Military Aircraft MRO Market Size

| Study Period | 2019 - 2033 |

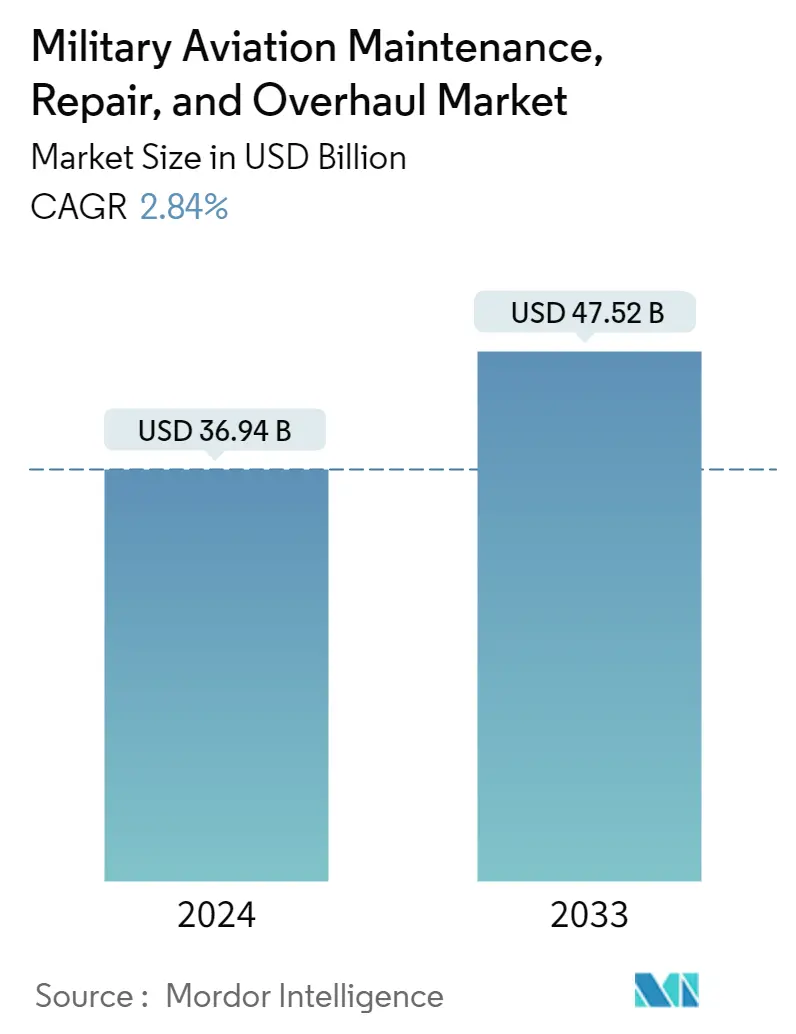

| Market Size (2024) | USD 36.94 Billion |

| Market Size (2033) | USD 47.52 Billion |

| CAGR (2024 - 2033) | 2.84 % |

| Fastest Growing Market | Europe |

| Largest Market | North America |

Major Players

*Disclaimer: Major Players sorted in no particular order |

Need a report that reflects how COVID-19 has impacted this market and its growth?

Military Aircraft MRO Market Analysis

The Military Aviation Maintenance, Repair, and Overhaul Market size is estimated at USD 36.94 billion in 2024, and is expected to reach USD 47.52 billion by 2033, growing at a CAGR of 2.84% during the forecast period (2024-2033).

The military aviation sector has witnessed a mild impact of the COVID-19 pandemic. Growing defense expenditure and rising procurement contracts for fighter jets led to steady growth in the market. Supply chain disruptions, production halt from MRO players, and economic slowdown hinder market growth during the pandemic. The market showcased a strong recovery post-pandemic due to the increasing number of military modernization programs.

The military aviation MRO market is experiencing steady growth due to the increasing demand for maintenance, repair, and overhaul services for military aircraft. The demand is driven by factors such as expanding military fleets, the need for lifecycle extension of existing aircraft, and the rising complexity of aircraft systems. The procurement of new military aircraft leads to larger fleet size, subsequently increasing the demand for MRO services to support these aircraft throughout their operational lifespan.

