Pharmaceutical CMO Market Size

| Study Period | 2019 - 2029 |

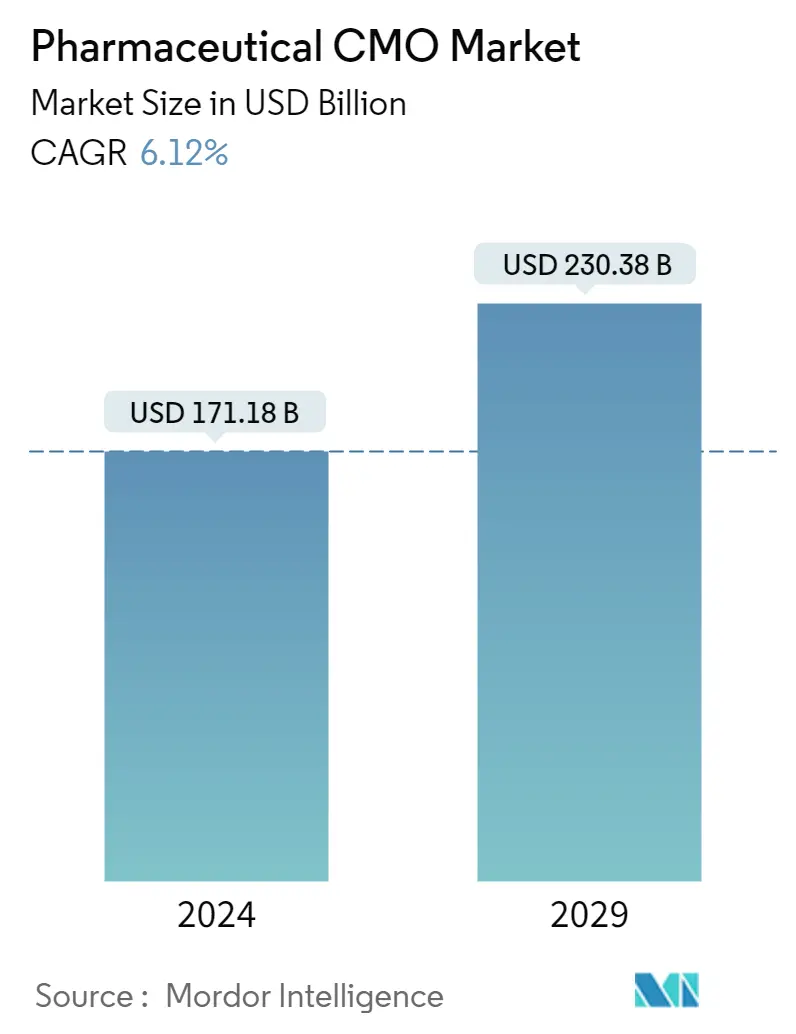

| Market Size (2024) | USD 171.18 Billion |

| Market Size (2029) | USD 230.38 Billion |

| CAGR (2024 - 2029) | 6.12 % |

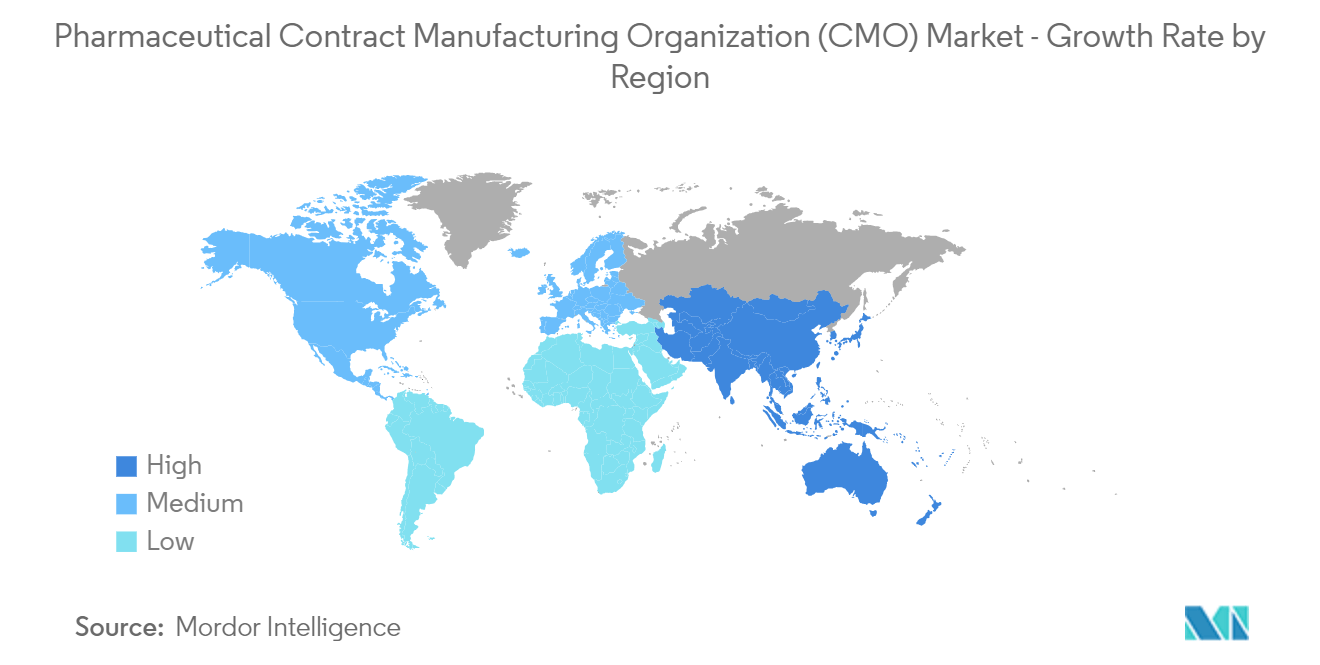

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

Major Players*Disclaimer: Major Players sorted in no particular order |

Need a report that reflects how COVID-19 has impacted this market and its growth?

Pharmaceutical CMO Market Analysis

The Pharmaceutical CMO Market size is estimated at USD 171.18 billion in 2024, and is expected to reach USD 230.38 billion by 2029, growing at a CAGR of 6.12% during the forecast period (2024-2029).

As a result of the rising demand for generic medicines and biologics, the capital-intensive nature of the business, and the complex manufacturing requirements, many pharmaceutical companies have identified the potential profitability in contracting with a CMO (contract manufacturing outsourcing) for both clinical and commercial stage manufacturing.

- The most significant factor driving the growth of CMOs in the pharmaceutical industry is the growing need for state-of-the-art processes and production technologies, which have proven significantly effective in meeting regulatory requirements.

- CMOs are consolidating as a means of enhancing profitability in the competitive market. The large CMOs could expand their geographical presence and penetrate multiple markets through consolidation. For instance, in January 2020, South Korea's Celltrion, a biosimilar maker, announced plans to invest USD 514 million over five years for its new plant in Wuhan, China's most extensive biologics facility with a capacity of 120,000 liters. The new facility is designed to develop and manufacture its biologics for the local market and perform contract work for Chinese biotech companies' emerging wave.

