Precision Medicine Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

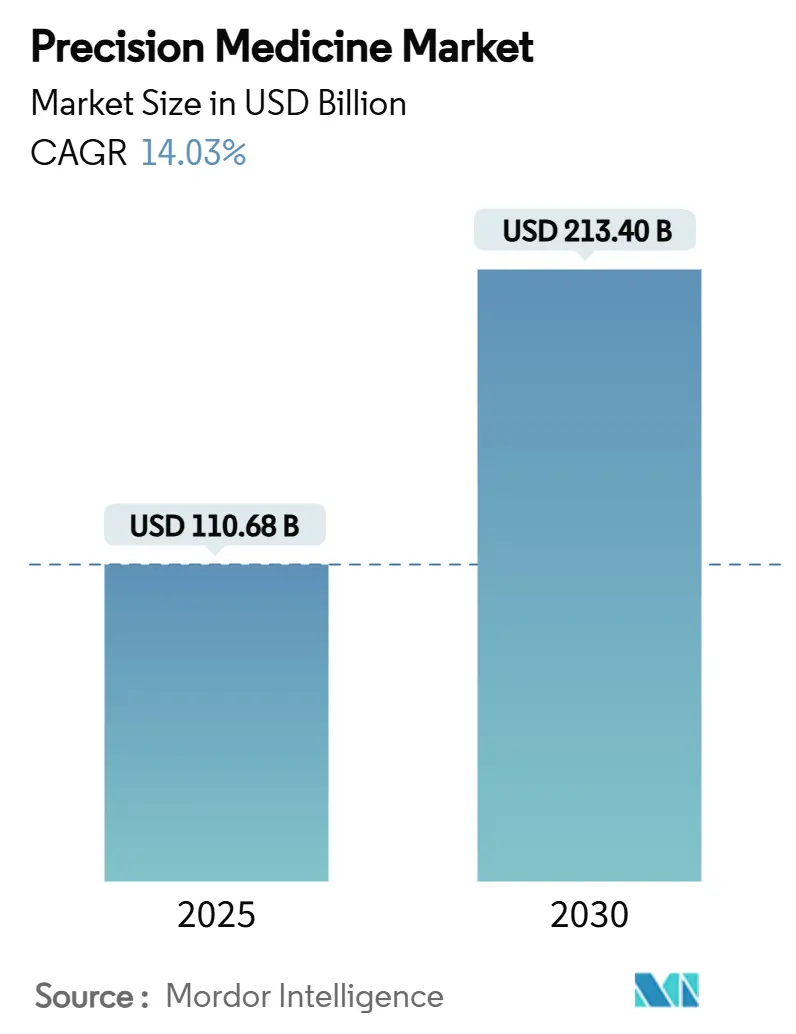

| Market Size (2025) | USD 110.68 Billion |

| Market Size (2030) | USD 213.40 Billion |

| Growth Rate (2025 - 2030) | 14.03% CAGR |

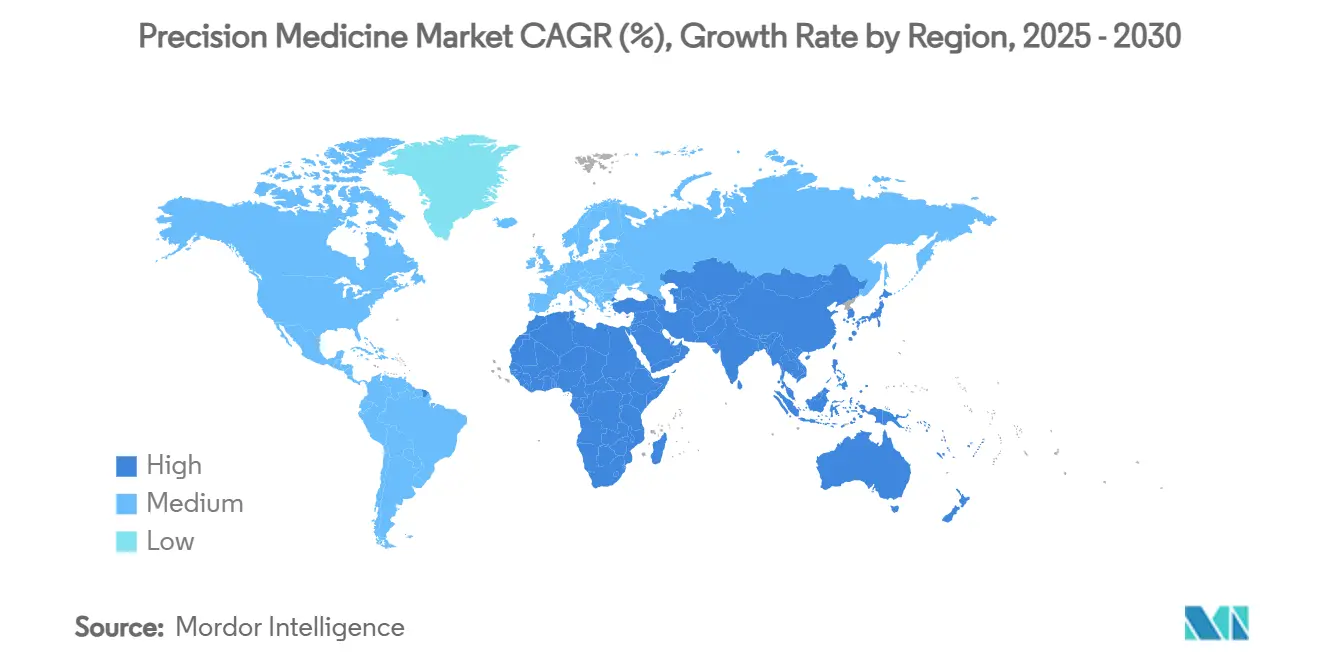

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Precision Medicine Market Analysis by Mordor Intelligence

The Precision Medicine Market size is estimated at USD 110.68 billion in 2025, and is expected to reach USD 213.40 billion by 2030, at a CAGR of 14.03% during the forecast period (2025-2030).

Falling sequencing costs, AI-driven analytics, and friendlier regulatory pathways are aligning to shift healthcare away from one-size-fits-all therapy toward data-rich, patient-specific interventions. Genomic programs in the United States, China, and India are feeding large multi-omics datasets into clinical decision support tools, while cloud-based bioinformatics platforms shorten the time from variant discovery to treatment choice. Progress in pan-cancer companion diagnostics is expanding label-linked drug markets, and new reimbursement codes for pharmacogenomics are improving test affordability. At the same time, stricter oversight of laboratory-developed tests in major markets is raising compliance costs but promises higher test quality and patient safety.