Defense organizations seek to maximize the value and longevity of their aircraft assets. The market for MRO services is experiencing growth, driven by the need for structural repairs, avionics upgrades, engine overhauls, and system modifications. The evolution of technology in military aircraft, such as advanced materials, avionics, and mission systems, contributes to the growth of the MRO market. As aircraft become more sophisticated, specialized expertise and advanced diagnostics tools are required to maintain and repair these complex systems effectively.

Military Aircraft MRO Market Trends

Fixed-Wing Aircraft Segment Will Showcase the Highest Growth During the Forecast Period

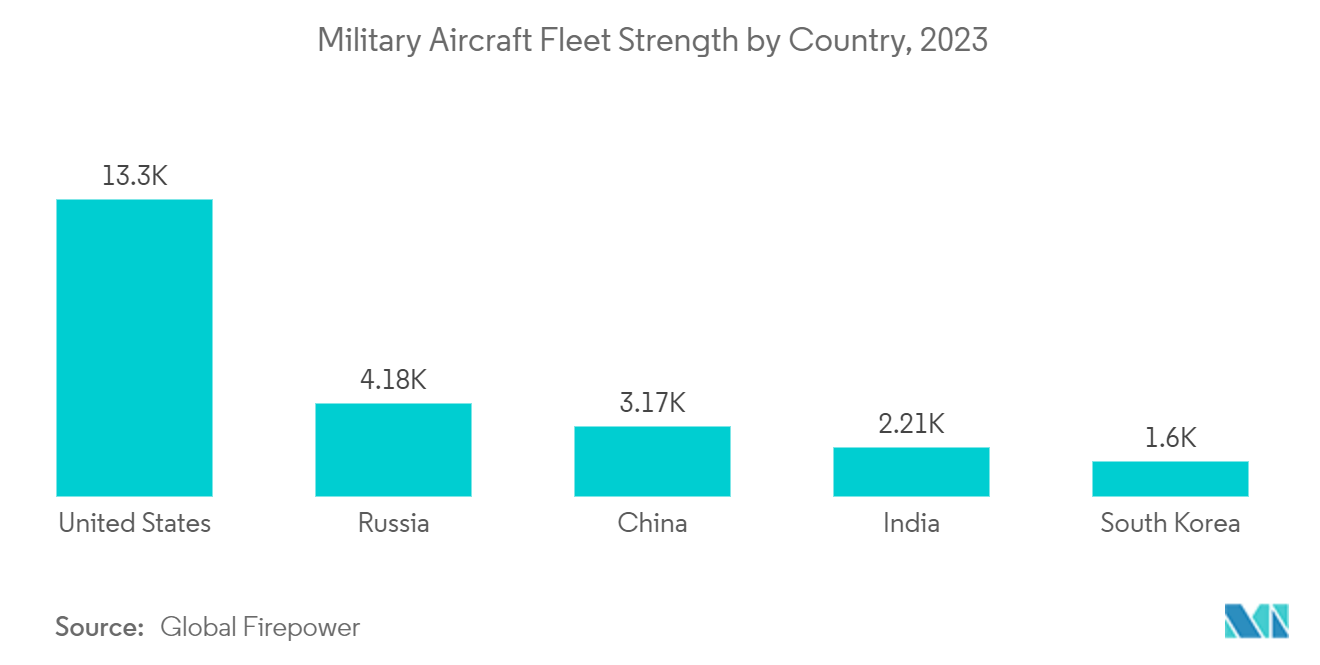

Fixed-wing aircraft segment is projected to show significant growth in the military aviation MRO market during the forecast period. The growth is attributed to the increasing demand for fighter jets and rising expenditure on improving military aviation capabilities from the defense forces. The United States and Russia have the highest number of military aircraft due to higher expenditures on the procurement of next-generation fighter jets. Rising warfare situations, political disputes among neighboring countries, and a growing number of cross-border conflicts lead to growing spending on the defense sector. The United States has the highest military aircraft fleet of 13,232 in 2021, followed by Russia, with a fleet of 4,143 aircraft. Fixed-wing aircraft in the armed forces play critical roles during war or special missions. This always necessitates proper maintenance of this aircraft and requires upgrades after certain years of operation to extend its service life.