- Additionally, the pharmaceutical companies have been directing their priorities toward the core areas of competency. Hence, they prefer not to dispense available resources, expertise, and technology in formulating the final dose of medicines. The increased competition and shrinking profit margins compelled the pharmaceutical companies to revisit their production processes and R&D activities instead of manufacturing the formulated drug to stay competitive in the market.

- With the ongoing growth in the pharmaceutical sector, particularly after the Covid-19 pandemic, pharmaceutical innovator companies need to stock their pipelines with new drugs. However, they do not have the resources to discover, develop, and manufacture products. Hence, the requirement for CMOs is quite significant.

- Further, the countries such as China, India, and Japan hold a significant share of the pharmaceutical CMO market, owing to low labor costs, low capital and overhead costs (compared to that of the United States and Europe), tax incentives, and undervalued currency combine that provides a significant cost advantage for pharmaceutical companies outsourcing to these countries.

- The most significant factor boosting the growth of CMOs in the pharmaceutical industry in the Asia Pacific region is the growing need for robust processes and production technologies, which have proven highly effective in meeting regulatory requirements.

- The outbreak of COVID-19 positively impacted the market as pharma companies suddenly were faced with the challenge of producing the many millions of vaccine doses that would likely be needed. Many companies such as Pfizer and AstraZeneca transferred non-COVID-19 biologics out of their proprietary manufacturing networks to make room for the new vaccines. Due to compressed timelines and manufacturing scaling challenges for the COVID-19 vaccines and medicines, CMOs signed contract manufacturing service agreements at an unprecedented rate with the onset of the pandemic.