Key Report Takeaways

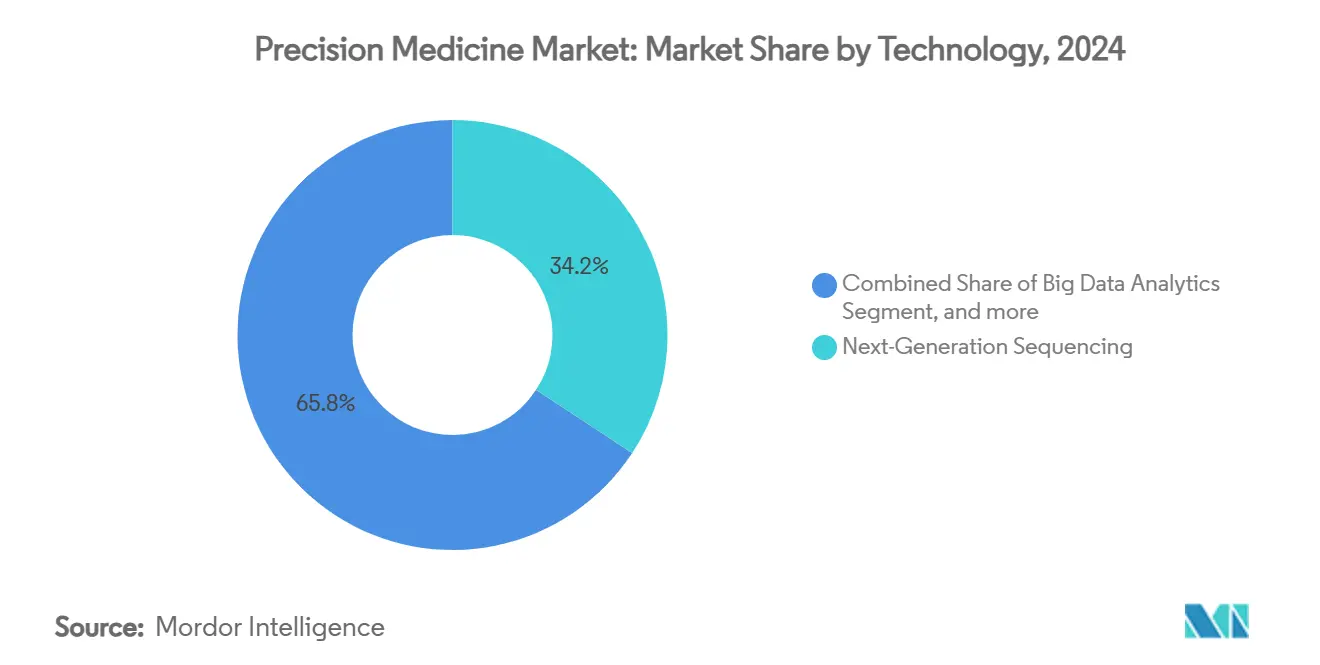

- By technology, next-generation sequencing led with 34.24% of precision medicine market share in 2024, whereas AI and machine learning are advancing at a 17.91% CAGR to 2030.

- By application, oncology accounted for 44.23% of the precision medicine market size in 2024, while rare and genetic disorders are forecast to expand at 15.74% CAGR through 2030.

