Industrial Packaging Market Size

| Study Period | 2019 - 2029 |

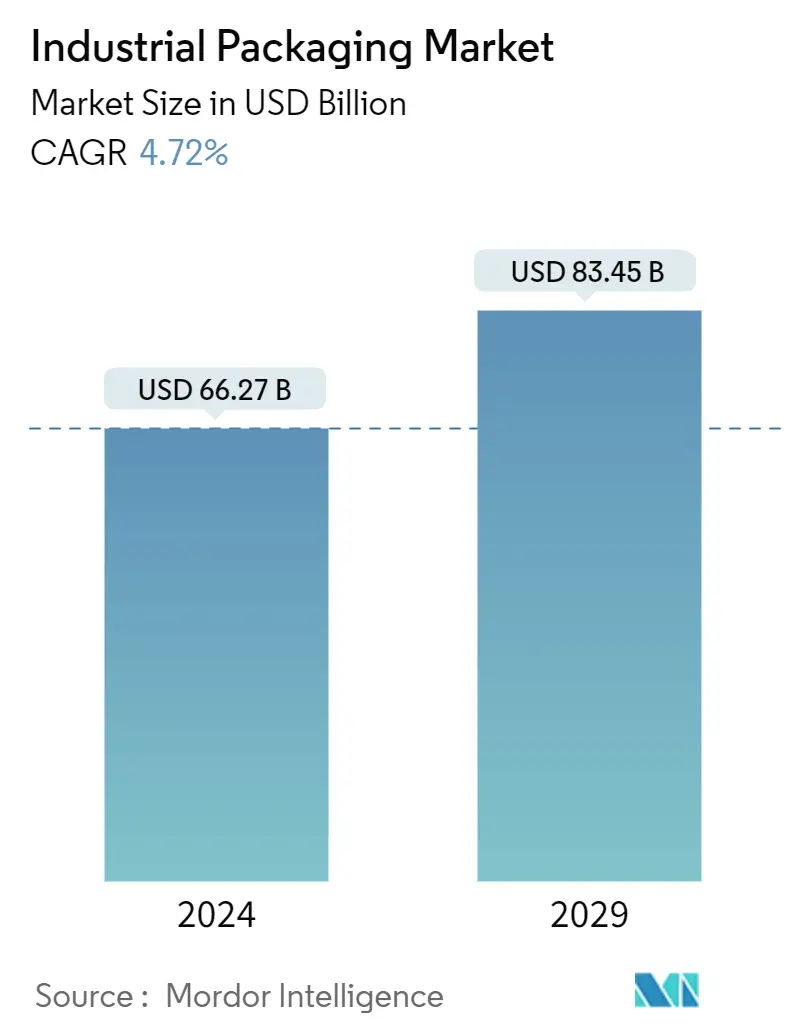

| Market Size (2024) | USD 66.27 Billion |

| Market Size (2029) | USD 83.45 Billion |

| CAGR (2024 - 2029) | 4.72 % |

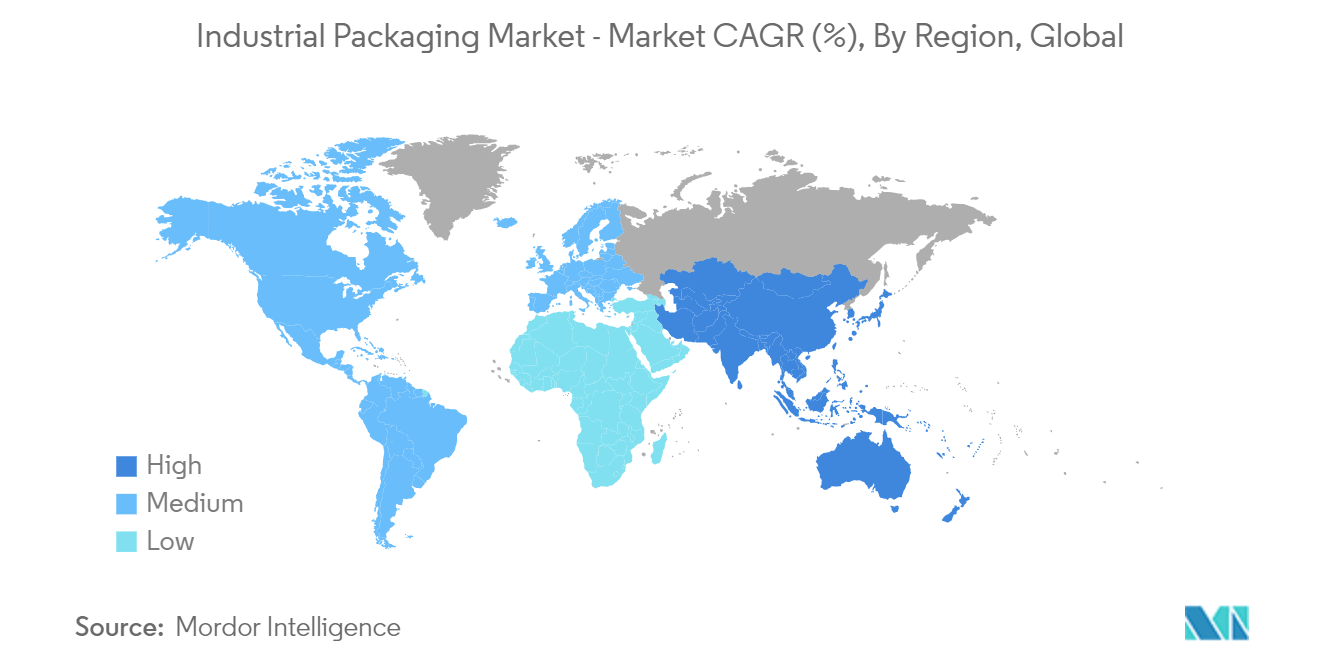

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Asia-Pacific |

Major Players

*Disclaimer: Major Players sorted in no particular order |

Need a report that reflects how COVID-19 has impacted this market and its growth?

Industrial Packaging Market Analysis

The Industrial Packaging Market size is estimated at USD 66.27 billion in 2024, and is expected to reach USD 83.45 billion by 2029, growing at a CAGR of 4.72% during the forecast period (2024-2029).

- The increasing volume of resources and products being transported across various regions is one of the primary factors that led to the growth of bulk industrial packaging. The industrial packaging market highly depends on global import and export activities. While products such as drums and pails experience huge demand from heavy manufacturing industries, other products, such as material handling containers and intermediate bulk containers (IBCs), include applications in logistics and the short-distance transportation of goods.

- Rigid plastic IBCs are used in food and beverage, pharmaceuticals, chemicals, paints, inks, and lubricants. North America's Rigid Intermediate Bulk Container Association (RIBCA) fosters the interests of persons, firms, and corporations that manufacture or assemble rigid intermediate bulk containers.

- During a customer event in Heidelberg, Germany, Mauser, an industrial packaging company, recently presented its new skINliner barrier technology. The Mauser skINliner barrier technology combines the advanced barrier performance of multilayer plastic film technology (e.g., against hydrocarbons and/or oxygen) with the logistical and lifecycle benefits of rigid packaging. The new modular packaging design promotes reuse and recyclability.

- Companies are launching new and innovative products in line with the changing demand for sustainable and recyclable industrial packaging. For instance, in May 2022, Berry Global's UK refuse sack business launched a new range of high-strength refuse sacks made from recycled plastics.

- The increase in the utilization of shipping containers drives the market. Thus, companies are collaborating to offer new and innovative products according to the customers' requirements. In April 2022, Novvia Group acquired Southern Container LLC, a fiber, plastic, glass, and metal packaging product distributor. Through this acquisition, Novvia strengthened its Inmark business and its market position.

- Over the last few years, awareness of the harmful effects of plastic usage significantly increased. Many public campaigns and initiatives are taken by governmental authorities, associations, and NGOs to spread this awareness. Thus, plastic packaging consumption significantly declined in the last few years.

- With the increasing demand for food and beverages, the agriculture industry faced many challenges. Supply chain challenges in materials, such as fertilizers, equipment, and transportation of crops, were only one of them. For instance, the global fertilizer market continued to witness challenges to logistical and other economic impacts of COVID-19. However, these impacts are highly uneven across markets, and not all are negative.

Industrial Packaging Market Trends

Food and Beverages Expected to Drive the Market

- The most used industrial packaging for food and beverage industries are drums, IBCs, corrugated boxes, pallets, and sacks. However, the packaging needs to be certified as food-grade. For instance, IBC totes (designed with stainless steel tanks or poly-caged totes) are certified by the DOT/UN and ensure that the packaging does contaminate the food products.

- Drums are widely used in the alcohol industry. Beer is the most-transported alcohol globally. Drums are made of steel, plastics, or fiber. However, steel drums are regarded as the safest by the US Department of Transportation. It is expected to drive further storing and transporting beverages in steel drums.

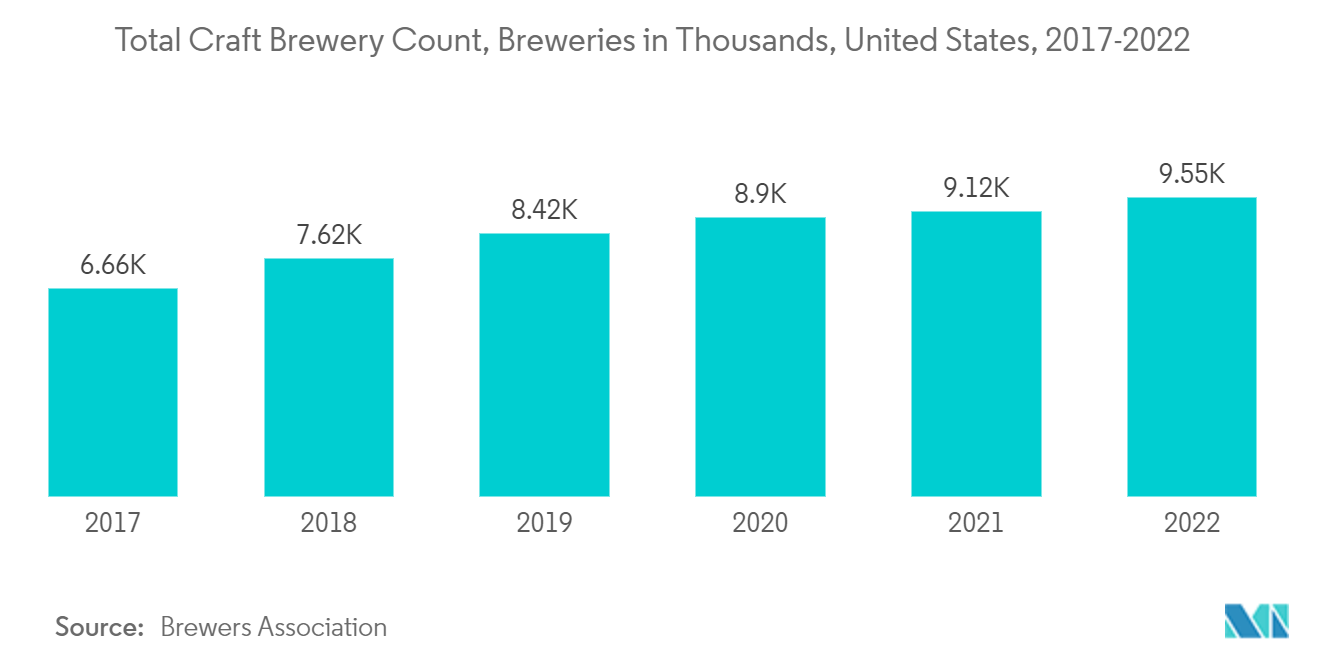

- The rising production volume of craft beer is expected to increase the demand for steel drums in the market. According to the Brewers Association, the share of craft beer in the total production volume of beer in the United States in 2022 was 13.2%, at par with 13.1% in 2021. It is expected to drive the demand for steel drums.

- This rapid wave of popular interest drove the surge in ecological packaging options. According to Food Dive, 67% of customers globally believe it is critical that the items they buy come in recyclable packaging, with 54% indicating it is a factor they consider when purchasing. These sentiments aren't going away, with a whopping 83% of younger buyers prepared to spend more for products that are packed sustainably.

- Corrugated packaging is mainly used for packaging processed foods, fresh food, produce, and beverages. For many food goods, corrugated packaging is becoming a viable alternative to plastic packaging. Paper packaging, for example, may be created more simply from recycled materials and recycled or composted. According to the most recent Brewers Association figures, there were 9,552 craft brewers in the United States in 2022, up from 6,661 in 2017.

Asia-Pacific Expected to Hold a Significant Market Share

- Over the last few decades, the industrial sector in China, one of the major market shareholders in the Asia-Pacific, witnessed astonishing growth. The sector's growth placed the country among the leading manufacturers and exporters of various goods. According to the National Bureau of Statistics of China, in 2022, the industrial sector contributed 39.9% of the country's GDP.

- Moreover, the adoption of industrial drums in the packaging industry is increasing. The packaging manufacturer is focusing on recycling, downgauging, optimizing pack size, and safety. Industrial drums offer many corporations and companies these features to effectively maintain sustainability initiatives. According to the Industrial Steel Drum Institute (ISDI), steel drums provide safe transport for approximately 50 million metric tons of material worldwide annually.

- Considering the growing demand, several vendors operating in the market are focusing on offering a broad portfolio of industrial packaging products. For instance, Plastene offers a variety of transport and storage containers (Jumbo bags/FIBCs) for both dry and liquid (bulk) goods. Jumbo bags increasingly substitute plastic, paper, and cardboard packaging solutions for industrial customers.

- The rest of Asia-Pacific comprises South Korea, Singapore, and Hong Kong. South Korea's largest industries are electronics, automobiles, telecommunications, shipbuilding, chemicals, and steel. South Korea's 5 biggest export products by value in 2022 were electronic integrated circuits, cars, refined petroleum oils, phone devices, smartphones, and automobile parts or accessories. Those major exports accounted for well over a third (38.8%) of South Korea's overall exports (source: International Trade Center). It majorly catered to the demand for industrial packaging.

- Increasing focus on achieving cost-effectiveness in logistics and growing transportation of hazardous and non-hazardous materials brought steel drums and IBCs to the center stage. Imported chemicals are essential in producing some of Korea's top exports. Korea's chemistry industry is rapidly developing, and the country is ranked on the world's 5th production scale. Still, the demands for high-quality, sophisticated chemical products and associated substances production present a lucrative opportunity for United States chemical manufacturers. It led to major demand for industrial packaging, such as drums, to export chemicals.

Industrial Packaging Industry Overview

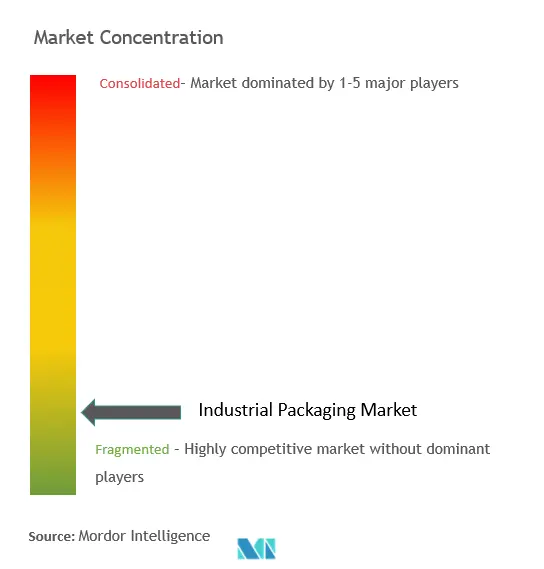

The Industrial Packaging market remains highly fragmented, with numerous international, regional, and local vendors. Local manufacturers of industrial packaging products cater to unique, innovative solutions at a lower price than international vendors, resulting in an intense price battle.

- January 2024 - Greif, Inc., one of the global leaders in industrial packaging products and services, and IonKraft, a barrier technology company specializing in plasma-based coatings, announced a new pilot-project partnership. The collaboration focuses on revolutionizing the challenges of recyclability and sustainability in plastic jerrycan packaging that requires an additional barrier solution.

Industrial Packaging Market Leaders

WERIT Kunststoffwerke W. Schneider GmbH & Co.

Mondi Plc

Greif Inc.

Mauser Packaging Solutions

Global-Pak Inc.

*Disclaimer: Major Players sorted in no particular order

Industrial Packaging Market News

- November 2023 - POWERS, one of the leaders in manufacturing productivity consulting, announced a partnership with a prominent player in the industrial custom packaging sector. This collaboration would revolutionize the client’s management operating system and introduce an innovative frontline leadership development program. The client, a heavyweight in customized industrial packaging, is recognized for its diverse offerings, including wood, steel, corrugated, and hybrid products.

Industrial Packaging Market Report - Table of Contents

1. INTRODUCTION

1.1 Study Assumptions and Market Definition

1.2 Scope of the Study

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET INSIGHTS

4.1 Market Overview

4.2 Industry Value Chain Analysis

4.3 Industry Attractiveness - Porter's Five Forces Analysis

4.3.1 Bargaining Power of Suppliers

4.3.2 Bargaining Power of Buyers

4.3.3 Threat of New Entrants

4.3.4 Threat of Substitute Products

4.3.5 Intensity of Competitive Rivalry

4.4 Impact of COVID-19 on the Market

5. MARKET DYNAMICS

5.1 Market Drivers

5.1.1 Emergence of Sustainable and Recyclable Packaging Materials

5.1.2 Increasing Utilization of the Shipping Containers

5.2 Market Restraints

5.2.1 Dynamic Changes in Regulatory Standards Due to Increasing Environmental Concerns

6. MARKET SEGMENTATION

6.1 By Product

6.1.1 Intermediate Bulk Containers (IBCs)

6.1.2 Sacks

6.1.3 Drums

6.1.4 Pails

6.1.5 Other Products

6.2 By End-user Industry

6.2.1 Automotive

6.2.2 Food and Beverage

6.2.3 Chemicals and Pharmaceuticals

6.2.4 Oil and Gas and Petrochemicals

6.2.5 Building and Construction

6.2.6 Other End-user Industries

6.3 By Geography

6.3.1 North America

6.3.1.1 United States

6.3.1.2 Canada

6.3.2 Europe

6.3.2.1 Germany

6.3.2.2 United Kingdom

6.3.2.3 France

6.3.2.4 Russia

6.3.2.5 Rest of Europe

6.3.3 Asia-Pacific

6.3.3.1 China

6.3.3.2 Japan

6.3.3.3 India

6.3.3.4 Rest of Asia-Pacific

6.3.4 Rest of the World

7. COMPETITIVE LANDSCAPE

7.1 Company Profiles*

7.1.1 WERIT Kunststoffwerke W. Schneider GmbH & Co.

7.1.2 Mondi PLC

7.1.3 Greif Inc.

7.1.4 Mauser Packaging Solutions

7.1.5 Global-Pak, Inc.

7.1.6 Berry Global Inc.

7.1.7 Smurfit Kappa Group PLC

7.1.8 Tank Holding Corp.

7.1.9 International Paper Company

7.1.10 Veritiv Corporation

7.1.11 Nefab Group

7.1.12 SCHÜTZ GmbH & Co. KGaA

7.1.13 DS Smith PLC

7.1.14 Amcor PLC

7.1.15 Packaging Corporation of America

7.1.16 Pact Group Holdings Ltd

7.1.17 Visy

7.1.18 Brambles Ltd (CHEP)

7.1.19 Snyder Industries LLC

7.1.20 Myers Containers

8. INVESTMENT ANALYSIS

9. MARKET OPPORTUNITIES AND FUTURE TRENDS

Industrial Packaging Industry Segmentation

Industrial packaging protects, ships, and stores a wide range of goods. Typically, industrial packaging is done at the production site right after production, although it can be used at any point in the supply chain. This type of packaging is usually done for sensitive products that heavily rely on stability or are hazardous or bulky or for products with components that are sensitive to each other.

The industrial packaging market is segmented by product (intermediate bulk containers (IBCs), sacks, drums, pails, and other Products), end-user industries (automotive, food and beverage, chemicals and pharmaceuticals, oil, gas, and petrochemical, building and construction, and other end-user industries), and geography (North America (United States, Canada), Europe (Germany, United Kingdom, France, Russia, and rest of Europe), Asia-Pacific (China, Japan, India, and rest of Asia-Pacific, rest of Asia-Pacific), and Rest of the World). The market sizes and forecasts are provided in value in (USD) for all the segments mentioned above.

| By Product | |

| Intermediate Bulk Containers (IBCs) | |

| Sacks | |

| Drums | |

| Pails | |

| Other Products |

| By End-user Industry | |

| Automotive | |

| Food and Beverage | |

| Chemicals and Pharmaceuticals | |

| Oil and Gas and Petrochemicals | |

| Building and Construction | |

| Other End-user Industries |

| By Geography | |||||||

| |||||||

| |||||||

| |||||||

| Rest of the World |

Industrial Packaging Market Research FAQs

How big is the Industrial Packaging Market?

The Industrial Packaging Market size is expected to reach USD 66.27 billion in 2024 and grow at a CAGR of 4.72% to reach USD 83.45 billion by 2029.

What is the current Industrial Packaging Market size?

In 2024, the Industrial Packaging Market size is expected to reach USD 66.27 billion.

Who are the key players in Industrial Packaging Market?

WERIT Kunststoffwerke W. Schneider GmbH & Co., Mondi Plc, Greif Inc., Mauser Packaging Solutions and Global-Pak Inc. are the major companies operating in the Industrial Packaging Market.

Which is the fastest growing region in Industrial Packaging Market?

Asia-Pacific is estimated to grow at the highest CAGR over the forecast period (2024-2029).

Which region has the biggest share in Industrial Packaging Market?

In 2024, the Asia-Pacific accounts for the largest market share in Industrial Packaging Market.

What years does this Industrial Packaging Market cover, and what was the market size in 2023?

In 2023, the Industrial Packaging Market size was estimated at USD 63.14 billion. The report covers the Industrial Packaging Market historical market size for years: 2019, 2020, 2021, 2022 and 2023. The report also forecasts the Industrial Packaging Market size for years: 2024, 2025, 2026, 2027, 2028 and 2029.

Industrial Packaging Industry Report

Statistics for the 2024 Industrial Packaging market share, size and revenue growth rate, created by Mordor Intelligence™ Industry Reports. Industrial Packaging analysis includes a market forecast outlook to 2029 and historical overview. Get a sample of this industry analysis as a free report PDF download.