Market Overview

| Study Period | 2020 - 2030 |

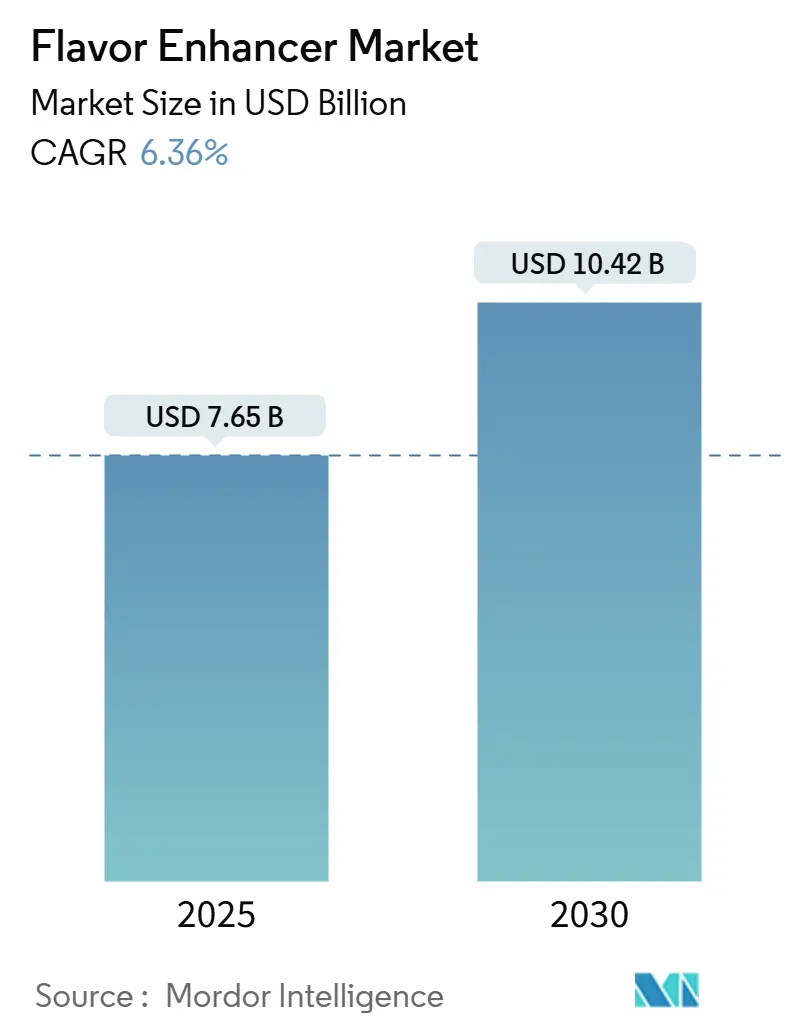

| Market Size (2025) | USD 7.65 Billion |

| Market Size (2030) | USD 10.42 Billion |

| Growth Rate (2025 - 2030) | 6.36% CAGR |

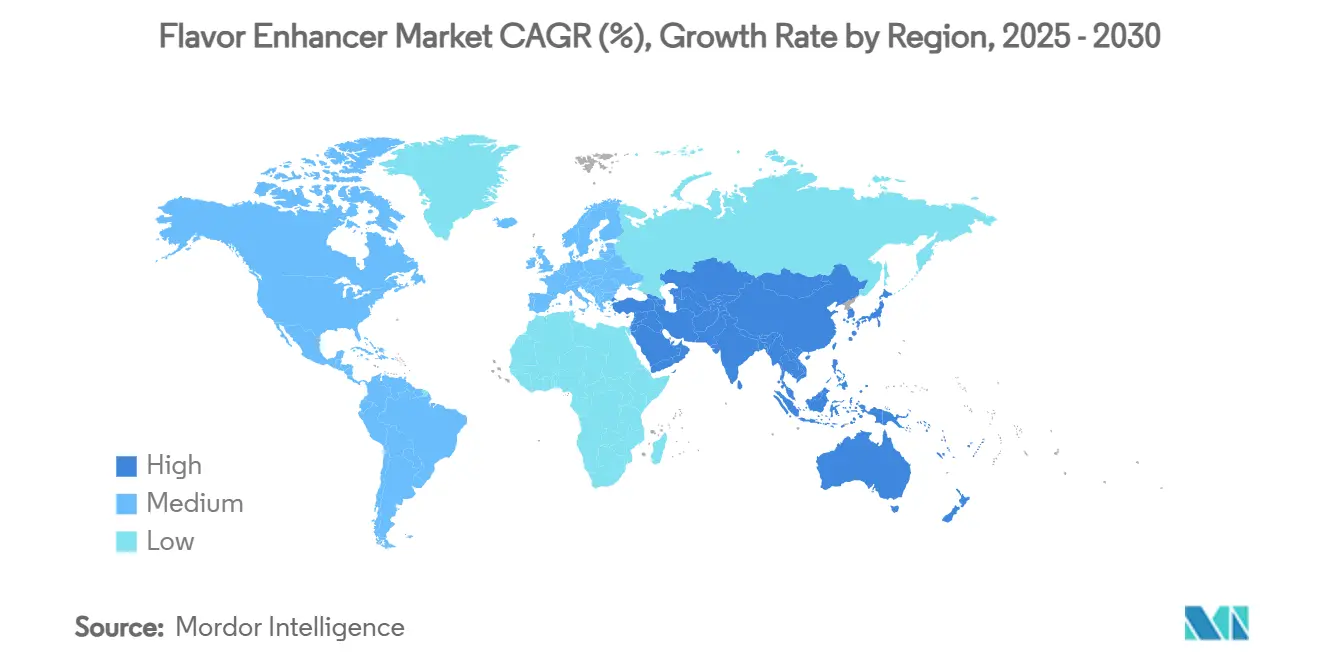

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Flavor Enhancer Market Analysis by Mordor Intelligence

The flavor enhancers market size is valued at USD 7.65 billion in 2025 and is forecast to climb to USD 10.42 billion by 2030, advancing at a solid 6.36% CAGR. This growth trajectory is underpinned by evolving preferences, rising demand for convenience and processed food products, and a significant shift toward natural and clean-label ingredients. The Asia-Pacific region emerges as the largest contributor to global revenue and is anticipated to exhibit the fastest growth during the forecast period. Glutamates continue to dominate the flavor enhancers market; however, yeast extracts are gaining traction as manufacturers increasingly prioritize cleaner-label formulations to align with consumer expectations. In the beverage segment, developers are accelerating the adoption of advanced flavor enhancers to effectively mask botanical off-notes while delivering distinctive and signature taste profiles. In North America and Europe, stringent regulations on food additives are compelling multinational companies to reformulate their products to ensure compliance with global standards. Concurrently, regional players are leveraging localized flavor preferences to establish and strengthen niche market positions.

Key Report Takeaways

- By type, glutamates commanded 41.43% of the flavor enhancers market share in 2024, whereas yeast extracts are on track for a 7.24% CAGR to 2030.

- By application, savory snacks accounted for 33.76% of the flavor enhancers market size in 2024; beverages are positioned to expand at a 6.60% CAGR through 2030.

- By form, liquid products led with 39.24% revenue share in 2024, also liquid is slated to post the quickest 7.43% CAGR between 2025-2030.

- By geography, Asia-Pacific held 28.34% of global revenue in 2024 and is projected to widen its lead at a 7.96% CAGR by 2030.

