Life and Non-Life Insurance Market Size

| Study Period | 2020 - 2029 |

| Base Year For Estimation | 2023 |

| CAGR | > 4.00 % |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

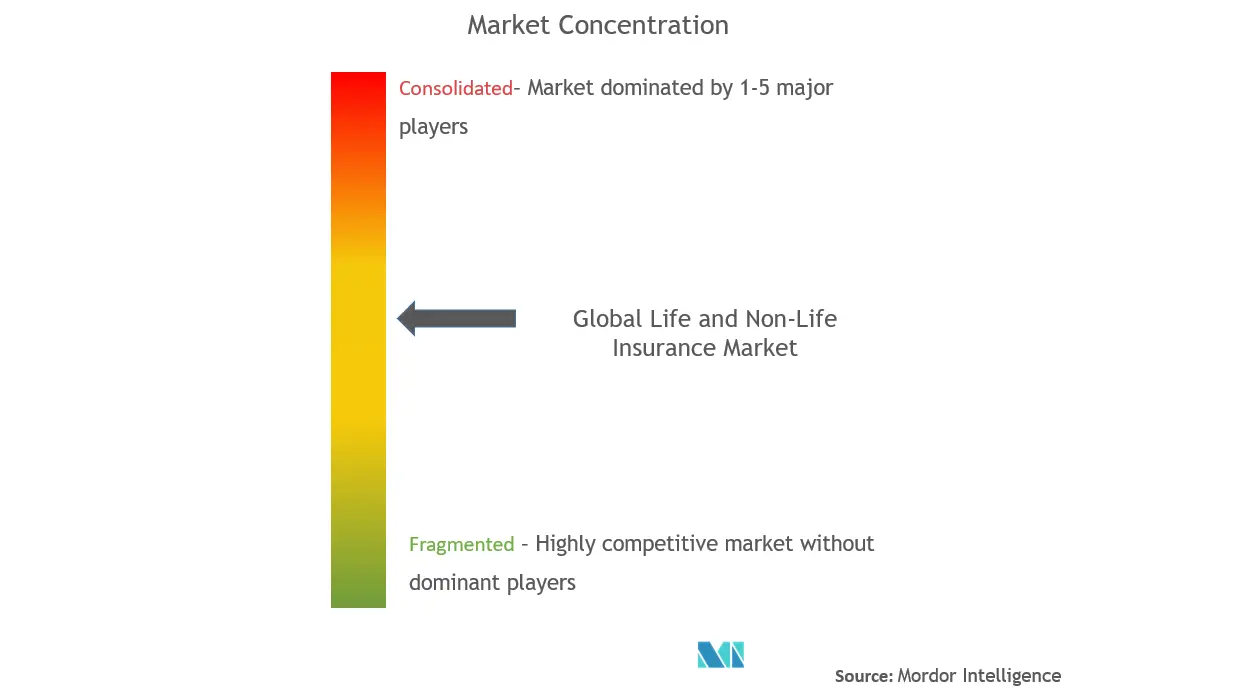

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order |

Need a report that reflects how COVID-19 has impacted this market and its growth?

Life and Non-Life Insurance Market Analysis

The global life and non-life insurance market is estimated at approximately USD 8100 billion during the current year and is poised to grow at a CAGR of greater than 4% during the forecast period. Direct insurance providers are entities that are engaged in primary underwriting and assuming the risk of annuities and insurance policies. Reinsurance providers are businesses that assume all or part of the risk associated with an existing insurance policy or set of policies originally underwritten by another insurance carrier (direct insurance carrier). The main types of insurance are life insurance, property and casualty insurance, and health and medical insurance. Life insurance refers to the insurance that covers the package of lifetime critical benefits for the individual. The various mode is online and offline. The services are used by corporate and individual end users. The insurtech sector has seen much technological and investment development over the past few years. Traditional insurance business lines, such as health, auto, and commercial, are being revolutionized by new digital-centric startups. New technologies, such as AI and IoT, have been re-architecting insurance data, the foundation of the insurance industry.

The COVID-19 crisis continues to have a significant impact on individuals, society, businesses, and the wider economy across the world. The insurance industry has not escaped its impact, but insurers have responded quickly to the crisis. As the broader economy recovers and responds to the pandemic, insurers will face several challenges but also see many new opportunities in the medium to long term. The pandemic significantly changed the claims experiences for several types of insurance. In some countries, there has been an increase in claims on the life insurance segment due to COVID-19. The crisis has affected the solvency, profitability, and profitability of the insurance sector. There was a strong recovery in global insurance premiums growth in 2021.

