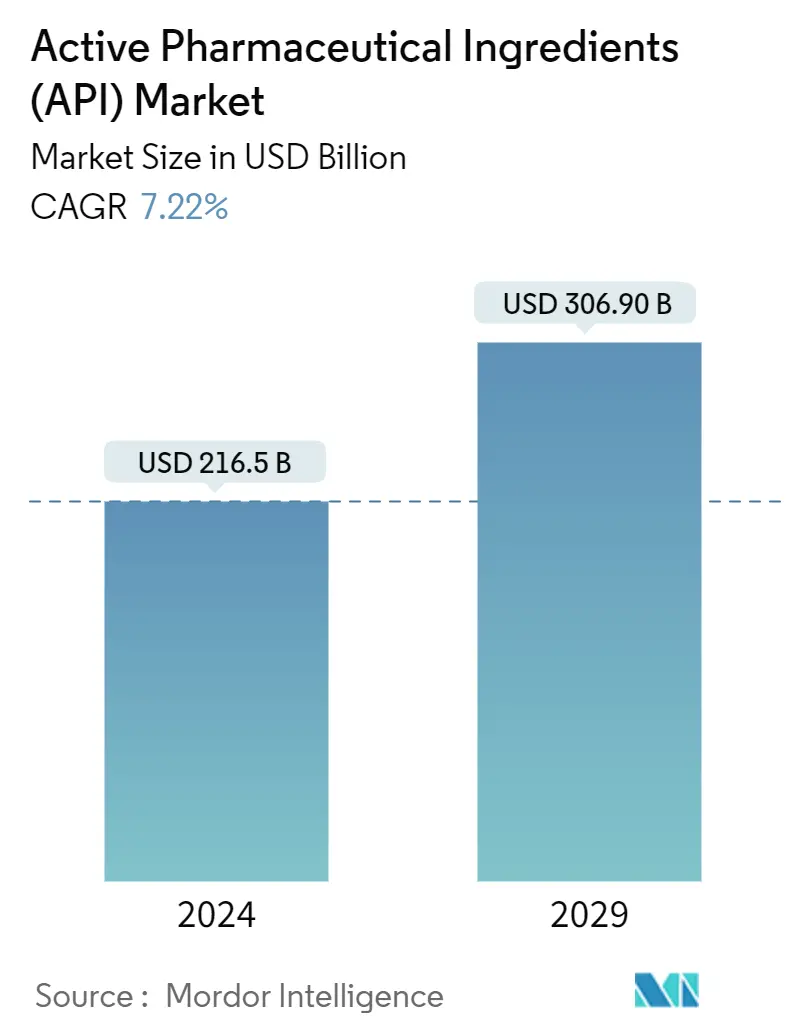

Active Pharmaceutical Ingredients (API) Market Size

| Study Period | 2021-2029 |

| Market Size (2024) | USD 216.5 Billion |

| Market Size (2029) | USD 306.90 Billion |

| CAGR (2024 - 2029) | 7.22 % |

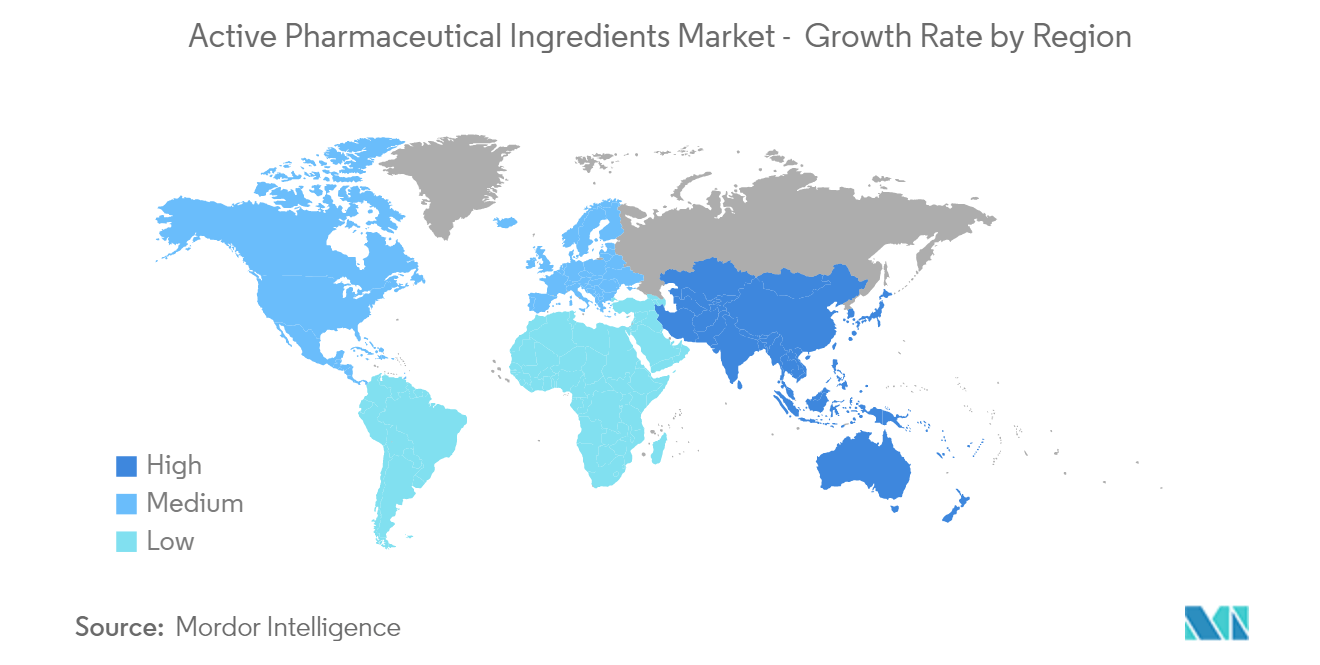

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

Major Players

*Disclaimer: Major Players sorted in no particular order |

Need a report that reflects how COVID-19 has impacted this market and its growth?

Active Pharmaceutical Ingredients (API) Market Analysis

The Active Pharmaceutical Ingredients Market size is estimated at USD 216.5 billion in 2024, and is expected to reach USD 306.90 billion by 2029, growing at a CAGR of 7.22% during the forecast period (2024-2029).

Factors such as the increasing prevalence of infectious, genetic, cardiovascular, and other chronic disorders, increasing adoption of biologics and biosimilars, rising prevalence of cancer, and growing sophistication in oncology drug research are expected to boost the market growth over the forecast period.

The increasing prevalence and burden of chronic diseases, infectious diseases, and genetic disorders worldwide are driving the demand for effective and safe drugs, which in turn increases the demand for active pharmaceutical ingredients across the globe. For instance, according to the 2022 statistics published by the International Diabetes Federation (IDF), diabetic cases are projected to reach 643 million and 784 million by 2030 and 2045, respectively. Additionally, in December 2023, the Australian Bureau of Statistics reported that around 1.3 million people in Australia had diabetes in 2022, which accounted for 5.3% of the population. Therefore, high blood sugar caused by diabetes can damage the nerves that control the heart and blood vessels, leading to a variety of cardiovascular diseases like coronary artery disease and stroke, which can narrow the arteries and necessitate the administration of drugs, propelling the growth of the API market.

Additionally, the increasing development and clinical trials of biosimilar and biologic drugs for new therapeutic classes urge companies to adopt strategic initiatives for manufacturing and developing APIs, which is expected to contribute to market growth. For instance, in September 2022, CuraTeQ Biologics, a wholly owned subsidiary of Aurobindo Pharma, invested approximately INR 300 (USD 3.82) crore in the capacity expansion of biologics manufacturing facilities. In addition, the company received approval to enter contract manufacturing operations for biologicals. Similarly, in September 2022, Novartis invested USD 300 million to increase its production and development capabilities for biological drugs. Such investments in improving biologic manufacturing and rising biologic approvals are anticipated to increase its adoption, which in turn is expected to increase the demand for APIs for developing drugs globally.

