Market Overview

| Study Period | 2019 - 2030 |

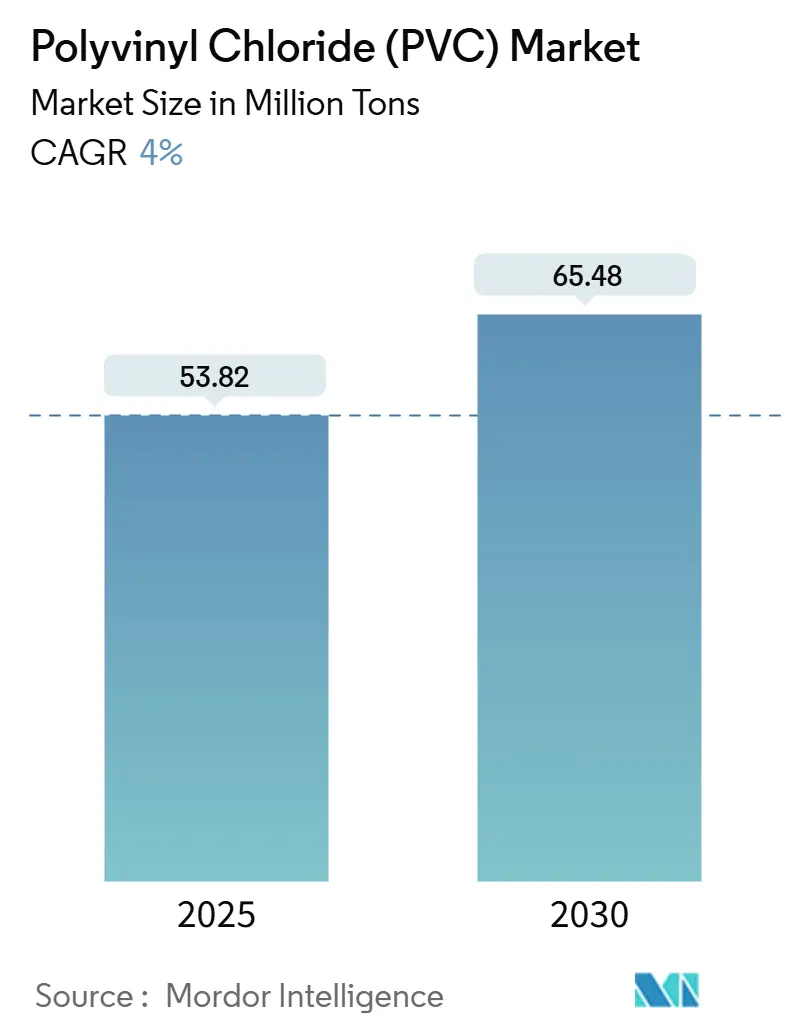

| Market Volume (2025) | 53.82 Million tons |

| Market Volume (2030) | 65.48 Million tons |

| Growth Rate (2025 - 2030) | 4.00% CAGR |

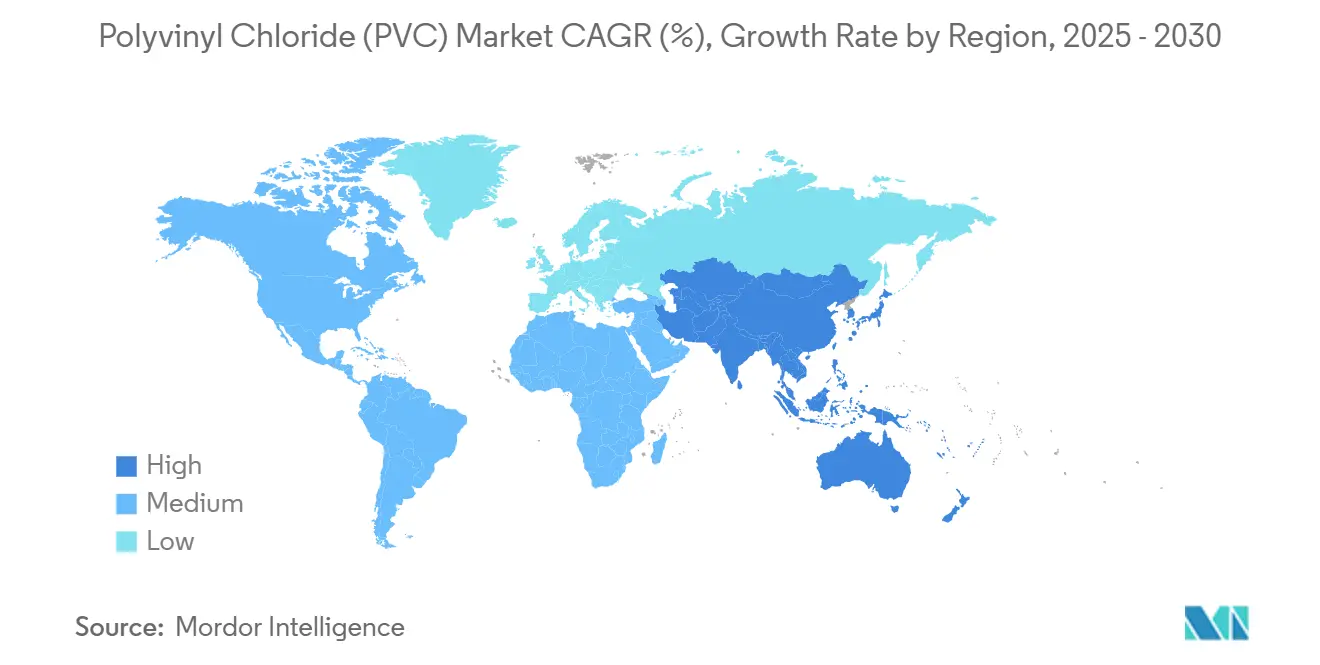

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Polyvinyl Chloride (PVC) Market Analysis by Mordor Intelligence

The Polyvinyl Chloride Market size is estimated at 53.82 Million tons in 2025, and is expected to reach 65.48 Million tons by 2030, at a CAGR of 4% during the forecast period (2025-2030). This expansion reflects PVC’s entrenched role in water infrastructure, healthcare disposables, and new-generation electric vehicles, even as regulations tighten around traditional additives. Sustained demand arises from a favorable performance-to-price ratio, especially in fast-urbanizing regions where substitutes cannot yet match PVC’s durability, chemical resistance, or ease of processing. Large-diameter pipes for stormwater and potable-water grids, phthalate-free medical tubing, and lightweight automotive interiors all reinforce the growth trajectory of the polyvinyl chloride market. Meanwhile, producer margins face mixed pressures: Chinese overcapacity weighs on global prices, but vertical integration into chlor-alkali and recycling operations helps offset feedstock and compliance costs for leading firms.

