Ketogenic Diet Market Size and Share

Market Overview

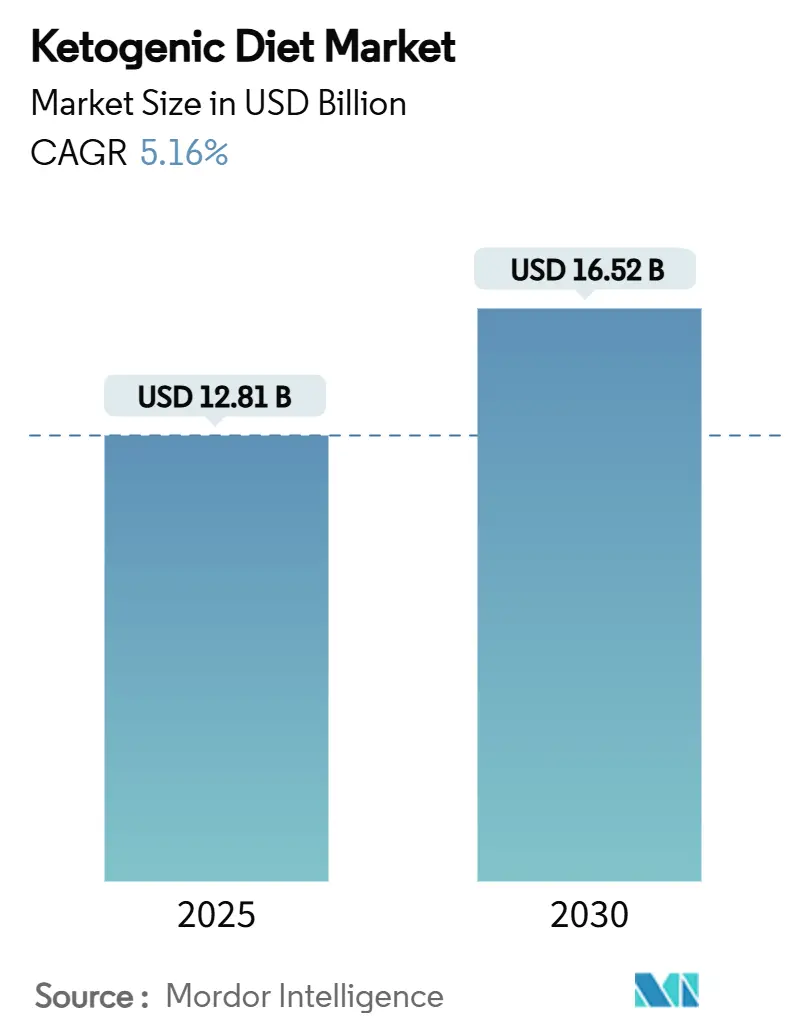

| Study Period | 2020 - 2030 |

| Market Size (2025) | USD 12.81 Billion |

| Market Size (2030) | USD 16.52 Billion |

| Growth Rate (2025 - 2030) | 5.16% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Low |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Ketogenic Diet Market Analysis by Mordor Intelligence

The ketogenic food products market is valued at USD 12.81 billion in 2025 and is forecast to reach USD 16.52 billion by 2030, advancing at a 5.16% CAGR. This growth is attributed to increasing awareness of metabolic health, a global shift toward low-carb dietary preferences, and continuous product advancements that enhance the convenience of ketogenic consumption. Strategic investments in functional ingredients, such as medium-chain triglycerides (MCTs) and exogenous ketones, are driving portfolio diversification. Additionally, regulatory developments in the U.S. and Europe are improving labeling transparency and creating new opportunities for health-related claims. North America continues to dominate the market due to strong brand presence, while the Asia-Pacific region is experiencing faster growth, driven by rising disposable incomes, increasing diabetes prevalence, and rapidly evolving retail infrastructure. Furthermore, the expansion of e-commerce platforms and direct-to-consumer models is enhancing market dynamics by offering a wider product range and enabling tailored nutrition solutions.