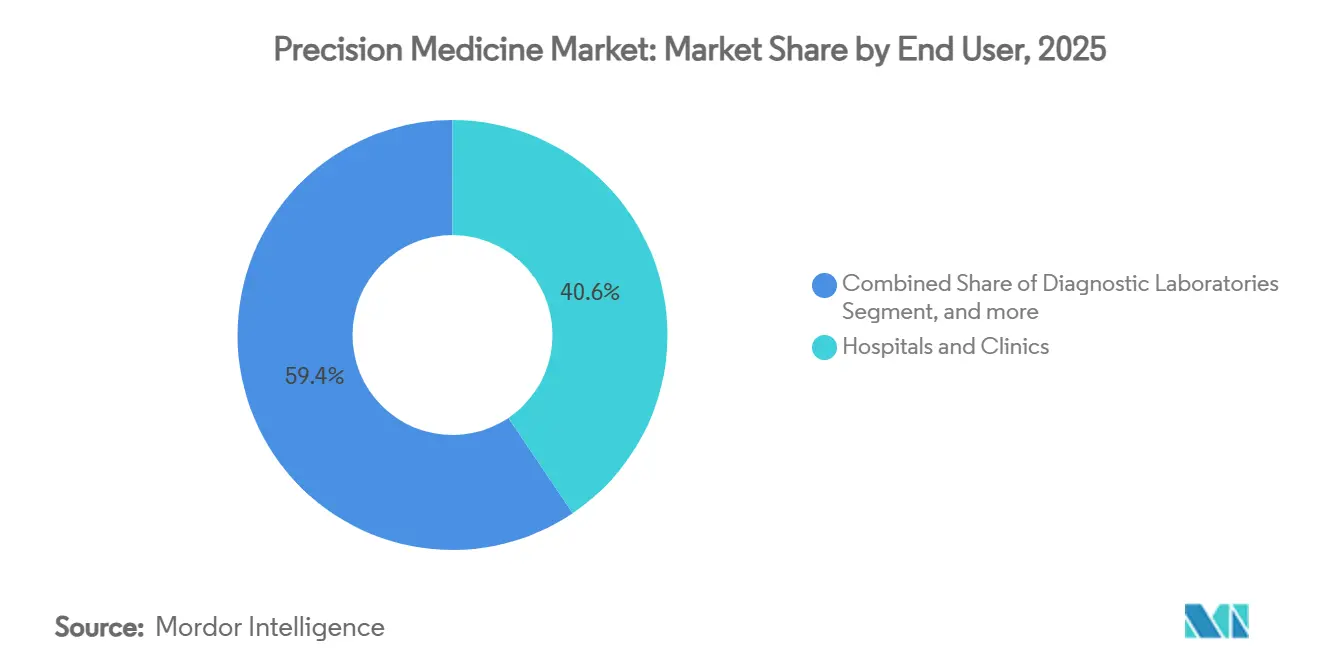

- By end user, hospitals and clinics captured 40.56% of the precision medicine market share in 2024; home-care settings are growing fastest at 16.87% CAGR.

- By geography, North America dominated with 48.43% revenue share in 2024, while Asia-Pacific is projected to post a 14.56% CAGR to 2030.

Global Precision Medicine Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| National Genomic Initiatives Accelerating R&D Funding | +2.1% | Global, with concentration in North America, Europe, and Asia-Pacific | Medium term (2-4 years) |

| Oncology Biomarker Pipeline Expansion Fuelling Companion Diagnostics | +2.3% | North America & EU, expanding to Asia-Pacific | Medium term (2-4 years) |

| Integration of AI and Machine Learning in Genomics | +2.4% | Global | Long term (≥ 4 years) |

| Reimbursement Reforms Supporting Pharmacogenomic Testing | +1.6% | North America & EU primarily | Short term (≤ 2 years) |

| Strategic Pharma–Big-Tech Alliances Speeding Precision Drug Discovery | +1.9% | Global, with North America and Europe leading | Medium term (2-4 years) |

| Advancement in Cancer Biology | +1.8% | Global | Long term (≥ 4 years) |

Source: Mordor Intelligence

National Genomic Initiatives Accelerating R&D Funding

Government genomics programs are underwriting infrastructure that moves sequencing from research labs to routine care. The NIH funded USD 27 million for learning health systems that embed genomics into six U.S. hospital networks. China’s Human Genome Project 2 plans to sequence 80 million genomes, creating the world’s largest reference panel for variant interpretation. India released 10,000 personal genomes in 2025, filling South Asian gaps in global databases. Sweden’s PROMISE program links national registries with multi-omics data to support real-time clinical decision making. Collectively, these projects create interoperable data ecosystems that lift diagnostic accuracy and spur new drug targets.

Oncology Biomarker Pipeline Expansion Fuelling Companion Diagnostics

More than 15 FDA clearances since 2024 have tied targeted drugs to specific biomarker tests, widening the addressable patient pool for precision oncology.[1]U.S. Food and Drug Administration, “TruSight Oncology Comprehensive Approval,” fda.gov Illumina’s TruSight Oncology Comprehensive became the first FDA-cleared pan-cancer in-vitro diagnostic that reads 500 plus biomarkers in one run. FoundationOne CDx now detects NTRK fusions across solid tumors, linking patients to larotrectinib therapy. The therascreen KRAS RGQ PCR Kit guides sotorasib plus panitumumab for KRAS G12C-mutated colorectal cancer. Guardant Health’s Shield blood test adds a non-invasive option that detects colorectal cancer with 83% sensitivity in average-risk adults. Frequent diagnostic approvals give drug developers strong incentives to co-develop assays, reinforcing a virtuous cycle for biomarker-guided therapy.

Integration of AI and Machine Learning in Genomics

Machine learning handles multi-layer omics data that traditional statistics cannot parse. AI-enhanced proteomics measures more than 10,000 plasma proteins from a single drop of blood, enabling early disease prediction.[2]Science Magazine Staff, “Proteomics at Unprecedented Scale,” science.org Large language models acting as “co-scientists” generate novel hypotheses and cut drug discovery timelines in liver fibrosis and acute myeloid leukemia studies. Retrieval-augmented GPT-4 systems triage clinical trial candidates with up to 100% accuracy at a fraction of conventional screening cost.[3]New England Journal of Medicine AI, “Large Language Model Trial Screening,” nejm.org AI-enabled pharmacogenomics predicts drug–gene interactions in chronic diseases, improving dosing safety. As algorithms mature, every new dataset trains models that in turn unlock deeper biological insight, fueling continuous innovation.