Therefore, owing to the high burden of diabetes among the population and growing company activities to increase the development of biologics and biosimilar drugs, the studied market is expected to grow over the forecast period. However, the drug price control policies across various countries, high competition between API manufacturers, and stringent regulation are expected to impede the growth of the active pharmaceutical ingredients market over the forecast period.

Active Pharmaceutical Ingredients (API) Market Trends

Oncology Segment is Expected to Register Significant Growth Over the Forecast Period

The growing burden of cancer cases across the globe is one of the crucial health concerns witnessed by many countries. The incidence of cancer rises dramatically with age, which raises the demand for effective therapeutics.

The oncology segment is expected to witness significant growth in the active pharmaceutical ingredients market over the forecast period owing to factors such as the rising burden of cancer cases and raising awareness towards treating the early-onset cancer epidemic. For instance, in March 2023, another study published in the Indian Journal of Medical Research, the prevalence of cancer in India is expected to rise from 1.46 million in 2022 to 1.57 million by 2025. This data shows a rapid increase in the incidence of cancer cases in the country. Over the forecast period, the incidence of cancer will further increase, thus raising the demand for oncology drugs that need API for drug formulation. Hence, the market is expecting a significant impact over the forecast period.

Furthermore, the increasing focus of companies on adopting key strategic activities such as collaborations, agreements, and partnerships is expected to accelerate the development of novel cancer drugs. For instance, in October 2022, Mendus AB entered a deal to enable the technology transfer to manufacture the company's lead development program DCP-001 with Minaris Regenerative Medicine GmbH. DCP-001 is being evaluated in the ADVANCE II Phase 2 clinical trial to prevent cases of tumor recurrence in Acute Myeloid Leukemia (AML) and in the ALISON Phase 1 clinical trial in ovarian cancer.

Similarly, in October 2022, GenScript ProBio, a global CDMO, and GeneCraft entered a strategic partnership MOU concerning the development and production of new drugs needed for RX001. GenScript ProBio and GeneCraft are signing a contract for plasmid and AAV development and production of new drug candidate Pan-KRAS non-small cell lung cancer anti-cancer gene therapy (RX001).

Moreover, the increasing investments to accelerate the production of APIs are also expected to contribute to segment growth over the forecast period. For instance, in July 2022, NovasepPharmaZell Group invested EUR 7.3 (USD 7.6) million for its Mourenx site (southwestern France). This new industrial tool will support the growth of the Mourenx site and sustain the growing demand to produce active pharmaceutical ingredients (APIs), particularly the highly potent drugs (HPAPIs) used to treat cancer.

Hence, owing to the growing incidence of cancer and its risk factors, new company initiatives toward cancer drugs, and further research and development activities, the studied segment is expected to grow over the forecast period.

North America is Expected to Hold Significant Market Share Over the Forecast Period

North America is anticipated to hold a significant market share over the forecast period owing to factors such as the prevalence of chronic diseases such as cancer, diabetes, cardiovascular and neurological diseases coupled with the geriatric population. In addition, the high healthcare expenditures and the presence of key market players in the region are also anticipated to boost market growth over the forecast period.

