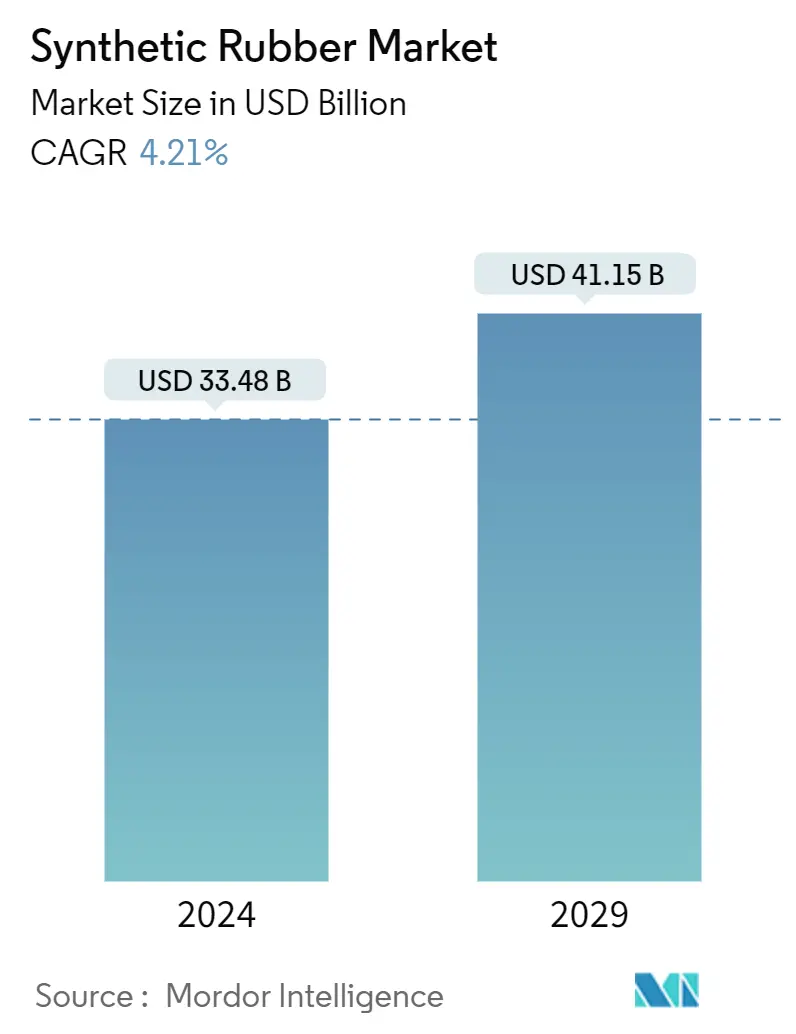

Synthetic Rubber Market Size

| Study Period | 2024 - 2029 |

| Market Size (2024) | USD 33.48 Billion |

| Market Size (2029) | USD 41.15 Billion |

| CAGR (2024 - 2029) | 4.21 % |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Asia-Pacific |

Major Players

*Disclaimer: Major Players sorted in no particular order |

Need a report that reflects how COVID-19 has impacted this market and its growth?

Synthetic Rubber Market Analysis

The Synthetic Rubber Market size is estimated at USD 33.48 billion in 2024, and is expected to reach USD 41.15 billion by 2029, growing at a CAGR of 4.21% during the forecast period (2024-2029).

In 2020, due to the COVID-19 pandemic, the global synthetic rubber market experienced a downturn, resulting in widespread lockdowns, disruptions in manufacturing and supply chains, and production stoppages. However, conditions began to improve in 2021-2022, and the market is expected to grow year-on-year during the forecast period as automotive demand is expected to increase.

- The growth of the market is expected to receive a boost due to the increasing production of electric vehicles.

- On the other hand, using polyurethanes instead of synthetic rubber in some applications is likely to decelerate the growth of the market.

- Future opportunities for the market could come from the development of bio-based feedstock for synthetic rubber and the growing demand for medical gloves.

