Styrenic Block Copolymers Market Size

| Study Period | 2019 - 2029 |

| Base Year For Estimation | 2023 |

| CAGR | < 4.00 % |

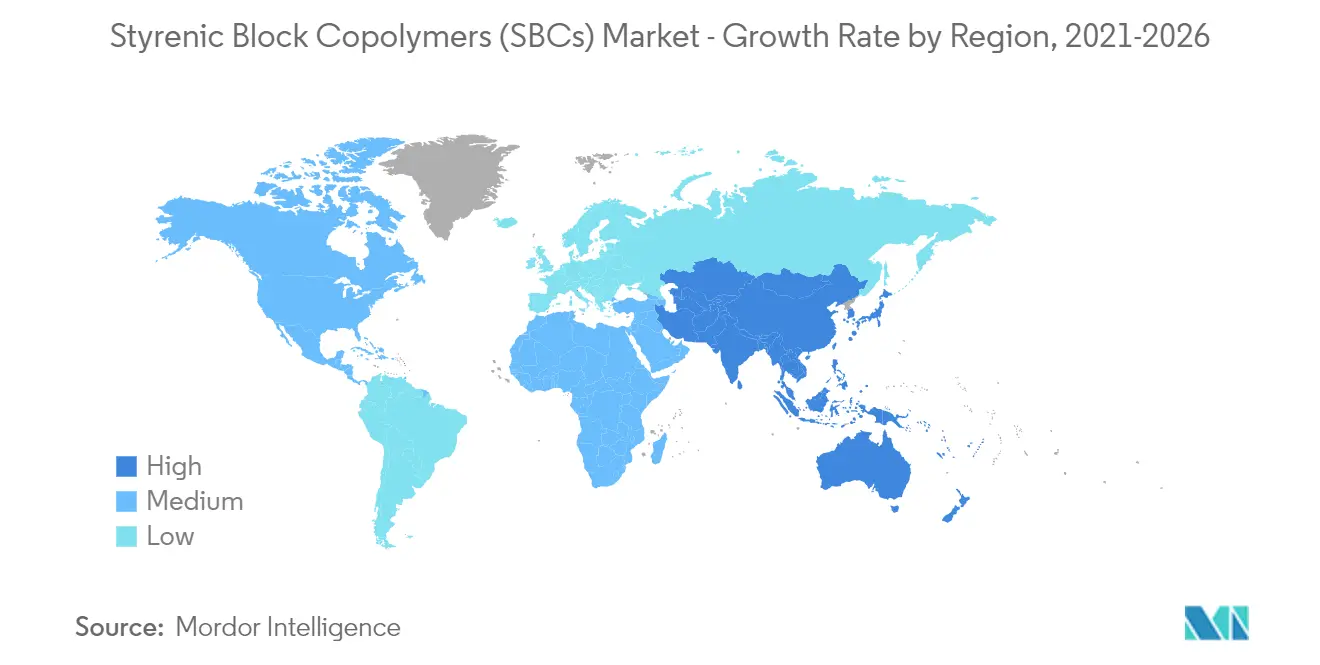

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | High |

Major Players_Market_-_Key_Players.webp)

*Disclaimer: Major Players sorted in no particular order |

Need a report that reflects how COVID-19 has impacted this market and its growth?

Styrenic Block Copolymers Market Analysis

The styrenic block copolymers (SBCs) market size was estimated at over 2.3 million metric ton in 2020, and the market is projected to register a CAGR of below 4% during the forecast period (2021-2026).

The market was negatively impacted by COVID-19 in 2020. Considering the pandemic scenario, the building and construction activities were stopped temporarily during the lockdown in order to curb the spread of the new COVID-19 cases. For instance, according to Eurostat, the construction industry declined by 28.4% in the EU-19 countries and by 24% in the European Union (EU-27) countries, thereby witnessing a reduction in demand for styrene-butadiene-styrene (SBS) in roofing felt and shingle applications and SBC-based adhesives and sealants in different construction activities. However, the demand for SBC-based medical bags, containers, tubings, medical beds, and others had been increased during the pandemic situation, thereby enhanced the demand for the market studied.

- Over the short term, the increasing applications of styrene block copolymers in bitumen modification, which are majorly used in road making and construction applications, are expected to drive the market's growth. Modified bitumen performs better than conventional bitumen in situations where the aggregates are prone to stripping. Due to its better creep resistance properties, it can also be used at busy intersections, bridge decks, and roundabouts for increased life of the surfacing.

- On the flipside, substitutes such as thermoplastic polyurethane and thermoplastic polyolefin elastomers are posing competition to SBCs in various applications.

- Development and introduction of new products with better properties and growth opportunities in hot-melt adhesives are likely to act as the opportunity for the market in the future.

- Asia-Pacific dominated the market studied, and the region is expected to witness the highest CAGR during the forecast period.

Styrenic Block Copolymers Market Trends

This section covers the major market trends shaping the Styrenic Block Copolymers Market according to our research experts:

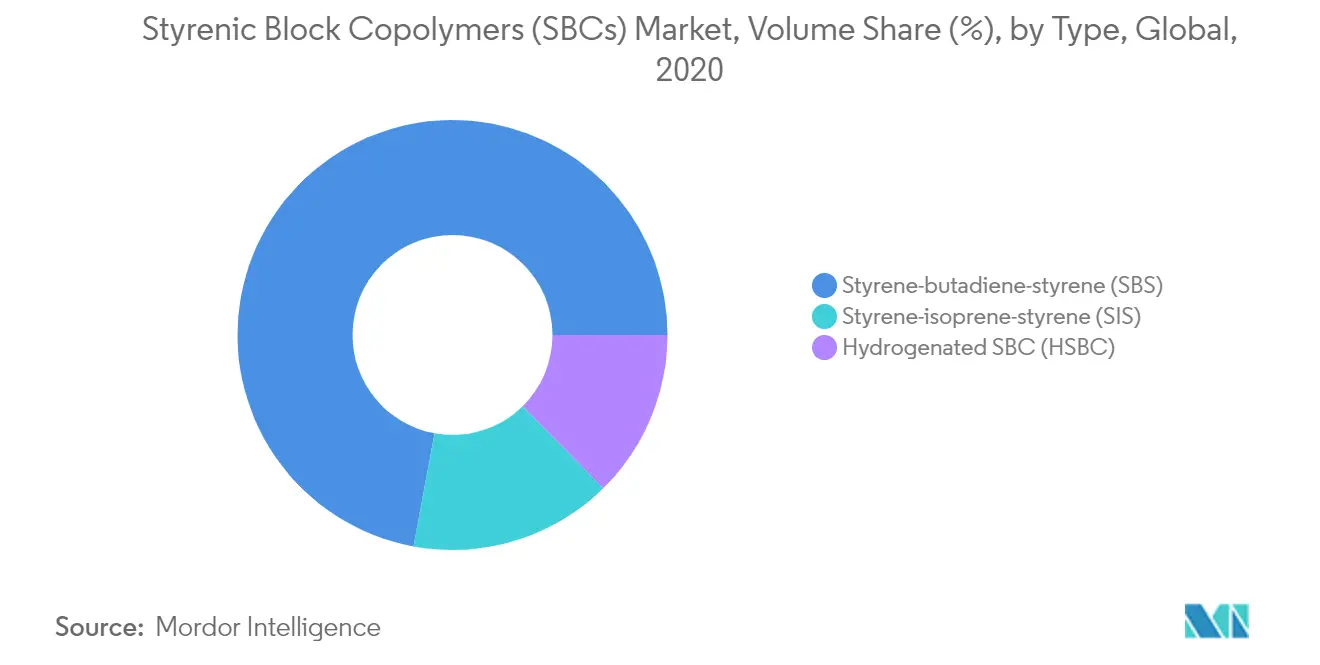

Styrene-butadiene-styrene (SBS) Segment to Dominate the Market

- SBS accounts for the largest share, in terms of production and demand, among the different types of styrene block copolymers. It is basically a thermoplastic elastomer consisting of styrene and butadiene monomers.

- SBS holds the advantages of properties achieved from both polystyrene and butadiene. The polybutadiene chains in the structure allow the material to be stretched and get back to its normal state. On the other hand, the polystyrene composition in the structure gives it the required durability. SBS elastomers are not suitable for continuous usage in the ultraviolet (UV) and ozone conditions.

- These properties make SBS ideal for usage in applications, such as road pavement, plastic modification, adhesives, and footwear.

- Asphalt modification applications involve the addition of small amounts of SBS, approximately 2-6% by weight to asphalt used in road paving and around 11% by weight in roofing felts and shingles, to enhance the properties of the end product. The increased cost of installing SBS-enhanced asphalt is offset by future maintenance savings and the benefit of less disruption due to the increased durability.

- In 2019, the new highway and street construction put in place was valued at about USD 97.56 billion in the United States, and it is estimated to reach about USD 107.74 billion by 2024, registering a CAGR of about 2%. Thus, this is expected to enhance the demand for SBS from the highway and street construction sector.

- Furthermore, the expenditure of airport runway construction in the United States was valued at about USD 4.7 billion in 2019 and reached about USD 5.7 billion in 2020, with a growth rate of about 21%, thus enhanced the demand for the market studied.

- Moreover, the total value of new construction in the United States was about USD 1,365 billion in 2019 and reached about USD 1,430 billion in 2020, with a growth rate of about 4.5%, increasing the demand for SBS in roofing felt and shingle applications.

- The consumption of SBS might witness a slight decline for polymer modification applications, owing to the increasing usage of PET in food packaging and other applications in the current scenario.

- Despite having higher tensile strength than SBR rubber, SBS materials possess lower heat resistance on a relative scale. Oil extended SBS is witnessing an increase in terms of production as compared to dry SBS in recent times.

- Therefore, the aforementioned factors are expected to show a significant impact on the market in the coming years.

China to Dominate the Asia-Pacific Market

- In the Asia-Pacific region, China is the largest economy in terms of GDP. The country witnessed about 6.1% growth in its GDP during 2019, even after the trade disturbance caused due to its trade war with the United States. The economic growth rate of China in 2020 was initially expected to be moderate as compared to the previous year. However, due to the onset of COVID-19, in 2020, the economic growth of China was estimated to contract to 1.90%, and it is expected to witness recovery at a rate of 8.20% in 2021.

- The construction industry grew at a strong pace in 2019, even though the growth slowed down during the year compared to 2018. The construction sector supported the economic growth in the country, while the US-China trade war affected the performance in other industries, such as automotive.

- China's 13th Five Year Plan started in 2016 (2016-2021), and it was an important year for the country's engineering, procurement, and construction (EPC) industries. In addition, the country ventured into new business models domestically and internationally during the year. Although the construction sector slowed down after 2013, it is still a major contributor to the GDP of the country.

- According to the National Bureau of Statistics of China, the revenue generated by the Chinese construction industry increased from CNY 17.67 trillion in 2014 to CNY 24.84 trillion in 2019. The Chinese construction industry was valued at about USD 1,049.2 billion in 2020, and it is estimated to reach about USD 1,117.4 billion by 2021, with a growth rate of about 6.5%.

- Furthermore, China planned to invest about USD 21.43 billion for the construction of 30 new expressway links with a total length of 2,109 km in Guangxi Province, which will be completed by the end of 2021. Thus, this is expected to enhance the demand for the market studied.

- Owing to the huge footwear manufacturing industry, China accounts for over 45% of the total SBS produced around the world. India and Thailand are other key footwear markets in the region, where the demand for SBC is expected to witness positive growth.

- The Chinese footwear industry was valued at about USD 64.78 billion in 2019, and it is estimated to reach about USD 86.05 billion by 2024, with a CAGR of about 6%. Thus, this is expected to enhance the demand for the SBC.

- Therefore, the aforementioned factors are expected to show a significant impact on the styrenic block copolymers (SBCs) market in the coming years.

Styrenic Block Copolymers Industry Overview

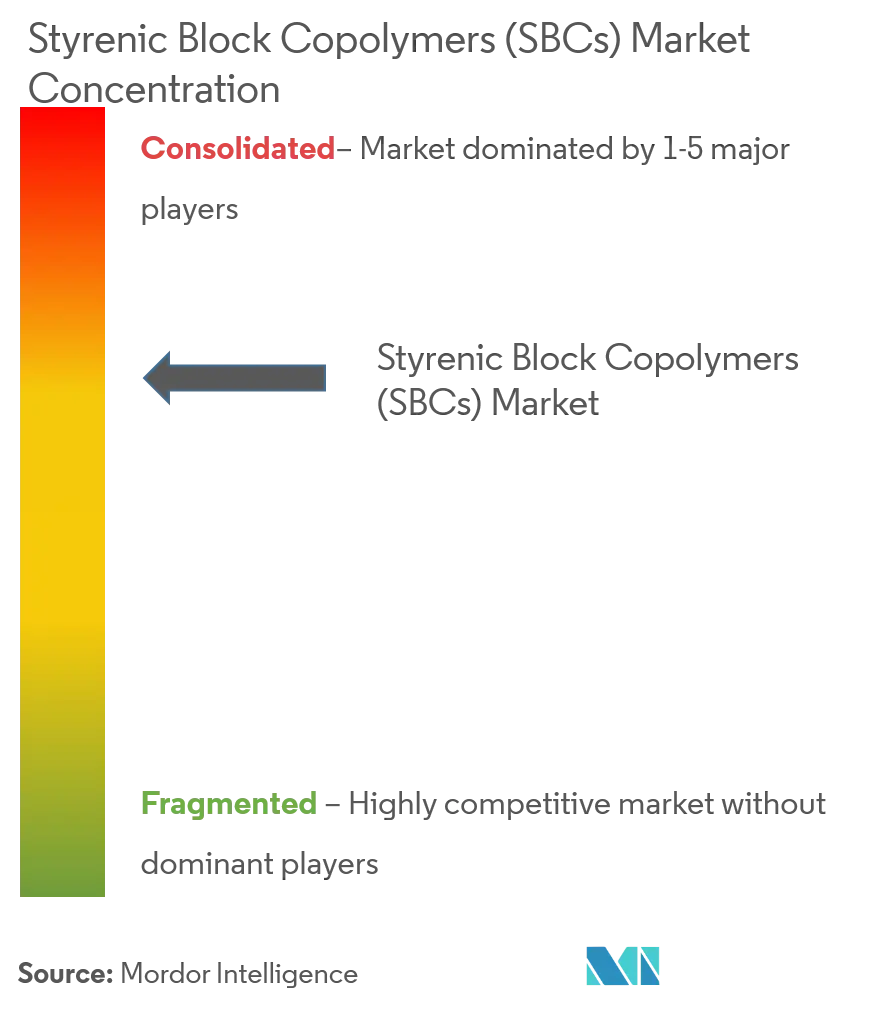

The styrenic block copolymers (SBCs) market is partially consolidated, and the top five players accounted for over 60% of the global market in terms of production capacity. Some of the key players in the global market include KRATON CORPORATION, Grupo Dynasol, TSRC, LCY GROUP, and China Petrochemical Corporation (SINOPEC), among others.

Styrenic Block Copolymers Market Leaders

Grupo Dynasol

TSRC

LCY GROUP

KRATON CORPORATION

China Petrochemical Corporation (SINOPEC)

*Disclaimer: Major Players sorted in no particular order

Styrenic Block Copolymers Market News

- In January 2019, KURARAY CO. LTD, PTT Global Chemical Public Company Limited, and Sumitomo Corporation decided to invest in a project for manufacturing butadiene derivatives, including thermoplastic elastomers in Thailand. The project will be operated by a joint venture called Kuraray GC Advanced Materials Co. Ltd, with an annual production capacity of 16 kilotons of TPEs based on hydrogenated stryenic block copolymers.