Key Report Takeaways

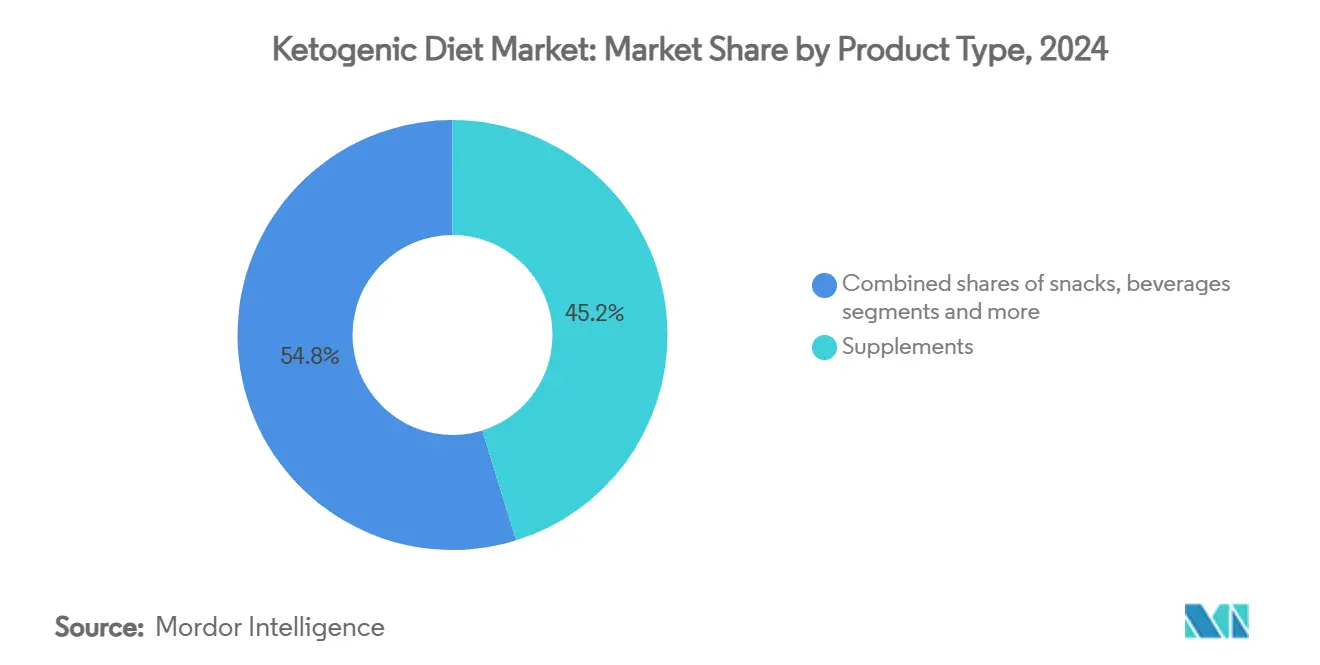

- By product type, supplements led with 45.21% of the ketogenic food products market share in 2024; beverages record the highest projected CAGR at 6.56% through 2030.