Key Report Takeaways

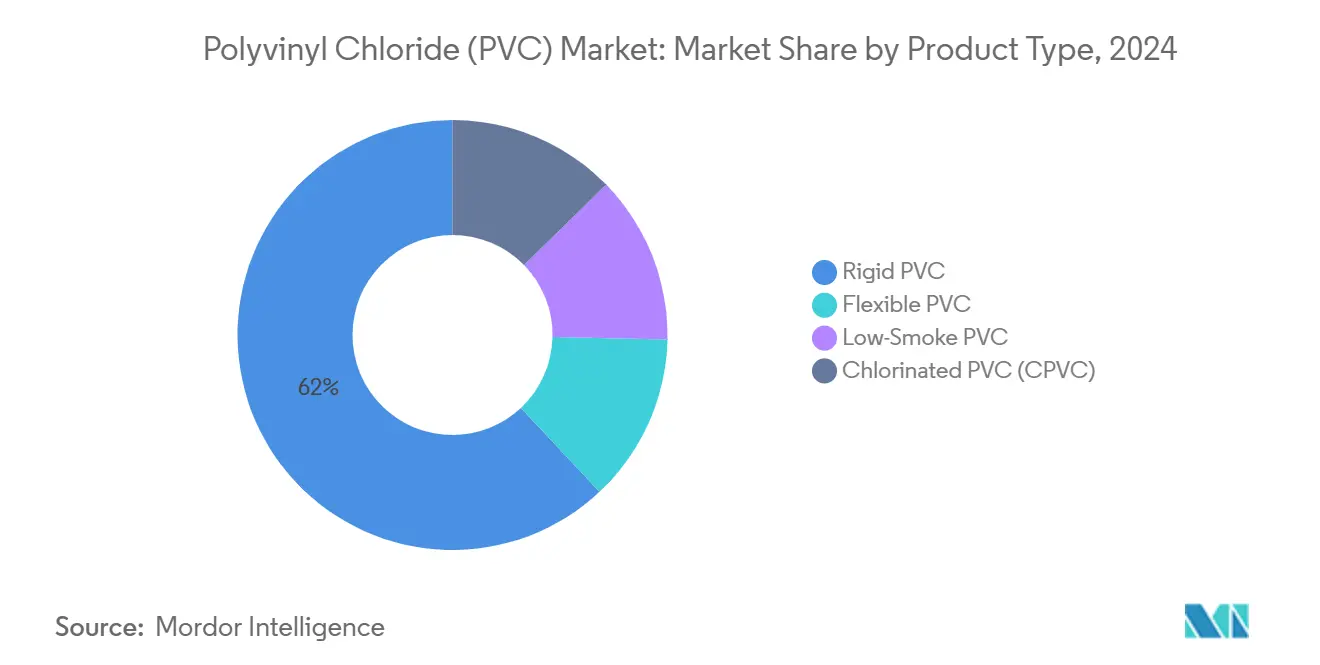

- By product type, rigid PVC commanded 62% of the polyvinyl chloride market share in 2024, while chlorinated PVC registered the fastest 4.80% CAGR outlook to 2030.

- By manufacturing process, suspension PVC contributed 75% of 2024 revenue, whereas emulsion PVC is poised for a 4.61% CAGR through 2030.

- By stabilizer type, calcium-based systems captured 48% of the polyvinyl chloride market size in 2024, with organotin stabilizers expanding at 5.31% CAGR to 2030.

- By application, pipes and fittings held 50% of the polyvinyl chloride market size in 2024 and are projected to grow at 4.40% CAGR through 2030.