Global Flavor Enhancer Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing consumption of convenience food products | +1.4% | Global urban centers | Medium term (2-4 years) |

| Consumer preference for bold and unique flavors | +1.2% | North America, Europe, Asia-Pacific | Long term (≥ 4 years) |

| Growing demand for monosodium glutamate (MSG) as a flavor enhancer in food products | +0.9% | North America, Asia-Pacific | Long term (≥ 4 years) |

| Low cost and wide availability associated with flavor enhancers | +0.8% | Emerging markets | Short term (≤ 2 years) |

| Rising demand for processed and packaged foods | +0.6% | Global | Short term (≤ 2 years) |

| Increasing application of flavor enhancers in the beverage industry | +0.4% | North America, Asia-Pacific | Medium term (2-4 years) |

Source: Mordor Intelligence

Growing Consumption of Convenience Food Products

With the growing preference for convenience foods, particularly in urban areas, the flavor enhancers market is undergoing significant transformation. Manufacturers are increasingly prioritizing the development of solutions that ensure the preservation of taste quality while extending product shelf life. This shift is driven by the rising demand for ready-to-eat meals and processed foods among time-constrained consumers. In India, this trend is reflected in the consistent growth of the Wholesale Price Index (WPI) for processed, ready-to-eat foods, which increased from 141.2 in 2023 to 146.3 in 2024, as per data from the Office of Economic Advisers[1]Source: Office of Economic Adviser' "Annual Average of Monthly Index" www.eaindustry.nic.in. However, the competitive nature of the market presents an additional challenge for manufacturers: creating distinctive and appealing flavor profiles that enable their products to stand out. To address this, companies are adopting advanced flavor systems that combine traditional enhancers, such as MSG, with innovative alternatives. For example, yeast extracts are being utilized to deliver rich umami flavors while adhering to clean-label requirements, thereby meeting evolving consumer preferences.