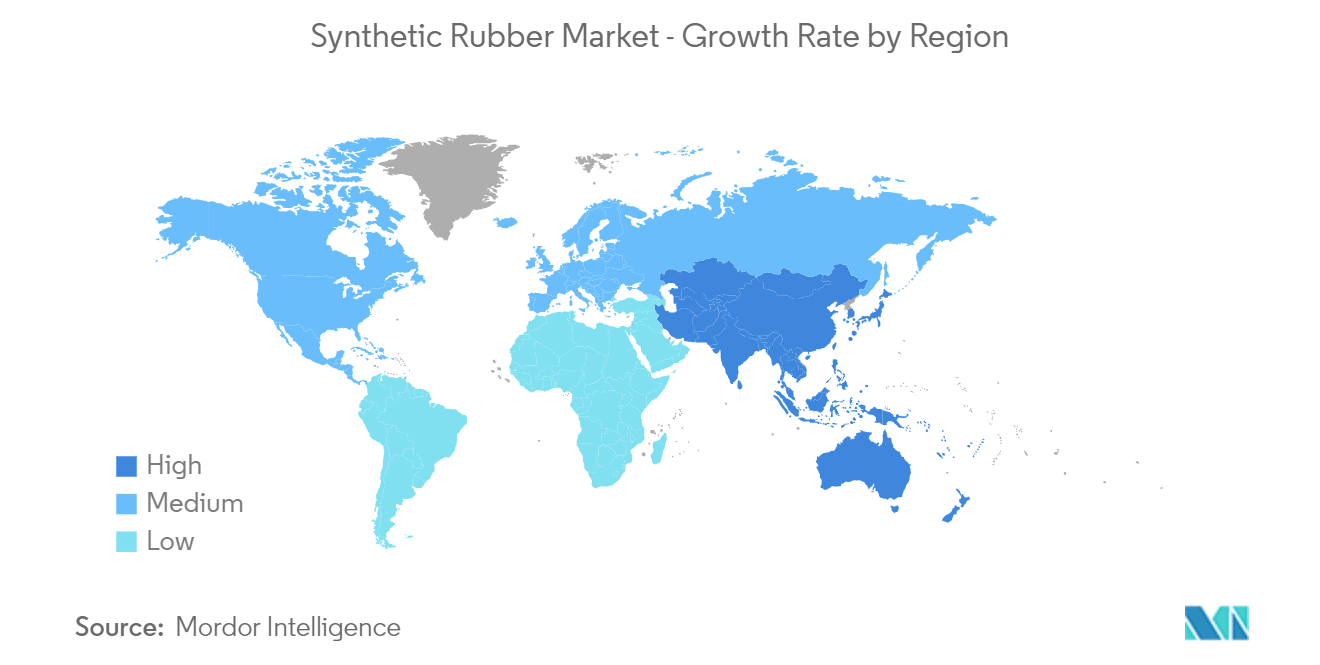

- Due to high demand from China, India, and Japan, Asia-Pacific has the largest market share and is likely to lead the market during the forecast period.