Life and Non-Life Insurance Market Trends

This section covers the major market trends shaping the Life & Non-Life Insurance Market according to our research experts:

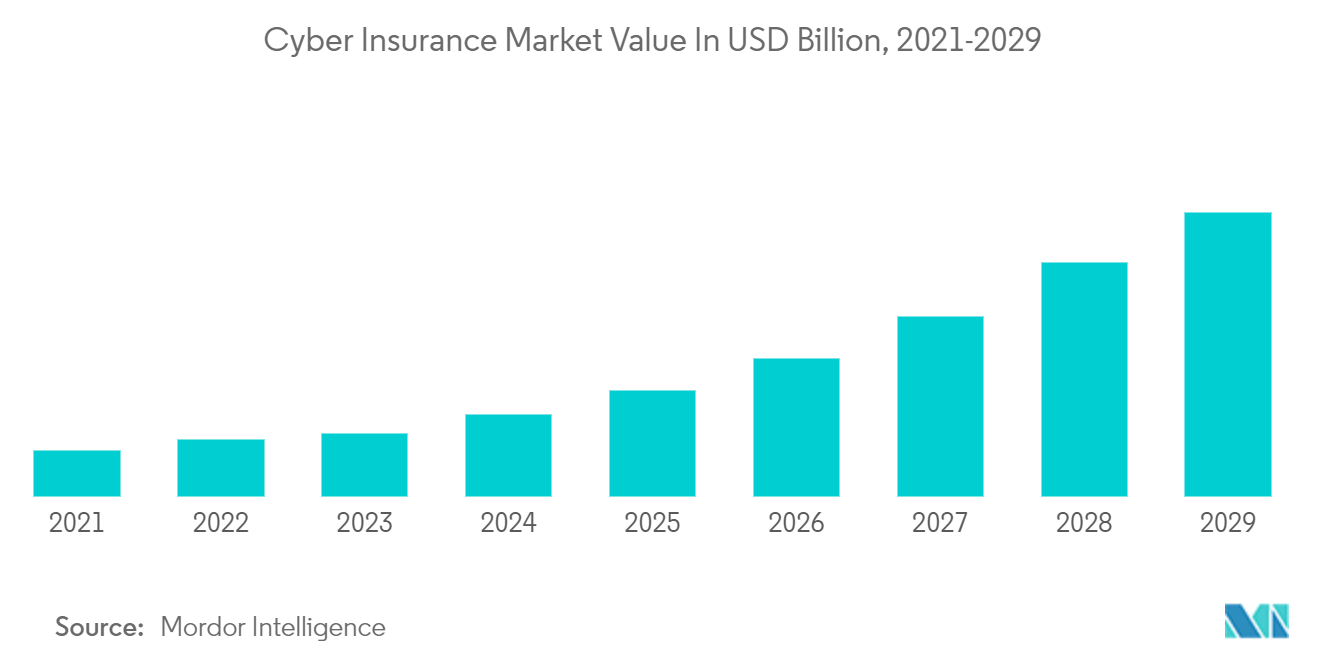

Cyber Insurance is Driving the Market

Cyber insurance solutions enable organizations to mitigate the risk of cyber threat activity, such as data breaches and cyberattacks. It protects businesses from the cost of internet-based attacks affecting information governance, IT infrastructure, and information policy, which often are not covered by traditional insurance products and commercial liability policies. The increasing data breaches and cybersecurity risks drive businesses to implement cyber insurance policies. Also, many countries impose fines and mandate governing terms and conditions on companies for any data breach. Small and medium enterprises are also being targeted for cyberattacks. This fuels the demand for new insurance products for small businesses.