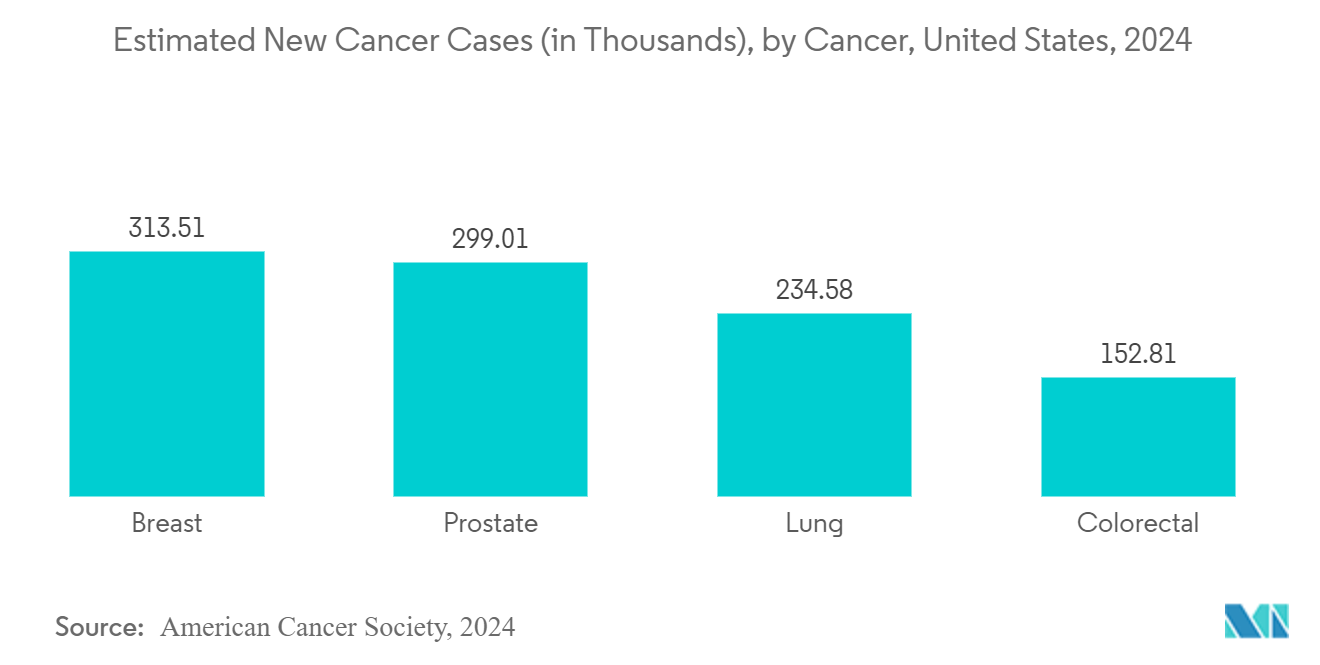

The rising burden of chronic diseases is the key factor driving the demand for effective drugs for treatment, hence expected to fuel the market growth. For instance, according to 2024 statistics published by the American Cancer Society, about 2,001,140 new cancer cases are expected to be diagnosed in the United States in 2024, including 353,820 digestive system cancer, 313,510 breast cancer, and 252,950 respiratory-related cancer.

Similarly, as per the Canadian Institute for Health Information data published in July 2022, about 2.4 million Canadians have heart disease in 2022. This fuels the demand for APIs for manufacturing cancer and cardiovascular drugs, which is anticipated to propel the market growth in the North American region.

Furthermore, in February 2023, the Government of Canada issued Good manufacturing practices guidelines for active pharmaceutical ingredients (GUI-0104) for people who work with Active Pharmaceutical Ingredients (APIs) and their intermediates to understand and comply with Part C, Division 2 of the Food and Drug Regulations (the Regulations), which is about Good Manufacturing Practices (GMP). This guide applies to the fabricators, packagers/labelers (including re-packagers/re-labelers), testers, importers, distributors, and wholesalers. Such a government initiative is expected to increase the requirement for finished products and boost the API market over the forecast period.

Moreover, increasing company activities to increase API production by expanding manufacturing facilities is also expected to bolster market growth. For instance, in January 2023, Eurofins announced that it relocated and expanded its API development laboratories by moving to a new space in Ontario, Canada. Similarly, in May 2022, Piramal Pharma announced that a new active pharmaceutical ingredient (API) plant at the company's site in Aurora, Ontario, has come online and completed its initial production runs.

Therefore, the studied market is expected to grow over the forecast period due to the rising prevalence of cancer and cardiovascular diseases, increasing government initiatives, and growing company manufacturing facility expansion activities.