Strategic Pharma–Big-Tech Alliances Speeding Precision Drug Discovery

Partnerships between pharmaceutical firms and cloud or data companies merge wet-lab know-how with scalable computing. GSK paid USD 1.15 billion to acquire IDRx and its KIT inhibitor IDRX-42 after a 53% response rate in gastrointestinal stromal tumors. 23andMe now licenses its 14-million-person genetic database to Mirador Therapeutics to refine immune-disease targets. Illumina’s USD 350 million purchase of SomaLogic folds 10,000-protein assays into its sequencing workflow. These deals bundle sequencing, proteomics, and AI analytics under one roof, letting sponsors iterate faster on target validation and patient identification.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Fragmented Cross-Border Multi-Omics Data Regulations | -1.4% | EU and Global cross-border initiatives | Medium term (2-4 years) |

| High Cost and Limited Accessibility of Genetic Testing | -1.8% | Global, with higher impact in emerging markets | Long term (≥ 4 years) |

| Shift from Treatment-based to Preventive Healthcare | -1.2% | Global, with higher impact in developed markets | Long term (≥ 4 years) |

| Declining Trends in FDA Pharmacotherapy Approval Rate | -1.6% | North America, with spillover effects globally | Medium term (2-4 years) |

Source: Mordor Intelligence

Fragmented Cross-Border Multi-Omics Data Regulations

GDPR in Europe treats genomic data as highly sensitive, forcing most omics repositories to operate outside the bloc or navigate complex consent rules. The European Health Data Space introduces extra documentation for any non-EU entity seeking access, lengthening project timelines. In the United States HIPAA governs clinical data, yet many research databases fall outside its scope, adding another compliance layer for cross-Atlantic studies. Privacy-preserving technologies such as federated learning help but cannot fully align legal interpretations across borders. Consequently, global consortia must negotiate region-specific contracts, raising transaction costs and delaying large-scale studies.

High Cost and Limited Accessibility of Genetic Testing

Medicare, Medicaid, and private insurers each apply different coverage rules, so many patients still pay out-of-pocket for multigene panels. Billing complexity persists because only a handful of CPT codes represent thousands of distinct tests, leaving payers unsure about clinical utility. UnitedHealthcare began tying reimbursement to evidence of clinical benefit, adding paperwork for providers. In low- and middle-income countries, out-of-pocket costs remain prohibitive despite cheaper sequencing because clinical interpretation services and genetic counselors are scarce. Until broader reimbursement and workforce development materialize, precision medicine uptake will lag in resource-constrained settings.

Segment Analysis

By Technology: NGS Dominance Amid AI Revolution

Next-generation sequencing captured 34.24% of precision medicine market share in 2024, underpinning most companion diagnostics and pharmacogenomic workflows. FDA clearance of Illumina’s TruSight Oncology Comprehensive assay, which profiles more than 500 biomarkers in one run, cements NGS as the gold standard for broad genomic profiling. Sequencers now feed cloud bioinformatics pipelines that flag actionable variants within hours, making genomic reports manageable during routine clinician visits. Parallel advances in spatial proteomics and high-throughput plasma protein analysis extend the reach of omics beyond DNA, while metabolomics and epigenomics add regulatory context. The integration of these layers builds patient-specific molecular signatures that guide both drug selection and dosing.

A second technology wave centers on artificial intelligence and machine learning, the fastest-growing segment at a 17.91% CAGR. AI tools scale variant annotation, detect mutational signatures linked to tumor aggressiveness, and optimize algorithmic trial enrollment. One retrieval-augmented GPT-4 prototype screened candidates for a solid-tumor trial with 98% accuracy at USD 0.11 per participant versus USD 34.75 for manual review. Proteomics firm SomaLogic measures 10,000 proteins from a microliter sample, producing high-density data that AI models translate into early disease risk scores. As datasets expand, model performance improves, generating a self-reinforcing cycle that attracts further R&D funds. The enduring centrality of sequencing, combined with rapid adoption of AI analytics, suggests a hybrid ecosystem where NGS provides raw data while intelligent software unlocks its clinical value.