Styrenic Block Copolymers Market Report - Table of Contents

1. INTRODUCTION

1.1 Study Assumptions

1.2 Scope of the Study

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET DYNAMICS

4.1 Drivers

4.1.1 Increasing Application in Bitumen Modification

4.1.2 Other Drivers

4.2 Restraints

4.2.1 Unfavorable Conditions Arising Due to the COVID-19 Outbreak

4.2.2 Other Restraints

4.3 Industry Value Chain Analysis

4.4 Porter's Five Forces Analysis

4.4.1 Bargaining Power of Suppliers

4.4.2 Bargaining Power of Consumers

4.4.3 Threat of New Entrants

4.4.4 Threat of Substitute Products and Services

4.4.5 Degree of Competition

4.5 Price Analysis

4.6 Technological Snapshot

4.7 Feedstock Analysis

5. MARKET SEGMENTATION

5.1 Type

5.1.1 Styrene-butadiene-styrene (SBS)

5.1.2 Styrene-isoprene-styrene (SIS)

5.1.3 Hydrogenated SBC (HSBC)

5.2 Application

5.2.1 Asphalt Modification (Paving and Roofing)

5.2.2 Footwear

5.2.3 Polymer Modification

5.2.4 Adhesives and Sealants

5.2.5 Other Applications (Medical Devices and Wires and Cables)

5.3 Geography

5.3.1 Asia-Pacific

5.3.1.1 China

5.3.1.2 India

5.3.1.3 Japan

5.3.1.4 South Korea

5.3.1.5 ASEAN Countries

5.3.1.6 Rest of Asia-Pacific

5.3.2 North America

5.3.2.1 United States

5.3.2.2 Canada

5.3.2.3 Mexico

5.3.3 Europe

5.3.3.1 Germany

5.3.3.2 United Kingdom

5.3.3.3 France

5.3.3.4 Italy

5.3.3.5 Rest of Europe

5.3.4 South America

5.3.4.1 Brazil

5.3.4.2 Argentina

5.3.4.3 Rest of South America

5.3.5 Middle-East and Africa

5.3.5.1 Saudi Arabia

5.3.5.2 South Africa

5.3.5.3 Rest of Middle-East and Africa

6. COMPETITIVE LANDSCAPE

6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

6.2 Market Share (%)**/Ranking Analysis

6.3 Strategies Adopted by Leading Players

6.4 Company Profiles

6.4.1 Asahi Kasei Corporation

6.4.2 Avient Corporation

6.4.3 China Petrochemical Corporation (SINOPEC)

6.4.4 Grupo Dynasol

6.4.5 INEOS

6.4.6 JSR Corporation

6.4.7 KRATON CORPORATION

6.4.8 KURARAY CO. LTD

6.4.9 LCY GROUP

6.4.10 LG Chem

6.4.11 TSRC

6.4.12 ZEON CORPORATION

- *List Not Exhaustive

7. MARKET OPPORTUNITIES AND FUTURE TRENDS

7.1 Introduction of New Products with Better Properties

7.2 Growth Opportunities in Hot-melt Adhesives

7.3 Other Opportunities

Styrenic Block Copolymers Industry Segmentation

Styrenic block copolymers (SBCs) are a class of thermoplastic elastomers, which processes like plastic and behave like rubber, mainly due to the physical crosslink inherent in the SBC structure. When the SBC material is stretched, those crosslinks bring it back to its original shape. SBCs can be made up of butadiene, styrene, and isoprene raw materials. They have a two-phase structure composed of hard polystyrene end blocks and soft rubber mid-locks. SBCs find their major application in asphalt modification, rigid thermoplastic impact modification, production of soft plastic elastomer, and others. By type, the market is segmented into styrene-butadiene-styrene (SBS), styrene-isoprene-styrene (SIS), and hydrogenated SBC (HSBC). By application, the market is segmented into asphalt modification, footwear, polymer modification, adhesives and sealants, and other applications. The report also covers the market size and forecasts for the styrenic block copolymers (SBCs) market in 16 countries across major regions. For each segment, the market sizing and forecasts have been done on the basis of volume (kilo tons).

| Type | |

| Styrene-butadiene-styrene (SBS) | |

| Styrene-isoprene-styrene (SIS) | |

| Hydrogenated SBC (HSBC) |

| Application | |

| Asphalt Modification (Paving and Roofing) | |

| Footwear | |

| Polymer Modification | |

| Adhesives and Sealants | |

| Other Applications (Medical Devices and Wires and Cables) |

| Geography | ||||||||

| ||||||||

| ||||||||

| ||||||||

| ||||||||

|

Styrenic Block Copolymers Market Research FAQs

What is the current Styrenic Block Copolymers (SBCs) Market size?

The Styrenic Block Copolymers (SBCs) Market is projected to register a CAGR of less than 4% during the forecast period (2024-2029)

Who are the key players in Styrenic Block Copolymers (SBCs) Market?

Grupo Dynasol, TSRC, LCY GROUP, KRATON CORPORATION and China Petrochemical Corporation (SINOPEC) are the major companies operating in the Styrenic Block Copolymers (SBCs) Market.

Which is the fastest growing region in Styrenic Block Copolymers (SBCs) Market?

Asia Pacific is estimated to grow at the highest CAGR over the forecast period (2024-2029).

Which region has the biggest share in Styrenic Block Copolymers (SBCs) Market?

In 2024, the Asia Pacific accounts for the largest market share in Styrenic Block Copolymers (SBCs) Market.

What years does this Styrenic Block Copolymers (SBCs) Market cover?

The report covers the Styrenic Block Copolymers (SBCs) Market historical market size for years: 2019, 2020, 2021, 2022 and 2023. The report also forecasts the Styrenic Block Copolymers (SBCs) Market size for years: 2024, 2025, 2026, 2027, 2028 and 2029.

Styrenic Block Copolymers (SBCs) Industry Report

Statistics for the 2024 Styrenic Block Copolymers (SBCs) market share, size and revenue growth rate, created by Mordor Intelligence™ Industry Reports. Styrenic Block Copolymers (SBCs) analysis includes a market forecast outlook to 2029 and historical overview. Get a sample of this industry analysis as a free report PDF download.