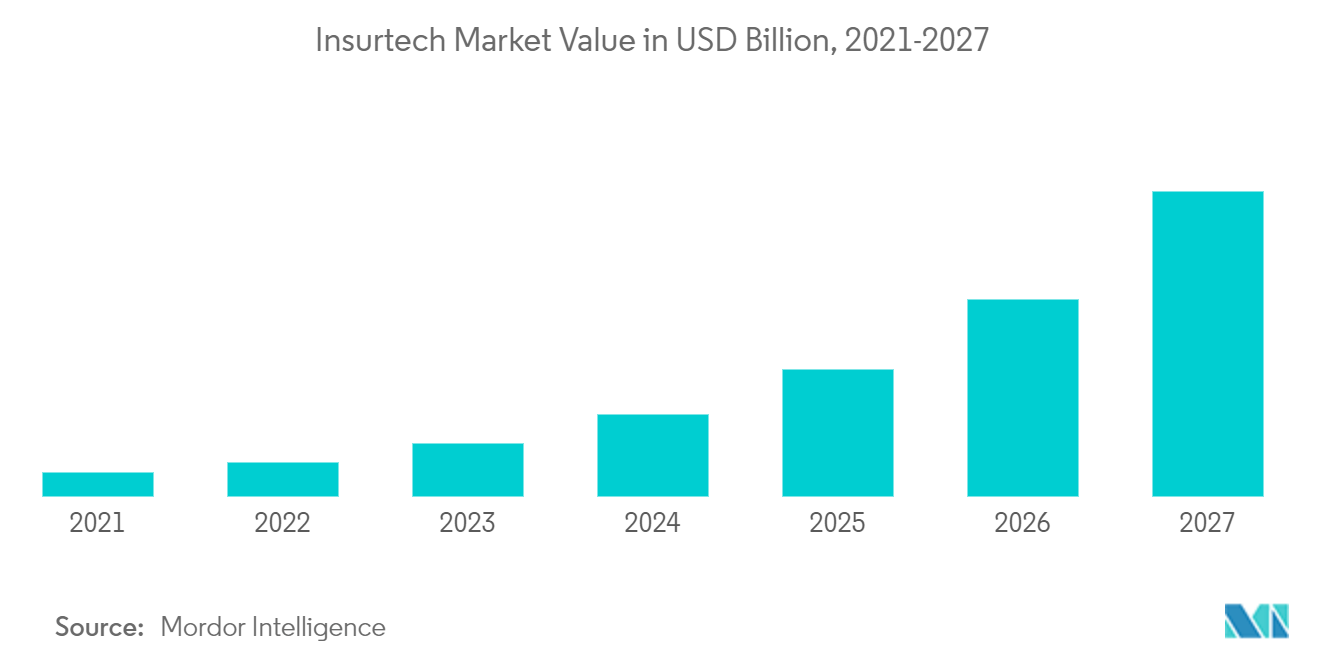

Significant Growth in Insurtech Adoption is Driving the Market

The increasing number of insurance claims worldwide is one of the major factors accentuating the market growth. Auto, life, and home are the most common insurance claims secured by people worldwide. The use of technology in insurance can make products more affordable, businesses more profitable, and provide access to new risk pools. Insurance companies have been integrating digital technologies into their traditional processes and everyday workflows to reduce manual efforts, time, and costs. As the insurance sectors of developing and emerging markets become more sophisticated, it can be expected that digital solutions may filter down through the insurance supply chain, driving operational efficiency and, ultimately, profitability, as is already being seen in more advanced markets.

Life and Non-Life Insurance Industry Overview

The report covers the major players operating in the global life and non-life insurance market. The market is fragmented; technology adoption in the insurance sector, government initiatives toward changes in insurance regulations, like MTPL (third-party motor liability), and many other factors can drive the market during the forecast period. Companies such as AXA Group, United Health Group, Allianz, and China Life, among others have been profiled in the report.

Life and Non-Life Insurance Market Leaders

Ping An Insurance Group

UnitedHealth Group

Allianz

AXA Group

China Life

*Disclaimer: Major Players sorted in no particular order

Life and Non-Life Insurance Market News

- June 2022: UnitedHealthcare announced the plans of acquiring EMIS Group. The EMIS Group is a leading health technology company based in the UK. The deal is expected to be an all-cash deal of GBP 1.24 billion (USD 1.5 billion).

- February 2022: Allianz SE one of the leading insurance company globally announced that is entering into a Share Purchase Agreement (SPA), to acquire 72% of European Reliance General Insurance Company SA ('European Reliance'). European Reliance is one of the leader in the Greek insurance sector with a network of 5,667 agents and 110 retail offices.