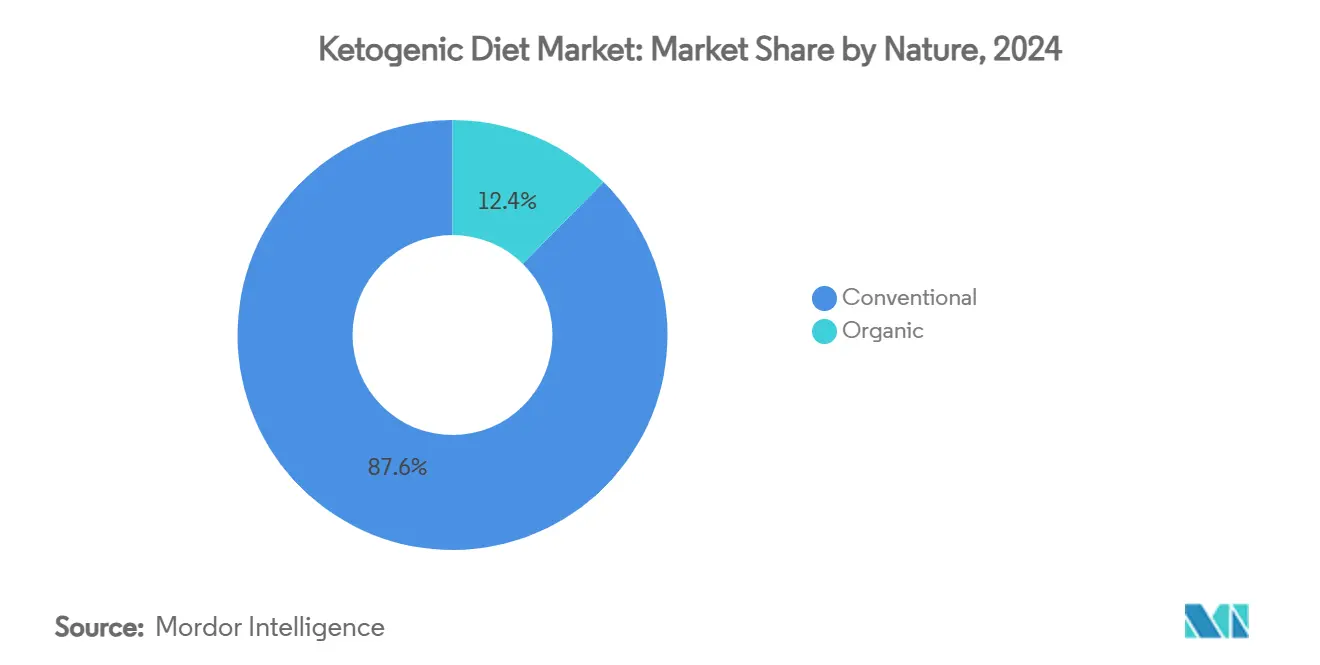

- By nature, conventional items commanded 87.63% of the ketogenic food products market size in 2024; organic offerings are forecast to grow at an 8.07% CAGR between 2025-2030.

- By distribution channel, supermarkets and hypermarkets held 61.87% of the ketogenic food products market in 2024, while online retail is projected to expand at a 7.33% CAGR to 2030.