Synthetic Rubber Market Trends

Increasing Demand From Tire and Tire Components

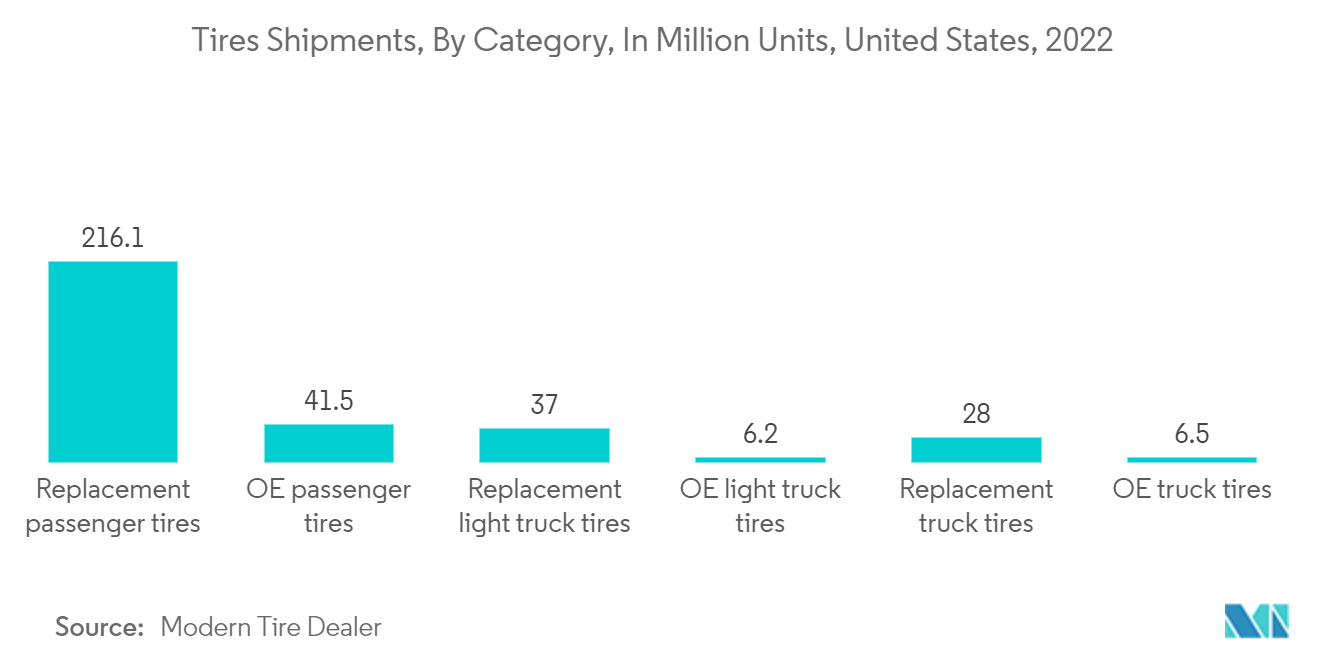

- The segment for tires and tire parts holds the largest market share in the synthetic rubber market. Tires are predominantly made using styrene-butadiene rubber due to its durability and resistance to wear over time.

- It is the preferred material in the tire manufacturing sector. Around 50% of car tires are made of styrene-butadiene rubber blended with natural rubber.

- For low-end tires, the ratio of SBR to natural rubber is lower to reduce the cost of production. Although this reduces the overall tire life, it is a cost-effective option.

- According to the International Tyre and Rubber Association (ITRA), China and the United States are the two largest tire producer countries in the world.

- According to the National Bureau of Statistics of China, the Chinese tire industry made about 859.19 million tires in 2022. Moreover, due to factors such as high demand and overseas company expansion, the domestic tire industry in China is likely to experience substantial growth in 2024, as it did in 2023. For instance, China's export of semi-steel tires, primarily utilized for passenger vehicles, witnessed a 20% year-on-year surge and reached a total of 287 million units in 2023, according to Global Times.

- The globally increasing demand for passenger cars will also likely increase the production of tires and their components during the forecast period. For instance, according to EV-Volumes.com, the unit volume of global EV sales is projected to triple from 10.5 million in 2022 to over 31 million in 2027.

- Due to the above-mentioned factors, the tire and tire components segment is expected to boost the growth of the market significantly during the forecast period.

Asia-Pacific to Dominate the Market

- Asia-Pacific accounts for the largest share of the synthetic rubber market because of countries such as India, China, and Japan, where the demand is significantly high.

- Countries such as China, India, Japan, South Korea, Thailand, and Indonesia are home to major tire-producing companies in the world.

- India is second only to China in the Asia-Pacific region in terms of how much rubber it makes and uses. Even though the country is one of the biggest producers of rubber, it imports a lot of rubber from other countries to meet local demand.

- According to the Rubber Board, synthetic rubber consumption in India was about 0.75 million metric tons in the financial year 2023. Furthermore, almost three-quarters of this total was consumed by the auto tires and tubes sector, with the remaining quantity used for general rubber goods.

- The Japanese tire industry is also expanding significantly in the region. Toyo Tire Corporation is one of Japan's largest rubber corporations, specializing in automobile tires and other automotive-related products.

- The net sales of Toyo Tire Corporation amounted to approximately JPY 497.2 billion (USD 3.3 billion) in 2022, up from around JPY 393.7 billion (USD 2.6 billion) in the previous year, thus boosting the growth of the market significantly in the region.

- These factors are expected to assist Asia-Pacific dominate the overall market during the forecast period.

Synthetic Rubber Industry Overview

The synthetic rubber market is fragmented in nature. Some of the major players in the market include Exxon Mobil Corporation, Kumho Petrochemical, Saudi Arabian Oil Co., TSRC, and China Petrochemical Corporation, among others.

Synthetic Rubber Market Leaders

Kumho Petrochemical

Saudi Arabian Oil Co.