Pharmaceutical CMO Market Trends

Growing Investment in R&D is Expected to Drive the Market

- The United States is one of the largest pharmaceutical markets, accounting for about half of the R&D spending in the pharmaceutical and biotech markets. CMOs play a vital role in this market, investing in new facilities and technology to serve various outsourcing entities. Also, companies are not only reaping the benefits of their Asian footprint through in-house investments but also looking to research-based partnerships to acquire high-end sourcing expertise, build drug discovery, and invest in Asia.

- The Chinese professional manufacturer of drugs for dermatology and anti-tuberculosis, Huapont, is one of the fastest-growing pharmaceutical manufacturers in China, mainly dependent on R&D and market expansion. CMOs can leverage their expertise, owing to their R&D and complex manufacturing capabilities, to fill the needs of large generic pharmaceutical and biotech companies.

- The gradual change in the working principles of the companies in the market led to the shift in pattern from cost-control to re-emphasis on value-added services. They also allowed their integration into the value chain of companies. The highly fragmented nature of the US pharmaceutical contract manufacturing market, with more than 150 CMOs, results in competition (in terms of price) and drives impact on the revenue of CMOs.

- R&D investments and capacity expansions are expected in the injectable and sterile liquid dose formulations segment. Small biotech firms get access to specialized knowledge and resources, which help them expedite their R&D activities. Greater technological complexity in drug development and greater specificity in targets helped in the average R&D costs, as firms identify drugs with molecular characteristics instead of using trial-and-error methods to find compounds that work in the desired way.