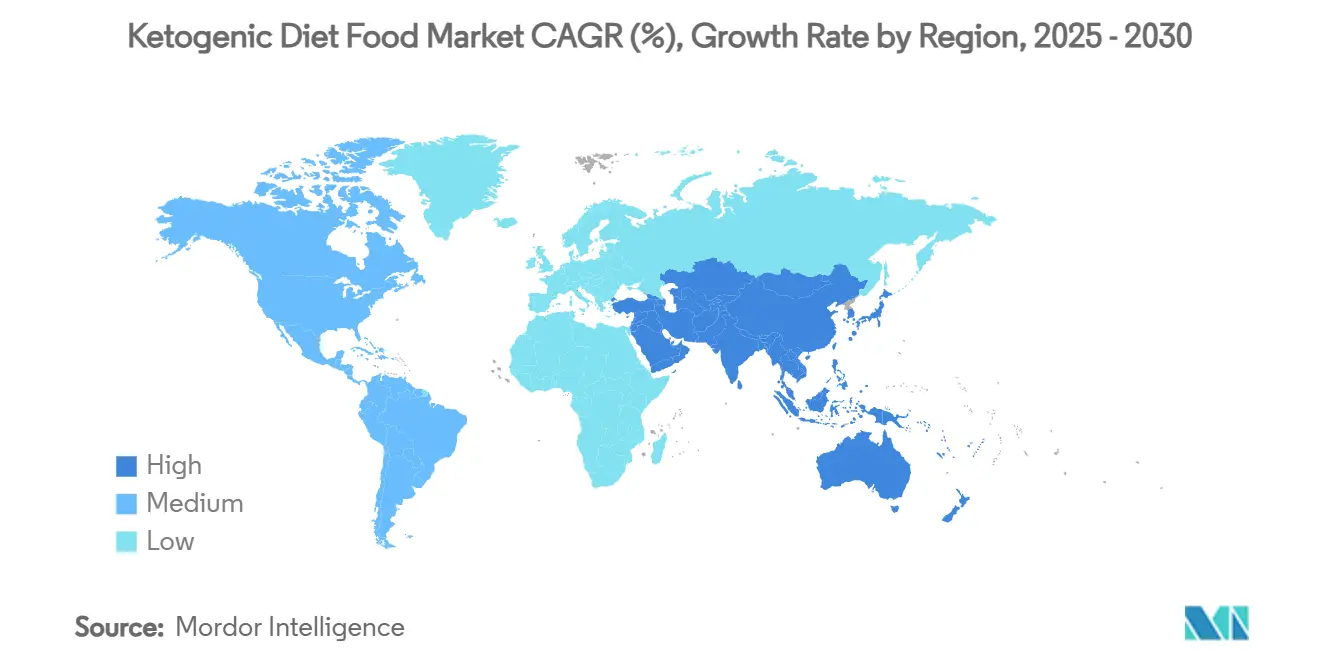

- By geography, North America accounted for 39.4% of the ketogenic food products market in 2024, whereas Asia-Pacific posts the fastest regional CAGR of 7.59% to 2030.

Global Ketogenic Diet Market Trends and Insights

Drivers Impact Analysis

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Rising prevalence of obesity and lifestyle disorders | +1.8% | Global, highest in North America and Asia-Pacific | Long term (≥ 4 years) |

| Expanding retail availability of keto-labelled SKUs | +1.2% | Global, led by North America and Europe | Medium term (2-4 years) |

| Growing adoption among athletes and fitness enthusiasts | +0.9% | North America, Europe, urban Asia-Pacific | Medium term (2-4 years) |

| Growing demand for low-carb and clean label foods | +1.1% | Global, premium segments in developed markets | Long term (≥ 4 years) |

| Expansion of e-commerce and DTC channels | +0.8% | Global, fastest in Asia-Pacific and Latin America | Short term (≤ 2 years) |

| Innovation in product offerings drives the market | +0.7% | Global, concentrated in North America and Europe | Medium term (2-4 years) |

Source: Mordor Intelligence

Rising prevalence of obesity and lifestyle disorders

As global obesity rates continue to climb, the demand for ketogenic food products is witnessing significant growth. The impact of this metabolic challenge extends beyond weight management, driving the need for solutions that address insulin resistance and other metabolic disorders. In 2024, 1 billion individuals were affected by obesity, with one in eight deaths from non-communicable diseases attributed to being overweight or obese [1]Source: Global Obesity Observatory. "World Obesity Atlas 2024,"worldobesity.org. Clinical studies have demonstrated the effectiveness of ketogenic diets in addressing obesity, outperforming traditional low-fat diets in promoting weight loss due to improved appetite regulation and enhanced insulin sensitivity. Dietary interventions, such as the ketogenic diet, are increasingly viewed as cost-efficient and proactive strategies to combat obesity, especially when compared to the high costs associated with managing obesity-related chronic conditions. As consumers prioritize effective, scientifically supported, and often fast-acting weight management solutions, the ketogenic diet has positioned itself as a leading choice in the market.