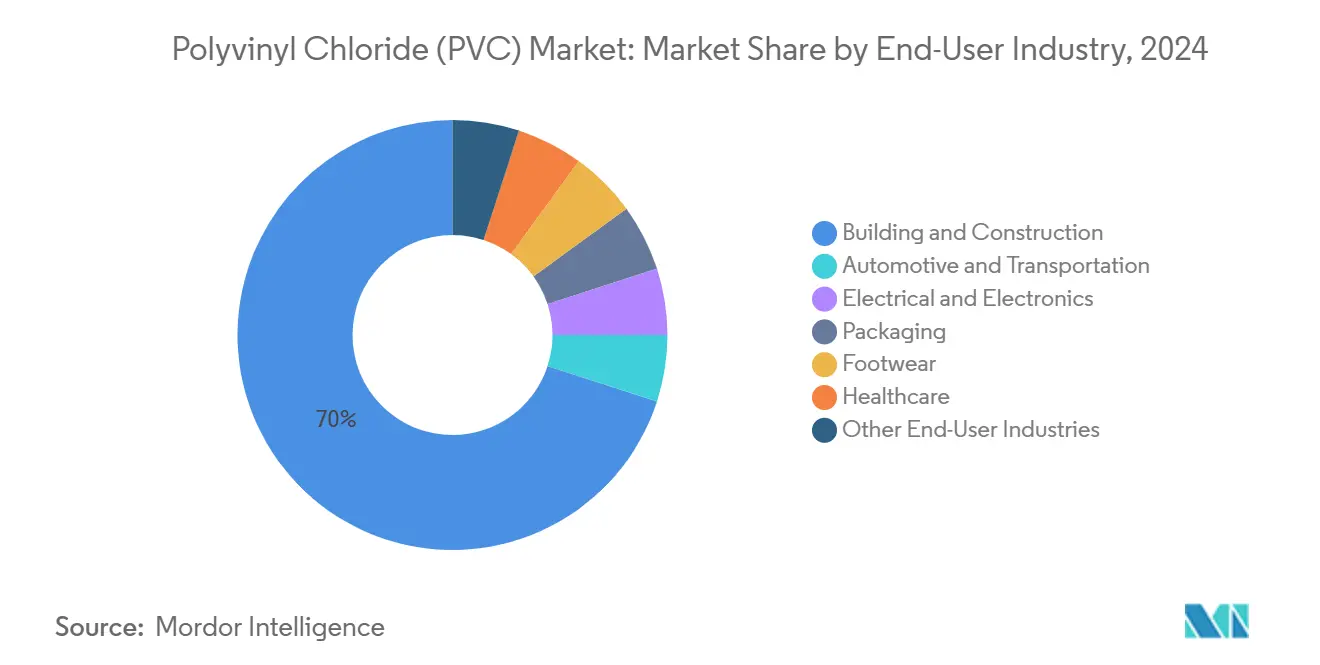

- By end-user industry, building and construction led with 70% revenue share in 2024, and is projected to accelerate at 4.16% CAGR to 2030.

- By region, Asia-Pacific accounted for 60% of 2024 consumption and is forecast to pace the polyvinyl chloride market with a 4.38% CAGR to 2030.

Global Polyvinyl Chloride (PVC) Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid Urban Infrastructure Expansion in SPAC-Driven Megacities across Asia | +1.20% | Asia-Pacific core, spill-over to MEA | Long term (≥ 4 years) |

| Surge in Single-Use Medical Devices Favoring DEHP-Free PVC Compounds in North America and Europe | +0.80% | North America & EU | Medium term (2-4 years) |

| Rising Demand for Clean Water Infrastructure | +0.90% | Global | Long term (≥ 4 years) |

| OEM Shift Toward Lightweight Flexible PVC Interiors in Electric Vehicles Produced | +0.60% | Global, with early gains in China, Germany, United States | Medium term (2-4 years) |

| Chlor-Alkali Capacity Integration by Producers in the US and EU Lowering PVC Production Costs | +0.70% | North America & EU, competitive impact globally | Short term (≤ 2 years) |

Source: Mordor Intelligence

Rapid Urban Infrastructure Expansion in SPAC-Financed Megacities

Continued spending on flood management and potable-water grids in Asia’s megacities drives specification of large-diameter PVC pipes exceeding 2m, a departure from legacy residential bore sizes. Projects in India and Indonesia illustrate how acoustic leak-detection technology embedded in PVC piping allows utilities to address non-revenue water losses while extending asset life. Governments also link climate-resilience funding to materials with long service lives, which favors PVC over ductile iron or concrete. As a result, premium grades capable of handling higher pressures and aggressive soil conditions obtain stronger margins than commodity pipe. Similar infrastructure commitments across Gulf Cooperation Council states suggest spill-over demand into the Middle East over the next decade.

Surge in Single-Use Medical Devices Favoring DEHP-Free PVC Compounds

California’s impending DEHP ban in 2030 prompted North American converters to adopt DOTP-plasticized PVC as the default choice for blood bags, IV sets, and peritoneal-dialysis tubing[1]AABB, “California Assembly Bill on DEHP in Medical Devices,” aabb.org . Teknor Apex, for instance, commercialized low-extractable APEX medical compounds that match flexibility targets without reproductive-toxicity concerns. Simultaneously, EU postponement of its own DEHP prohibition until mid-2030 offers first-mover advantage to suppliers that have already re-qualified with phthalate-free formulations. Higher compliance costs are readily absorbed by hospital procurement budgets, rounding out a premium niche that shields specialty PVC grades from commodity cycles.

Rising Demand for Clean-Water Infrastructure

Upgrades to aging water mains in the United States, Germany, and Japan emphasize corrosion-resistant PVC as maintenance budgets tighten. CPVC’s ability to withstand 90 °C service temperatures has positioned it as the material of choice for hot-water reticulation in commercial buildings, reducing life-cycle costs relative to copper. Smart-grid ambitions encourage utilities to specify sensor-ready PVC pipes that transmit leak, pressure, and water-quality analytics, thus elevating manufacturers from raw-materials suppliers to solution partners. ESG-driven municipalities further favor pipes with certified recycled content, nudging PVC producers toward post-consumer resin investments.