In June 2023, the Norwegian Defense Materiel Agency (NDMA) signed an extension contract with Kongsberg Aviation Maintenance Services to overhaul and make ready-for-sale a total of 32 F-16 combat aircraft. The contract also includes technical assistance and support for training Romanian technical personnel. The value of the contract was over USD 63.61 million. In April 2023, GE Aerospace signed an agreement with Lockheed Martin Corporation to support avionics and electrical power systems on the F-35 military aircraft. Under the four-year agreement, the company will provide MRO services for GE Aerospace systems on the F-35 Lightning II aircraft. The company will service the F-35 systems at its repair and maintenance locations in California, Georgia, and Utah. Thus, growing procurement of fighter jets and rising expenditure on military aircraft modernization programs drive the growth of the market during the forecast period.

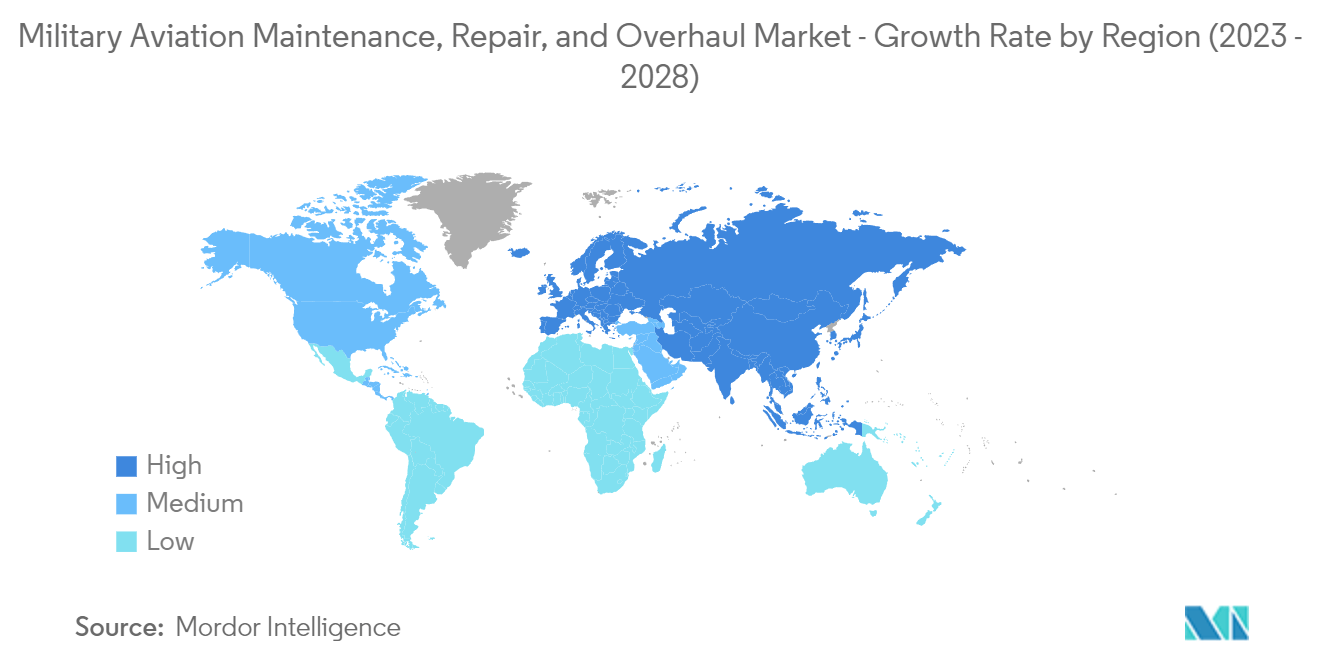

North America to Dominate Market Share

North America held the highest shares in the market and continued its domination during the forecast period. The growth is due to the presence of the largest military aircraft fleet, growing spending on enhancing US Air Force (USAF) capabilities, and rising aircraft modernization programs.