Life and Non-Life Insurance Market Report - Table of Contents

1. INTRODUCTION

1.1 Study Assumptions and Market Definition

1.2 Scope of the Study

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET INSIGHTS AND DYNAMICS

4.1 Market Overview

4.2 Market Drivers

4.3 Market Restraints

4.4 Industry Attractiveness - Porter's Five Forces Analysis

4.4.1 Threat of New Entrants

4.4.2 Bargaining Power of Buyers/Consumers

4.4.3 Bargaining Power of Suppliers

4.4.4 Threat of Substitute Products

4.4.5 Intensity of Competitive Rivalry

4.5 Insights into Various Regulatory Trends Shaping the Market

4.6 Insights into Impact of Technology in the Market

4.7 Impact of COVID-19 on the Market

5. MARKET SEGMENTATION

5.1 By Insurance Type

5.1.1 Life Insurance

5.1.1.1 Individual

5.1.1.2 Group

5.1.2 Non-life Insurance

5.1.2.1 Home

5.1.2.2 Motor

5.1.2.3 Other Non-life Insurances

5.2 By Distribution Channel

5.2.1 Direct

5.2.2 Agency

5.2.3 Banks

5.2.4 Other Distribution Channels

5.3 Geography

5.3.1 North America

5.3.1.1 United States

5.3.1.2 Canada

5.3.1.3 Mexico

5.3.1.4 Rest of North America

5.3.2 Europe

5.3.2.1 Germany

5.3.2.2 United Kingdom

5.3.2.3 France

5.3.2.4 Russia

5.3.2.5 Spain

5.3.2.6 Rest of Europe

5.3.3 Asia-Pacific

5.3.3.1 India

5.3.3.2 China

5.3.3.3 Japan

5.3.3.4 Rest of Asia-Pacific

5.3.4 South America

5.3.4.1 Brazil

5.3.4.2 Argentina

5.3.4.3 Rest of South America

5.3.5 Middle East

5.3.5.1 United Arab Emirates

5.3.5.2 Saudi Arabia

5.3.5.3 Rest of the Middle East

6. COMPETITIVE LANDSCAPE

6.1 Market Concentration Overview

6.2 Company Profiles

6.2.1 Ping An Insurance Group

6.2.2 UnitedHealth Group

6.2.3 Allianz

6.2.4 AXA Group

6.2.5 China Life

6.2.6 AIA Group

6.2.7 MetLife

6.2.8 Zurich Insurance

6.2.9 Cigna*

- *List Not Exhaustive

7. MARKET OPPORTUNITIES AND FUTURE TRENDS

8. DISCLAIMER AND ABOUT US

Life and Non-Life Insurance Industry Segmentation

The Life and Non-life Insurance Market is segmented by Insurance Type (Life and Non-Life Insurance), Distribution Channel (Direct, Agency, Banks, and Other Distribution Channels), and Geography (North America, Europe, Asia-Pacific, South America, and the Middle East). The report offers market size and values in (USD billion) during the forecast years for the above segments.

| By Insurance Type | |||||

| |||||

|

| By Distribution Channel | |

| Direct | |

| Agency | |

| Banks | |

| Other Distribution Channels |

| Geography | ||||||||

| ||||||||

| ||||||||

| ||||||||

| ||||||||

|

Life and Non-Life Insurance Market Research FAQs

What is the current Global Life and Non-Life Insurance Market size?

The Global Life and Non-Life Insurance Market is projected to register a CAGR of greater than 4% during the forecast period (2024-2029)

Who are the key players in Global Life and Non-Life Insurance Market?

Ping An Insurance Group, UnitedHealth Group, Allianz, AXA Group and China Life are the major companies operating in the Global Life and Non-Life Insurance Market.

Which is the fastest growing region in Global Life and Non-Life Insurance Market?

Asia Pacific is estimated to grow at the highest CAGR over the forecast period (2024-2029).

Which region has the biggest share in Global Life and Non-Life Insurance Market?

In 2024, the North America accounts for the largest market share in Global Life and Non-Life Insurance Market.

What years does this Global Life and Non-Life Insurance Market cover?

The report covers the Global Life and Non-Life Insurance Market historical market size for years: 2020, 2021, 2022 and 2023. The report also forecasts the Global Life and Non-Life Insurance Market size for years: 2024, 2025, 2026, 2027, 2028 and 2029.

Life and Non-Life Insurance Industry Report

Statistics for the 2024 Life and Non-Life Insurance market share, size and revenue growth rate, created by Mordor Intelligence™ Industry Reports. Life and Non-Life Insurance analysis includes a market forecast outlook to 2029 and historical overview. Get a sample of this industry analysis as a free report PDF download.