Active Pharmaceutical Ingredients (API) Industry Overview

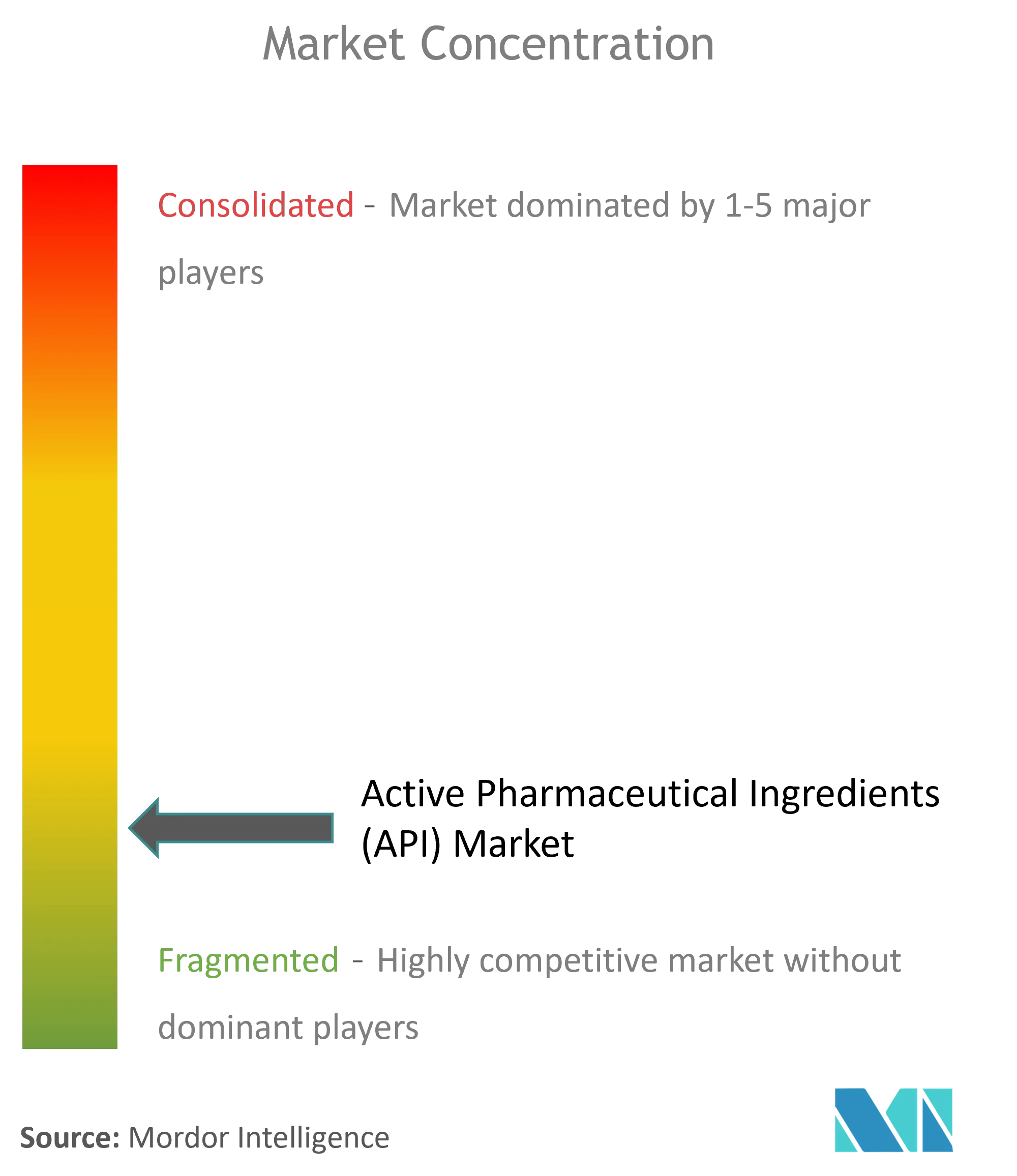

The active pharmaceutical ingredients (API) market is fragmented in nature due to the presence of various companies operating globally as well as regionally. The competitive landscape includes an analysis of a few international as well as local companies that hold market shares and are well-known, including Pfizer Inc., BASF SE, Viatris Inc., Merck KGaA, and Teva Pharmaceutical Industries Ltd., among others.