Expanding retail availability of keto-labelled SKUs

Ketogenic products, which were previously limited to niche health stores, have now transitioned into mainstream supermarkets, driven by accelerated retail penetration. This significant shift has been supported by regulatory advancements, particularly the FDA's GRAS (Generally Recognized as Safe) approval of D-β-hydroxybutyrate. This regulatory approval permits its inclusion in sports and nutritional beverages at concentrations of up to 6 grams per serving, paving the way for broader product development and market acceptance. Retailers are showcasing a strategic commitment to the ketogenic category by introducing dedicated ketogenic sections and employing cross-merchandising strategies with diabetes management products. Additionally, advancements in supply chain management have played a pivotal role in ensuring consistent product availability. These improvements have effectively mitigated previous challenges, such as limited product supply and inconsistent quality standards, thereby fostering greater consumer adoption and trust in the category.

Growing adoption among athletes and fitness enthusiasts

Athletic performance applications are driving a paradigm shift in the sports nutrition market, moving away from traditional carbohydrate-based approaches. Scientific studies have confirmed the metabolic benefits of ketosis for endurance activities. For example, compounds such as bis-octanoyl (R)-1,3-butanediol have demonstrated safety and tolerability in healthy adults while effectively increasing blood β-hydroxybutyrate to therapeutic levels. Professional athlete endorsements have fueled demand among recreational athletes, particularly in endurance sports, where sustained energy delivery offers a competitive edge. In 2024, the Japan Sports Agency reported that 13.7% of fitness club users were men, while 17.5% were women, highlighting gender-specific trends in fitness participation [2]Source: Japan Sports Agency, "Opinion survey on sports participation 2024,"mext.go.jp. Companies are accelerating innovation in ketogenic sports nutrition. For instance, in August 2024, KEY introduced zero-sugar energy drinks powered by ketones, targeting consumers seeking long-lasting energy without the drawbacks of sugar crashes.

Growing demand for low-carb and clean label foods

Rising consumer awareness of nutritional labels has driven demand for minimally processed products with transparent ingredient lists, aligning closely with ketogenic dietary trends. Both the clean label movement and ketogenic diets focus on whole food ingredients and low carbohydrate content. Regulatory developments, such as updated FDA guidelines allowing products like nuts, seeds, and avocados to carry "healthy" claims, have further validated high-fat, low-carb formulations. Innovations in natural sweeteners and fat sources have facilitated the development of clean-label ketogenic products without compromising on taste or texture. Companies that effectively integrate ketogenic and clean-label strategies can leverage premium pricing while addressing diverse consumer needs, establishing a sustainable competitive advantage in the market.

Restraints Impact Analysis

| RESTRAINT | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Health-risk concerns and nutritional deficiencies | -0.8% | Global, higher in conservative dietary regions | Long term (≥ 4 years) |

| Strict dietary compliance required | -0.6% | Global, strongest where carb staples dominate | Medium term (2-4 years) |

| High cost of keto products limits the growth | -0.6% | Global | Medium term (2-4 years) |

| Competition from emerging metabolic diets | -0.4% | Global | Medium term (2-4 years) |

Source: Mordor Intelligence

Health-risk concerns and nutritional deficiencies

Ongoing debates within the medical community regarding the long-term safety of the ketogenic diet continue to limit its widespread adoption, particularly among healthcare providers who significantly influence patient dietary decisions. Concerns over potential cardiovascular risks, such as the suppression of T-regulatory cells and the promotion of cardiac fibrosis due to inhibited mitochondrial function, have reinforced cautious approaches within the industry. This conservative stance is further supported by the European Food Safety Authority's (EFSA) rejection of β-hydroxybutyrate salts as a novel food, citing insufficient safety data, despite their prevalent use in ketogenic supplements. Nutritional adequacy remains a key issue, with challenges related to potential micronutrient deficiencies and maintaining ketosis without compromising balanced nutrition. Healthcare provider skepticism results in limited clinical endorsements, restricting market growth among medically supervised consumer segments.

Strict dietary compliance required

Adherence to the ketogenic diet remains a significant challenge, with approximately two-thirds of individuals unable to sustain ketosis beyond six months. In Asian markets, where carbohydrate-rich staples like rice are deeply ingrained in traditional diets, adopting the ketogenic lifestyle requires substantial lifestyle adjustments. The metabolic transition phase, often accompanied by fatigue and digestive discomfort, contributes to early dropout rates, thereby constraining market growth. To address these compliance issues, companies have introduced ready-to-eat ketogenic products, supported by clinical studies that highlight improved adherence through convenient solutions. However, the necessity for precise macronutrient tracking and strict carbohydrate restrictions continues to act as a major barrier to large-scale market adoption, particularly among time-pressed consumers seeking practical dietary options.

Segment Analysis

By Product Type: Supplements Sustain Leadership, Beverages Accelerate

In 2024, supplements accounted for 45.21% of the ketogenic food products market, reflecting strong consumer demand for MCT oil, ketone salts, and esters, which are essential for simplifying ketosis management. With advancements in formulation science improving flavor and digestibility, the market for ketogenic supplements is experiencing steady growth. The beverage segment is projected to lead the market with a 6.56% CAGR (2025-2030), driven by the increasing popularity of ready-to-drink protein shakes and ketone-rich energy drinks that combine convenience with a sports-nutrition focus.

Snacks are achieving consistent growth by converting traditional products like bars, cheese crisps, and nut mixes into low-net-carb options that cater to busy, on-the-go consumers. Dairy and plant-based alternatives are gaining traction through innovative high-fat, low-lactose formulations designed for lactose-sensitive individuals. Additionally, emerging sub-segments, such as glycerol tri-acetoacetate-based meal replacements, are expanding the range of functional ingredients, signaling continued diversification within the ketogenic food products market.

Note: Segment shares of all individual segments available upon report purchase

By Nature: Organic Premiumization Picks Up Pace

In 2024, conventional products hold a commanding 87.63% market share, highlighting consumer preference for functional benefits over organic certification. In this segment, taste and ketogenic compliance take priority over production methods. The dominance of conventional products is driven by well-established supply chains and cost efficiencies, enabling broader market penetration, an essential factor for a category already positioned at premium price points. On the other hand, organic variants, despite their smaller market base, are experiencing significant growth with an 8.07% CAGR projected through 2030.

The premium pricing of organic products reflects both higher production costs and consumers' willingness to pay for perceived quality benefits. Innovation in organic ketogenic formulations is gaining momentum, particularly in coconut-derived MCT oils, where organic certification aligns with sustainable sourcing practices from key production regions. The regulatory framework supports the growth of organic products through clear certification standards and increased consumer trust in organic labeling.

By Distribution Channel: Digital Transformation Gains Momentum

In 2024, supermarkets and hypermarkets hold a significant 61.87% market share, leveraging their established consumer base and offering value-added services such as in-store demonstrations and nutritional counseling. These channels excel in enabling product trials and comparison shopping, which are critical for categories where taste and texture drive consumer adoption. Conversely, online retail is the fastest-expanding channel, with a 7.33% CAGR projected through 2030. The convenience of subscription-based models and access to specialized products unavailable in traditional retail propels this growth. Digital platforms benefit from direct-to-consumer strategies, allowing brands to educate consumers on ketogenic principles while fostering loyalty through personalized nutrition solutions.

Specialty nutrition stores remain relevant by offering expert consultations and curated product assortments, though geographic constraints and higher operational expenses limit their growth. Pharmacy and drugstore channels capitalize on the medicalization of ketogenic diets, particularly for diabetes management, with healthcare provider endorsements driving consumer traffic. Convenience stores present a growing opportunity, positioned to capture impulse purchases and meet the needs of ketogenic consumers seeking compliant snack options during travel or work.

Geography Analysis

In 2024, North America captured a leading 39.4% share of the ketogenic food products market, driven by strong consumer awareness, clear FDA labeling standards, and a well-established retail distribution network. The adoption of medical-grade product lines continues to grow, supported by clinical use for epilepsy and expanding applications in glucose management. Intense competition drives innovation, exemplified by Nestlé Health Science’s COGNIKET-MCI clinical trial, which focuses on cognitive support through ketogenic formulations.

Asia-Pacific is the fastest-growing region, recording a 7.59% CAGR, fueled by increasing diabetes prevalence and rising disposable incomes. According to the International Diabetes Federation, China’s adult diabetes prevalence reached 11.9% in 2024 [3]Source: International Diabetes Federation, "Members-China,"idf.org. Regulatory advancements across ASEAN markets are streamlining nutraceutical pathways, boosting the adoption of functional keto SKUs. Strategic partnerships, such as the Nestlé India-Dr. Reddy’s joint ventures are accelerating the development of localized formulations tailored to regional preferences and regulatory requirements.

Europe remains a significant but mature market, shaped by stringent Novel Food regulations. In February 2025, EFSA introduced updated guidance aimed at reducing review timelines while maintaining safety standards, encouraging the development of next-generation ketone ingredients. The demand for sustainability and clean-label products aligns well with premium keto claims. However, Europe’s diverse culinary traditions necessitate country-specific marketing strategies to achieve success in the ketogenic food products market.

Competitive Landscape

The global ketogenic diet market is fragmented and comprises regional and international competitors. The market is dominated by players like Nestle SA, Perfect Keto LLC, General Mills Inc., Glanbia Plc, and Now Foods. These players focus on leveraging the opportunities posed by emerging markets to expand their product portfolios to cater to the requirements of various product segments, especially supplements and beverages. Also, companies have turned to strategic partnerships as their main way to expand their customer base and geographic reach.

Leading companies are implementing vertical integration strategies to enhance quality control and cost efficiency. Meanwhile, smaller firms are prioritizing innovation and direct-to-consumer models to mitigate the distribution advantages held by larger competitors. The market is increasingly moving toward consolidation. For example, in March 2025, Herbalife acquired Pruvit Ventures Inc. in a strategic move to integrate specialized ketogenic expertise and patented supplement formulations into its expansive distribution network.

Technology adoption is becoming a critical competitive factor. Businesses are investing in personalized nutrition platforms and digital health solutions to strengthen consumer engagement and loyalty. In June 2024, Nestlé Health Science launched its GLP-1 nutrition support platform, illustrating how established players are leveraging digital tools to address targeted consumer needs while fostering ecosystem dependency. Additionally, advancements in ingredient sourcing and processing are driving competitive advantages. However, the regulatory complexities associated with novel food approvals create significant barriers to entry, favoring companies with robust regulatory expertise and financial resources. For instance, EFSA recently rejected β-hydroxybutyrate salts due to insufficient data quality, highlighting the challenges in navigating regulatory requirements.

Ketogenic Diet Industry Leaders

-

Perfect Keto, LLC

-

Nestlé S.A.

-

Glanbia PLC

-

General Mills Inc

-

Now Foods

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Nature's Own launched its Keto Life Multigrain Sliced Bread, featuring just 1 Net Carb per slice. The bread offers a luxuriously soft, pillowy texture, enriched with wholesome grains, making it perfect for any meal.

- May 2025: GNC India unveiled its latest offering, GNC Pro Performance 100% Whey + Keto Surge, a groundbreaking protein supplement. This innovative product merges premium whey protein with potent fat-burning components, aiming to aid users in their weight loss journey while promoting lean muscle development.

- April 2025: HeyLO launched keto-friendly Brownie Bars, is available in Choco, Ginger, and Orange flavors. These bars are high in fiber, low in sugar, vegan, and gluten-free, enabling consumers to satisfy their sweet cravings while adhering to their low-carb dietary goals.

- April 2024: Nestlé India entered into a joint venture with Dr. Reddy's Laboratories to expand their nutraceutical portfolio within the metabolic health segment. This partnership leverages Nestlé's expertise in nutrition and Dr. Reddy's commercial capabilities to address opportunities in the rapidly growing Indian market.

