Semiconductor Materials Market Size

| Study Period | 2019 - 2029 |

| Base Year For Estimation | 2023 |

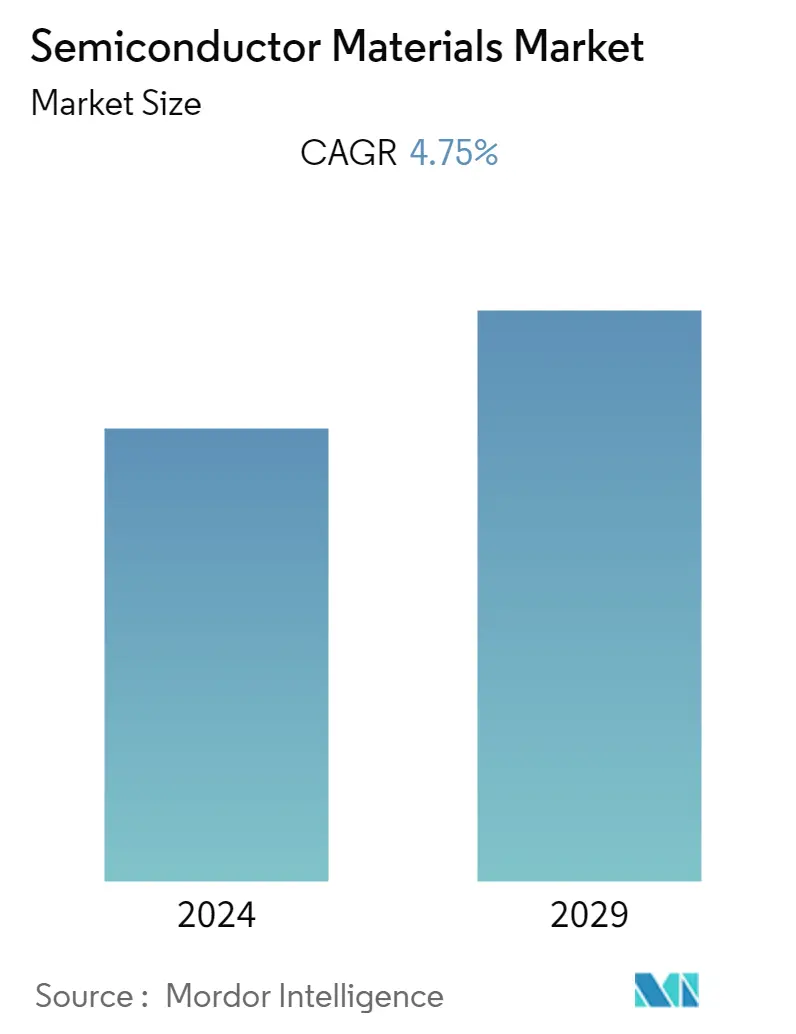

| CAGR | 4.75 % |

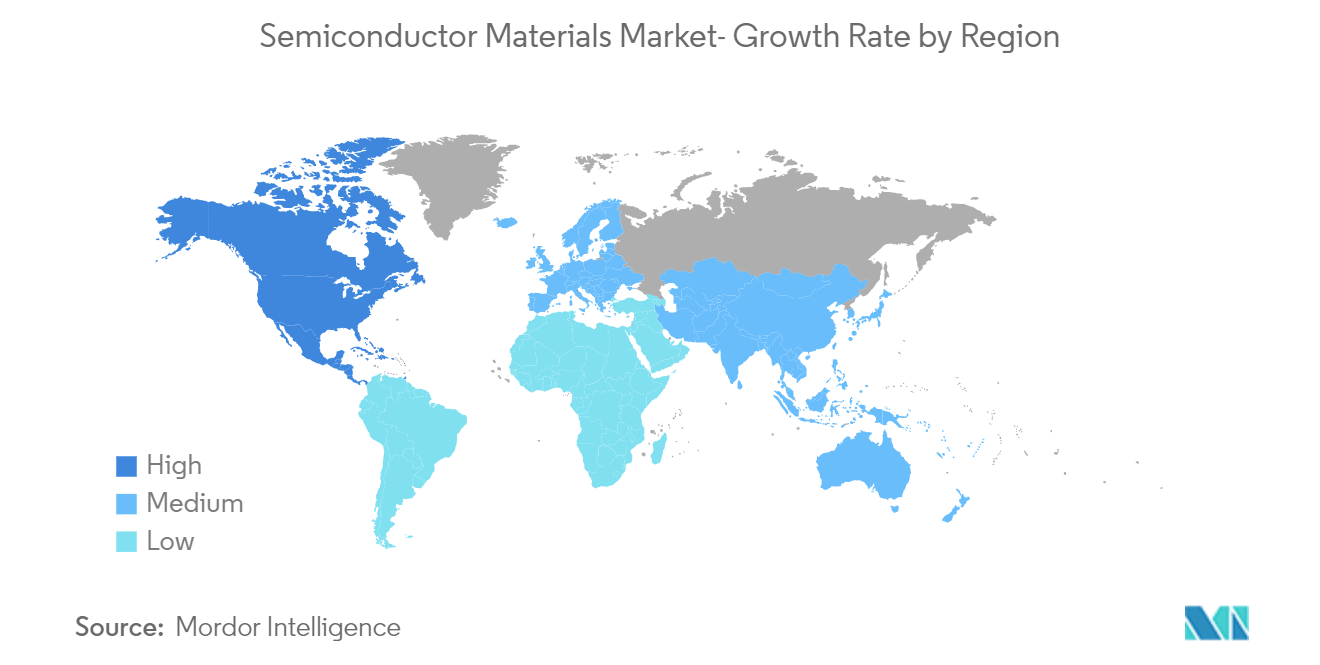

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

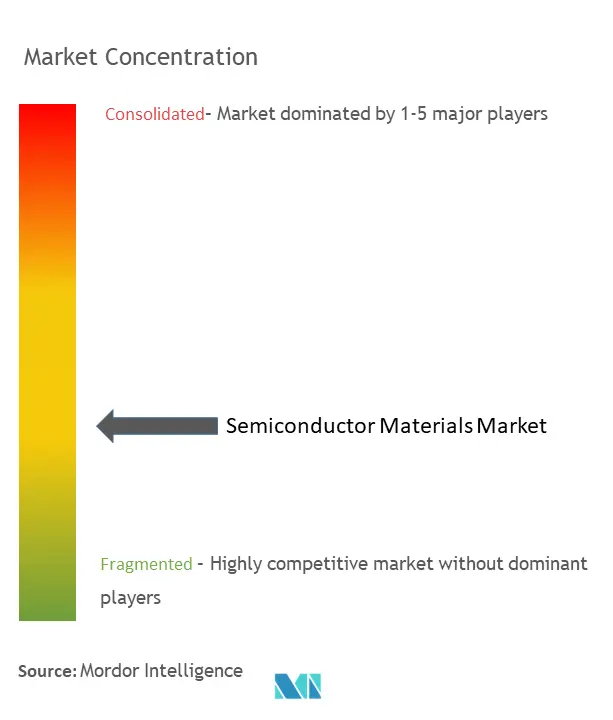

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order |

Need a report that reflects how COVID-19 has impacted this market and its growth?

Semiconductor Materials Market Analysis

The semiconductor materials market size is estimated at USD 70.30 billion in the current year. It is expected to reach USD 88.66 billion by the next five years, registering a CAGR of 4.75% during the forecast period. Semiconductor materials represent one of the significant innovations in the electronics industry. By using materials such as silicon (Si), germanium (Ge), and gallium arsenide (GaAs), electronics manufacturers can replace traditional thermionic devices that make electronic devices heavy and expensive. Since the introduction of semiconductor devices, advanced miniaturization has progressed, and electronic devices have become more compact and mobile.

- With the miniaturization trend gaining momentum in the semiconductor industry, the demand for semiconductor materials is also expected to grow as manufacturing advanced node ICs, heterogeneous integration, and 3D memory architectures require more processing steps; this drives higher wafer fabrication and packaging materials consumption.

- Semiconductors are moving away from rigid substrates to more flexible plastic material and paper, all due to new material and fabrication discoveries. The trend toward more flexible substrates has led to numerous devices, from light-emitting diodes to solar cells and transistors.

- The semiconductor industry has been growing with miniaturization, and advancements and innovations in this field have directly impacted all downstream technologies. With the surging demand for high-end packaging solutions and rising packaging costs, OSAT vendors witnessed a considerable surge in demand from all the end-user industries, especially consumer electronics and automotive applications.