Active Pharmaceutical Ingredients (API) Market Leaders

Teva Pharmaceutical Industries Ltd

Pfizer Inc.

Merck KGaA

BASF SE

Viatris, Inc.

*Disclaimer: Major Players sorted in no particular order

Active Pharmaceutical Ingredients (API) Market News

- April 2023: Aurobindo Pharma approved the transfer of two API units (Unit V and XVII) to its wholly-owned subsidiary Apitoria Pharma Private Limited.

- January 2023: Novartis sold its active pharmaceutical ingredient (API) manufacturing facility in Ringaskiddy, Ireland, to Sterling Pharma Solutions. Under the terms of the agreement, Novartis continues to manufacture several APIs for cardiovascular, immunology, and oncology medicines at Ringaskiddy.

Active Pharmaceutical Ingredients (API) Market Report - Table of Contents

1. INTRODUCTION

1.1 Study Assumptions and Market Definition

1.2 Scope of the Study

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET DYNAMICS

4.1 Market Overview

4.2 Market Drivers

4.2.1 Increasing Prevalence of Infectious, Genetic, Cardiovascular, and Other Chronic Disorders

4.2.2 Increasing Adoption of Biologicals and Biosimilars

4.2.3 Rising Prevalence of Cancer and Increasing Sophistication in Oncology Drug Research

4.3 Market Restraints

4.3.1 Drug Price Control Policies across Various Countries

4.3.2 High Competition between API Manufacturers

4.3.3 Stringent Regulations

4.4 Industry Attractiveness - Porter's Five Forces Analysis

4.4.1 Threat of New Entrants

4.4.2 Bargaining Power of Buyers/Consumers

4.4.3 Bargaining Power of Suppliers

4.4.4 Threat of Substitute Products

4.4.5 Intensity of Competitive Rivalry

5. MARKET SEGMENTATION (Market Size by Value - USD)

5.1 By Business Mode

5.1.1 Captive API

5.1.2 Merchant API

5.2 By Synthesis Type

5.2.1 Synthetic

5.2.2 Biotech

5.3 By Type of Drug

5.3.1 Generic

5.3.2 Branded

5.4 By Application

5.4.1 Cardiology

5.4.2 Pulmonology

5.4.3 Oncology

5.4.4 Ophthalmology

5.4.5 Neurology

5.4.6 Orthopedic

5.4.7 Other Applications

5.5 Geography

5.5.1 North America

5.5.1.1 United States

5.5.1.2 Canada

5.5.1.3 Mexico

5.5.2 Europe

5.5.2.1 Germany

5.5.2.2 United Kingdom

5.5.2.3 France

5.5.2.4 Italy

5.5.2.5 Spain

5.5.2.6 Rest of Europe

5.5.3 Asia-Pacific

5.5.3.1 China

5.5.3.2 Japan

5.5.3.3 India

5.5.3.4 Australia

5.5.3.5 South Korea

5.5.3.6 Rest of Asia-Pacific

5.5.4 Middle East and Africa

5.5.4.1 GCC

5.5.4.2 South Africa

5.5.4.3 Rest of Middle East and Africa

5.5.5 South America

5.5.5.1 Brazil

5.5.5.2 Argentina

5.5.5.3 Rest of South America

6. COMPETITIVE LANDSCAPE

6.1 Company Profiles

6.1.1 Aurobindo Pharma

6.1.2 Teva Pharmaceutical Industries Ltd

6.1.3 Pfizer Inc.

6.1.4 Novartis AG

6.1.5 BASF SE

6.1.6 Merck KGaA

6.1.7 Dr. Reddy's Laboratories Ltd

6.1.8 Lupin Ltd

6.1.9 Viatris Inc.

6.1.10 Sun Pharmaceutical Industries Ltd

- *List Not Exhaustive

7. MARKET OPPORTUNITIES AND FUTURE TRENDS

Active Pharmaceutical Ingredients (API) Industry Segmentation

As per the scope of the report, an active pharmaceutical ingredient (API) is a part of any drug that produces its effects. Some drugs, such as combination therapies, have multiple active ingredients to treat different symptoms or act in different ways.