Consumer Preference for Bold and Unique Flavors

The growing consumer demand for flavor enhancers reflects a pursuit of complex and authentic sensory experiences. This trend spans various demographics, with younger consumers showing a strong inclination toward globally-inspired flavor profiles. In 2024, China's processed food sector saw a 2.2% growth, reaching USD 1.26 trillion, according to the United States Department of Agriculture[2]Source: United States Department of Agriculture, "China: Food Processing Ingredients Annual", www.fas.usda.gov, exemplifying this shift, with consumers favoring hot, spicy, and smoked flavors. These evolving preferences extend beyond taste, representing cultural dynamics as consumers leverage food choices to express identity and explore new experiences. In response, flavor enhancer manufacturers are developing advanced compounds that replicate authentic regional profiles while ensuring stability across diverse food applications. As consumer preferences shift toward bolder profiles such as tangy, fermented, spicy, or smoky, companies are reformulating existing products or launching new variants. The flavor enhancer suppliers are facilitating these reformulations by delivering tailored ingredient systems designed to meet both sensory and technical requirements, including flavor retention during processes like baking or frying.

Growing Demand for Monosodium Glutamate (MSG) as a Flavor Enhancer in Food Products

MSG has solidified its leadership position in the Flavor Enhancers industry by offering a highly effective umami flavor at an exceptionally low cost, just fractions of a cent per serving. This unparalleled cost-to-impact efficiency remains a significant competitive advantage. Ajinomoto is strategically repositioning MSG, traditionally perceived as a mere additive, as a contributor to health and wellness, with a particular focus on its potential to aid in sodium reduction. This repositioning has encouraged several U.S. school districts to discreetly incorporate MSG into their reduced-sodium meal formulations. Furthermore, recent sensory research has demonstrated that MSG, when combined with potassium chloride, effectively neutralizes the metallic aftertaste associated with the latter. This breakthrough provides product formulators with an innovative solution for salt reformulation. As a result, there is a growing opportunity for increased MSG adoption, even among premium wellness brands, especially if its natural occurrence in ingredients like tomatoes and Parmesan cheese is effectively communicated to consumers.

Low Cost and Wide Availability Associated with Flavor Enhancers

Flavor enhancers, priced at fractions of a cent per serving, provide a significant competitive edge by delivering superior taste profiles, particularly appealing to cost-conscious consumers in regions such as South America, Africa, and parts of Southeast Asia. The ability to incorporate these enhancers at microgram levels enables food processors to reduce dependency on high-cost ingredients like meat stocks, dairy fats, or spice extracts while still achieving optimal flavor standards. For instance, Angel Yeast’s Angeoboost, enriched with 5’-nucleotides, exemplifies how cost-effective yeast-derived powders can outperform traditional salt reduction methods in applications such as snacks and soups, thereby enhancing profitability in emerging markets. As fast-moving consumer goods companies increasingly adopt hybrid cost-plus and value-based pricing models, the flavor enhancers market is poised to remain a vital tool for driving profit margins.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact timeline |

|---|---|---|---|

| Stringent regulations and quality standards restraining flavor enhancers market growth | -1.1% | North America, Europe | Medium term (2-4 years |

| Health concerns related to flavor enhancers | -0.7% | Global | Long term (≥ 4 years) |

| Rising awareness of potential allergic reactions further limit market expansion | -0.6% | North America, Europe | Long term (≥ 4 years) |

| Availability of raw materials restraining market growth | -0.4% | Global | Medium term (2-4 years |

Source: Mordor Intelligence

Stringent Regulations and Quality Standards Restraining Flavor Enhancers Market Growth

Global manufacturers encounter significant compliance challenges due to varying regional standards, complicating efforts to expand into new markets. Regulatory changes, such as the FDA's deauthorization of red dye No. 3 and California's bans on brominated vegetable oil (BVO) and potassium bromate, highlight the fast-evolving regulatory landscape, requiring businesses to promptly adapt and reformulate their products. This environment increases pressure on synthetic flavor enhancers, which, despite being cost-efficient, are under growing regulatory scrutiny. The FDA's March 2024 update on its post-market assessment of food chemicals indicates potential regulatory changes that could impact the approval status of existing flavor enhancers. For multinational companies, navigating this complex regulatory framework necessitates substantial investments in compliance infrastructure and market-specific product development, providing a competitive advantage to larger players with advanced regulatory capabilities.