OEM Shift Toward Lightweight Flexible PVC Interiors in Electric Vehicles

Global automakers increasingly rely on flexible PVC compounds that integrate ambient back-lighting, molded graining, and scratch-resistant coatings. Continental’s Acella next-generation trim foils deliver up to 20% weight savings versus traditional synthetics, contributing directly to extended EV driving range. Tier-1 suppliers also highlight PVC’s low VOC profile after phthalate-free transition, addressing interior air-quality regulations. Integrating post-industrial recycled PVC into non-visible parts, such as under-floor coverings, helps car manufacturers hit circular-economy targets without compromising performance.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Accelerating Bans on Lead-Based Stabilizers under EU REACH and Indian BIS Standards | -0.70% | Europe & India, expanding to other regions | Short term (≤ 2 years) |

| Brand-Owner Push for Phthalate-Free Packaging Diminishing Conventional Flexible PVC Demand | -0.50% | Global, with concentration in North America & EU | Medium term (2-4 years) |

| Ethylene Price Volatility Linked to Crude-Oil Fluctuations Compressing Margins | -0.40% | Global | Short term (≤ 2 years) |

Source: Mordor Intelligence

Accelerating Bans on Lead-Based Stabilizers under EU REACH and Indian BIS

EU Regulation 923/2023 limits total lead content in PVC articles to 0.1 wt% starting January 2026[2]European Chemicals Agency, “Regulation (EU) 2023/923 on Lead in PVC,” echa.europa.eu . The same threshold is being replicated by India’s Bureau of Indian Standards. Re-formulation to calcium-zinc stabilizers, while environmentally favorable, reduces processing windows and can lower dielectric strength—posing particular issues for wire and cable grades. Companies with patented synergistic additive packages secure a pricing premium, yet smaller extruders lacking R&D scale face qualification delays. Cost pass-through remains challenging in price-sensitive markets, compressing margins and encouraging consolidation.

Brand-Owner Push for Phthalate-Free Packaging Diminishing Conventional Flexible PVC Demand

Multinational FMCG firms now specify phthalate-free compounds for blister packs and shrink films ahead of regulatory mandates. Perstorp’s bio-based Pevalen Pro 100 addresses both toxicological and carbon-footprint requirements but carries a price uplift of 35% versus DEHP. High-volume, low-margin packaging converters consequently weigh polymer substitution for cost-critical SKUs, pressuring demand for flexible PVC in North America and the EU. Growth persists in applications where clarity, heat-seal integrity, or puncture resistance override cost considerations, yet overall restraint on flexible volumes is visible through 2027 contracts.

Segment Analysis

By Product Type: Special-Purpose Grades Gain Momentum

Rigid PVC accounted for 62% of polyvinyl chloride market share in 2024, anchored by construction profiles, window frames, and infrastructure pipe. Volume leadership rests on standardized tooling, wide raw-material availability, and cost-efficient mass production. However, CPVC—while representing a single-digit share—shows the strongest 4.80% CAGR to 2030 thanks to superior temperature tolerance for hot-and-cold potable systems in hotels, hospitals, and data centers[3]Plastic Pipe and Fittings Association, “CPVC Growth in Potable Water Systems,” ppfahome.org . CPVC’s performance premium permits double-digit price differentials that cushion producers from commodity swings in the polyvinyl chloride market. Flexible PVC continues to serve medical bags, vehicle interiors, and consumer hoses; advances in DOTP and citrate plasticizers resolve regulatory scrutiny, retaining these applications. Low-smoke zero-halogen PVC variants further unlock growth in metro-rail and public-venue cabling where fire-safety codes tighten.

A notable spill-over effect involves CPVC blends that deliver incremental heat resistance in pipe-in-pipe installations without the full cost of neat CPVC. Producers exploit these hybrids to extend product portfolios and capture projects beyond standard temperature thresholds. Meanwhile, rigid PVC suppliers counter CPVC’s rise by marketing co-extruded pipes with foam cores or impact-modified skins that reduce weight and resin consumption. These innovations collectively sustain competition across the polyvinyl chloride market even as specialized niches attract premium pricing.