TSRC

Exxon Mobil Corporation

China Petrochemical Corporation

*Disclaimer: Major Players sorted in no particular order

Synthetic Rubber Market News

- December 2023: SIBUR's Nizhnekamskneftekhim completed the upgrade of its halobutyl rubbers (HBR) capacities by ramping them up from 150 to 200 kilotons. About RUB 8 billion (USD 85.5 million) was spent on this upgrade project, which installed six new HBR production units and revamped 16 existing ones.

- May 2023: Arlanxeo announces planned to build a rubber production plant in Jubail, Saudi Arabia, with an annual capacity of 140,000 metric tons. This plant will be part of the USD 11 billion Amiral complex planned by Saudi Aramco and Total Energies to produce two elastomers, including ultra-high cis polybutadiene (NdBR) and lithium butadiene rubber (LiBR).

- May 2023: Hankook Tire and Kumho Petrochemical entered into a memorandum of understanding (MoU) to collaborate on advancing environmentally friendly tires by utilizing eco-solution-polymerized styrene-butadiene rubber (eco-SSBR).

- April 2023: The Hainan-based subsidiary of China Petroleum and Chemical Corp., Hainan Baling Chemical New Material Co., Ltd, announced the launch of its latest project focused on the production of Styrene-Butadiene Copolymer (SBC) in Hainan, China. The annual production capacity of 170,000 tons will make Sinopec the world's largest producer of SBC plants.

- March 2023: The Saudi Arabian Oil Company (Aramco) completed the USD 2.65 billion acquisition of Valvoline Inc., a provider of automotive and industrial solutions, through one of its wholly-owned subsidiaries.

- December 2022: Korea Kumho Petrochemical Co. (KKPC) announced plans for a series of synthetic rubber expansions at its production facilities in South Korea, including its plan to expand its Solution Styrene-Butadiene Rubber (SSBR) capacity to 123 Kilo-Tons Per Annum, which was scheduled to be completed by the end of 2023.