Note: Segment shares of all individual segments available upon report purchase

By Application: Oncology Leadership with Rare Disease Acceleration

Oncology retained 44.23% of the precision medicine market size in 2024, buoyed by a steady cadence of biomarker-linked drug approvals. The FDA validated the PATHWAY anti-HER2/neu test for zanidatamab in biliary tract cancer and paired sotorasib with panitumumab for KRAS G12C-mutated colorectal cancer, each tied to companion diagnostics that speed patient identification. Liquid biopsy is gaining momentum as Guardant’s Shield test offers non-invasive CRC screening, while multi-omics approaches blend genomic, transcriptomic, and proteomic data to forecast therapy response. AI-driven radiomics now merges imaging phenotypes with genetic mutations, sharpening tumor subtyping and prognostication.

Rare and genetic disorders represent the fastest-growing application segment at 15.74% CAGR through 2030. Newborn sequencing in China flagged lysosomal storage disorders before symptom onset, enabling early enzyme replacement therapy. Whole-exome analysis is elucidating the genetic roots of neurodevelopmental and metabolic syndromes, and AI-assisted variant calling is cutting diagnostic odysseys. Orphan-drug policies with market exclusivity incentives motivate sponsors to pursue niche indications, while patient advocacy groups crowdsource data that enrich natural-history studies. As databases broaden and long-read sequencing resolves structural variants, the precision medicine market will graduate from disease-specific programs to pan-omic early-intervention models.

By End User: Hospital Dominance Shifting to Home Care

Hospitals and clinics controlled 40.56% of precision medicine market share in 2024, handling complex assays and integrating genomic insights into multidisciplinary care teams. Leading cancer centers now embed molecular tumor boards that match patients to trials within three days of sequencing report receipt. Diagnostic laboratories have scaled rapid whole-genome sequencing for neonatal intensive care units, returning actionable results in under 24 hours. Pharmaceutical and biotechnology companies continue investing in multi-omics real-world evidence platforms, capturing post-marketing safety and effectiveness data that feed next-generation drug pipelines.

Home-care settings, growing at 16.87% CAGR, symbolize a democratization of genetic insight. Direct-to-consumer saliva kits now ship with integrated pharmacogenomic panels, and wearable sensors stream longitudinal physiologic data that AI models combine with genotype to flag early disease signals. Point-of-care PCR devices deliver pathogen genotyping in under 30 minutes in community clinics, while pharmacist-run genomic counseling kiosks are piloting in retail chains. Healthcare IT vendors provide secure apps that store personal genomic files and push therapy alerts to clinicians, improving medication adherence. As payers recognize the cost offsets from early detection and personalized dosing, reimbursement for home testing is expected to broaden, further tilting volume away from hospital labs.

Note: Segment shares of all individual segments available upon report purchase

Geography Analysis

North America led the precision medicine market with a 48.43% revenue share in 2024, underpinned by federal genomics funding, payer coverage for pharmacogenomics, and an accommodating regulatory stance. The FDA’s July 2024 framework for laboratory-developed tests introduces USD 1.29 billion in annual compliance spend, yet stakeholders anticipate higher assay quality that will reinforce patient and clinician confidence fda.gov. Canada supports similar progress through Genomics for Precision Health initiatives, while Mexico is channeling INMEGEN resources into rare-disease sequencing. Collectively, the region hosts most top-ten sequencing vendors and a high concentration of AI health startups, ensuring ongoing leadership in technology and clinical adoption.

Europe ranks second by revenue yet faces slower cross-border data exchange due to GDPR. Germany’s Digital Health Act lifts restrictions on using anonymized claims data for research, which could attract multinational trials to the country. Sweden’s PROMISE links national cancer registry data with whole-genome sequencing and electronic health records, illustrating how coordinated data strategy can work inside existing privacy law. The United Kingdom, France, Italy, and Spain are each expanding biobank capacity and revising reimbursement schedules for pharmacogenomic tests, narrowing the adoption gap with North America.