Note: Segment shares of all individual segments available upon report purchase

By Manufacturing Process: Suspension Dominance Meets Emulsion Upside

Suspension polymerization delivered 75% of 2024 volume, reflecting unmatched economies of scale and broad compatibility with additives. Most construction-grade resins stem from suspension lines exceeding 300 kt/yr, enabling cost leadership across the polyvinyl chloride market. Yet emulsion PVC, while holding a modest base, is forecast for a 4.61% CAGR driven by its fine-particle morphology which supports high-definition calendared films and medical-grade tubing. Emulsion plants are inherently smaller and more flexible, allowing rapid grade switches toward higher-margin niches such as transparent blood-collection film or synthetic leather for EV interiors.

Suppliers use process versatility as a differentiation lever. Integrated producers operate both suspension and emulsion assets, bundling supply contracts and technical services to lock in converters shifting between commodity and specialty applications. Bulk polymerization, although limited, serves ultra-high-purity segments like semiconductor clean-room paneling where extractables must be minimized. As regulatory and end-user demands become more exacting, process diversification protects revenue streams and tempers price volatility in the polyvinyl chloride market.

By Stabilizer Type: Regulatory Compliance Re-Shuffles Value Pools

Calcium-zinc systems captured 48% of 2024 demand after successive REACH updates curtailed lead, barium, and cadmium usage. Early adopters report smoother global export approvals and brand-owner endorsements, granting share gains within the polyvinyl chloride industry. Organotin stabilizers, though expensive, grow at 5.31% CAGR in high-heat, potable-water, and rigid-film applications where superior clarity or thermal stability justifies the premium. Lead-based variants retreat fastest in Europe and India, yet retain pockets of demand in Africa where enforcement is nascent.

Stabilizer suppliers offset higher raw-material costs through proprietary synergists that cut dosage rates by up to 20%. Knowledge-intensive formulating further raises entry barriers, concentrating market power among a handful of multinational additive firms. PVC resin producers increasingly form joint ventures or strategic sourcing pacts to secure compliant stabilizer supply and shield themselves from future regulatory shocks.

By Application: Pipe Dominance Under Soft Diversification

Pipe and fitting products generated 50% of the polyvinyl chloride market size in 2024, underpinned by water-supply investments and municipal stormwater upgrades. The segment is projected to grow at 4.40% CAGR as smart-leak detection and trenchless installation methods favor lightweight, corrosion-resistant PVC. Films and sheets applications, notably in stretch-shrink and protective agricultural films, benefit from improved barrier chemistry that extends shelf life and crop yields. Cable insulation retains a steady share yet must recalibrate formulations as legacy lead stabilizers exit the supply chain. Bottles and blister packs face down-sizing due to consumer anti-plastic campaigns, but find resilience in pharma and medical device packaging, where sterilization compatibility is critical. Profiles, hoses, and tubing ride construction and automotive demand cycles, respectively, providing a buffer against any abrupt slowdown in building starts.

By End-User Industry: Construction Lead Faces EV-Driven Reshoring

The construction sector held 70% of polyvinyl chloride market revenue in 2024, and is projected to grow at a 4.16% CAGR. High-efficiency window frames, roofing membranes, and large-diameter sewage pipes remain core, but incremental growth comes from code-driven retrofits emphasizing energy savings and climate resilience. Electric vehicles accelerate demand for lightweight dashboards and battery-enclosure liners where PVC competes favorably versus thermoplastic polyolefins on cost and tooling flexibility. Healthcare, with phthalate-free medical disposables, maintains momentum as hospitals adopt single-use protocols. Packaging volumes stagnate in mature economies, though medical blister demand partially compensates. Long-tail markets such as footwear and consumer goods provide steady albeit modest contributions to the polyvinyl chloride market.

Note: Segment shares of all individual segments available upon report purchase

Geography Analysis

Asia-Pacific preserved a commanding 60% share of the polyvinyl chloride market in 2024 and is forecasting a 4.38% CAGR to 2030. China’s decision to raise PVC import tariffs to 5.5% underscores a policy focus on utilizing its 30 million t/yr domestic nameplate capacity while encouraging technological upgrades in suspension and paste lines. India’s Jal Jeevan Mission funnels record capital into rural drinking-water networks, supporting large-bore PVC pipe demand alongside leak-detection infrastructure. Thailand’s feedstock diversification, enabled by US ethane imports from 2029, secures cost competitiveness for Southeast Asian converters. In parallel, regional producers invest in vinyl recycling plants that create certified post-consumer resin for export-compliant building products.