Health Concerns Related to Flavor Enhancers

The growing emphasis on clean-label products is driving consumers to actively scan QR codes to verify supply-chain transparency. This shift in consumer behavior has resulted in a marked preference for yeast extracts over chemically modified alternatives. In response, companies are strategically enhancing their branding efforts by integrating on-pack storytelling with detailed online nutritional explanations. Additionally, they are repositioning umami peptides as culinary equivalents to the rich, authentic flavors of slow-simmered broths. However, despite these efforts, synthetic flavor enhancer categories continue to face significant consumer skepticism, which often delays product launches by several months. This persistent trust deficit is fueling increased research and development investments in fermentation-derived innovations, a critical area expected to shape product development pipelines within the flavor enhancers market.

Segment Analysis

By Product Type: Yeast Extracts Challenge Glutamate Pre-eminence

Yeast extracts are anticipated to achieve a 7.24% CAGR through 2030, surpassing overall market growth, driven by their compatibility with vegan, vegetarian, and reduced-salt food categories. Advances in tailored autolysis now enable suppliers to develop extracts with precise nucleotide-to-peptide ratios tailored for specific applications such as retorted broths and high-moisture meat analogs. This versatility positions yeast extracts as a strategic option for manufacturers preparing for potential MSG labeling restrictions. Meanwhile, glutamates maintain a 41.43% market share due to their superior cost-performance balance, ensuring steady demand for mass-market snacks. Strategic portfolio managers are increasingly adopting dual-sourcing approaches to secure supply continuity for both traditional umami and clean-label solutions.

In addition to delivering umami, yeast extracts enhance kokumi mouthfeel, allowing product developers to reduce saturated fat without compromising texture, an essential feature for low-fat dairy and alternative meat spreads. Suppliers are also integrating yeast extracts with natural antioxidants to improve oxidative stability and extend shelf life, particularly for export-oriented products. Regulatory authorities have not introduced additional barriers for yeast extracts, offering them a smoother regulatory pathway compared to synthetic alternatives. These combined advantages suggest that yeast extracts will continue to gain market share within the flavor enhancers segment, while glutamates retain their stronghold due to cost efficiency.

Note: Segment shares of all individual segments available upon report purchase

By Application: Beverages Lead Innovation While Savory Snacks Maintain Volume

In 2024, the savory snack segment secured a substantial 33.76% share of total revenue. Consumer preferences are shifting toward bold and long-lasting flavors in savory snacks, with popular options including masala, cheese, BBQ, peri-peri, and wasabi. To deliver these flavor profiles cost-effectively, manufacturers are leveraging flavor enhancers such as MSG, yeast extract, hydrolyzed vegetable protein, and chili oil powders. The flavor enhancers market for beverages is anticipated to expand at a strong 6.60% CAGR (2025-2030). Energy drink manufacturers are incorporating positive allosteric modulators, such as thaumatin, alongside encapsulated bitterness blockers to highlight key flavor notes like guarana and green tea. The increasing production of non-alcoholic beverages is fueling the demand for flavor enhancers in the beverage market. In May 2025, China reported a production volume of 16.13 million metric tons of non-alcoholic beverages, as per the National Bureau of Statistics of China[3]Source: National Bureau of Statistics of China, "Value of beverage production", www.data.stat.gov.cn.

In the beverage sector, the durability of flavor enhancers under acidic pH conditions and pasteurization heat is critical. Suppliers are addressing this need by developing oil-in-water microemulsions that protect aromatic compounds from degradation, ensuring a strong aroma release upon opening. Due to the high rate of consumer trials in beverages, successful flavor launches can achieve rapid scalability compared to solid foods. This dynamic positions the beverage segment as a key testing ground for innovative flavor systems. Consequently, the beverage segment has gained strategic importance within the flavor enhancers market, attracting a disproportionate share of research and devlopment investments despite its smaller volume.