Asia-Pacific is the fastest-growing region with a 14.56% CAGR, propelled by national genome initiatives and rising healthcare spend. China’s Human Genome Project 2 and its AI-centered precision health roadmap receive strong central funding and provincial rollouts. India’s Genome India Project corrects South-Asian under-representation and boosts discovery of region-specific drug targets. Japan has committed to analyze 100,000 cancer genomes under a national program to guide targeted therapy development. Australia and South Korea are combining government grants with venture investment to build multi-omics hubs, and Singapore is scaling AI genomics in public hospitals. Southeast Asian and Middle East countries are laying regulatory and reimbursement groundwork that will support catch-up growth during the forecast horizon.

Competitive Landscape

The precision medicine market is moderately fragmented, with more than 200 active platform providers and a long tail of niche analytics firms. Illumina, Thermo Fisher Scientific, and Roche command the largest installed sequencing bases. Illumina’s USD 350 million acquisition of SomaLogic integrates high-throughput proteomics and sequencing on one platform, positioning the firm for systems-biology workflows that span DNA, RNA, and protein. Thermo Fisher is pairing Ion Torrent sequencers with Amazon Web Services analytics to lower entry barriers for community labs. Roche continues to expand Foundation Medicine’s companion-diagnostic portfolio while investing in spatial biology through its Navify digital ecosystem.

New entrants leverage algorithmic strength rather than hardware. Recursion Pharmaceuticals uses automated microscopy and deep learning to map gene function, accelerating target validation timelines. Freenome applies machine learning to cell-free DNA and protein markers for early cancer detection, competing with Guardant in liquid biopsy. Color Health partners with employers and public health agencies to deliver large-scale genomic screening that feeds anonymized data into learning networks. Vertical alliances are intensifying as pharma, tech, and diagnostics players seek full-stack capabilities; GSK’s IDRx deal for a KIT inhibitor and 23andMe’s data licensing to Mirador highlight this convergence.

Regulatory landscapes shape competitive strategy. Companies that invest early in quality-management systems and external quality assessment programs will navigate the FDA’s new laboratory-developed test rule with fewer disruptions. Those that adopt privacy-preserving data architectures can win European contracts under the Health Data Space Regulation. As payers expand coverage of pharmacogenomic tests, firms offering end-to-end solutions—from sequencing to decision support—stand to gain share, while reagent-only vendors may face margin pressure. Overall, expect continued acquisitions aimed at filling technology gaps and scaling data assets.

Precision Medicine Industry Leaders

-

Pfizer Inc.

-

Thermo Fisher Scientific Inc.

-

Novartis AG

-

Medtronic

-

Qiagen N.V.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Labcorp announced the expansion of its precision oncology portfolio, including the launch of Labcorp Plasma Detect, a clinically validated ctDNA MRD solution, and enhancements to Labcorp Plasma Complete, a genomic profiling assay.

- March 2025: Oncodesign Precision Medicine (OPM) Submits Protocol for Phase 1b/2a Study, REVERT, Combining OPM-101 and Pembrolizumab for Advanced Melanoma Patients Resistant to Anti-PD1Oncodesign Precision Medicine (OPM), a clinical-stage firm pioneering therapies to tackle immune evasion and drug resistance, has submitted its REVERT study protocol to Swiss authorities. REVERT (RIPK2 for rEsistant and adVanced mElanoma tReatmenT) is a Phase 1b/2a clinical trial using OPM-101, OPM's RIPK2 inhibitor, targeting advanced melanoma patients resistant to anti-PD-1. This protocol submission comes on the heels of positive Phase 1 study results announced in October 2024.

- January 2025: GSK announced the acquisition of IDRx for up to USD 1.15 billion, including USD 1 billion upfront, to strengthen its precision medicine portfolio targeting gastrointestinal stromal tumors with the selective KIT inhibitor IDRX-42, which achieved a 53% objective response rate in trials.