- The semiconductor industry is one of the most complex because of the more than 500 processing steps involved in manufacturing different products and the challenging environment faced by industry workers, including volatile electronics markets and unpredictable demand. It is considered. Depending on the complexity of the manufacturing process, there can be up to 1,400 process steps in semiconductor wafer manufacturing alone. Transistors are formed on the bottom layer, and the process is repeated as many circuits are assembled to create the final product.

- The Russia-Ukraine war is impacting the supply chain of semiconductors. Being a significant supplier of raw materials for producing semiconductors and electronic components, including various equipment. The dispute has disrupted the supply chain, causing shortages and price increases for these materials, impacting manufacturers and potentially leading to higher costs for end-users.

- Further, according to UkraineInvest, copper prices escalated to USD 10,845/mt in early March 2022. The ongoing war between Russia and Ukraine, high energy costs, and stricter emissions standards in Europe have been noted as the primary reasons for the continued shortage of copper.

Semiconductor Materials Market Trends

Rising Demand for Consumer Electronics Goods to Drive the Market

- Consumer electronics (CE) forms a multibillion-dollar industry, steadily progressing and developing technology and adding new product lines toward changing lifestyles. With the advent of IoT, various end-user industries are increasingly adopting advanced consumer electronic products to enhance their operations.

- According to Cisco, the Internet of Things (IoT) has become a prevalent system by which people, processes, devices, and data connection to the Internet and each other. M2M connections are anticipated to grow from 6.1 billion in 2018 to 14.7 billion globally in 2023. Furthermore, Cisco predicts that, by 2023, there will be 1.8 M2M (machine-to-machine) connections for each member of the global population.

- By 2023, the consumer share of the total devices, including fixed and mobile devices, will be 74 percent, with businesses claiming the remaining 26 percent. However, according to Cisco, consumer share will grow at a slightly slower rate, at a 9.1 percent CAGR relative to the business segment, which is expected to witness a 12.0 percent CAGR.

- With the growing deployment of massive IoT technologies such as NB-IoT and Cat-M – primarily consisting of wide-area use cases involving large numbers of low-cost, low-complexity devices with long battery life and low throughput, the number of IoT devices connected by Cat-M and NB-IoT technologies is expected to overtake 2G/3G connected IoT devices in 2023. Broadband IoT in 2027 made up 51 percent of all cellular IoT connections at that time (Source: Ericsson). Such trends are expected to significantly transform the outlook of the consumer electronics industry, which in turn will drive the demand for semiconductor chips to support connectivity features.

- The smartphone market is the major consumer of semiconductors in this segment. The smartphone market has been very competitive in recent years. The increasing usage of cell phones is anticipated to drive the global market. For instance, according to Ericsson, smartphone subscriptions are expected to reach 7.8 billion by 2027, from 6.3 billion in 2021.