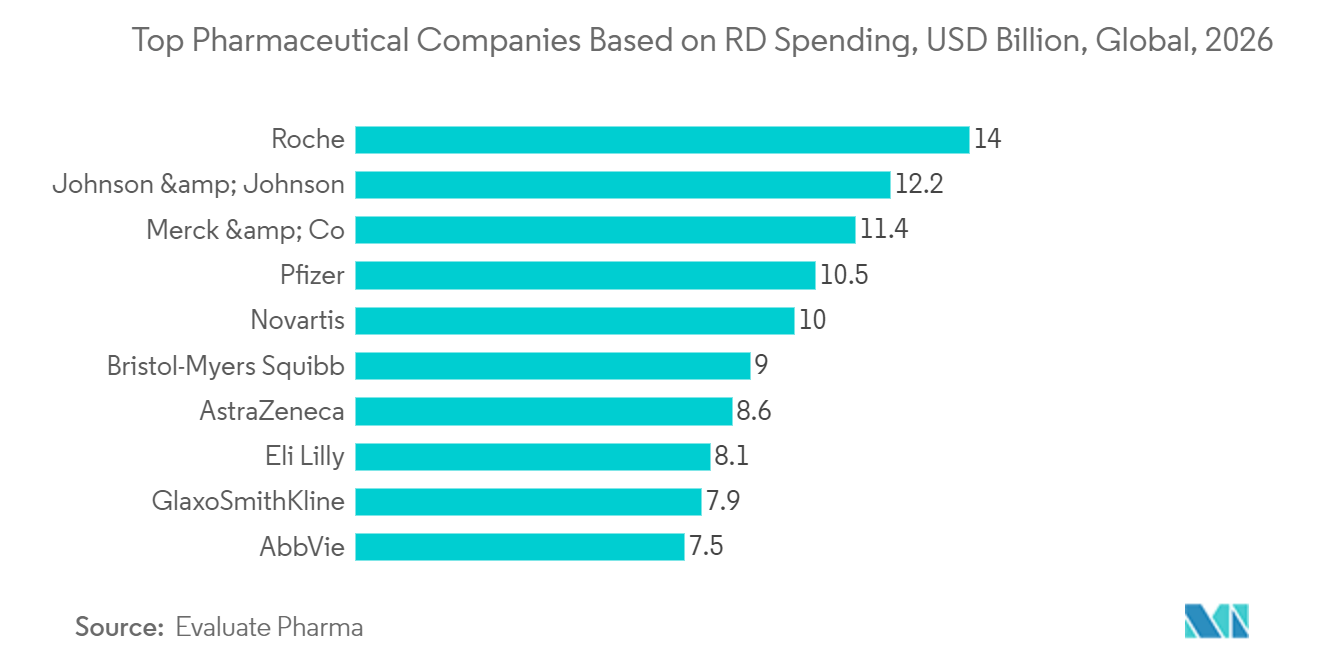

- In addition, market vendors are expanding their research services to cater to the dynamic requirements of pharmaceutical companies, leading to a boost in the given market. According to Evaluate Pharma, in 2026, Swiss-based Roche is projected to spend USD 14 billion on pharmaceutical research and development (R&D). Other companies with high projected R&D expenditures are Merck, Pfizer, and Johnson & Johnson.

North America to Hold Significant Market Share

- The United States contract manufacturing organizations (CMOs) have evolved from an initial offering of essential manufacturing services to a wide range of services to meet market and outsourcer demand. Steady growth in the U.S. pharmaceutical industry and increasing outsourcing by major pharmaceutical companies focusing on their core competencies to improve profit margins drive the country's market.

- Stricter domestic regulations ensure superior manufacturing quality and final products that CMOs adhere to. For instance, manufacturing an autologous or allogeneic therapy is complex, and the manufacturing facility must obtain its GMP certification.

- The country has emerged as one of the largest drug markets, accounting for almost half of the R&D spending in pharmaceutical and biotechnology markets. Hence, CMOs play a critical role in this market and have invested in new facilities and technologies to cater to various outsourcers. The country is experiencing a shortage in manufacturing capability for specific sectors, like cell, peptide, and gene therapy. The CMOs have increased their manufacturing bases over the past two years.

- Canada's pharmaceutical industry is one of the most innovative in terms of products. Pharmaceuticals, a key sector of the Canadian economy, is supported by the Canadian government, which provides a business-friendly environment for pharmaceutical companies and can leverage assets for short- and long-term business strategies.

- In the wake of the patent cliffs, pharmaceutical companies in the country are reorganizing and looking for new business models built on third-party partnerships and external networks. This business model mainly relies on outsourcing most operations, including manufacturing, providing good growth opportunities for CMOs in this region.

Pharmaceutical CMO Industry Overview

Although the market studied is highly fragmented, major vendors account for most of the market share. The presence of many players in the market studied impacts the pricing of services, making it a direct competing factor, especially for small-scale vendors. The vendors in the market studied are expected to focus on providing one-stop-shop services, providing them with a competitive advantage. These practices would be possible for the CMOs with access to large capital. This factor increases the competition and creates a new players' entry barrier. Some of the major players in the market are Patheon Inc. (Thermo Fisher Scientific Inc.), Lonza Group, Catalant Inc., Pfizer CentreOne (Pfizer Inc.), Boehringer Ingelheim Group, etc.

In June 2023, OneBioSuite, an integrated development, production, and supply solution from Catalent, was developed to include various biologic modalities, including mRNA, cell and gene therapies, antibody and recombinant proteins, and recombinant proteins. The debut of the extended service will take place in conjunction with Catalent's participation in the BIO International Convention (booth 785) in Boston from June 5-8, 2023.

In December 2022, RedHillBiopharma's medication Talicia used to treat H. pylori infection, would continue to manufacture commercially by Recipharmthrough 2026. RedHilland Recipharmhave worked closely since 2015 to develop and manufacture Talicia (delayed-release capsules, omeprazole magnesium, amoxicillin, and rifabutin, 10 mg/250 mg/12.5 mg).

Pharmaceutical CMO Market Leaders

Catalent Inc.

Recipharm AB

Jubilant Biosys Ltd.(Jubilant Pharmova Ltd)

Patheon Inc. (Thermo Fisher Scientific Inc.)

Boehringer Ingelheim Group

*Disclaimer: Major Players sorted in no particular order

_Market.webp)

Pharmaceutical CMO Market News

- January 2023: Catalent announced that it had signed a development and license agreement with EthicannPharmaceuticals Inc., a Canadian/American specialty pharmaceutical company specializing in creating high-value cannabinoid drug therapies using Zydisorally disintegrating tablet (ODT) technology to advance Ethicann'sclinical drug pipeline. Per the agreement, Catalent would use its Zydistechnology to create pharmaceutical products containing cannabidiol (CBD) and tetrahydrocannabinol (THC) for Ethicann'suse in clinical trials for various conditions.

- October 2022: Recipharm invested in a new high-speed filling line for pre-filled syringes and cartridges at its site in Wasserburg, Germany, to address the rising client demand for high-growth file formats, international contract development, and manufacturing organization (CDMO). This investment was expected to further strengthen Recipharm'sentire manufacturing offering for injectable pharmaceuticals that need sterile filling as part of a recent program of investments and expansions across the more significant business.

Pharmaceutical CMO Market Report - Table of Contents

1. INTRODUCTION

1.1 Study Assumptions and Market Definition

1.2 Scope of the Study

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET INSIGHTS

4.1 Market Overview

4.2 Industry Attractiveness-Porter's Five Forces Analysis

4.3 Industry Value Chain Analysis

4.4 Industry Policies

4.5 Market Drivers

4.6 Assessment of the Impact of COVID-19 on the Pharmaceutical CMO Market

5. MARKET DYNAMICS

5.1 Market Drivers

5.1.1 Increasing Outsourcing Volume by Pharmaceutical Companies

5.1.2 Increasing Investment in R&D

5.2 Market Restraints

5.2.1 Increasing Lead Time and Logistics Costs

5.2.2 Stringent Regulatory Requirements

5.2.3 Capacity Utilization Issues Affecting the Profitability of CMOs

5.3 Analysis of Current Licensing and Business Models in the CMO Industry

5.4 Key Criteria Considered for Selection of CMO

5.5 Coverage on Thin Film Contract Outsourcing

6. MARKET SEGMENTATION

6.1 By Service Type

6.1.1 Active Pharmaceutical Ingredient (API) Manufacturing

6.1.1.1 Small Molecule

6.1.1.2 Large Molecule

6.1.1.3 High Potency API (HPAPI)

6.1.2 Finished Dosage Formulation (FDF) Development and Manufacturing

6.1.2.1 Solid Dose Formulation

6.1.2.1.1 Tablets

6.1.2.1.2 Other Types(Capsules, Powders, Etc.)

6.1.2.2 Liquid Dose Formulation

6.1.2.3 Injectable Dose Formulation

6.1.3 Secondary Packaging

6.2 By Geography^

6.2.1 North America

6.2.1.1 United States

6.2.1.2 Canada

6.2.2 Europe

6.2.2.1 United Kingdom

6.2.2.2 Germany

6.2.2.3 France

6.2.2.4 Italy

6.2.2.5 Rest of Europe

6.2.3 Asia-Pacific

6.2.3.1 China

6.2.3.2 India

6.2.3.3 Japan

6.2.3.4 Australia

6.2.3.5 Rest of Asia-Pacific

6.2.4 Latin America

6.2.4.1 Brazil

6.2.4.2 Mexico

6.2.4.3 Argentina

6.2.4.4 Rest of Latin America

6.2.5 Middle East and Africa

6.2.5.1 United Arab Emirates

6.2.5.2 Saudi Arabia

6.2.5.3 South Africa

6.2.5.4 Rest of Middle East and Africa

7. VENDOR MARKET SHARE

8. COMPETITIVE LANDSCAPE

8.1 Company Profiles

8.1.1 Catalent Inc.

8.1.2 Recipharm AB

8.1.3 Jubilant Biosys Ltd.(Jubilant Pharmova Ltd.)

8.1.4 Patheon Inc. (Thermo Fisher Scientific Inc.)

8.1.5 Boehringer Ingelheim Group

8.1.6 Pfizer CentreSource (Pfizer Inc.)

8.1.7 Aenova Holdings GMBH

8.1.8 Famar SA

8.1.9 Baxter Biopharma Solutions (Baxter International Inc.)

8.1.10 Lonza Group

8.1.11 Tesa Labtec GmbH (Tesa SE)

8.1.12 Tapemark

8.1.13 ARX LLC

- *List Not Exhaustive

9. ANALYSIS OF MAJOR CMOS WHO ARE EQUIPPED TO MANUFACTURE SCHEDULED DRUGS

10. INVESTMENT ANALYSIS

11. FUTURE OUTLOOK OF THE MARKET

12. APPENDIX

12.1 Dosage Formulation Technologies

12.1.1 Abuse-deterrent Formulation Technology

12.1.2 Lipid Multiparticulate (LMP) Technology

12.1.3 Dry Powder Inhalation Technology

12.1.4 Force Control Agent Technology

12.1.5 High-potency Drug Formulation Technology

12.1.6 Fluidized Bed Coating Technology

12.1.7 High-potency Drug Formulation Technology

12.2 Dosage Forms By Route of Administration

12.2.1 Oral

12.2.2 Topical

12.2.3 Parenteral

12.2.4 Rectal

12.2.5 Vaginal

12.2.6 Inhaled

12.2.7 Otic

Pharmaceutical CMO Industry Segmentation