The US currently has the largest fleet of military aircraft in the world. In 2023, the country operates a fleet of 2,757 combat aircraft, 731 special mission aircraft, 632 tanker aircraft, 962 transport aircraft, 5,584 combat helicopters, and 2,634 training aircraft/ helicopters. The major driving factor for the MRO in this country is the significant demand to upgrade such a vast fleet with the latest technologies and systems. The US Department of Defense (DoD) plans to spend USD 61.1 billion on aircraft and related systems in 2024. The DoD plans to buy a diverse mix of 270 aircraft, ranging from nearly USD 700 million B-21 stealth bombers for the USAF to twin-engine King Air 200-derived trainers for the US Navy.

In FY2021, the US DoD received USD 32.5 billion for procurement, and research, operations & maintenance, development, test, and evaluation appropriations for depot maintenance activities. The US DoD budget requests for FY2022 and FY2023 depot maintenance reached USD 32.6 and USD 35.1 billion, respectively. According to DoD, the FY2023 budget request would fund 50% of total executable Army depot maintenance requirements, 85% of Air Force requirements, 80% of Marine Corps requirements, 71% of Navy requirements, and 83% of Space Force requirements. The majority of the MRO expenditure is on the nation's large fleet of multi-role aircraft, transport aircraft, and surveillance aircraft that require high maintenance on engines and airframes, along with field and component maintenance services.

Military Aircraft MRO Industry Overview

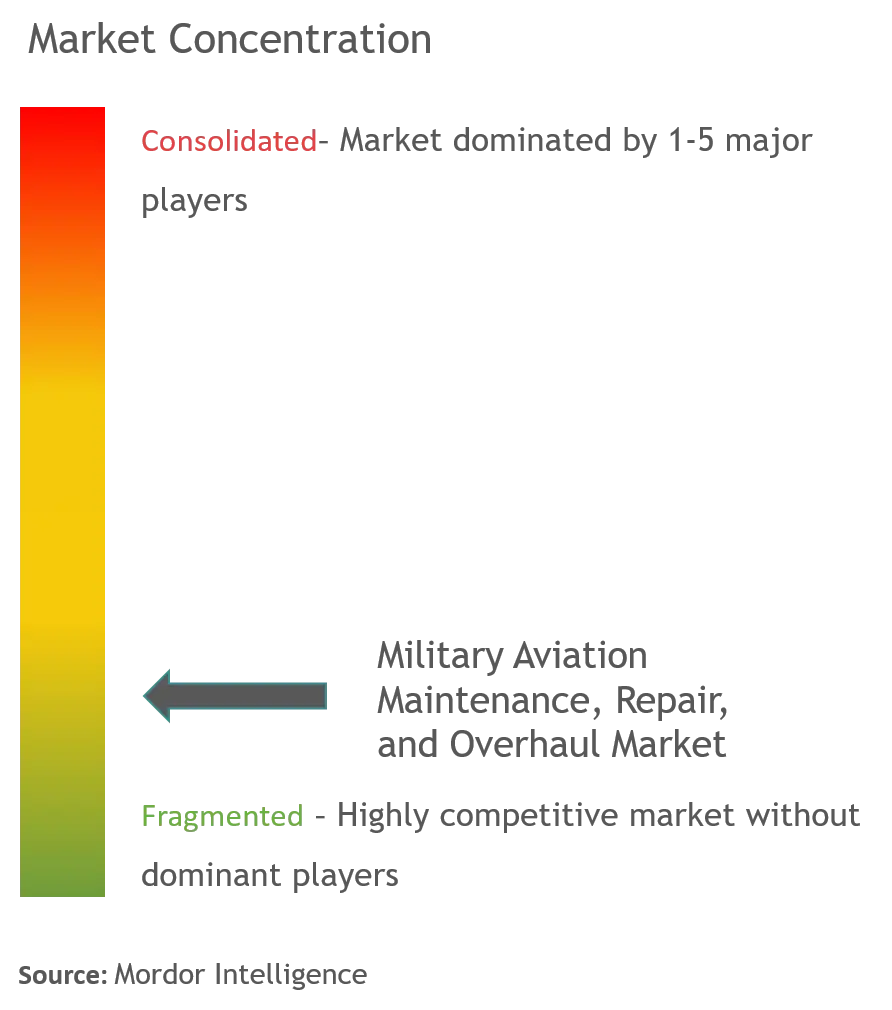

The market is fragmented, with numerous local and international players providing various MRO services to the existing military aircraft fleet. The major players in the military aviation MRO market are Lockheed Martin Corporation, Safran, The Boeing Company, Raytheon Technologies Corporation, and BAE Systems plc.

