASF, DSM-Firmenich, Evonik—employ balance-sheet strength and process-engineering know-how to scale next-generation assets, while pure-play synbio firms—Ginkgo Bioworks, Genomatica, Zymergen—offer design-as-a-service and licensing models. Industrial enzymes remain relatively concentrated; Novozymes and IFF together controlled over 50% of 2024 enzyme revenue before Novozymes merged with Chr. Hansen will form Novonesis, a platform designed to capture synergies across food, health, and agriculture.

Strategic moves emphasise feedstock control, with Cargill and ADM expanding into PHA and 1,4-butanediol via joint ventures that integrate farming, processing, and distribution. Hyosung’s investment in Geno-enabled BDO plants demonstrates the appeal of drop-in monomers for established polymer chains. Pharmaceutical outsourcing is fertile ground: Pearl Bio and Merck’s partnership targets high-value cyclic peptides where synthetic routes are prohibitive. Consolidation continues as private-equity owners seek scale efficiencies, illustrated by Novo Holdings’ USD 16.5 billion acquisition of Catalent’s small-molecule CDMO network, securing capacity for biologically produced APIs that overlap with enzyme and biopolymer markets.

Technology alliances proliferate; VTT’s AI-driven biomaterial platform partners with pulp companies to create innovative packaging solutions, while Austrian and German breweries co-fund fermentation start-ups to secure low-carbon aroma hops. Such bilateral deals reduce development cycles and spread risk. Competitive advantage increasingly lies in data assets—strain libraries, process digital twins, and real-time QC algorithms—rather than in proprietary feedstock access alone.

White Biotechnology Industry Leaders

-

Novozymes

-

IFF (DuPont Genencor)

-

DSM-Firmenich

-

BASF

-

Cargill

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Pohang University achieved the first ribosomal synthesis of cyclic peptides, expanding pharma options.

- March 2025: Lesaffre acquired Altar to boost fermentation innovation for agricultural biosolutions.

- July 2024: Lawrence Berkeley National Laboratory unveiled a one-day gene-writing technique using the TdT enzyme, advancing rapid DNA synthesis.

Global White Biotechnology Market Report Scope

| Industrial Enzymes |

| Bio-based Chemicals (Organic Acids, Alcohols, Ketones) |

| Biofuels (Bioethanol, Biodiesel, SAF, Biogas) |

| Bioplastics & Bio-polymers (PLA, PHA, Bio-PET, Bio-PE) |

| Chemicals & Materials Manufacturing |

| Energy & Fuels |

| Food & Beverage Processing |

| Animal Feed & Agriculture |

| Home & Personal Care |

| Textile & Pulp/Paper Processing |

| Wastewater Treatment |

| Fermentation |

| Biocatalysis / Enzymatic Conversion |

| Cell-free Biosynthesis |

| Precision Fermentation & Synthetic Biology |

| Down-stream Processing |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product Type | Industrial Enzymes | |

| Bio-based Chemicals (Organic Acids, Alcohols, Ketones) | ||

| Biofuels (Bioethanol, Biodiesel, SAF, Biogas) | ||

| Bioplastics & Bio-polymers (PLA, PHA, Bio-PET, Bio-PE) | ||

| By Application | Chemicals & Materials Manufacturing | |

| Energy & Fuels | ||

| Food & Beverage Processing | ||

| Animal Feed & Agriculture | ||

| Home & Personal Care | ||

| Textile & Pulp/Paper Processing | ||

| Wastewater Treatment | ||

| By Technology | Fermentation | |

| Biocatalysis / Enzymatic Conversion | ||

| Cell-free Biosynthesis | ||

| Precision Fermentation & Synthetic Biology | ||

| Down-stream Processing | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the projected size of the white biotechnology market by 2030?

The white biotechnology market size is expected to reach USD 720 billion by 2030, doubling its 2025 value at a 10.8% CAGR.

Which product segment leads the white biotechnology market?

Industrial enzymes dominate, holding 23.2% of the white biotechnology market share in 2024 due to long-standing use in food, textile, and detergent applications.

Why is Asia-Pacific considered the fastest-growing region?

Asia-Pacific shows a 9.8% CAGR forecast as China invests USD 4.17 billion in synthetic-biology hubs and India positions itself as a strategic alternative supply base.

How do policy frameworks influence the white biotechnology market?

Net-zero mandates, carbon border adjustments, and green-procurement rules guarantee demand for bio-based inputs, making biological routes economically compelling even before full cost parity.

What technologies are accelerating market growth?

Precision fermentation and synthetic-biology platforms—backed by AI design tools—enable microbes to produce complex molecules, driving a 28.6% CAGR for these technologies within the market.

What is the main barrier to rapid scale-up?

Cost competitiveness against fossil-based incumbents remains the chief restraint, with bio-based production currently 20-50% more expensive until carbon pricing, larger reactor trains, and higher titres close the gap.

Page last updated on: