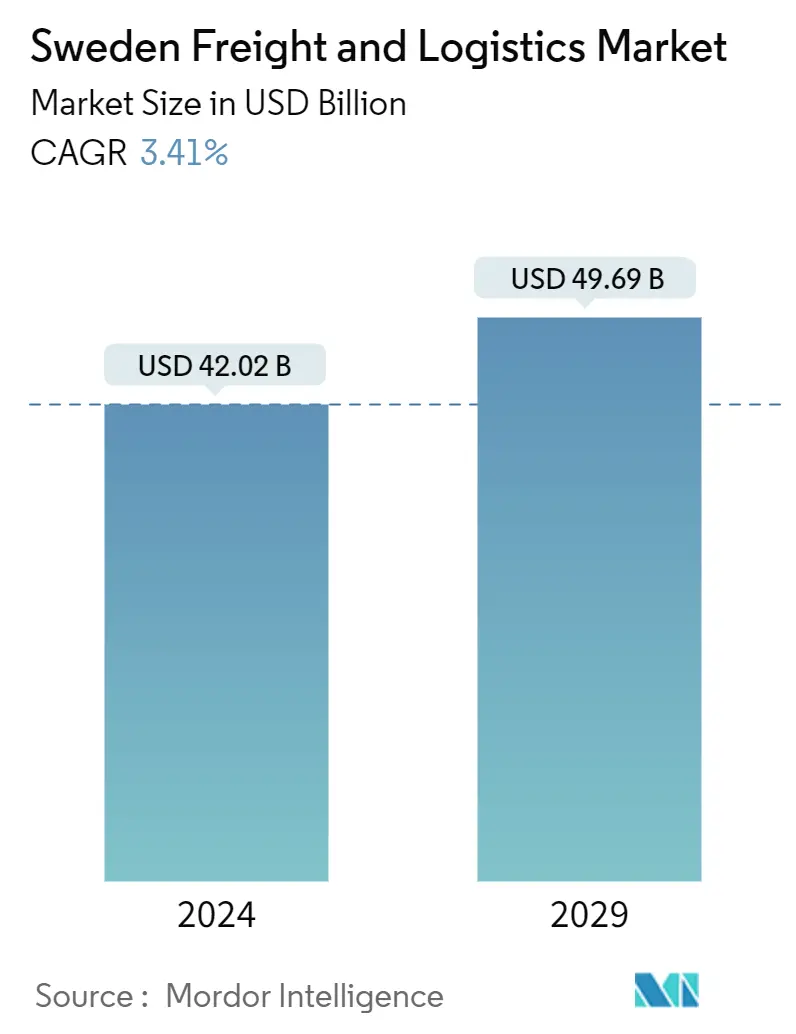

Sweden Logistics Market Size

| Study Period | 2020-2029 |

| Base Year For Estimation | 2023 |

| Market Size (2024) | USD 42.02 Billion |

| Market Size (2029) | USD 49.69 Billion |

| CAGR (2024 - 2029) | 3.41 % |

| Market Concentration | Low |

Major Players

*Disclaimer: Major Players sorted in no particular order |

Need a report that reflects how COVID-19 has impacted this market and its growth?

Sweden Logistics Market Analysis

The Sweden Freight And Logistics Market size is estimated at USD 42.02 billion in 2024, and is expected to reach USD 49.69 billion by 2029, growing at a CAGR of 3.41% during the forecast period (2024-2029).

- The logistics market in Sweden is the largest in the Scandinavian region. Investments in infrastructure have made the country one of the top logistics markets in Europe and the World. The central location in the region makes it the preferred choice for companies that are looking to consolidate distribution and warehousing activities in Northern Europe into one central location. Foreign companies use some 10 Swedish locations for centralized distribution in Northern Europe.

- The Swedish economy is highly dependent on exports of goods. The strong cross-border impacts on the transportation industry and logistics market. Gothenburg is a leading logistics location in the country, supported by the Port of Gothenburg and new logistics establishments. The Port of Gothenburg has a 53% share of the Swedish container market, which is an increase of three percentage points compared with the first half of 2021. The Port of Gothenburg also increased its market share for containers compared with nearby major ports in Northern Europe.

- 10% of consumers indicated that they had made online purchases from outside of Sweden, with six out of ten of these purchases originating in Germany, China, and the United Kingdom. Germany has experienced a surge in online shopping from Sweden, with 32% of online purchases originating from outside of the country, second only to China at 15%. Germany is particularly popular due to its automotive industry, which produces a substantial amount of affordable spare parts and accessory imports.

- The cleantech, ICT, life sciences, automotive, and materials science industries are some emerging industries in Sweden. E-commerce and retail are also fast-growing sectors in the country, which are expected to boost the logistics demand, especially in the warehousing sector.

Sweden Logistics Market Trends

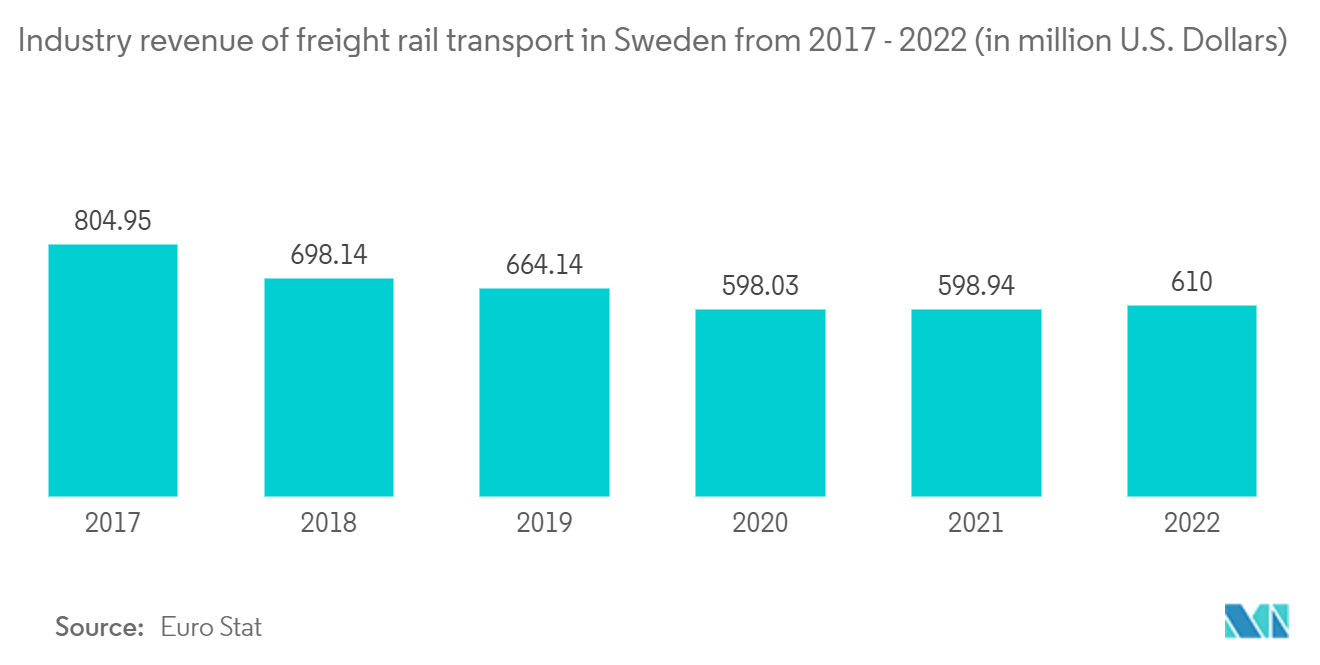

Growth in the rail freight segment

The share of new entrants in the Swedish rail freight sector has significantly increased. The vertical separation of the Swedish rail industry between infrastructure and train operations is often regarded as highly successful, bringing the benefits of competition. The Swedish government has established that new main lines are needed between Stockholm, Gothenburg, and Malmö. To increase opportunities for sustainable and reliable passenger and freight transport by rail, the Swedish Transport Administration is planning and building new main lines. The new main lines will be made in stages, with the first three being the East Link, Gothenburg–Borås, and Hässleholm–Lund.

The rail freight sector in the country faces high competition from the road freight industry. The Shift2Rail initiative is based on digitalization, enabling various levels of automation and intelligence in the rail system, and it involves an investment of about SEK 8 million (USD 0.76 million). Multimodality is a required field where also ITS solutions/applications are developed. More than 60% of the containers handled in the port are transported by rail, and around 70 trains arrive and depart from the Port of Gothenburg daily. Also, the rail-port intermodal concept of the port contributes to significant emission reduction. One subproject is about intelligent video gates (IVG) capturing data with the help of optics and RFID, enabling better information sharing and operational planning in, e.g., intermodal terminals.

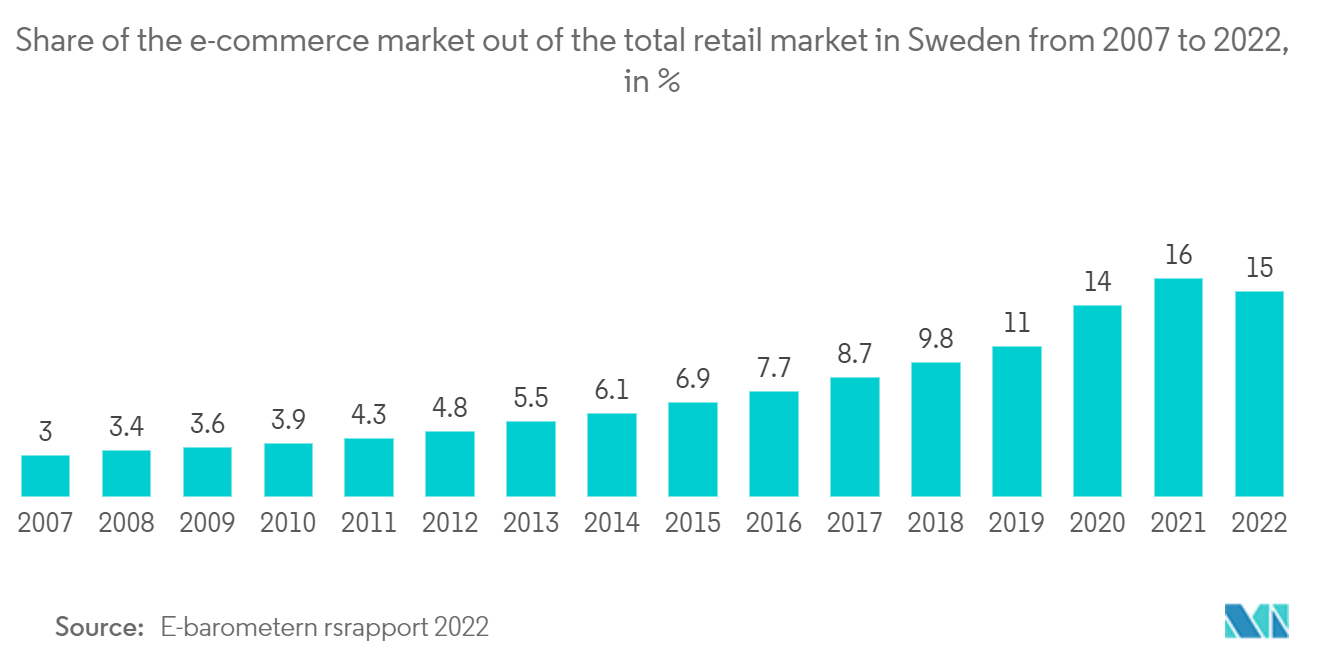

Growing e-commerce accelerating the demand for logistics facilities

E-commerce revenue in Sweden in 2022 was estimated to be around 136 billion kronor (USD 12.24 billion), which is more than 12 billion euros (USD 12.86 billion) in comparison to the previous year. User penetration stood at the level of 74.8%, and by the end of 2025, it is expected to hit 81.8%. About 8 million people shop online in Sweden, which is quite a lot considering that the country has only ten million people. This means that many Swedes depend on digital commerce to fulfill their shopping needs. Online shopping is convenient because it is available 24 hours a day, 7 days a week, and at lower prices than in-person shopping.

According to e-commerce demographics, geography, age, and income play a role in online shopping. Younger generations purchased more online in 2022 than older generations did in the past. Women aged 25-34 bought the most online, while older men aged 35-44 did the same. All eight national regions were highly familiar with online shopping. However, Western Sweden has the largest number of online shoppers. When we look at income levels, we see that the higher your disposable income, the more likely you are to shop online. More than 80 percent of shoppers who had the highest disposable income bought online, compared to 55 percent who had the lowest disposable income.

Sweden Logistics Industry Overview

Sweden's freight and logistics market is fragmented, with many international and domestic players active. The distribution network comprises many freight forwarders and third-party logistics (3PL) companies. Some prominent players in the market include DHL, DB Schenker, DSV, Greencarrier, Geodis, and PostNord.Technologies such as automation, Big Data, and analytics are expected to play a significant role in the Swedish logistics market.

Sweden Logistics Market Leaders

Deutsche Post DHL Group

DB Schenker

DSV A/S

Greencarrier AB

Cool Carriers AB

*Disclaimer: Major Players sorted in no particular order

Sweden Logistics Market News

- August 2023: DHL and Volvo have joined forces to accelerate the deployment of electric heavy-duty trucks for regional transport across Europe. The partnership marks another significant step towards climate-friendly transport solutions. Until now, electric trucks have only been used for short distances within urban areas. DHL and Volvo have launched a project focused on long-distance heavy transport. This project includes exclusive, world-first pilot tests of Volvo FH trucks with gross combined weights of 60 tonnes. From March, the Volvo FH trucks will be deployed between DHL’s logistics terminals located in Sweden, covering an approximate 150 km one-way distance.

- June 2022: CEVA Logistics opened a new 14,000-square-meter facility in the Philippines earlier this month as the company looks to enhance its capabilities for the Southeast Asian market. The warehouse will serve the electronics and F&B sector with a full range of warehousing, distribution, and value-added services, including picking and packing, labeling, bundling, re-work, tax stamping, and digital bottle printing.

- April 2022: French rolling stock manufacturer Alstom won a EUR 650 million (USD 685.88 million) contract from Swedish national rail operator SJ to deliver 25 Zefiro Express electric high-speed trains. The agreement also includes an option to supply a further 15 trains. Zefiro Express electric high-speed trains are slated to be delivered in 2026.

Sweden Logistics Market Report - Table of Contents

1. INTRODUCTION

1.1 Study Assumptions and Market Definition

1.2 Scope of the Study

2. RESEARCH METHODOLOGY

2.1 Analysis Methodology

2.2 Research Phases

3. EXECUTIVE SUMMARY

4. MARKET DYNAMICS AND INSIGHTS

4.1 Current Market Scenario

4.2 Market Dynamics

4.2.1 Market Drivers

4.2.1.1 Growth In E-commerce is driving the market

4.2.1.2 Growing in Cross Border Activities is driving the market

4.2.2 Market Restraints

4.2.2.1 Shortage of Skilled labor

4.2.3 Market Opportunities

4.2.3.1 Technological Innovation

4.3 Industry Attractiveness - Porter's Five Forces Analysis

4.3.1 Brgaining Power of Supplierrs

4.3.2 Bargaining Power of Buyers/Consumers

4.3.3 Threat of New Entrants

4.3.4 Threat of Substitute Products

4.3.5 Intensity of Competitive Rivalry

4.4 Value Chain/Supply Chain Analysis

4.5 Government Regulations and Initiatives

4.6 Technological Trends

4.7 Insights into the E-commerce Industry (Domestic and Cross-border E-commerce)

4.8 Insights into Intermodal Transportation and Dry Ports

4.9 Brief on Freight Transportation Costs/Freight Rates, Warehousing Rents in Sweden

4.10 Brief on Transport Corridors

4.11 Spotlight on Logistics Markets in Key Cities of Sweden (Gothenburg, Helsingborg, Stockholm, etc.)

4.12 Impact of COVID-19 on the Market

5. MARKET SEGMENTATION

5.1 By Function

5.1.1 Freight Transport

5.1.1.1 Road

5.1.1.2 Shipping and Inland Water

5.1.1.3 Air

5.1.1.4 Rail

5.1.2 Freight Forwarding

5.1.3 Warehousing

5.1.4 Value-added Services and Other Functions

5.2 By End User

5.2.1 Manufacturing and Automotive

5.2.2 Oil and Gas, Mining, and Quarrying

5.2.3 Agriculture, Fishing, and Forestry

5.2.4 Construction

5.2.5 Distributive Trade (Wholesale and Retail Segments - FMCG included)

5.2.6 Other End Users (Telecommunications, Food and Beverage, and Pharmaceuticals)

6. COMPETITIVE LANDSCAPE

6.1 Market Concentration Overview

6.2 Company Profiles

6.2.1 Deutsche Post DHL Group

6.2.2 DB Schenker

6.2.3 DSV AS

6.2.4 Greencarrier AB

6.2.5 Geodis

6.2.6 PostNord AB

6.2.7 GDL Transport AB

6.2.8 MaserFrakt AB

6.2.9 United Parcel Service Inc.

6.2.10 Kuehne + Nagel International AG

6.2.11 Cool Carriers AB

6.2.12 CEVA Logistics

6.2.13 Fraktkedjan*

- *List Not Exhaustive

6.3 Other Companies (Key Information/Overview)

6.3.1 Posten Norge, Ceva Logistics, Agility Logistics Pvt. Ltd, Hellmann Worldwide Logistics, Foria AB, Hector Rail AB, DFDS, Marsta Forenade Akeriforetag AB, Scandfibre Logistics AB, Reaxcer AB, Alwex Transport AB, Aditro Logistics AB, Scan Global Logistics A/S, Spedman Global Logistics, Godecke Logistics, Exacta, and Avatar Logistics AB

7. FUTURE O F THE MARKET

8. APPENDIX

8.1 GDP Distribution, by Activity and Region

8.2 Insights into Capital Flows

8.3 Economic Statistics - Transport and Storage Sector, Contribution to Economy

8.4 External Trade Statistics - Export and Import, by Product

8.5 Insights into Key Export Destinations

8.6 List of Prospective Clients for Logistics Service Providers

Sweden Logistics Industry Segmentation

Freight and logistics involve road, rail, sea, and air transportation and supporting services such as warehousing, storage, freight forwarding, and customs brokerage for domestic and international trade. The report provides a complete background analysis of the Swedish freight and logistics market, which includes an assessment of the economy, a market overview, market size estimation for critical segments, emerging trends in the market, market dynamics, and key company profiles covered in the report. The report also covers the impact of COVID-19 on the market.

The Swedish freight and logistics market is segmented by function (freight transport, freight forwarding, warehousing, value-added services, and other functions) and end-user (manufacturing and automotive, oil and gas, mining, and quarrying, agriculture, fishing, and forestry, construction, distributive trade (wholesale and retail segments - FMCG included), and other end users (telecommunications, pharmaceuticals, etc.).

The report offers market size and forecasts for the Sweden freight & logistics market in value (USD) for all the above segments.

| By Function | ||||||

| ||||||

| Freight Forwarding | ||||||

| Warehousing | ||||||

| Value-added Services and Other Functions |

| By End User | |

| Manufacturing and Automotive | |

| Oil and Gas, Mining, and Quarrying | |

| Agriculture, Fishing, and Forestry | |

| Construction | |

| Distributive Trade (Wholesale and Retail Segments - FMCG included) | |

| Other End Users (Telecommunications, Food and Beverage, and Pharmaceuticals) |

Sweden Logistics Market Research FAQs

How big is the Sweden Freight And Logistics Market?

The Sweden Freight And Logistics Market size is expected to reach USD 42.02 billion in 2024 and grow at a CAGR of 3.41% to reach USD 49.69 billion by 2029.

What is the current Sweden Freight And Logistics Market size?

In 2024, the Sweden Freight And Logistics Market size is expected to reach USD 42.02 billion.

Who are the key players in Sweden Freight And Logistics Market?

Deutsche Post DHL Group, DB Schenker, DSV A/S, Greencarrier AB and Cool Carriers AB are the major companies operating in the Sweden Freight And Logistics Market.

What years does this Sweden Freight And Logistics Market cover, and what was the market size in 2023?

In 2023, the Sweden Freight And Logistics Market size was estimated at USD 40.59 billion. The report covers the Sweden Freight And Logistics Market historical market size for years: 2020, 2021, 2022 and 2023. The report also forecasts the Sweden Freight And Logistics Market size for years: 2024, 2025, 2026, 2027, 2028 and 2029.

Sweden Logistics Industry Report

Statistics for the 2024 Sweden Logistics market share, size and revenue growth rate, created by Mordor Intelligence™ Industry Reports. Sweden Logistics analysis includes a market forecast outlook to 2029 and historical overview. Get a sample of this industry analysis as a free report PDF download.