Strategic partnerships between the players may help them gain more contracts while expanding their reach to untapped markets in the long run. As most MRO contracts are for the long term, it could be a time-consuming process for new players to establish themselves in the market by competing with the existing ones. Artificial intelligence (AI)-based predictive maintenance technologies are also envisioned to witness mass adoption during the forecast period. Potential investments would be required to enhance the IT capabilities of MRO operators for maintenance execution, supply chain management, enhancing mobility, and adopting e-signatures. Advanced data analytics are also being used by MROs for inventory optimization to plan, stock, and optimize spares as and when required at minimal procurement costs. Such tools enable operators to function efficiently, derive maximum profits, and support the digitization of global aircraft MRO operations.

Military Aircraft MRO Market Leaders

BAE Systems plc

Lockheed Martin Corporation

The Boeing Company

Raytheon Technologies Corporation

Safran

*Disclaimer: Major Players sorted in no particular order

Military Aircraft MRO Market News

April 2023: Brazilian Air Force selected StandardAero to provide comprehensive maintenance, repair, and overhaul (MRO) services for the Rolls-Royce AE 3007 engines that power its fleet of Embraer ERJ-145 aircraft. Under the exclusive multi-year agreement, StandardAero will provide MRO services for FAB's AE 3007A equipped fleet from its facility located in Maryville, United States, which is an OEM-approved Authorized Maintenance Center (AMC) for the AE 3007 family of engines.

March 2023: GE Aerospace granted a service contract extension to ITP Aero to conduct maintenance, repair, and overhaul services for CT7 engines at its facility in Albacete, Spain. The CT7-8 is a powerful engine designed to meet the demanding mission needs of commercial heavy-lift helicopters and modern military medium helicopters throughout the world.