Contract manufacturing is outsourcing, where a manufacturer enters a formal agreement with another manufacturing firm for its parts, products, or components. The former manufacturer uses these in its manufacturing process for manufacturing its products. A contract manufacturing organization (CMO) is an organization that serves the pharmaceutical industry and provides clients with comprehensive services, from drug development to manufacturing. Outsourcing to a CMO allows pharmaceutical clients to expand their technical resources without increased overhead. The client can manage its internal resources and costs by focusing on the core competencies and high-value projects while reducing or not adding infrastructure or technical staff.

The Pharmaceutical Contract Manufacturing Organization (CMO) Market is segmented by Service Type (Active Pharmaceutical Ingredient (API) Manufacturing (Small Molecule, Large Molecule, High Potency API (HPAPI)), Finished Dosage Formulation (FDF) Development and Manufacturing (Solid Dose Formulation (Tablets), Liquid Dose Formulation, Injectable Dose Formulation), Secondary Packaging), by Geography (North America (Segmentation by Service Type, Segmentation by Country (United States, Canada)), Europe (Segmentation by Service Type (Segmentation by Country (United Kingdom, Germany, France, Italy, Rest of Europe)), Asia-Pacific (Segmentation by Service Type, Segmentation by Country (China, India, Japan, Australia, Rest of Asia-Pacific)), Latin America (Segmentation by Service Type, Segmentation by Country (Brazil, Mexico, Argentina, Rest of Latin America)), Middle East and Africa (Segmentation by Service Type, Segmentation by Country (United Arab Emirates, Saudi Arabia, South Africa, Rest of Middle East and Africa))). The market sizes and forecasts are provided in terms of value in USD billion for all the segments.

| By Service Type | ||||||||

| ||||||||

| ||||||||

| Secondary Packaging |

| By Geography^ | |||||||

| |||||||

| |||||||

| |||||||

| |||||||

|

Pharmaceutical CMO Market Research FAQs

How big is the Pharmaceutical CMO Market?

The Pharmaceutical CMO Market size is expected to reach USD 171.18 billion in 2024 and grow at a CAGR of 6.12% to reach USD 230.38 billion by 2029.

What is the current Pharmaceutical CMO Market size?

In 2024, the Pharmaceutical CMO Market size is expected to reach USD 171.18 billion.

Who are the key players in Pharmaceutical CMO Market?

Catalent Inc., Recipharm AB, Jubilant Biosys Ltd.(Jubilant Pharmova Ltd), Patheon Inc. (Thermo Fisher Scientific Inc.) and Boehringer Ingelheim Group are the major companies operating in the Pharmaceutical CMO Market.

Which is the fastest growing region in Pharmaceutical CMO Market?

Asia Pacific is estimated to grow at the highest CAGR over the forecast period (2024-2029).

Which region has the biggest share in Pharmaceutical CMO Market?

In 2024, the North America accounts for the largest market share in Pharmaceutical CMO Market.

What years does this Pharmaceutical CMO Market cover, and what was the market size in 2023?

In 2023, the Pharmaceutical CMO Market size was estimated at USD 161.31 billion. The report covers the Pharmaceutical CMO Market historical market size for years: 2019, 2020, 2021, 2022 and 2023. The report also forecasts the Pharmaceutical CMO Market size for years: 2024, 2025, 2026, 2027, 2028 and 2029.

Pharmaceutical CMO Industry Report

Statistics for the 2024 Pharmaceutical CMO market share, size and revenue growth rate, created by Mordor Intelligence™ Industry Reports. Pharmaceutical CMO analysis includes a market forecast outlook to 2029 and historical overview. Get a sample of this industry analysis as a free report PDF download.