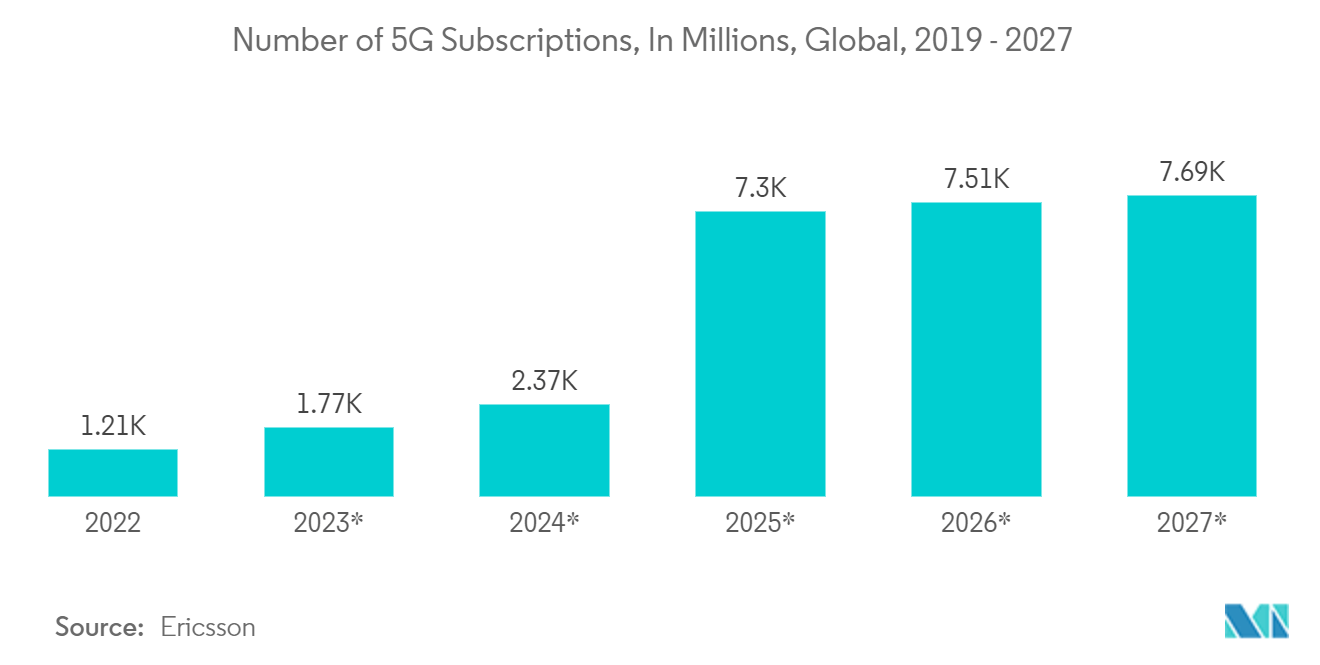

- Other significant drivers behind the demand growth are the 5G rollout and IoT. The growing interest of telecom operators to invest and launch in 5G technology is expected to fuel the demand for 5G capable devices, where consumers and industries are expected to opt for 5G devices. For instance, according to Ericsson, 5G mobile subscription, which grew from 273.96 million in 2020 to 664.18 million in 2021, is expected to reach 4,389.77 million globally by 2027, driving the demand for semiconductor chips and semiconductor materials in the process.

- 5G networks use massive MIMO in which many antennas are deployed at the base station, wherein semiconductor chips are widely used. Therefore, 5G will offer an enormous opportunity for the market studied during the forecast period.

China to Witness Significant Growth

- The Chinese government's national strategic plan, ``Made in China 2025,'' has become a key factor in the growth of the country's semiconductor industry. A central goal of this plan is the growth of the semiconductor industry. Furthermore, the 2021 budget of the China National Intellectual Property Administration (CNIP) targets 2 million registrations per year by 2023, which is expected to revitalize the semiconductor materials market.

- China's new five-year plan for 2021-25, announced in March 2021 by the government, establishes boosting basic research as a critical priority. Central government spending on basic research was expected to increase by 11 percent in 2021, well above the 7 percent planned for the overall R&D investment and the 6 percent target for GDP (Gross Domestic Product) growth. Semiconductors have been identified as one of seven areas for priority funding and resources. Design companies develop nanoscale integrated circuits that perform important tasks that make electronic devices work, such as computing, storage, network connectivity, and power management.

- Furthermore, the growth in wearable electronic devices has also been leading to the adoption of new miniaturized chips, propelling the semiconductor's growth and increasing the demand for wafers, further driving the studied market. As per Cisco Systems, the number of connected wearable devices in China is expected to reach 439 million by 2022 from 378.8 million in 2021. Additionally, according to Ericsson, the number of smartphone mobile network subscriptions is expected to reach approximately 6.6 billion worldwide in 2022 and exceed 7.8 billion by 2028. This will further promote the studied market.

- Furthermore, China's automotive industry has been increasing, and the country plays an increasingly important role in the global automotive market. The Chinese government positions the automobile industry, including the auto parts sector, as one of its key industries. The government predicted that China's car production would reach 30 million vehicles by 2020 and 35 million by 2025.

- Although the pandemic had a notable impact on the country's automobile industry, recent data suggests that the country's automotive industry is on track to its 2025 goals. For instance, according to the China Association for Automobile Manufacturers (CAAM), in 2021, the total number of cars produced in China was about 26.1 million. Furthermore, in 2022, the automotive industry has reported steady growth. For instance, in September 2022, about 2.6 million vehicles were sold in the country.

- According to Semiconductor Equipment and Materials International, China's revenue from semiconductor equipment reached USD 12.97 billion in 2022. The growing demand for semiconductor chips and increasing investment in manufacturing facilities and equipment are expected to create new growth opportunities for the vendors operating in the market.