- November 2024: 23andMe and Mirador Therapeutics began a strategic collaboration to advance precision medicines for immunology and inflammation, with Mirador using 23andMe’s genetic and phenotypic data to enhance its Mirador360™ development engine.

Global Precision Medicine Market Report Scope

As per the scope of the report, precision medicine, a combination of molecular biology techniques and system biology, is an emerging approach to disease treatment and prevention. The market growth for this approach is gaining momentum as it takes individual variability in genes, environment, and lifestyle into account when developing drugs and vaccines. The global market for precision medicine is segmented by technology (big data analytics, bioinformatics, gene sequencing, drug discovery, companion diagnostics, and other technologies), application (oncology, CNS, immunology, respiratory, and other applications), and geography (North America, Europe, Asia-Pacific, the Middle East and Africa, and South America). The report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers the value (in USD million) for the above segments.

| By Technology | Big Data Analytics | ||

| Bioinformatics | |||

| Next-Generation Sequencing (NGS) | |||

| AI & Machine Learning | |||

| Companion Diagnostics | |||

| Genomics | |||

| Proteomics | |||

| Metabolomics | |||

| Epigenomics | |||

| Transcriptomics | |||

| By Application | Oncology | ||

| Neurology (CNS) | |||

| Immunology | |||

| Cardiology | |||

| Infectious Diseases | |||

| Respiratory | |||

| Rare & Genetic Disorders | |||

| Metabolic Disorders | |||

| Other Indications | |||

| By End User | Pharmaceutical & Biotechnology Companies | ||

| Diagnostic Laboratories | |||

| Hospitals & Clinics | |||

| Academic & Research Institutes | |||

| Contract Research Organizations (CROs) | |||

| Healthcare IT & Bioinformatics Firms | |||

| Home-care Settings | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| Australia | |||

| South Korea | |||

| Rest of Asia-Pacific | |||

| Middle East & Africa | GCC | ||

| South Africa | |||

| Rest of Middle East & Africa | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Big Data Analytics |

| Bioinformatics |

| Next-Generation Sequencing (NGS) |

| AI & Machine Learning |

| Companion Diagnostics |

| Genomics |

| Proteomics |

| Metabolomics |

| Epigenomics |

| Transcriptomics |

| Oncology |

| Neurology (CNS) |

| Immunology |

| Cardiology |

| Infectious Diseases |

| Respiratory |

| Rare & Genetic Disorders |

| Metabolic Disorders |

| Other Indications |

| Pharmaceutical & Biotechnology Companies |

| Diagnostic Laboratories |

| Hospitals & Clinics |

| Academic & Research Institutes |

| Contract Research Organizations (CROs) |

| Healthcare IT & Bioinformatics Firms |

| Home-care Settings |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

Key Questions Answered in the Report

What is driving the strong CAGR in the precision medicine market?

Falling sequencing costs, AI analytics that clarify variant impact, and expanding reimbursement for pharmacogenomic tests are combining to deliver a 14.03% CAGR between 2025 and 2030.

Which technology segment leads revenue today?

Next-generation sequencing holds 34.24% of the 2024 revenue base because it underpins most companion diagnostics and genomic workflows.

Why are Asia-Pacific growth rates higher than those in Europe and North America?

National genome projects in China, India, and Japan add large datasets and government funding, pushing the region toward a forecast 14.56% CAGR.

How will the FDA’s laboratory-developed test rule affect suppliers?

Compliance costs of USD 1.29 billion annually will favor companies that already maintain robust quality systems, raising barriers for smaller labs.

Which end-user segment is expanding fastest?

Home-care settings are growing at 16.87% CAGR as direct-to-consumer kits and point-of-care molecular devices bring genetic testing out of hospital walls.

What competitive strategy is emerging among market leaders?

Vertical integration that pairs sequencing, proteomics, and AI analytics—seen in Illumina’s purchase of SomaLogic and GSK’s acquisition of IDRx—is becoming common to shorten discovery timelines and secure data assets.

Page last updated on: July 14, 2025