Synthetic Rubber Market Report - Table of Contents

1. INTRODUCTION

1.1 Study Assumptions

1.2 Scope of the Study

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET DYNAMICS

4.1 Drivers

4.1.1 Increasing Demand from Rising Sales of Electric Vehicles

4.1.2 Other Drivers

4.2 Restraints

4.2.1 Replacement of Rubber by Polyurethanes in Some Applications

4.2.2 Other Restraints

4.3 Industry Value Chain Analysis

4.4 Porter's Five Forces Analysis

4.4.1 Bargaining Power of Suppliers

4.4.2 Bargaining Power of Consumers

4.4.3 Threat of New Entrants

4.4.4 Threat of Substitute Products and Services

4.4.5 Degree of Competition

5. MARKET SEGMENTATION (Market Size in Value)

5.1 Type

5.1.1 Styrene Butadiene Rubber (SBR)

5.1.2 Ethylene Propylenediene Rubber (EPDM)

5.1.3 Polyisoprene (IR)

5.1.4 Polybutadiene Rubber (BR)

5.1.5 Isobutylene Isoprene Rubber (IIR)

5.1.6 Other Types

5.2 Application

5.2.1 Tire and Tire Components

5.2.2 Non-tire Automobile Applications

5.2.3 Footwear

5.2.4 Industrial Goods

5.2.5 Other Applications

5.3 Geography

5.3.1 Asia-Pacific

5.3.1.1 China

5.3.1.2 India

5.3.1.3 Japan

5.3.1.4 South Korea

5.3.1.5 Malaysia

5.3.1.6 Thailand

5.3.1.7 Vietnam

5.3.1.8 Indonesia

5.3.1.9 Rest of Asia-Pacific

5.3.2 North America

5.3.2.1 United States

5.3.2.2 Canada

5.3.2.3 Mexico

5.3.3 Europe

5.3.3.1 Germany

5.3.3.2 United Kingdom

5.3.3.3 France

5.3.3.4 Italy

5.3.3.5 Spain

5.3.3.6 Russia

5.3.3.7 NORDIC

5.3.3.8 Turkey

5.3.3.9 Rest of Europe

5.3.4 South America

5.3.4.1 Brazil

5.3.4.2 Argentina

5.3.4.3 Colombia

5.3.4.4 Rest of South America

5.3.5 Middle-East and Africa

5.3.5.1 Saudi Arabia

5.3.5.2 South Africa

5.3.5.3 United Arab Emirates

5.3.5.4 Nigeria

5.3.5.5 Qatar

5.3.5.6 Egypt

5.3.5.7 Rest of Middle-East and Africa

6. COMPETITIVE LANDSCAPE

6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

6.2 Market Share (%)**/Ranking Analysis

6.3 Strategies Adopted by Leading Players

6.4 Company Profiles

6.4.1 Apcotex

6.4.2 China Petrochemical Corporation

6.4.3 ENEOS Corporation

6.4.4 Exxon Mobil Corporation

6.4.5 Kumho Petrochemical

6.4.6 LANXESS

6.4.7 LG Chem

6.4.8 Mitsubishi Chemical Corporation

6.4.9 Reliance Industries Limited

6.4.10 SABIC

6.4.11 Saudi Arabian Oil Co.

6.4.12 SIBUR

6.4.13 Synthos

6.4.14 The Goodyear Tire & Rubber Company

6.4.15 TSRC

6.4.16 Versalis S.p.A.

6.4.17 Dow

- *List Not Exhaustive

7. MARKET OPPORTUNITIES AND FUTURE TRENDS

7.1 Development of Bio-based Feedstock for Synthetic Rubber

7.2 Other Opportunities

Synthetic Rubber Industry Segmentation

Synthetic rubber is a man-made rubber produced by combining minerals and oil in plants. The most commonly used type of synthetic rubber is styrene-butadiene rubber (SBR), which is created by copolymerizing styrene and 1,3-butadiene.

The synthetic rubber market is segmented by type, application, and geography. By type, the market is segmented into styrene-butadiene rubber, ethylene propylene diene rubber, polyisoprene rubber, polybutadiene rubber, isobutylene isoprene rubber, and other types. By application, the market is segmented into tire and tire components, non-tire automobile applications, footwear, industrial goods, and other applications (consumer goods, etc.). The report also covers the market size and forecasts in 27 countries across major regions. For each segment, market sizing and forecasts were made based on revenue (USD).

| Type | |

| Styrene Butadiene Rubber (SBR) | |

| Ethylene Propylenediene Rubber (EPDM) | |

| Polyisoprene (IR) | |

| Polybutadiene Rubber (BR) | |

| Isobutylene Isoprene Rubber (IIR) | |

| Other Types |

| Application | |

| Tire and Tire Components | |

| Non-tire Automobile Applications | |

| Footwear | |

| Industrial Goods | |

| Other Applications |

| Geography | |||||||||||

| |||||||||||

| |||||||||||

| |||||||||||

| |||||||||||

|

Synthetic Rubber Market Research FAQs

How big is the Synthetic Rubber Market?

The Synthetic Rubber Market size is expected to reach USD 33.48 billion in 2024 and grow at a CAGR of 4.21% to reach USD 41.15 billion by 2029.

What is the current Synthetic Rubber Market size?

In 2024, the Synthetic Rubber Market size is expected to reach USD 33.48 billion.

Who are the key players in Synthetic Rubber Market?

Kumho Petrochemical, Saudi Arabian Oil Co., TSRC, Exxon Mobil Corporation and China Petrochemical Corporation are the major companies operating in the Synthetic Rubber Market.

Which is the fastest growing region in Synthetic Rubber Market?

Asia-Pacific is estimated to grow at the highest CAGR over the forecast period (2024-2029).

Which region has the biggest share in Synthetic Rubber Market?

In 2024, the Asia-Pacific accounts for the largest market share in Synthetic Rubber Market.

What years does this Synthetic Rubber Market cover, and what was the market size in 2023?

In 2023, the Synthetic Rubber Market size was estimated at USD 32.07 billion. The report covers the Synthetic Rubber Market historical market size for years: . The report also forecasts the Synthetic Rubber Market size for years: 2024, 2025, 2026, 2027, 2028 and 2029.

Synthetic Elastomers Industry Report

Statistics for the 2024 Synthetic Elastomers market share, size and revenue growth rate, created by Mordor Intelligence™ Industry Reports. Synthetic Elastomers analysis includes a market forecast outlook to 2029 and historical overview. Get a sample of this industry analysis as a free report PDF download.