North America balances infrastructure-renewal spending with rising EV assembly investments. Shin-Etsu’s USD 1.25 billion Louisiana debottlenecking project and Formosa’s Baton Rouge expansion add over 800 kt/yr of new suspension capacity between 2025 and 2027. Environmental permitting remains strict, compelling operators to integrate brine mining and vinyl chloride monomer emissions-reduction technology. As state regulations phase out DEHP, US compounders expedite phthalate-free offerings, thereby raising value per tonne and cushioning the cyclical construction market.

Europe endures the world’s most stringent additive rules, driving capital toward calcium-zinc stabilizer production while accelerating R&D on recyclable mono-material profiles. VinylPlus exceeded its 2025 voluntary recycling target five years early, lifting the region’s recycled-content rate in PVC profiles above 20%. Meanwhile, regional producers operate at reduced run-rates when power prices spike, exporting PVC from US Gulf Coast plants to backfill European contract commitments. Beyond OECD markets, South America and Africa seek polymer self-sufficiency; Brazil’s sugar-cane-based ethylene project signifies a differentiated low-carbon route to PVC, while Nigeria evaluates chlor-alkali investments to reduce import reliance. Political and currency volatility remains a hurdle, yet infrastructure deficits present an undeniable addressable need for the polyvinyl chloride market.

Competitive Landscape

The polyvinyl chloride market is moderately concentrated, with the top five producers controlling approximately 43% of global capacity. Leaders employ vertical integration into chlorine, caustic soda, and ethylene dichloride to mitigate feedstock volatility. Shin-Etsu’s Louisiana build-out relies on abundant shale-ethane economics, allowing it to defend margins even amid Chinese oversupply. Meanwhile, Orbia’s Vinyl in Motion program turns post-consumer PVC into pipe and flooring feedstock, addressing brand-owner decarbonization targets while lowering resin acquisition costs.

Strategic acquisitions target stabilizers, plasticizers, and recycling technologies rather than raw PVC capacity. Westlake recently took a minority stake in a European calcium-zinc stabilizer supplier, ensuring additive security for its German and French compounding sites. Technology collaborations also rise; the Vinyl Institute’s partnership with Cyclyx sets a pathway to raise PVC post-consumer collection from 10% to 90% over the next decade, bolstering the supply of circular resin for American pipe manufacturers.

Competitive positioning hinges on regulatory readiness and specialty-grade portfolios. Companies able to certify products under global drinking-water and medical standards command premium pricing and long-term contracts. Conversely, producers concentrated solely in commodity suspension resin face margin erosion from Chinese export competition and rising compliance costs. The path forward thus favors diversified, vertically integrated players with proven end-market application expertise.

Polyvinyl Chloride (PVC) Industry Leaders

-

Shin-Etsu Chemical Co., Ltd.

-

Westlake Corporation

-

Formosa Plastics Corporation

-

Orbia

-

INEOS

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- May 2025: Orbia has introduced a comprehensive PVC recycling initiative under its Vinyl in Motion program. The company aims to repurpose PVC plastic for various applications by establishing a collection and processing infrastructure.

- July 2024: Formosa Plastics Corporation announced a significant expansion of its PVC plant in Baton Rouge, Louisiana, United States. This substantial investment is expected to enhance the facility's capacity, enabling it to better address the increasing demands of its customers.

Global Polyvinyl Chloride (PVC) Market Report Scope

Polyvinyl chloride (PVC) is a high-strength thermoplastic material widely used in various applications, such as pipes and fittings, films and sheets, wires and cables, bottles, profiles, hoses, and tubings. The market is segmented by product type, stabilizer type, application, end-user industry, and geography. The polyvinyl chloride (PVC) market is segmented by product type into rigid PVC, flexible PVC, low-smoke PVC, and chlorinated PVC. The polyvinyl chloride (PVC) market is segmented by stabilizer type, which contains calcium-based stabilizers, lead-based stabilizers, tin- and organotin-based stabilizers, and barium-based and other stabilizers. Applications, including pipes and fittings, films and sheets, wires and cables, bottles, profiles, hoses and tubings, and other applications, further segment the market. End-user industries, like building and construction, automotive, electrical and electronics, packaging, footwear, healthcare, and other end-user industries, segment the market. The report also covers the market size and forecast for the polyvinyl chloride market in 16 countries across major regions. The market sizing and forecast for each segment are given by volume (kiloton).

| By Product Type | Rigid PVC | Clear Rigid PVC | |

| Non-clear Rigid PVC | |||

| Flexible PVC | Clear Flexible PVC | ||

| Non-clear Flexible PVC | |||

| Low-Smoke PVC | |||

| Chlorinated PVC (CPVC) | |||

| By Manufacturing Process | Suspension PVC | ||

| Emulsion PVC | |||

| Bulk/Mass Polymerized PVC | |||

| By Stabilizer Type | Calcium-based Stabilizers (Ca-Zn Stabilizers) | ||

| Lead-based Stabilizers (Pb Stabilizers) | |||

| Tin and Organotin-based (Sn Stabilizers) | |||

| Barium-based and Other Stabilizer Types (Liquid Mixed Metals) | |||

| By Application | Pipes and Fittings | ||

| Films and Sheets | |||

| Wires and Cables | |||

| Bottles | |||

| Profiles, Hoses and Tubings | |||

| Other Applications | |||

| By End-User Industry | Building and Construction | ||

| Automotive and Transportation | |||

| Electrical and Electronics | |||

| Packaging | |||

| Footwear | |||

| Healthcare | |||

| Other End-User Industries | |||

| By Geography | Asia-Pacific | China | |

| India | |||

| Japan | |||

| South Korea | |||

| Rest of Asia-Pacific | |||

| North America | United States | ||

| Canada | |||

| Mexico | |||

| Europe | Germany | ||

| United Kingdom | |||

| Italy | |||

| France | |||

| Spain | |||

| Rest of Europe | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Middle East and Africa | Saudi Arabia | ||

| South Africa | |||

| Nigeria | |||

| Rest of Middle East and Africa | |||

By Product Type

| Rigid PVC | Clear Rigid PVC |

| Non-clear Rigid PVC | |

| Flexible PVC | Clear Flexible PVC |

| Non-clear Flexible PVC | |

| Low-Smoke PVC | |

| Chlorinated PVC (CPVC) |

By Manufacturing Process

| Suspension PVC |

| Emulsion PVC |

| Bulk/Mass Polymerized PVC |

By Stabilizer Type

| Calcium-based Stabilizers (Ca-Zn Stabilizers) |

| Lead-based Stabilizers (Pb Stabilizers) |

| Tin and Organotin-based (Sn Stabilizers) |

| Barium-based and Other Stabilizer Types (Liquid Mixed Metals) |

By Application

| Pipes and Fittings |

| Films and Sheets |

| Wires and Cables |

| Bottles |

| Profiles, Hoses and Tubings |

| Other Applications |

By End-User Industry

| Building and Construction |

| Automotive and Transportation |

| Electrical and Electronics |

| Packaging |

| Footwear |

| Healthcare |

| Other End-User Industries |

By Geography

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| South Africa | |

| Nigeria | |

| Rest of Middle East and Africa |

Need A Different Region or Segment?

Customize Now

Key Questions Answered in the Report

What is the current polyvinyl chloride market size?

The polyvinyl chloride market size reached 53.82 million tons in 2025 and is projected to climb to 65.48 million tons by 2030 at a 4.0% CAGR.

Which region dominates the polyvinyl chloride market?

Asia-Pacific leads with 60% of global consumption, driven by large-scale infrastructure programs and local production capacity.

Why is CPVC growing faster than standard PVC?

CPVC tolerates higher temperatures and aggressive water conditions, making it ideal for hot-and-cold potable systems and thus sustaining a 4.80% CAGR through 2030.

How are regulations affecting PVC additives?

New EU and Indian limits on lead stabilizers and global moves toward phthalate-free plasticizers are accelerating adoption of calcium-zinc and DOTP systems.

What role does recycling play in the polyvinyl chloride industry?

Recycling initiatives such as Orbia’s Vinyl in Motion and the Vinyl Institute–Cyclyx partnership aim to convert post-consumer PVC into new pipes and building products, supporting circular-economy targets while securing resin supply.

Page last updated on: July 1, 2025