By Form: Liquid Category Dominance

In 2024, liquid enhancers contributed 39.24% of the revenue, driven by their ease of use and rapid dispersion capabilities, and are expected to achieve a CAGR of 7.43% during the forecast period of 2025-2030. Emulsion carriers at liquid interfaces enable flavor payloads exceeding 20%, reducing transportation costs and aligning with sustainability objectives. The integration of probiotic spores with flavor precursors in a single capsule is an emerging trend, creating opportunities for synbiotic snack claims. These advancements emphasize the role of form innovation in redefining value creation within the flavor enhancers market, benefiting suppliers proficient in both delivery systems and flavor chemistry.

Liquid enhancers outperform powders in achieving uniform dispersion across food matrices, particularly in applications such as sauces, soups, gravies, marinades, and beverages. This ensures consistent and reliable flavor delivery in the final product, a key requirement in industrial food processing. Furthermore, when effectively emulsified or preserved, liquid enhancers demonstrate excellent stability, making them a preferred choice for packaged food products. However, chefs and home cooks alike often turn to powdered flavor enhancers for their convenience and long shelf life. These enhancers boost a dish's taste without overshadowing its primary flavors. Moreover, certain enhancers, such as MSG, can lessen the need for salt, paving the way for healthier culinary choices.

Note: Segment shares of all individual segments available upon report purchase

Geography Analysis

In 2024, Asia-Pacific accounted for the largest market share at 28.34%. Driven by China's robust corn-to-MSG supply chain, the region is positioned to lead global volume and growth. China's Fufeng Group leverages its raw material advantage, while Japan's Ajinomoto enhances enzymatic processes to minimize water consumption, aligning with eco-score standards prioritized by multinational quick-service restaurant chains. Simultaneously, regional start-ups are innovating by transforming indigenous chilies and misos into low-salt savory powders, catering to the growing demand for instant noodles across Southeast Asia. These advancements reinforce Asia-Pacific's role as both a manufacturing hub and a leader in flavor trends within the flavor enhancers market. The region is projected to grow at a strong CAGR of 7.96% during the forecast period of 2025-2030.

In North America, regulatory oversight and digital transparency take center stage. The FDA's chemical-safety reviews prompt vigilant label audits, and QR codes now enlighten retail shoppers on ingredient origins. Venture capital is flowing into precision-fermentation hubs, notably the San Francisco Bay Area, with a keen focus on biosynthesizing rare diketopiperazines, heralded for their low-dose mouth-feel enhancement. As a result, North American suppliers are touting "regulatory readiness" as a lucrative commercial service, amplifying their revenue streams in the flavor enhancers market.

Europe, while setting stringent additive caps, is at the forefront of the sustainability movement. DSM-Firmenich, with its flagship research and development center in the Netherlands, is experimenting with kombucha-derived enhancer bases, eyeing deployment in the Middle East and Africa markets, where halal certification holds significance. Southern European producers are turning grape-pomace amino acids into savory concentrates, a move that echoes the circularity ethos championed by the EU Green Deal. Meanwhile, South America and Africa are focusing on cost-effective enhancers to elevate local staples; for instance, repurposing soybean ferment side-streams into hydrolyzed vegetable proteins, enriching the regional landscape within the broader flavor enhancers market.

Competitive Landscape

The flavor enhancers market is moderately concentrated, with established players and emerging specialists competing intensely. Prominent companies in the market include Ajinomoto Co. Inc., International Flavors and Fragrances Inc., DSM-Firmenich N.V., Symrise AG, and Sensient Technologies Corporation. The 2023 merger of DSM and Firmenich, which created a combined entity generating EUR 12.31 billion in sales, highlights the ongoing consolidation trend. Businesses are pursuing mergers to achieve scale advantages in areas such as research, regulatory compliance, and global distribution.

Technological innovation is becoming a critical differentiator, with companies like Givaudan utilizing AI-driven tools such as Customer Foresight for trend forecasting and ATOM for enhancing flavor formulation processes. Regulatory changes, particularly the FDA's ongoing post-market evaluations of food chemicals, are influencing competitive dynamics. These assessments may restrict certain ingredients while creating opportunities for compliant alternatives, thereby reshaping the market landscape.