Semiconductor Materials Industry Overview

Brand identity plays a major role in the Semiconductor Materials market, considering the importance of quality that the end-users expect from a semiconductor manufacturing player. The market penetration is also high with the presence of large market incumbents, such as BASF, L.G Chem Ltd., and KYOCERA Corporation. Overall, the intensity of competitive rivalry is expected to grow moderately over the forecast period.

In November 2022, Indium Corporation, a worldwide materials provider to the electronics assembly and semiconductor packaging company in the United States, opened its newest 37,500-square-foot production plant in Penang, Malaysia. The new plant has begun manufacturing operations and will increase production capacity to service better the company's clients in Malaysia and the neighboring area, notably Thailand and Vietnam.

In May 2022, L.G. Chem began developing photoresist (P.R.) utilized in the semiconductor back-end processes with the intention of providing it to worldwide semiconductor businesses. After engraving ultra-fine circuit designs on the front-end procedure of semiconductors, the company is creating P.R. for the back-end technique to improve chip performance.

Semiconductor Materials Market Leaders

BASF SE

LG Chem Ltd

Indium Corporation

Showa Denko Materials Co. Ltd (showa Denko K.K)

KYOCERA Corporation

*Disclaimer: Major Players sorted in no particular order

Semiconductor Materials Market News

- September 2022 - Showa Denko K.K. (SDK) announced its merger with Showa Denko Materials Co., Ltd. (SDMC) on January 1, 2023, to form "Resonac." Resonac Holdings Corporation will replace SDK as a holding company, while Resonac Corporation will replace SDMC as an operational corporation. Through ongoing restructuring efforts, the Showa Denko Group intends to establish a significant chemical firm with cutting-edge functional materials.

- August 2022 - Indium Corporation introduced products from its GalliTHERM line of gallium-based liquid metals solutions. The company's over 60 years of expertise in producing liquid metals based on gallium are incorporated into this cutting-edge product range.