The active pharmaceutical ingredients (API) market is segmented by business mode into captive API and merchant API, by synthesis type, the market is bifurcated into synthetic and biotech, based on the type of drug the market is segregatted into generic and branded, based on the application the market is classified into cardiology, pulmonology, oncology, ophthalmology, neurology, orthopedic, and other applications, and by geography the market is divided inot North America, Europe, Asia-Pacific, Middle East and Africa, and South America. The report also covers the estimated market sizes and trends for 17 different countries across major regions globally. The report offers the value (in USD) for the above segments.

| By Business Mode | |

| Captive API | |

| Merchant API |

| By Synthesis Type | |

| Synthetic | |

| Biotech |

| By Type of Drug | |

| Generic | |

| Branded |

| By Application | |

| Cardiology | |

| Pulmonology | |

| Oncology | |

| Ophthalmology | |

| Neurology | |

| Orthopedic | |

| Other Applications |

| Geography | ||||||||

| ||||||||

| ||||||||

| ||||||||

| ||||||||

|

Active Pharmaceutical Ingredients (API) Market Research FAQs

How big is the Active Pharmaceutical Ingredients Market?

The Active Pharmaceutical Ingredients Market size is expected to reach USD 216.5 billion in 2024 and grow at a CAGR of 7.22% to reach USD 306.90 billion by 2029.

What is the current Active Pharmaceutical Ingredients Market size?

In 2024, the Active Pharmaceutical Ingredients Market size is expected to reach USD 216.5 billion.

Who are the key players in Active Pharmaceutical Ingredients Market?

Teva Pharmaceutical Industries Ltd, Pfizer Inc., Merck KGaA, BASF SE and Viatris, Inc. are the major companies operating in the Active Pharmaceutical Ingredients Market.

Which is the fastest growing region in Active Pharmaceutical Ingredients Market?

Asia-Pacific is estimated to grow at the highest CAGR over the forecast period (2024-2029).

Which region has the biggest share in Active Pharmaceutical Ingredients Market?

In 2024, the North America accounts for the largest market share in Active Pharmaceutical Ingredients Market.

What years does this Active Pharmaceutical Ingredients Market cover, and what was the market size in 2023?

In 2023, the Active Pharmaceutical Ingredients Market size was estimated at USD 200.87 billion. The report covers the Active Pharmaceutical Ingredients Market historical market size for years: 2021, 2022 and 2023. The report also forecasts the Active Pharmaceutical Ingredients Market size for years: 2024, 2025, 2026, 2027, 2028 and 2029.

Which segment is expected to witness significant growth in the Active Pharmaceutical Ingredients Market?

The oncology segment is expected to witness significant growth in the Active Pharmaceutical Ingredients Market over the forecast period.

What are the major restraints in the Active Pharmaceutical Ingredients Market?

The major restraints in the Active Pharmaceutical Ingredients Market are due to a) Drug price control policies across various countries b) High competition between API manufacturers.

API Industry Report

This comprehensive report offers a deep dive into the active pharmaceuticals ingredients industry, providing a detailed analysis of key market drivers and market segments. Mordor Intelligence offers customization based on your specific interests, including: 1. Products type: (Cytokines, Hormones) 2. Drug Type: Over-the-Counter (OTC) Drugs 3. Type (Innovative Active Pharmaceutical Ingredients, Generic Innovative Active Pharmaceutical Ingredients)