Global Ketogenic Diet Market Report Scope

Keto is short for ketogenic, referring to a diet or food that is low in carbohydrates but high in protein. While originating as a medical diet, it is popularly associated with weight loss. It also helps in boosting metabolism, reducing appetite, and improving the balance of the gut. The report on ketogenic diet food is segmented by product type into supplements, beverages, snacks, and other product types. By distribution channel, the market is segmented into supermarkets, hypermarkets, pharmacies, drug stores, specialty stores, online retail stores, and other distribution channels. By geography, the market is segmented into North America, Europe, Asia-Pacific, South America, and the Middle East and Africa. For each segment, the market sizing and forecasts have been done on the basis of value (in USD million).

| By Product Type | Supplements | Ketone Salts | |

| Ketone Esters | |||

| MCT Oil | |||

| Others | |||

| Snacks | Bars | ||

| Nuts and Seed Mixes | |||

| Cookies and Brownies | |||

| Meat and Cheese Snacks | |||

| Beverages | Ready-To-Drinks | ||

| Shakes | |||

| Coffee and Creamers | |||

| Dairy and Dairy Alternatives | |||

| Others | |||

| By Distribution Channel | Supermarkets/Hypermarkets | ||

| Specialty Nutrition Stores | |||

| Pharmacy/Drug Stores | |||

| Convenience Stores | |||

| Online Retail Stores | |||

| Others | |||

| By Nature | Conventional | ||

| Organic | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Rest of North America | |||

| Europe | United Kingdom | ||

| Germany | |||

| France | |||

| Italy | |||

| Spain | |||

| Netherlands | |||

| Poland | |||

| Belgium | |||

| Sweden | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| Australia | |||

| Indonesia | |||

| South Korea | |||

| Thailand | |||

| Singapore | |||

| Rest of Asia-Pacific | |||

| South America | Brazil | ||

| Argentina | |||

| Colombia | |||

| Chile | |||

| Peru | |||

| Rest of South America | |||

| Middle East and Africa | South Africa | ||

| Saudi Arabia | |||

| United Arab Emirates | |||

| Nigeria | |||

| Egypt | |||

| Morocco | |||

| Turkey | |||

| Rest of Middle East and Africa | |||

| Supplements | Ketone Salts |

| Ketone Esters | |

| MCT Oil | |

| Others | |

| Snacks | Bars |

| Nuts and Seed Mixes | |

| Cookies and Brownies | |

| Meat and Cheese Snacks | |

| Beverages | Ready-To-Drinks |

| Shakes | |

| Coffee and Creamers | |

| Dairy and Dairy Alternatives | |

| Others |

| Supermarkets/Hypermarkets |

| Specialty Nutrition Stores |

| Pharmacy/Drug Stores |

| Convenience Stores |

| Online Retail Stores |

| Others |

| Conventional |

| Organic |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Italy | |

| Spain | |

| Netherlands | |

| Poland | |

| Belgium | |

| Sweden | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| Indonesia | |

| South Korea | |

| Thailand | |

| Singapore | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Chile | |

| Peru | |

| Rest of South America | |

| Middle East and Africa | South Africa |

| Saudi Arabia | |

| United Arab Emirates | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

Key Questions Answered in the Report

What is the current value of the ketogenic food products market?

The market is worth USD 12.8 billion in 2025 and is projected to grow to USD 16.5 billion by 2030 at a 5.16% CAGR.

Which product segment holds the largest share?

Supplements lead with 45.2% of the ketogenic food products market share in 2024, driven by demand for convenient ketone and MCT formulations.

Why is Asia-Pacific the fastest-growing region?

Asia-Pacific combines rising disposable incomes, accelerating e-commerce, and a sharp increase in diabetes incidence, producing a 7.59% forecast CAGR for the region.

How will new FDA “healthy” rules affect keto products?

The updated criteria allow high-fat, nutrient-dense foods like nuts and avocados to claim “healthy,” boosting mainstream acceptance of many ketogenic formulations.

Page last updated on: July 5, 2025