Military Aircraft MRO Market Report - Table of Contents

1. INTRODUCTION

1.1 Study Assumptions

1.2 Scope of the Study

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET DYNAMICS

4.1 Market Overview

4.2 Market Drivers

4.2.1 Growing Demand for Stealth Aircraft

4.3 Market Restraints

4.3.1 Replacement of Ageing Aircraft

4.4 Industry Attractiveness - Porter's Five Forces Analysis

4.4.1 Threat of New Entrants

4.4.2 Bargaining Power of Buyers/Consumers

4.4.3 Bargaining Power of Suppliers

4.4.4 Threat of Substitute Products

4.4.5 Intensity of Competitive Rivalry

5. MARKET SEGMENTATION

5.1 By MRO Type

5.1.1 Engine MRO

5.1.2 Components and Modifications MRO

5.1.3 Airframe MRO

5.1.4 Field Maintenance

5.2 By Aircraft Type

5.2.1 Fixed-wing Aircraft

5.2.2 Rotorcraft

5.3 By Geography

5.3.1 North America

5.3.1.1 United States

5.3.1.2 Canada

5.3.2 Europe

5.3.2.1 United Kingdom

5.3.2.2 France

5.3.2.3 Germany

5.3.2.4 Russia

5.3.2.5 Rest of Europe

5.3.3 Asia-Pacific

5.3.3.1 China

5.3.3.2 India

5.3.3.3 Japan

5.3.3.4 South Korea

5.3.3.5 Rest of Asia-Pacific

5.3.4 Latin America

5.3.4.1 Brazil

5.3.4.2 Rest of Latin America

5.3.5 Middle East & Africa

5.3.5.1 United Arab Emirates

5.3.5.2 Saudi Arabia

5.3.5.3 Qatar

5.3.5.4 Egypt

5.3.5.5 Rest of Middle East & Africa

6. COMPETITIVE LANDSCAPE

6.1 Vendor Market Share

6.2 Company Profiles

6.2.1 The Boeing Company

6.2.2 BAE Systems plc

6.2.3 Elbit Systems Ltd.

6.2.4 Saab AB

6.2.5 Lockheed Martin Corporation

6.2.6 General Atomics

6.2.7 Northrop Grumman Corporation

6.2.8 Amentum Services Inc.

6.2.9 Raytheon Technologies Corporation

6.2.10 Rolls-Royce plc

6.2.11 Safran

6.2.12 MTU Aero Engines AG

7. MARKET OPPORTUNITIES AND FUTURE TRENDS

Military Aircraft MRO Industry Segmentation

Aircraft MRO includes tasks performed to ensure the continuing airworthiness of an aircraft and its parts. MRO service providers perform overhaul, inspection, replacement, defect rectification, and the embodiment of modifications in compliance with airworthiness directives and repair.

The Report Covers Military Aviation MRO Market Companies & Trends, and it is Segmented by MRO Type (Engine MRO, Components and Modifications MRO, Airframe MRO, and Field Maintenance), Aircraft Type (Fixed-wing Aircraft and Rotorcraft), and Geography (North America (United States and Canada), Europe (United Kingdom, France, Germany, Russia, and Rest of Europe), Asia-Pacific (China, India, Japan, South Korea, and Rest of Asia-Pacific), Latin America (Brazil and Rest of Latin America), and Middle East & Africa (United Arab Emirates, Saudi Arabia, Qatar, Egypt, and Rest of Middle East & Africa)). The report offers the market size in value terms in USD (billion) for all the abovementioned segments.

| By MRO Type | |

| Engine MRO | |

| Components and Modifications MRO | |

| Airframe MRO | |

| Field Maintenance |

| By Aircraft Type | |

| Fixed-wing Aircraft | |

| Rotorcraft |

| By Geography | |||||||

| |||||||

| |||||||

| |||||||

| |||||||

|

Military Aircraft MRO Market Research FAQs

How big is the Military Aviation Maintenance, Repair, and Overhaul Market?

The Military Aviation Maintenance, Repair, and Overhaul Market size is expected to reach USD 36.94 billion in 2024 and grow at a CAGR of 2.84% to reach USD 47.52 billion by 2033.

What is the current Military Aviation Maintenance, Repair, and Overhaul Market size?

In 2024, the Military Aviation Maintenance, Repair, and Overhaul Market size is expected to reach USD 36.94 billion.

Who are the key players in Military Aviation Maintenance, Repair, and Overhaul Market?

BAE Systems plc, Lockheed Martin Corporation, The Boeing Company, Raytheon Technologies Corporation and Safran are the major companies operating in the Military Aviation Maintenance, Repair, and Overhaul Market.

Which is the fastest growing region in Military Aviation Maintenance, Repair, and Overhaul Market?

Europe is estimated to grow at the highest CAGR over the forecast period (2024-2033).

Which region has the biggest share in Military Aviation Maintenance, Repair, and Overhaul Market?

In 2024, the North America accounts for the largest market share in Military Aviation Maintenance, Repair, and Overhaul Market.

What years does this Military Aviation Maintenance, Repair, and Overhaul Market cover, and what was the market size in 2023?

In 2023, the Military Aviation Maintenance, Repair, and Overhaul Market size was estimated at USD 35.92 billion. The report covers the Military Aviation Maintenance, Repair, and Overhaul Market historical market size for years: 2019, 2020, 2021, 2022 and 2023. The report also forecasts the Military Aviation Maintenance, Repair, and Overhaul Market size for years: 2024, 2025, 2026, 2027, 2028, 2029, 2030, 2031, 2032 and 2033.

Military Aircraft MRO Industry Report

Statistics for the 2024 Military Aviation Maintenance, Repair, and Overhaul market share, size and revenue growth rate, created by Mordor Intelligence™ Industry Reports. Military Aviation Maintenance, Repair, and Overhaul analysis includes a market forecast outlook to for 2024 to 2029 and historical overview. Get a sample of this industry analysis as a free report PDF download.