Semiconductor Materials Market Report - Table of Contents

1. INTRODUCTION

1.1 Study Assumptions and Market Definition

1.2 Scope of the Study

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET INSIGHTS

4.1 Market Overview

4.2 Industry Attractiveness - Porter's Five Forces Analysis

4.2.1 Bargaining Power of Suppliers

4.2.2 Bargaining Power of Consumers

4.2.3 Threat of New Entrants

4.2.4 Threat of Substitutes

4.2.5 Intensity of Competitive Rivalry

4.3 Assessment of the Impact of Key Macro Trends on the Market

5. MARKET DYNAMICS

5.1 Market Drivers

5.1.1 Technical Advancements and Product Innovation of the Electronic Materials

5.1.2 Rising Demand for Consumer Electronics Goods

5.1.3 Increased Demand From OSAT/Packaging Companies

5.2 Market Restraints

5.2.1 Complexity in the Manufacturing Process

6. MARKET SEGMENTATION

6.1 By Application

6.1.1 Fabrication

6.1.1.1 Process Chemicals

6.1.1.2 Photomasks

6.1.1.3 Electronic Gases

6.1.1.4 Photoresists Ancilliaries

6.1.1.5 Sputtering Targets

6.1.1.6 Silicon

6.1.1.7 Other Fabrication Materials

6.1.2 Packaging

6.1.2.1 Substrates

6.1.2.2 Lead-frames

6.1.2.3 Ceramic Packages

6.1.2.4 Bonding Wire

6.1.2.5 Encapsulation Resins (Liquid)

6.1.2.6 Die Attach Materials

6.1.2.7 Other Packaging Applications

6.2 By End User Industry

6.2.1 Consumer Electronics

6.2.2 Telecommunication

6.2.3 Manufacturing

6.2.4 Automotive

6.2.5 Energy and Utility

6.2.6 Other End User Industries

6.3 By Geography

6.3.1 North America

6.3.2 Europe

6.3.3 Asia Pacific

6.3.4 Rest of the World

7. COMPETITIVE LANDSCAPE

7.1 Company Profiles

7.1.1 BASF SE

7.1.2 LG Chem Ltd

7.1.3 Indium Corporation

7.1.4 Showa Denko Materials Co. Ltd (showa Denko K.K)

7.1.5 KYOCERA Corporation

7.1.6 Henkel AG & Company KGAA

7.1.7 Sumitomo Chemical Co. Ltd

7.1.8 Dow Chemical Co. (Dow Inc.)

7.1.9 International Quantum Epitaxy PLC

7.1.10 Nichia Corporation

7.1.11 CAPLINQ Europe BV

7.1.12 ShinEtsu Microsi

- *List Not Exhaustive

8. INVESTMENT ANALYSIS

9. FUTURE OF THE MARKET

Semiconductor Materials Industry Segmentation

Semiconductors are silicon-based materials that conduct electricity better than insulators like glass, but they are not pure conductors like copper or aluminum. Materials used to pattern the wafer are considered fabrication materials for the scope of the study. In contrast, the materials used to protect or connect the die are called packing materials. Semiconductor fabrication is a set of operations that involves depositing a sequence of layers onto a substrate, most often silicon, to create a device structure. Various thin film layers are deposited and removed in this process. Photolithography regulates the portions of the thin film that are to be deposited or withdrawn. Cleaning and inspection stages are usually performed after each deposition and removal operation.

The growth of global semiconductor materials market is segmented by application (fabrication (process chemicals, photomasks, electronic gases, photoresists ancillaries, sputtering targets, silicon, and other fabrication materials) and packaging (substrates, lead frames, ceramic packages, bonding wire, encapsulation resins (liquid), die attach materials and other packaging applications), by end-user industry (consumer electronics, telecommunication, manufacturing, automotive, energy and utility, and other end user industries), and by geography (Taiwan, South Korea, China, Japan, North America, Europe, and Rest of the World). The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

| By Application | |||||||||

| |||||||||

|

| By End User Industry | |

| Consumer Electronics | |

| Telecommunication | |

| Manufacturing | |

| Automotive | |

| Energy and Utility | |

| Other End User Industries |

| By Geography | |

| North America | |

| Europe | |

| Asia Pacific | |

| Rest of the World |

Semiconductor Materials Market Research FAQs

What is the current Semiconductor Materials Market size?

The Semiconductor Materials Market is projected to register a CAGR of 4.75% during the forecast period (2024-2029)

Who are the key players in Semiconductor Materials Market?

BASF SE, LG Chem Ltd, Indium Corporation, Showa Denko Materials Co. Ltd (showa Denko K.K) and KYOCERA Corporation are the major companies operating in the Semiconductor Materials Market.

Which is the fastest growing region in Semiconductor Materials Market?

Asia Pacific is estimated to grow at the highest CAGR over the forecast period (2024-2029).

Which region has the biggest share in Semiconductor Materials Market?

In 2024, the Asia Pacific accounts for the largest market share in Semiconductor Materials Market.

What years does this Semiconductor Materials Market cover?

The report covers the Semiconductor Materials Market historical market size for years: 2019, 2020, 2021, 2022 and 2023. The report also forecasts the Semiconductor Materials Market size for years: 2024, 2025, 2026, 2027, 2028 and 2029.

What are the latest trends in Semiconductor Materials Market?

The latest trends in the Semiconductor Material Industry include: a) Development of 3D semiconductor materials b) Use of silicon carbide (SiC) and gallium nitride (GaN) for power electronics c) Advancements in packaging technologies

What drives the Semiconductor Materials Market?

Key factors driving the Semiconductor Material Market are : a) Increasing demand for electronic devices b) Advancements in technologies c) Growing automotive sector d) Increased demand from obstructive structured assessment test (OSAT)/packaging companies

Semiconductor Materials Industry Report

The Global Semiconductor Materials Market is on a remarkable growth trajectory, fueled by escalating demand for semiconductor raw materials essential in electronic device production. Innovations such as silicon, germanium, gallium arsenide, and notably gallium nitride are revolutionizing the industry with their high efficiency and power conversion capabilities. This surge is propelled by the trend towards electronics miniaturization, necessitating materials that excel in speed, efficiency, and resistance to adverse conditions. The market is also seeing a notable shift towards materials that enhance the performance of modern electronics and optoelectronic devices, with the packaging materials segment and the communication segment, in particular, experiencing significant growth. This is largely due to their critical applications in aerospace and wireless communication technologies, respectively. The Asia Pacific region, with its strong electronics manufacturing base and supportive government initiatives from countries like South Korea and India, dominates the market share. Mordor Intelligence™ offers comprehensive analysis and forecasts on market share, size, and revenue growth in the semiconductor material industry, available for download as a free report PDF.