Regional experts are increasingly establishing their presence by offering tailored formulations that comply with diverse ingredient regulations specific to local markets. The adoption of software-enabled traceability systems is becoming a critical requirement, as these features are now frequently included in bid documents. This development is driving even smaller, boutique suppliers to allocate resources toward implementing cloud-based compliance dashboards to remain competitive. Within the flavor enhancers market, the ability to seamlessly integrate data and demonstrate regulatory expertise is evolving into a significant entry barrier, often surpassing the traditional emphasis on production scale as a determinant of market entry and success.

Flavor Enhancer Industry Leaders

-

Sensient Technologies Corporation

-

Ajinomoto Co. Inc.

-

DSM-Firmenich N.V

-

Symrise AG

-

International Flavors and Fragrances Inc.

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- July 2024: Ajinomoto Health and Nutrition North America has collaborated with Shiru to develop sweet proteins that are up to 5,000 times sweeter than sugar. This initiative utilizes Shiru's AI platform, Flourish, to identify novel proteins with desirable attributes.

- July 2024: Greenlab partnered with Ginkgo Bioworks to scale production of brazzein, a sweet protein derived from the West African oubli plant that is 2,000 times sweeter than sugar, with plans to produce it from corn for applications in food production and as a flavor enhancer by 2026

- May 2023: Firmenich, a fragrance and taste company, has completed its merger of equals with DSM. This milestone was achieved through the finalization of the share exchange offer and the contribution of Firmenich shares into DSM-Firmenich AG, solidifying their combined position in the market.

- January 2023: International Flavors and Fragrances Inc. launched ChoozIt Vintage in the United States and Canadian markets. ChoozIt Vintage helps cheddar cheese manufacturers in overcoming flavor development during aging, delivering highly consistent pH and texture results throughout the ripening process.

Global Flavor Enhancer Market Report Scope

Flavor enhancers are substances that are added to food to enhance the natural flavor. Flavor enhancers are mostly added to seasonings, noodles, and soups to enhance taste. The flavor enhancer market is segmented by type, application, form, and geography. Based on type, the market is segmented into acidulants, glutamates, hydrolysed vegetable proteins, yeast extracts, and other types. Based on application, the market is segmented into dairy, bakery, confectionery, savory snack, meat, beverage, and other applications. Based on form, the market is segmented into powder, liquid, and others. Based on geography, the market is segmented into North America, Europe, Asia-Pacific, South America, the Middle East, and Africa. The report offers the market size in value terms in USD for all the abovementioned segments.

| By Product Type | Acidulants | ||

| Glutamates | |||

| Hydrolysed Vegetable Proteins | |||

| Yeast Extracts | |||

| Others Types | |||

| By Application | Dairy | ||

| Bakery | |||

| Confectionery | |||

| Savory Snack | |||

| Meat | |||

| Beverage | |||

| Other Applications | |||

| By Form | Powder | ||

| Liquid | |||

| Others | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Rest of North America | |||

| Europe | United Kingdom | ||

| Germany | |||

| Spain | |||

| France | |||

| Italy | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| Australia | |||

| Rest of Asia Pacific | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Middle East and Africa | Saudi Arabia | ||

| South Africa | |||

| Rest of Middle East and Africa | |||

By Product Type

| Acidulants |

| Glutamates |

| Hydrolysed Vegetable Proteins |

| Yeast Extracts |

| Others Types |

By Application

| Dairy |

| Bakery |

| Confectionery |

| Savory Snack |

| Meat |

| Beverage |

| Other Applications |

By Form

| Powder |

| Liquid |

| Others |

By Geography

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | United Kingdom |

| Germany | |

| Spain | |

| France | |

| Italy | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Rest of Asia Pacific | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle East and Africa |

Need A Different Region or Segment?

Customize Now

Key Questions Answered in the Report

What is the projected flavor enhancers market size by 2030?

The market is expected to reach USD 10.42 billion in 2030 on a 6.36% CAGR.

Which region leads the flavor enhancers market?

Asia-Pacific holds 28.34% of global revenue in 2024 and is projected to grow the fastest through 2030.

Why are yeast extracts growing so quickly?

They deliver umami while satisfying clean-label rules, supporting a projected 7.24% CAGR versus the overall 6.36%.

How does MSG support sodium-reduction efforts?

Clinical research shows MSG can cut sodium by up to 40% in formulations without compromising taste.

Page last updated on: July 4, 2025